The debate between gold and real estate as investment vehicles is nothing new. But in 2026, the stakes are higher and the decision is more nuanced than ever. With global markets recalibrating after prolonged monetary tightening, you’re no longer just looking for a store of value. You’re demanding yield, flexibility, and asymmetric upside.

Both gold and real estate are tangible, inflation-resistant assets. But they function on entirely different investment principles, and confusing the two can cost you serious capital.

Gold offers purity. It’s inert, universally recognized, and thrives during systemic distress. It demands no maintenance, no tenants, no leverage, and no regional expertise. For that reason, it has earned its place as a hedge. Not a wealth builder, but a capital preserver.

Real estate is a different animal entirely. It generates income, appreciates through multiple economic levers, and can be controlled, improved, or leveraged to your advantage. It rewards active management and time in the market, not timing the market. Think of it not just as protection against inflation, but as a tool for long-term equity growth, tax optimization, and cash flow engineering.

What follows is a structural breakdown of the key differences between gold and real estate from your perspective as an investor. Not philosophical. Practical. We’re talking entry points, return composition, taxation, costs, and risk exposure.

The goal isn’t to crown a winner. It’s to define which asset serves which purpose, and for which type of investor you happen to be.

Table of Contents

What Is Gold to Real Estate Ratio

The Gold to Real Estate Ratio is a comparative metric that tells you how many ounces of gold it takes to purchase a unit of real estate, typically measured against the average home price in a given region.

And it’s not just a curiosity metric. Asset allocators, economists, and contrarian investors use it as a macro valuation tool to identify relative overvaluation or undervaluation between asset classes.

At its core, the ratio works much like the Gold-to-Dow ratio. It reveals capital flow trends between monetary assets like gold and productive assets like real estate. When the ratio is high, real estate is relatively expensive compared to gold. When it’s low, gold looks expensive relative to property. Smart investors watch this ratio to determine not just where value sits, but where capital is moving.

How It’s Used

- Macro timing: Some investors use it to determine whether to rotate between gold and property. If gold becomes historically undervalued relative to housing, it may signal that real estate is overheated.

- Hedging strategy: Family offices sometimes track this ratio to structure barbell portfolios—allocating to whichever side offers more upside with less relative risk.

- Historical context: In 1980, during peak gold prices and housing stagnation, you could buy a median U.S. home with just 100 ounces of gold. Today, it may take four to five times as much, depending on location.

Why It Matters in 2026

In a year where both gold and real estate are being repriced against tight monetary policy and sticky inflation, the ratio helps you identify entry asymmetry. If gold spikes during a risk-off environment while real estate softens due to rate pressures, the ratio tilts and opens a window for real estate acquisition at more favorable valuation multiples relative to hard-money alternatives. That’s a window worth watching.

Gold vs Real Estate: Entry Point

The barrier to entry in any asset class defines who can participate and at what scale. When you’re comparing gold and real estate, the entry dynamic isn’t just about initial capital. It’s about access, liquidity, friction costs, and how flexibly you can deploy your money.

Gold Entry: Low Friction, High Liquidity, Limited Leverage

Gold is accessible to virtually any investor. You can purchase it in forms ranging from physical bullion, think 1g to 1kg bars, to ETFs like GLD or IAU, to tokenized gold on blockchain networks.

That modularity makes it attractive whether you’re a small-scale investor just getting started or an institutional allocator moving serious capital.

- Minimum investment: <$100 via ETFs or fractional platforms

- Transaction time: Minutes (digital), 1–3 days (physical)

- Liquidity: Extremely high—global 24/7 markets

- Leverage potential: Minimal to none (unless trading futures, which introduces risk)

Gold also benefits from low transaction friction. You don’t need inspections, agents, or escrow. No title to transfer, no underwriting, no appraisal bottleneck. You buy it, you own it.

The downside? You can’t force appreciation. Gold enters your portfolio as-is. What you pay is what you own, with zero control over intrinsic value creation.

Real Estate Entry: High Friction, High Control, Strategic Leverage

Real estate requires more capital, more paperwork, and more due diligence. But what you get in return is real cash flow, control over asset performance, and long-term leverage advantages that gold simply can’t offer.

Yes, entry is more complex. But the payoff is rooted in multiple return drivers, including appreciation, depreciation, rental income, and equity build.

- Minimum investment: $10,000–$25,000 for REITs or crowdfunding; $100,000+ for direct ownership

- Transaction time: 30–90 days average (varies by deal type)

- Liquidity: Low (unless through REITs or securitized platforms)

- Leverage potential: High—LTVs of 60%–80% common with fixed-rate debt

And the ability to use leverage is what makes the entry hurdle worth climbing.

A $250,000 property acquired with 25% down lets you control the entire asset for $62,500 out of pocket, multiplying your exposure and amplifying ROI if managed correctly. Gold offers no such multiplier effect. It’s a one-to-one asset, full stop.

Gold is plug-and-play. Real estate is strategic capital deployment. It requires upfront planning, legal diligence, and cash reserves. But in return, you get more tools to scale, more control, and more ways to engineer value. If you’re curious about what types of real estate give you the best leverage on that deployment, the answer depends heavily on your timeline and risk appetite.

For investors capable of tackling the entry complexity, whether through direct purchase, partnerships, or syndications, real estate’s payoff extends well beyond price speculation. It becomes an engine for equity growth and financial engineering.

Gold vs Real Estate: Historical Performance

To figure out which asset delivers better long-term value, you need to go beyond anecdotes and study multi-decade performance data. Historical ROI is a function of not just asset appreciation, but also volatility, reinvestment opportunities, inflation correlation, and income contribution.

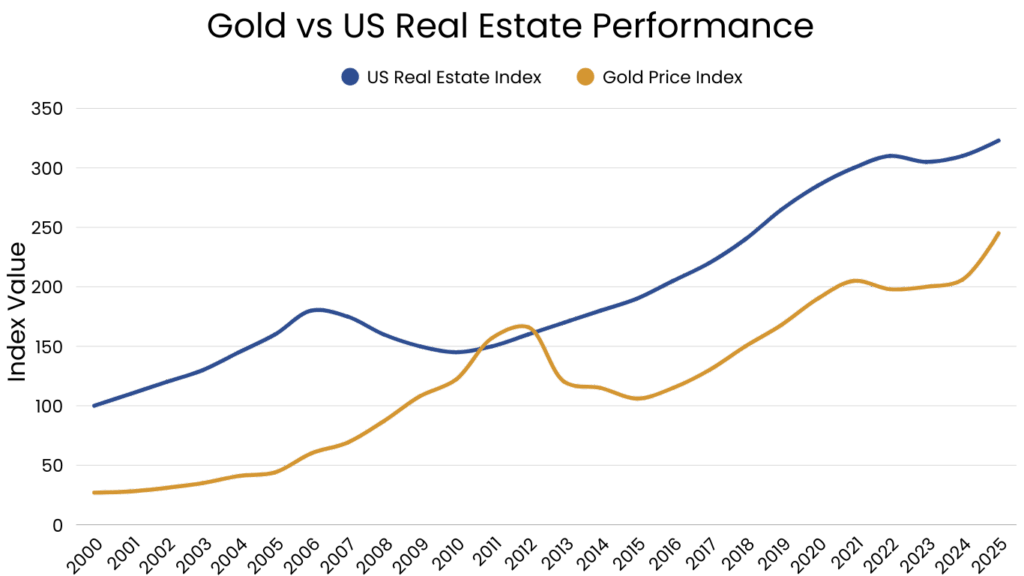

And when you look at the numbers honestly, U.S. real estate has outperformed on both an absolute and risk-adjusted basis across most economic cycles, even as gold has excelled as a hedge during systemic crises.

Gold

Gold’s performance is episodic. It shines in environments of monetary debasement, geopolitical shocks, and declining real yields. But it tends to underperform during expansionary or high-growth periods.

From 2000 to 2011, gold surged from $272 to over $1,800 per ounce, a 562% price gain largely driven by post-dot-com deflation fears, the 2008 financial crisis, and early quantitative easing policy.

But from 2012 to 2018, while equities and real estate rebounded sharply, gold drifted sideways, returning only around 1.3% CAGR during that six-year stretch. Even with the 2020 to 2022 inflation spike factored in, its overall 20-year CAGR from 2003 to 2023 sits around 6.9%, with high annual volatility of roughly 15% and no income component to stabilize returns. Bloomberg’s commodities data paints this picture clearly for anyone tracking gold’s long-term price behavior.

U.S. Real Estate

Real estate in the U.S. has delivered consistent, inflation-linked compounding for over a century. The Federal Housing Finance Agency reports a 6.3% average annual home price increase nationally since 1991.

From 2000 to 2023, the Case-Shiller U.S. National Home Price Index climbed from 100 to over 310, a 210% total price increase or roughly 5.5% annualized, and that’s before you factor in rental income or tax benefits.

What separates real estate from gold is its multi-dimensional return structure. When you fold in rental yield, mortgage principal reduction, and depreciation, the effective ROI on leveraged real estate climbs into the 10% to 20% range annually.

For example:

- Net operating income (NOI) growth: Residential landlords in high-growth MSAs (e.g., Austin, Phoenix, Tampa) saw NOI increases of 25–40% between 2019 and 2023, significantly outpacing CPI and gold.

- Multifamily cap rates: Even with rising rates, Class B and C assets in the Midwest and Southeast still offer 5.5%–7% cap rates, with value-add projects yielding IRRs in the 12%–18% range, according to CBRE’s 2024 multifamily report.

- Institutional real estate (NCREIF Property Index): Delivered a 10-year annualized return of 8.1% through Q3 2023, beating gold by over 140 basis points, with less volatility and far greater income generation.

Resilience Through Crisis

The 2008 crash gets used as a knock against real estate, but context matters. Yes, housing declined sharply, with national prices falling around 27% from peak to trough. But within five years, most major markets had rebounded, and investors who bought during the correction often saw double-digit annual returns over the following decade.

Gold surged during the same period, but unlike real estate, it didn’t create residual value. Once the crisis passed, gold retracted, while real estate cash flows grew and appreciated.

Real estate recovers and compounds. Gold reacts and plateaus.

Gold vs Real Estate: Tax Treatment

Both gold and real estate are classified as tangible assets, but the IRS treats them very differently, and understanding these distinctions is essential for proper portfolio planning. The tax implications tied to gains, losses, depreciation, and ownership structure vary enough that they can meaningfully shift the net return of each asset class.

Gold: Treated as a Collectible Under Federal Tax Code

In the U.S., physical gold including coins and bullion is taxed as a collectible under IRS rules. This classification directly impacts long-term capital gains rates for investors holding gold for more than a year.

- Short-term capital gains (held for less than 12 months) are taxed as ordinary income, at rates up to 37% depending on the investor’s bracket.

- Long-term gains on physical gold or gold-backed ETFs like GLD are subject to a maximum federal rate of 28%, higher than the typical long-term capital gains rate of 15%–20% applied to stocks and real estate.

- Gold ETFs structured as grantor trusts (e.g., GLD) may pass through phantom gains or taxable distributions, even without a sale event.

- Gold does not qualify for depreciation or deferral mechanisms like a 1031 exchange.

- Inherited gold assets receive a step-up in cost basis, aligning with standard IRS treatment for inherited property.

Real Estate: Classified as Investment Property with Tax Offsets

Real estate is taxed as investment property and comes with a broader set of deductions, deferral opportunities, and income treatment options. The rules apply differently depending on whether you’re holding rental property, a primary residence, or commercial assets.

- Rental income is taxed as ordinary income, though operating expenses (property taxes, maintenance, insurance, etc.) are fully deductible.

- Investors may claim depreciation on the property over 27.5 years (residential) or 39 years (commercial), reducing taxable rental income.

- When a property is sold, capital gains tax applies—15% or 20% federally depending on income, plus a possible 3.8% net investment income tax.

- Depreciation recapture is taxed separately at a maximum of 25%.

- Investors can defer capital gains via a 1031 exchange, by reinvesting into a “like-kind” property within specific IRS timelines.

- Real estate assets passed to heirs receive a step-up in basis, eliminating the accrued capital gain for tax purposes.

Key Differences Worth Knowing

Gold_vs_Real_Estate_Tax_Comparison_Vertical_2025.csv

Both gold and real estate are subject to federal taxes and potentially state-level taxes as well. But the structure and flexibility of that tax treatment differ quite a bit, especially for investors planning around income, legacy, or reinvestment strategies. You can dig deeper into how different real estate types carry different tax advantages depending on your goals.

Whatever your allocation looks like, consult a qualified tax advisor to assess how each asset aligns with your personal income profile and long-term planning goals.

Gold vs Real Estate: Ongoing Costs

Beyond acquisition price and tax treatment, ongoing ownership costs play a critical role in determining the net performance of any investment.

Both gold and real estate are considered hold assets rather than trade assets. But their maintenance expenses, storage logistics, and administrative burdens are worlds apart.

And those ongoing costs directly affect your net yield, your liquidity management, and how long you can comfortably hold the position.

Gold

Gold’s appeal partially comes from its simplicity. Once you’ve acquired it, recurring costs are minimal, especially when held in physical form.

- Storage Costs: Physical gold requires secure storage. High-net-worth investors often use private vaults or bank safety deposit boxes, costing between 0.5% to 1% annually based on total value and security tier.

- Insurance: To fully protect physical gold, especially in private storage, insurance is typically purchased separately. Annual premiums range from 0.3% to 1% of insured value, depending on policy specifics and provider.

- Management Fees (ETFs): Gold-backed ETFs like GLD carry annual expense ratios around 0.40%, which are deducted from fund assets rather than billed directly. These costs are invisible to most retail investors but accumulate over long holding periods.

- No Operational Costs: Gold doesn’t generate income or require active oversight—there are no tenants, repairs, or compliance obligations.

Gold’s ongoing cost structure is passive and predictable, which makes it attractive if you’re seeking simplicity and low operational engagement.

The trade-off is clear though. Low cost, no cash flow.

Real Estate

Real estate ownership, especially direct ownership, comes with a stack of recurring obligations that vary based on asset type, location, and scale. These costs are manageable and in many cases offset by rental income, but they do require attention and strategic planning.

- Property Taxes: Typically 0.7% to 2.5% of assessed value annually, depending on jurisdiction. In high-tax states like New Jersey or Illinois, this cost can materially impact cash flow.

- Insurance: Required by lenders and strongly advised for all owners. Annual costs range from 0.2% to 0.5% of property value, depending on location, coverage, and asset class.

- Maintenance and CapEx: General rule of thumb is 1% of property value annually for maintenance, not including major renovations or capital expenditures.

- Property Management Fees: If outsourced, fees range from 6% to 10% of monthly rent, plus leasing commissions and renewal charges.

- HOA or Condo Fees (where applicable): These vary widely, but can range from $200/month to $1,000+/month for high-end units or common-area intensive properties.

- Vacancy and Turnover Costs: Holding costs accrue when units are unoccupied. Average annual vacancy across U.S. multifamily was 5.7% in 2023, according to CBRE.

- Compliance and Legal: Local rental laws, zoning codes, and tenant protections require ongoing attention, especially in rent-controlled markets.

Real estate is not a passive asset unless you’re running it through professional management or accessing it through REITs. That said, many of these costs are deductible against rental income, and with optimized operations, strategic leasing, or smart tax planning, you can recover or outperform these expenses.

Cost Summary:

Gold_vs_Real_Estate_Cost_Comparison

Gold vs Real Estate: Risk

When you compare the risk profiles of gold and real estate, the difference isn’t just about scale. It’s about structure. Gold presents a deceptively clean exposure. No tenants, no lenders, no maintenance schedules. It sits, it waits, and its value is dictated entirely by external forces like monetary policy, macro sentiment, and risk-off capital flows.

That simplicity is part of its appeal. But it’s also its limitation.

Historically, gold has shown considerable volatility for a so-called defensive asset, with standard deviation levels that mirror equities during systemic stress. Its drawdowns can be sharp and prolonged. Between 2011 and 2015, gold lost over 40% of its value and didn’t recover for nearly a decade. Reuters has tracked gold’s price swings through multiple cycles, and the pattern is consistent.

No income streams soften that blow. Just pure price exposure, fully dependent on market conditions beyond your control. And while gold is often labeled an inflation hedge, its correlation to actual inflation data is inconsistent. It reacts more reliably to declining real yields and dollar weakness than to CPI itself.

Real estate operates differently. The risk is hands-on, multi-dimensional, and localized, but it’s controllable. Tenants can default, repairs cost real money, vacancies hit your yield. But you’re not a spectator.

Through asset management, financing strategy, lease structuring, and renovations, you can change the outcome. You can refinance when rates drop. You can re-tenant when markets shift. You can improve net operating income through deliberate execution.

These risks don’t vanish. But they can be mitigated and in many cases turned into returns.

The trade-off is liquidity. Real estate doesn’t sell overnight. You can’t tap your equity with a mouse click. Exiting a position can take months, and timing matters. Leverage adds pressure too. Misaligned debt terms during a downturn can force decisions earlier than you’d planned. Regulatory exposure, especially in urban or rent-controlled environments, can limit rent growth or introduce compliance costs. That’s worth understanding before you commit, particularly if you’re looking at markets increasingly exposed to climate-related risk.

But unlike gold, real estate risk comes with levers. It can be engineered, timed, deferred, hedged. Gold offers none of that. When it performs, it’s because markets panic or currencies erode. When it doesn’t, you wait. With real estate, performance can be created, sometimes regardless of the macro backdrop.

The risk with gold is external and uncontrollable. The risk with real estate is operational, but it comes with a toolkit. Which one you prefer depends on whether you want simplicity and surrender, or complexity and control.

What Type of Investors Choose Each Asset

Investor psychology drives allocation as much as return projections. The asset you choose, gold or real estate, often reveals more about your risk tolerance, liquidity needs, and strategic intent than it does about your ability to time markets.

Gold attracts investors who prioritize preservation over production. These are typically allocators who value simplicity, immediate liquidity, and low-maintenance security. It appeals to those with a distrust of financial systems, a desire for wealth insurance, or a need to park capital defensively during uncertainty.

Central banks hold gold for a reason. It’s liquid, borderless, and outside of counterparty risk. For you as an individual investor, it plays the same role, a passive anchor that doesn’t rely on GDP growth or tenant demand. You don’t have to manage gold.

You don’t have to think about it. That’s exactly the point.

Real estate, by contrast, is a magnet for investors who want control, cash flow, and the ability to manufacture returns. It draws in entrepreneurs, builders, and long-range planners who see capital not as something to be protected at all costs, but as something to be put to work. If you’re thinking about how to structure a portfolio around a core productive asset, real estate fits that satellite-builder role naturally.

The appeal isn’t just appreciation. It’s leverage, depreciation, and the compounding effect of reinvested income.

Real estate lets you add value. It lets you force outcomes.

It favors investors willing to engage with the asset, solve problems, and extract performance through execution. For these investors, the payoff isn’t just financial. It’s strategic autonomy. And according to the Financial Times, high-net-worth investors are increasingly tilting toward income-generating real assets precisely for this reason.

Some investors hold both, using gold as a macro hedge and real estate as an income generator. But in practice, those who overweight gold are often seeking insurance. Those who overweight real estate are building equity engines. One preserves, the other scales.

Choosing between them isn’t just about expected return. It’s about how active you want to be in creating that return, and how much risk you want to own versus delegate entirely to the market.

FAQ

Is gold or real estate a better investment in 2025?

Real estate offers better long-term growth through income, leverage, and tax efficiency. Gold is better for short-term capital preservation and macro hedging.

Which has better returns: gold or real estate?

Historically, real estate outperforms gold on a total return basis. Real estate combines appreciation, rental income, and tax benefits, while gold relies only on price movement.

Is gold easier to invest in than real estate?

Yes. Gold has lower entry costs and higher liquidity. You can buy gold instantly with minimal paperwork. Real estate requires capital, financing, and due diligence.

Does gold pay any income?

No. Gold produces no yield. You only profit from price appreciation. Real estate, in contrast, generates recurring income through rent.

Which is riskier: gold or real estate?

Gold carries market timing risk and no control. Real estate involves operational and liquidity risk but offers investor control and multiple value levers.

Can you leverage gold like real estate?

No. Gold is typically bought outright. Real estate allows 60–80% leverage, enhancing returns through mortgage financing.

Is gold better during a recession?

Gold performs well during economic crises and inflation spikes. Real estate also holds up if cash flows remain strong and debt is structured conservatively.

Which is more tax-efficient: gold or real estate?

Real estate is more tax-efficient. It offers depreciation, 1031 exchanges, and income sheltering. Gold is taxed as a collectible at up to 28% on long-term gains.