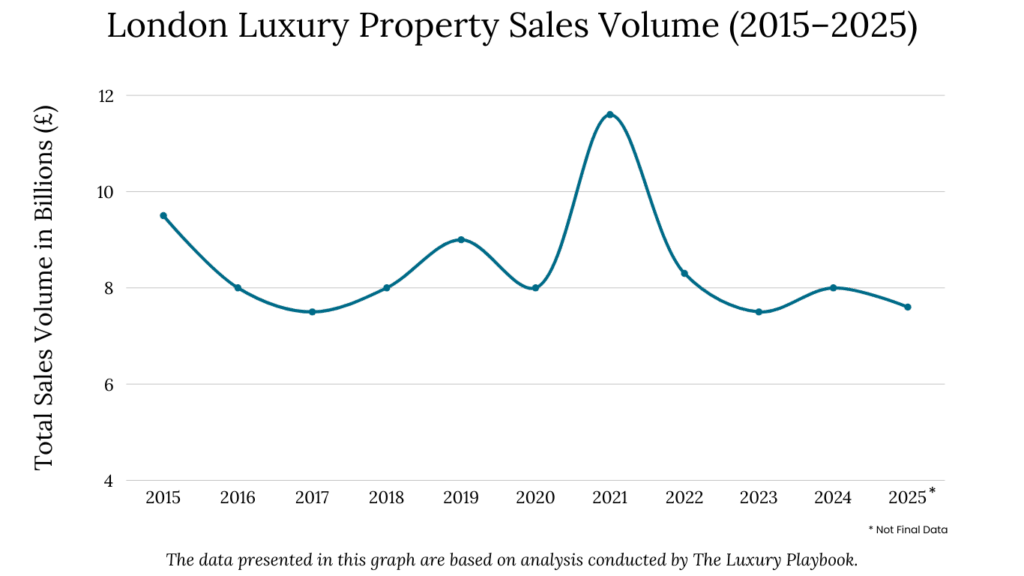

London has long been one of the most attractive cities in the world for property investors, but the latest numbers show that its luxury housing market is losing momentum. According to recent data from LonRes, sales of London Luxury Real Estate dropped by nearly 12% in July 2025 compared to last year, marking one of the steepest declines since the pandemic.

Even compared with pre-pandemic averages, sales volumes remain around 8% lower.

At the same time, new listings are rising, with a 22% increase year over year, pushing inventory higher and giving buyers more choice. Price growth in luxury zones has also flattened, with values rising only 0.4% over the past year—a stark contrast to the double-digit gains seen in 2021 and 2022.

This slowdown has caught the attention of investors worldwide. London real estate has traditionally been seen as a “safe haven” asset, but the combination of weak sales and stagnant prices has raised questions about whether the ultra-prime market still offers the returns it once did.

As Liam Bailey, Global Head of Research at Knight Frank, recently noted: “The market is not collapsing, but it is adjusting to new realities—higher costs, shifting demand, and a more cautious buyer base.”

For investors, the key question is whether the weakness in luxury properties signals a broader downturn—or if it is simply creating new opportunities elsewhere in the city.

Table of Contents

Why London Luxury Home Sales Are Declining in 2025

The weakness in London’s luxury property market is not happening by chance. Several factors have combined to slow down sales, leaving even some of the city’s most prestigious neighborhoods struggling to attract buyers.

One of the biggest issues is the drop in transaction volumes. In July 2025 alone, deals for homes priced above £2 million fell by nearly one-third year over year. Even properties that do go under offer are taking longer to complete, with failure-to-close rates nearly 20% higher than last year.

This suggests that buyers are hesitant, often backing out after negotiations when they weigh the true costs of ownership.

Prices also tell the story. While the broader UK housing market has shown modest gains, prime London prices have barely moved. Average annual growth in the city’s top neighborhoods sits at just 0.4%, well below inflation, meaning that in real terms luxury property values are actually shrinking.

Sellers who became accustomed to record-breaking bids during the pandemic are now facing a market where buyers have the upper hand.

Adding to the challenge is the rise in supply. With more new listings—up more than 22% compared to 2024—buyers now have greater choice, which dilutes demand for any single property.

As Zoopla’s head of research, Richard Donnell, pointed out earlier this year: “The luxury end of the market is highly discretionary. When buyers see too much stock and not enough urgency, they negotiate harder or they simply wait.”

The Impact of Higher Taxes and Policy Changes on Luxury Buyers

Taxes and regulation are another major reason London’s luxury housing market is under pressure in 2025. The UK has one of the highest tax burdens for high-end property buyers in Europe, and recent changes have made the environment even less attractive for wealthy investors.

Stamp Duty Land Tax (SDLT) remains one of the heaviest upfront costs. For homes over £1.5 million, the effective rate can exceed 12%, and foreign buyers face an additional 2% surcharge. This means that a £5 million property could carry more than £600,000 in taxes before the keys are even handed over.

For many international investors, that’s a serious deterrent compared to markets like Dubai or Lisbon, where transaction costs are far lower.

The UK government’s move to reform the non-dom tax regime has also shaken confidence. For decades, the non-domiciled status allowed wealthy foreigners living in London to shield overseas income from UK taxation, making the city especially appealing to global elites. With those benefits now being phased out, some long-time foreign owners are reassessing whether it makes financial sense to keep or purchase luxury properties in London.

At the same time, ongoing annual property taxes and maintenance costs have become harder to justify given stagnant price growth and low rental yields in prime areas (often below 3% gross yield). Investors comparing returns can see stronger cash flow in emerging neighborhoods or even in other European capitals, which further explains the shift in demand.

For investors, this highlights a crucial point: London luxury homes may still hold long-term prestige value, but in the current tax and policy environment, the cost-benefit balance is tilting away from prime central districts. This is one of the reasons why attention is moving toward secondary areas of the city, where the entry prices are lower, yields are higher, and future growth potential looks stronger.

Rising Inventory and Unsold Properties in Prime Central London

Another clear sign of weakness in the luxury segment is the growing stock of unsold homes. In mid-2025, the number of prime central London properties available on the market rose by nearly 16% compared to last year, driven by a surge in new listings. Sellers who were holding off during the pandemic are now bringing properties to market, just as demand is cooling.

This mismatch has tilted negotiating power toward buyers. When inventory rises faster than sales, sellers often face two choices: reduce asking prices or leave properties sitting on the market for months. Current data shows that the average time to sell a high-end London home has stretched well beyond six months, with some ultra-prime mansions lingering for more than a year without serious offers.

The increase in supply also puts downward pressure on values. With more options available, wealthy buyers are in no rush to commit. They can view multiple properties, compare features, and bargain aggressively—something that was much harder to do during the pandemic years of tight supply.

As one of our analysts recently explained, “Choice has returned to the luxury market, and choice breeds caution.”

From an investment perspective, this shift has important implications. Excess supply in the prime sector weakens short-term price appreciation, limiting potential returns for those looking at capital gains.

At the same time, low rental yields in areas like Mayfair or Knightsbridge—often under 3% gross—mean that holding these properties is increasingly expensive without the offset of strong rental income.

This environment has created a situation where prestige assets are losing their financial edge, even if they retain symbolic value. That dynamic is pushing capital toward neighborhoods where supply and demand are more balanced—and where buyers can still find meaningful upside.

Secondary London Neighborhoods Showing Stronger Growth

While luxury districts like Mayfair, Knightsbridge, and Belgravia are slowing, several secondary London neighborhoods are showing a very different trajectory. Areas once considered “fringe” are now becoming hotspots, with both domestic buyers and international investors fueling demand.

Take Hackney, for example. Once overshadowed by central zones, it has transformed into one of London’s most dynamic areas. Average home prices there have risen by around 6% year on year, outpacing prime central London, and rental yields often exceed 4%, making it far more attractive to yield-focused buyers.

The area’s mix of creative industries, trendy restaurants, and improved transport links has drawn in younger professionals who prefer lifestyle-oriented locations.

Wandsworth is another standout. Known for its family-friendly appeal and green spaces, it continues to benefit from strong domestic demand. Prices have grown steadily, with certain pockets outperforming the wider London average. Importantly, the borough’s relative affordability compared to prime central areas gives it more room for sustainable growth.

Victoria Park and East London more broadly have also seen consistent interest. Regeneration projects, new transport infrastructure, and a younger demographic have reshaped the area’s image. These neighborhoods are now viewed as both livable and investable, with homes that appeal to owner-occupiers and investors seeking stronger rental performance.

The contrast is striking. Where central luxury properties offer prestige but limited returns, these secondary neighborhoods are delivering tangible growth and healthier cash flow.

| Neighborhood | Avg. Price Growth (YoY) | Rental Yields |

|---|---|---|

| Hackney | ~6% | 4–4.5% |

| Wandsworth | ~5% | 3.5–4% |

| Victoria Park / East London | ~5–6% | 4–5% |

| Stratford | ~7% | 4.5–5% |

| Greenwich / Woolwich | ~6% | 4.5% |

| Peckham | ~5% | 4–4.5% |

| Brixton | ~4–5% | 4% |

| Tottenham / Seven Sisters | ~7%+ | 5% |

Why Secondary Areas Are Attracting More Buyers

The rise of secondary London neighborhoods isn’t just a passing trend—it’s being fueled by several structural factors that make them more appealing in today’s market.

Affordability is the biggest driver. With prime central properties often priced at £3,000 to £5,000 per square foot, many buyers are priced out or unwilling to pay those premiums. In contrast, secondary areas like Hackney or Wandsworth can still offer homes for 40% to 60% less per square foot, while providing strong lifestyle benefits.

This makes them accessible not only to local families but also to international investors seeking lower entry costs.

Rental yields are stronger outside the luxury core. While prime central yields often struggle to reach 3%, many secondary areas generate 4% to 5% gross yields, particularly in East London and parts of South London. For investors focused on income rather than prestige, that difference is significant—especially in an environment where borrowing costs remain elevated.

Lifestyle shifts are also reshaping demand. Post-pandemic buyers are prioritizing larger living spaces, proximity to parks, vibrant local communities, and better value for money. This has pulled demand toward neighborhoods that balance livability with investment potential. Areas with strong schools, creative hubs, or new cultural offerings are benefiting the most.

Finally, regeneration projects and infrastructure improvements are boosting the appeal of these districts. The Elizabeth Line, for example, has cut travel times across East and West London, making places like Stratford and Woolwich more attractive for both residents and investors. Planned developments continue to enhance connectivity and local amenities, laying the groundwork for further appreciation.

As a senior analyst at Savills recently observed, “The definition of prime in London is evolving. Buyers are less concerned with postcode prestige and more focused on where they can see long-term value and growth.”

The Impact of International Buyers and Domestic Demand on London Housing

The rebalancing of London’s property market is being driven by both international and domestic forces, though in very different ways.

Foreign buyers have historically been the backbone of London’s luxury housing market, particularly in prime central districts.

However, with higher taxes, stricter regulations, and weak price growth, their focus has started to shift. Many overseas investors, especially from the U.S. and Asia, are now looking at secondary areas where entry prices are lower, yields are stronger, and long-term appreciation looks more compelling.

A recent report from Knight Frank showed that U.S. buyers accounted for nearly a quarter of all prime London purchases in 2024, but a growing share of that activity is now happening outside the ultra-prime zones.

Domestic demand has also strengthened in secondary neighborhoods. Rising interest rates and higher living costs mean local buyers are seeking better value, avoiding the high running costs of central mansions.

For many London families, areas like Wandsworth, Richmond, and parts of East London offer the right balance between affordability, lifestyle, and connectivity. This organic demand provides stability, reducing the reliance on speculative foreign capital that once drove much of central London’s market.

Interestingly, the rental market is playing a bridging role. Wealthy buyers who are hesitant to commit to purchasing in prime areas are choosing to rent instead, while investor demand in secondary markets is meeting a strong pool of tenants. This dynamic is further reinforcing the appeal of neighborhoods that can deliver consistent rental income.