The Bristol Real Estate Market in 2025 remains one of the UK’s most sought-after regional markets, combining steady price growth, solid rental demand, and long-term urban development. As a core city in the South West with strong transport links, a thriving knowledge economy, and a high quality of life, Bristol continues to attract both domestic and international investment.

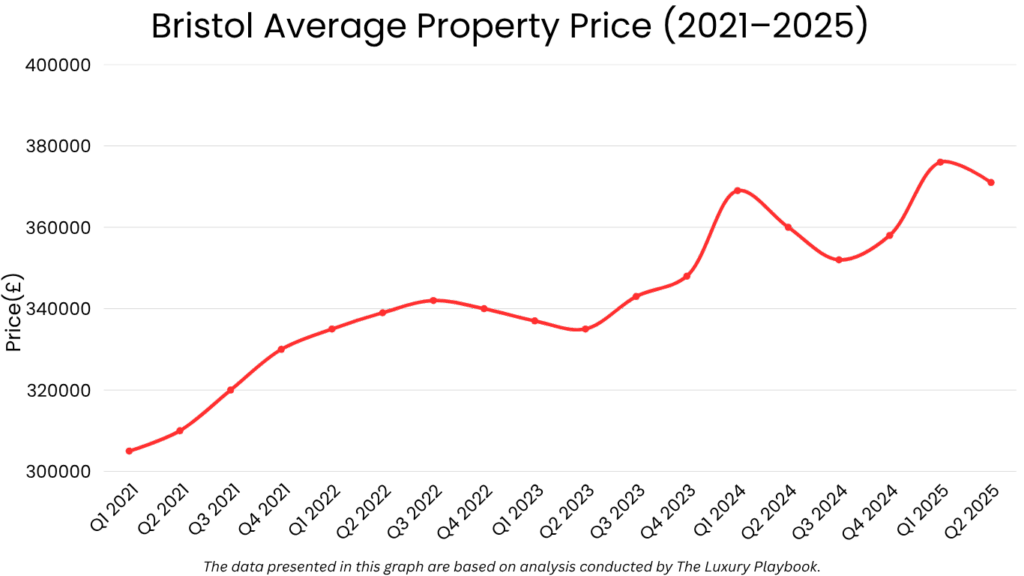

As of Q2 2025, the average property price in Bristol stands at approximately £371,000, showing a modest yet stable 3.0% year-on-year increase. This resilience follows a broader national slowdown and reflects the city’s structural undersupply, consistent inward migration, and tight planning environment.

Rental performance remains a key attraction. Gross yields across the city average between 4.5% and 5.5%, with the strongest income performance in value-growth districts such as Easton, St. George, and Bedminster. These areas continue to outperform due to tenant affordability constraints in the more expensive north and west Bristol postcodes.

Backed by ongoing regeneration projects—including the Temple Quarter Enterprise Zone and Western Harbour masterplan—Bristol offers investors a favourable mix of yield, stability, and mid-term appreciation potential.

Table of Contents

Overview of The Bristol Real Estate Market

The Bristol Real Estate Market in 2025 continues to demonstrate stability and long-term resilience, backed by a combination of strong local employment, supply-side restrictions, and sustained demand from both owner-occupiers and renters. As one of the UK’s most undersupplied housing markets, Bristol has retained price strength despite national economic volatility.

As of Q2 2025, the average house price in Bristol is approximately £371,000, marking a 3.0% increase year-on-year.

While growth has moderated compared to the post-pandemic surge, Bristol remains one of the UK’s most expensive regional cities—outpricing Leeds, Manchester, and Birmingham—due to its limited land availability and strict planning constraints.

The city’s price stability is supported by high demand in key employment sectors such as aerospace, finance, tech, and education. Bristol’s role as a regional capital ensures consistent buyer activity from professionals, families, and relocating workers. Additionally, its vibrant student population contributes to the strength of both the sales and rental markets.

Transaction volumes remain strong in the £300K–£450K range, particularly in districts where demand from young professionals and first-time buyers is highest.

Limited new-build supply is putting upward pressure on resale stock, especially in centrally located areas where regeneration projects are underway.

Key market characteristics in 2025:

- Average property price: £371,000

- Annual price growth: 3.0% (2024–2025)

- Buyer segments: First-time buyers, professional relocations, landlords, downsizers

- High-demand zones: Bishopston, Redland, Easton, Southville, Clifton

- New housing supply: Limited; concentrated around Temple Quarter and fringe developments

- Rental demand correlation: High in job-rich areas and university-adjacent neighbourhoods

In summary, the Bristol Housing Market maintains its status as a high-demand, high-barrier city with steady performance and long-term investment appeal. While not a speculative play, it offers investors consistent returns, tenant security, and exposure to one of the UK’s most economically resilient urban centres.

Neighborhood Analysis

Bristol’s property market is distinctly shaped by its varied neighborhoods, each with unique investment potential, tenant profiles, and price dynamics. Investors can choose from high-yield regeneration zones, established family-friendly suburbs, and prime resale districts with strong capital preservation.

Easton

Easton continues to attract investors and first-time buyers due to its affordability, strong rental demand, and proximity to the city centre. Known for its cultural diversity and independent high street, Easton is in the midst of gentrification, with increasing demand from young professionals.

Average prices are around £305,000, or approximately £3,400/sqm, with gross yields of 5.5% to 6.0%. Renters are typically young couples, remote workers, and graduate professionals.

Bedminster

Located south of the River Avon, Bedminster has seen considerable development and rising prices in recent years. Its close proximity to the Harbourside and Temple Meads Station makes it popular with commuters and families.

Prices range between £350,000 and £390,000, with per-square-meter values of around £4,100/sqm. Rental demand remains consistent, with gross yields of 4.5% to 5.2% depending on property type and finish.

Redland

Redland is one of Bristol’s most desirable and stable residential areas, popular with professionals and families due to its green space, schools, and Georgian architecture. It commands a premium but offers long-term value retention.

Average home prices exceed £500,000, with values approaching £5,000/sqm. Rental yields are lower, typically 3.8% to 4.2%, but void periods are minimal and demand is consistent.

St. George

St. George, particularly around Church Road, has gained momentum as a buy-to-let hub for those priced out of central Bristol. It appeals to budget-conscious renters and offers solid mid-range returns.

Property prices average £295,000, or about £3,200/sqm, with yields ranging from 5.5% to 6.2%, making it one of the most attractive areas for income-focused investors.

Clifton

Clifton remains Bristol’s most prestigious and expensive area. With Georgian squares, independent shops, and proximity to the University of Bristol, it is ideal for capital preservation and high-quality tenancies.

Prices average over £600,000, with per-square-meter values between £5,500 and £6,200. Yields are modest (3.0% to 3.5%), but the area is considered a low-risk, high-liquidity market.

Neighborhood Median Prices and Price per Square Meter

Bristol Rental Market Overview

The Bristol rental market in 2025 remains one of the strongest in the UK, driven by a limited supply of housing, high tenant demand, and steady population growth. The city’s appeal among young professionals, students, and relocating families has kept occupancy levels high and rents rising across nearly all property types and districts.

Rental performance in Bristol is defined by structural undersupply, rising affordability pressures, and the city’s expanding economic base—making it ideal for long-term income-focused property investment.

Average Monthly Rent by Property Type (2025)

- 1-Bedroom Apartment: £1,000 – £1,200

- 2-Bedroom Apartment: £1,300 – £1,500

- 3-Bedroom Apartment: £1,500 – £1,850

- Student HMO (per room): £575 – £700

- City Centre Luxury Units: £1,800 – £2,400+

As of Q2 2025, the average monthly rent in Bristol sits at approximately £1,749.

The tightest markets are in central areas like Redcliffe, Southville, and Clifton, where tenant competition is high, particularly for 1- and 2-bedroom furnished flats.

Demand is also surging in outer areas like Horfield, Easton, and St. George, where rents remain more accessible, but quality supply is limited. These districts are seeing above-average rental increases as professional tenants migrate outward in search of affordability and space.

Yield Performance and Tenant Demand

Rental yields across Bristol average between 4.5% and 6.2%, depending on district, property condition, and configuration. HMOs and converted Victorian terraces tend to outperform, particularly in Easton, Horfield, and St. George, where per-unit costs remain reasonable.

- High-Yield Zones: St. George, Easton, Fishponds (5.5%–6.2%)

- Balanced Performance: Horfield, Bedminster, Southville (4.8%–5.5%)

- Capital Preservation Zones: Clifton, Redland (3.2%–4.2%)

Tenant demand is diversified, including:

- Young professionals working in aerospace, finance, tech, and healthcare

- Students attending the University of Bristol and UWE

- Families relocating from London or the South East

- Digital nomads and hybrid workers seeking lifestyle-rich rental hubs

Most leases are for 12-month ASTs, though mid-term corporate tenancies and student pre-lets are also popular. EPC-compliant units with energy efficiency upgrades, fast internet, and outdoor space remain top of tenant wish lists.

While Bristol does not enforce rent caps, it operates additional and selective licensing schemes for HMOs in many zones, particularly Ashley, Easton, and Lawrence Hill. Licensing compliance, minimum energy standards, and planning considerations for larger HMOs must be factored into investment decisions.

Short-term letting remains legal but is subject to local planning restrictions in certain conservation areas. For most investors, long-term and professional lettings continue to offer the most stable and scalable model.

In summary, the Bristol rental market remains underpinned by solid fundamentals. With limited stock, rising rents, and consistent tenant demand, Bristol continues to offer strong income prospects for landlords targeting well-located, well-managed, and regulation-compliant properties.

Factors Influencing the Bristol Housing Market

The Bristol Housing Market in 2025 is driven by a blend of economic growth, limited land availability, and demographic shifts. These elements have combined to create a high-demand, low-supply environment that continues to support both property values and rental growth across the city.

- Strong Local Economy and Job Market: Bristol has one of the UK’s most dynamic regional economies, with a strong presence in aerospace, finance, digital tech, engineering, and media. Major employers like Airbus, Rolls-Royce, and the NHS continue to attract skilled professionals to the area, sustaining consistent housing demand across both rental and ownership sectors.

- Undersupplied Housing Stock: Bristol faces chronic housing undersupply, with planning restrictions and land constraints limiting the pace of new development. The city’s greenbelt and conservation areas restrict horizontal expansion, keeping resale stock in high demand and intensifying competition in key inner suburbs like Southville, Redland, and Bishopston.

- High Levels of In-Migration: Internal migration from London and the South East continues to push demand higher. Bristol’s relative affordability, lifestyle appeal, and growing employment opportunities make it a popular choice for remote and hybrid workers. This trend has placed additional pressure on the mid-market price segment, particularly for 2- and 3-bedroom family homes.

- Student and Graduate Retention: With over 50,000 students enrolled across the University of Bristol and UWE, the city maintains a strong base of short- and medium-term renters. Importantly, Bristol also retains a high number of graduates, many of whom stay in the city post-study to work in tech, education, and public health sectors—reinforcing demand in the £275K–£400K price range.

- Regeneration and Infrastructure: Ongoing regeneration in the Temple Quarter Enterprise Zone, Western Harbour, and around Temple Meads station is transforming underutilised sites into residential and mixed-use hubs. These developments are drawing investors to fringe areas such as Brislington, Barton Hill, and St. Philip’s Marsh, where long-term value appreciation is expected.

- Limited Affordability for Local Buyers: Despite high demand, affordability remains a challenge for many residents. Bristol’s average home price is 9.5 times the local average salary, placing it among the least affordable UK cities outside London. This imbalance supports rental demand but may cap short-term price growth in more saturated, high-end districts.

Bristol Housing Market Forecast for 2026

The Bristol Housing Market is expected to maintain its trajectory of steady growth through 2026, with price appreciation underpinned by limited supply, consistent buyer demand, and expanding infrastructure. While the pace of growth is likely to remain moderate compared to the post-pandemic surge, both capital values and rental income are forecast to rise across most districts.

For long-term investors and income-focused landlords, Bristol remains a resilient and fundamentally strong market with sustainable upside and low volatility.

Property prices in Bristol are forecast to rise by 3.5% to 5.0% Growth will be led by outer-ring neighborhoods benefiting from regeneration and infrastructure connectivity, including Brislington, Barton Hill, Horfield, and parts of St. George. These areas are expected to outperform due to relative affordability and expanding tenant demand.

Citywide, the average property price is expected to increase from £371,000 to between £390,000 and £395,000 by the end of 2026, with centrally located family homes and energy-efficient flats maintaining the strongest resale values.

Premium districts like Clifton, Redland, and Cotham will likely grow at a slower pace (2.5%–3.5%) due to their already mature pricing and smaller buyer pools, although demand remains strong for well-maintained, character-rich homes.

Rental prices are projected to increase by 4.5% to 6.0%. The city’s housing undersupply, rising population, and ongoing student and professional in-migration will continue to pressure the rental market. Central and fringe neighborhoods with good transport links and high EPC-rated properties will experience the strongest gains.

- 2-bedroom apartments are expected to average £1,600–£1,650/month

- 3-bedroom homes in high-demand suburbs could reach £1,800–£2,000/month

- Student HMOs and multi-lets will continue to generate strong income, particularly in Horfield, Bishopston, and Easton

Yields will remain stable or improve slightly in emerging districts, with gross returns of 5.5% to 6.2% achievable in high-demand but relatively low-cost neighborhoods.

New development will remain constrained. Planning bottlenecks, greenbelt restrictions, and cost pressures will continue to limit large-scale housing delivery. Most new inventory will come from brownfield redevelopment near Temple Meads and fringe urban districts, rather than widespread suburban expansion.

This limited pipeline supports ongoing appreciation in the resale market, particularly for energy-efficient, tenant-ready homes.

Investor outlook remains cautiously optimistic. While affordability ceilings and tighter regulation may limit aggressive capital gains, Bristol remains one of the UK’s most structurally sound markets. Investors targeting mid-tier properties in emerging corridors can expect stable occupancy, increasing rents, and capital preservation over a 5–10 year horizon.

In summary, the Bristol Housing Market in 2026 is forecast to offer measured capital growth and healthy rental gains. Investors focused on income and long-term asset quality—especially in regeneration-linked or mid-range zones—will continue to find strong opportunities across the city.

Is It Worth Buying a Property in Bristol?

Yes—with the right strategy and location, Bristol remains a smart choice for property investors in 2025 and into 2026. While not a market for aggressive short-term gains, Bristol offers a combination of long-term capital stability, consistent rental demand, and economic fundamentals that continue to outperform national benchmarks.

Bristol’s appeal lies in its balance. Investors benefit from a well-educated workforce, strong tenant diversity, and a housing market that holds value even in broader downturns.

Average yields across the city range from 4.5% to 6.2%, with above-average returns found in emerging regeneration corridors such as St. George, Easton, Horfield, and Brislington. Meanwhile, investors focused on capital preservation and low tenant turnover often target Clifton, Redland, or Bishopston, where price growth is slower but voids are rare.

However, investors should consider the following:

- Capital growth is likely to be modest in fully priced central neighborhoods like Clifton and Redland.

- Licensing requirements are active in many high-density HMO zones, adding administrative cost and complexity.

- Planning constraints and Bristol’s tightly defined urban footprint limit access to large development sites.

- Affordability pressure may impact buyer demand in the short term, particularly in premium segments.

Despite these limitations, Bristol consistently ranks among the most investable UK cities due to its lifestyle appeal, job creation, and infrastructure pipeline.

Investors focused on well-maintained, EPC-compliant resale stock in high-demand rental areas will find the market offers low volatility, stable returns, and the security of long-term urban growth.

Other Market Forecasts & Overviews

London Real Estate Market Overview & Forecast

Manchester Real Estate Market Overview & Forecast

Liverpool Real Estate Market Overview & Forecast

Derby Real Estate Market Overview & Forecast

FAQ

Is Bristol a good place to invest in property in 2025?

Yes. Bristol offers stable capital growth, strong tenant demand, and consistent rental yields.

What is the average house price in Bristol in 2025?

Approximately £371,000, with prices higher in Clifton and Redland, and lower in Easton and St. George.

Where are the best areas to invest in Bristol?

St. George, Easton, Bedminster, Horfield, and Brislington offer solid rental returns and growth potential.

What rental yields can I expect in Bristol?

Yields typically range from 4.5% to 6.2%, depending on location and property type.

Is Bristol a good market for buy-to-let investors?

Yes. Demand from students, professionals, and families supports year-round occupancy and rising rents.

Are there rent controls in Bristol?

No. Bristol currently has no rent caps, but certain areas require licensing for HMOs and multi-lets.

Can foreign investors buy property in Bristol?

Yes. The UK allows foreign ownership of residential property with no restrictions.

Is short-term letting allowed in Bristol?

Yes, but local planning rules apply in conservation zones. Long-term and mid-term lets are more stable.