European equities are quietly enjoying one of their best stretches in years, and part of the story has little to do with earnings or macro surprises. It’s the euro itself that’s helping push valuations higher.

In 2026, the euro has shown impressive resilience, holding steady against the dollar and even gaining ground against other major currencies like the yen and pound. That strength is more than just a macro footnote. It’s creating new dynamics in European equity markets that are favoring domestic-facing sectors, boosting investor confidence, and changing how global capital flows into the region.

For long-term investors, especially those used to watching U.S. dollar trends, this is a shift you can’t afford to ignore.

As BlackRock noted in a recent European strategy update, “currency alignment is one of the most overlooked tailwinds in equity performance. When the currency works in your favor, you don’t need 10% EPS growth to make money.”

With valuations still trading at a discount to U.S. peers and fresh capital pouring into eurozone equities, it’s worth asking whether currency trends can keep powering this rally deeper into 2026. Understanding how hedging fits into this picture is a smart place to start.

Table of Contents

How Currency Movements Affect Stock Prices in Europe

Currencies can quietly make or break your equity performance, especially in regions like Europe where many companies rely on both global exports and local consumer demand. When the euro strengthens, it changes the playing field for different types of European businesses in ways that are easy to miss if you’re not watching closely.

A weaker euro tends to benefit exporters. Companies that sell goods to the U.S., China, or the Middle East suddenly look more competitive because their prices drop in foreign currency terms. That’s been the traditional narrative for German automakers or French luxury houses like LVMH, who earn a big chunk of their revenue abroad.

But in 2026, the trend is starting to flip. The euro has stayed relatively strong, hovering around $1.11 to $1.13 in recent months, buoyed by improved investor confidence, tighter monetary policy from the European Central Bank (ECB), and stable inflation data. That’s tilting the advantage toward domestic-facing sectors like financials, utilities, and real estate, which are businesses that earn most of their revenue in euros.

According to a recent Goldman Sachs research note, “When the euro stabilizes or appreciates, investors tend to shift their focus from exporters to sectors with more predictable euro-denominated cash flows. The result is better performance from domestic equities that had previously lagged.”

And it’s not just theory. The Stoxx Europe 600 Banks Index is up over 12% year-to-date, outpacing many export-heavy subindices. Domestic stocks in countries like Spain, Italy, and the Netherlands have also gained traction, with local financials and infrastructure plays benefiting from a combination of stronger currency, firming economic data, and a more confident consumer base.

This shift in currency dynamics is changing how you should think about European investing altogether. Rather than betting on external demand and currency arbitrage, more investors are backing sectors with lower FX risk and clearer profit visibility in a stable euro environment.

The Euro’s Performance in 2024 and 2026

The euro’s recent stability hasn’t made headlines. But for you as an investor, it’s one of the quiet forces reshaping Europe’s equity story in 2026.

After a volatile 2022 and early 2023, the euro has regained its footing. From January 2024 through mid-2026, it has traded mostly in the $1.08 to $1.13 range, showing surprising resilience against both the U.S. dollar and the British pound. And this strength isn’t coming from speculative momentum. It’s backed by solid fundamentals.

The European Central Bank has played a key role here. By holding interest rates higher for longer while gradually taming inflation, it sent a clear message that the eurozone is committed to price stability. Annual inflation in the euro area fell to around 2.1% in early 2026, close to the ECB’s target.

In contrast, markets have begun pricing in more aggressive rate cuts in the U.S., which has put downward pressure on the dollar and given the euro more breathing room.

That divergence in policy has made the euro more attractive to global investors looking for yield stability and lower currency risk. If you’re managing a cross-border portfolio, that’s a meaningful edge.

As Christine Lagarde, President of the ECB, noted earlier this year, “Our objective is clear: stable prices and a resilient financial environment that supports confidence in the euro.”

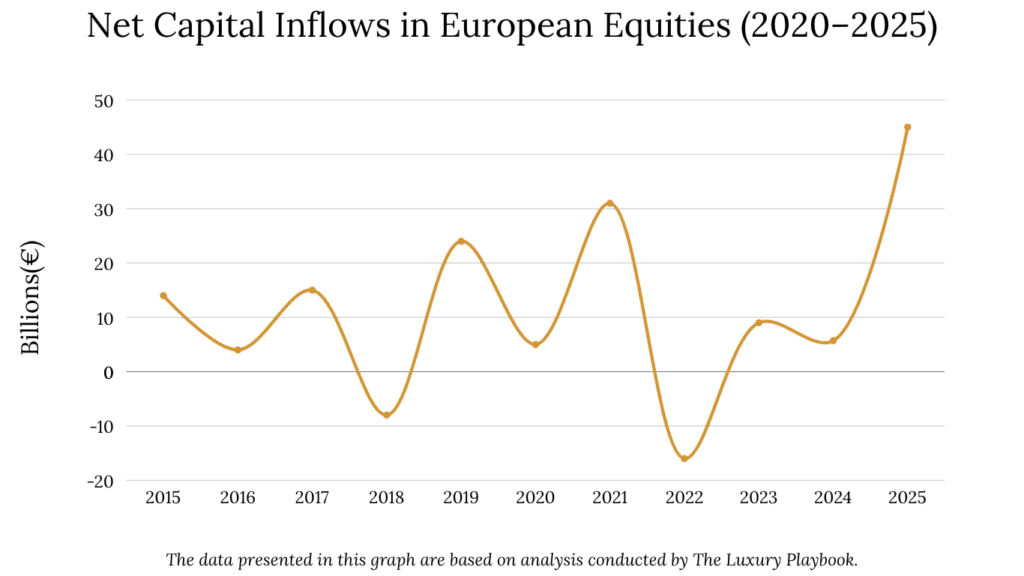

Markets have responded. According to Bloomberg data, net portfolio inflows into eurozone equities rose by over €40 billion in the first half of 2026, a clear sign that international capital is rotating into the region.

The euro’s performance against other currencies like the Japanese yen and Chinese yuan has also been strong, making European assets relatively more appealing for Asian investors. This global positioning reinforces the idea that European stocks are benefiting not only from domestic fundamentals, but from being priced in a currency the market currently trusts.

Sectors and Companies Benefiting from Currency Trends

As the euro strengthens and holds steady, the biggest winners aren’t the usual suspects like exporters or multinationals. The real action is in domestic-facing sectors, which are businesses that earn and spend primarily in euros, and they’re quietly leading the charge in 2026.

Start with European banks. After years of underperformance, many have finally found their footing. A stable euro supports interest income, reduces FX risk on foreign debt, and makes the region more attractive for capital inflows. The Stoxx Europe 600 Banks Index is up over 12% year-to-date, with names like Banco Santander, ING, and UniCredit drawing fresh investor attention.

UniCredit’s Q1 2026 earnings call specifically credited currency stability and stronger domestic loan growth for beating revenue expectations. That kind of transparency is exactly what institutional investors want to hear.

Next up are utilities and infrastructure. These are typically quieter sectors, but in this environment, that steadiness is precisely the appeal. With stable euro pricing, predictable income streams, and limited international exposure, utilities have emerged as a favorite for long-term, risk-conscious investors. Companies like Iberdrola, Enel, and EDF have seen modest but consistent stock price growth since early 2024, aided by government-backed capex projects and stable consumer demand.

Real estate is another story worth your attention. While high rates in 2023 and 2024 cooled enthusiasm across Europe, the outlook in 2026 is shifting. As inflation moderates and long-term borrowing costs ease slightly, prime property markets in Germany, the Netherlands, and Austria have begun to stabilize. Understanding property tax structures across European countries is essential before you commit capital to any of these markets. REITs with euro-only exposure are especially appealing to institutional investors looking to avoid currency conversion losses.

According to Blackstone Europe, “We’re seeing renewed interest in continental real estate because the yield spread is becoming attractive again, and the currency isn’t working against us.”

Even consumer discretionary stocks have seen pockets of strength. Retailers with a strong eurozone footprint like Zalando, Inditex (Zara’s parent), and Ahold Delhaize are benefiting from renewed consumer confidence as inflation comes down and purchasing power stabilizes.

How Currency Stability Is Attracting Global Investors to Europe

For years, many global investors treated Europe as a value play that rarely delivered. But in 2026, the tone has shifted, and currency stability is a big part of why. A stronger euro means less uncertainty, especially for institutional investors managing cross-border portfolios.

And with U.S. stocks feeling richly valued, Europe suddenly looks like a more balanced and attractive option for your money.

So where is the money actually coming from?

According to J.P. Morgan’s mid-year investment report, capital flows into European equities reached a three-year high in Q2 2026, with more than €45 billion in net inflows. Much of this is being driven by large asset managers from North America and Asia, looking to reduce exposure to overbought U.S. tech and diversify into regions with steadier currencies and lower valuations.

Samantha Grant, Head of European Strategy at Franklin Templeton, recently noted, “When currency volatility is low, it opens the door for long-term investors to move in with confidence. You don’t need to hedge aggressively, and the return profile becomes easier to model.”

The euro’s consistency has also made unhedged ETFs more attractive. Several euro-denominated ETFs have seen strong volume growth in 2026, particularly those focused on real assets, infrastructure, and banking. Funds like the iShares MSCI EMU ETF and Lyxor Euro Stoxx Banks ETF have seen a spike in demand from U.S. investors looking to capitalize on euro-denominated income streams.

In Asia, sovereign wealth funds and pension managers are following the same playbook. Several Singaporean and Korean institutions have increased their allocation to European real estate and listed equities, citing both valuation opportunity and currency clarity. Asian investors are also reassessing their overexposure to AI-driven markets, which is pushing more capital toward European alternatives.

On top of that, many investors view the euro as a stabilizer during turbulent times. Unlike more volatile emerging market currencies, or even the dollar, which faces political and fiscal headwinds, the euro today is seen as a moderate-risk, high-visibility currency. That makes it easier for global allocators to justify exposure to European assets without overcomplicating FX strategies.

Put simply, the steady euro has removed a major friction point. You no longer need to hedge aggressively, worry about currency drag, or wait for a better entry point. The environment is already aligned, and global capital is responding accordingly.

How to Build Exposure to European Equities Based on Currency Trends

If you’re looking to ride the wave of currency-fueled momentum in European equities, the good news is that it’s never been easier to get positioned. Whether you’re a retail investor or managing a larger portfolio, there are practical, low-friction ways to gain exposure to this shift without overcomplicating things with aggressive currency hedging or exotic instruments.

Start with the simplest route, which is ETFs. Broad-based eurozone ETFs have seen a clear surge in inflows in 2026. Funds like the iShares MSCI EMU ETF (EZU) and the Vanguard FTSE Developed Europe ETF (VEA) offer diversified exposure to euro-denominated equities, including leading banks, consumer brands, and industrials.

If you’re targeting specific winners from this euro stability trend, like domestic-facing banks or infrastructure, sector-focused ETFs such as the Lyxor EURO STOXX Banks ETF or iShares Eurozone Infrastructure ETF are strong tactical choices worth exploring.

The question of currency hedging often comes up, especially for U.S. investors. But this year, many professionals are choosing unhedged positions.

Why? Because the euro has been stable and even appreciating modestly against the dollar, offering an additional layer of return. As Peter Oppenheimer of Goldman Sachs put it in a recent outlook piece,

“We see currency exposure in Europe as a modest tailwind rather than a risk factor in the current macro cycle.”

For investors seeking more direct exposure, American Depositary Receipts (ADRs) for major European companies are a convenient option. Firms like SAP, Sanofi, and TotalEnergies are all eurozone-based and traded on U.S. exchanges in dollars, making it easier for retail investors to participate without opening foreign brokerage accounts. You can read more about the latest European equity coverage from the Financial Times to stay current on individual names.

If you’re a longer-term investor looking for deeper conviction plays, some are turning to dividend-focused European funds. These portfolios concentrate on stable, euro-denominated income streams, which benefit directly from a strong local currency. Working with a wealth management firm can help you structure this kind of exposure efficiently, especially across multiple currencies and jurisdictions.

Names like the WisdomTree Europe Quality Dividend Growth ETF and SPDR Euro Dividend Aristocrats ETF have gained traction for this very reason.

Institutional investors, meanwhile, are looking beyond equities. With a stable euro and falling inflation, core European real estate is regaining appeal. Pension funds are allocating capital toward REITs and direct property investments in cities like Berlin, Amsterdam, and Vienna, where pricing has stabilized and yields are recovering. If you’re thinking along those lines, understanding the four phases of the real estate market cycle will help you time your entry with far more precision.