The Liverpool Real Estate Market in 2025 stands out as one of the UK’s most attractive regional opportunities for property investors. With affordable entry points, strong rental demand, and major regeneration projects underway, Liverpool continues to offer a compelling mix of income potential and mid-term capital appreciation.

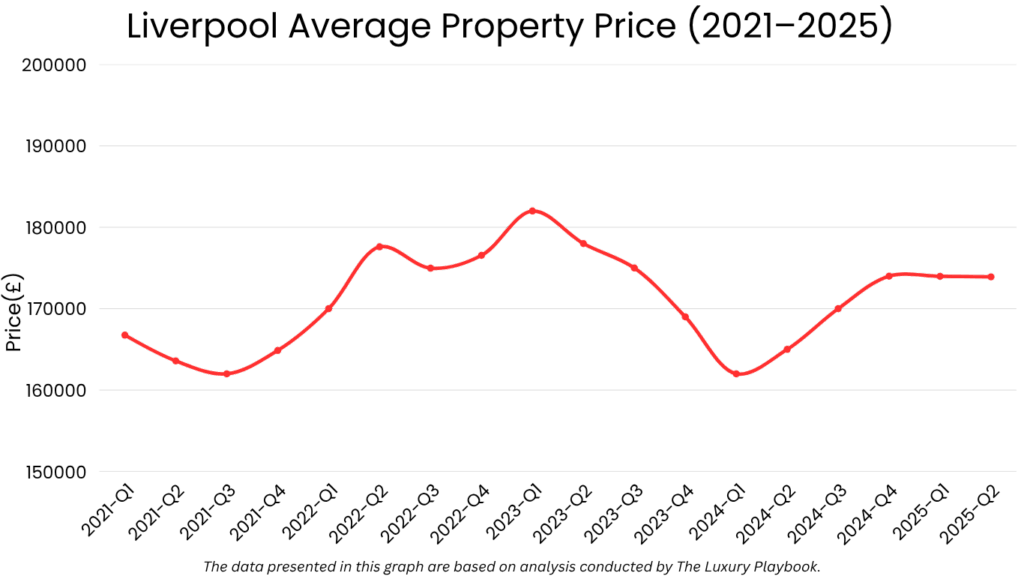

As of Q2 2025, the average property price in Liverpool is approximately £174,000, reflecting an 8.5% year-on-year increase—well above the national growth rate.

This performance is underpinned by rising demand across both first-time buyers and rental sectors, as well as the city’s broader transformation through strategic redevelopment zones.

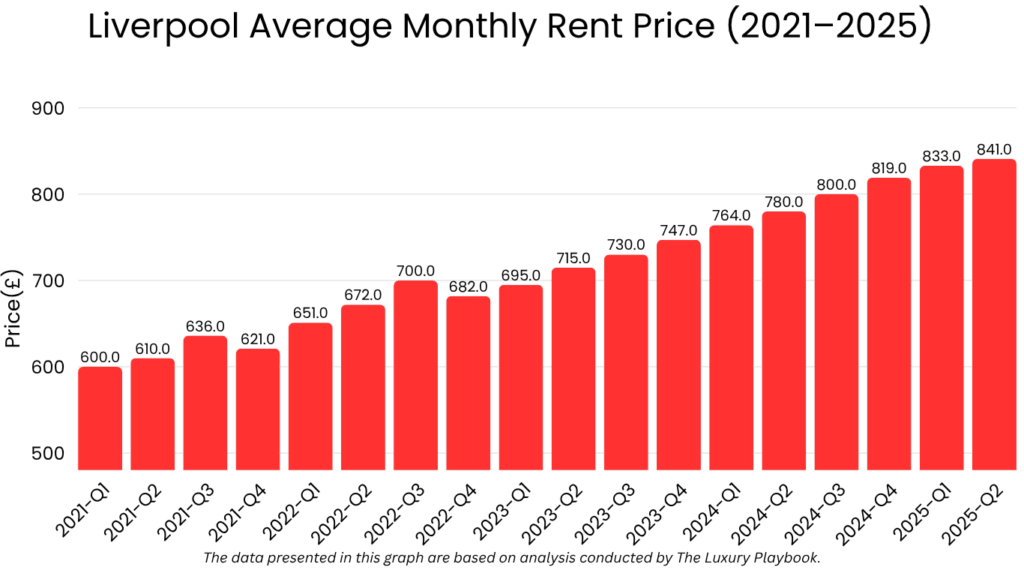

Rental performance remains a key draw. Average rents in the city now exceed £830/month, following a 9.9% increase over the past year. This rental uplift, combined with low purchase prices in many postcodes, delivers gross yields in the 6% to 8% range, positioning Liverpool as a standout location for buy-to-let investors seeking dependable income and long-term tenant demand.

Table of Contents

Overview of The Liverpool Real Estate Market

The Liverpool Housing Market in 2025 is performing ahead of many UK regional cities in both price growth and rental performance. This momentum is underpinned by a city-wide strategy focused on regeneration, infrastructure, and economic diversification—making Liverpool one of the strongest value-to-growth propositions in the country.

As of Q2 2025, the average house price in Liverpool is approximately £174,000, showing an 8.5% increase year-over-year.

This growth has been most concentrated in city-centre postcodes and regeneration zones such as Baltic Triangle, Anfield, and Toxteth, where pricing remains accessible and demand is supported by infrastructure enhancements and lifestyle-led redevelopment.

Transaction volumes remain strong in the sub-£200K bracket, particularly among first-time buyers and individual landlords. Many of these buyers are capitalising on below-average purchase prices combined with above-average gross yields.

Despite market-wide affordability pressures, Liverpool continues to offer entry-level opportunities well below the UK average, attracting both domestic and overseas investment.

New-build supply is limited relative to demand, particularly for modern apartments near employment clusters, universities, and transport corridors. This imbalance has created an undersupplied resale market that continues to support steady capital growth.

Key market characteristics in 2025:

- Average property price: £174,000

- Annual price growth: 8.5% (2024–2025)

- Growth corridors: Baltic Triangle, Anfield, Wavertree, Toxteth

- Buyer profile: First-time buyers, buy-to-let investors, student landlords

- New supply: Moderate; mostly BTR and PRS-led schemes

- Sales activity: Concentrated below £200K; high in postcodes L1, L3, L4, L7

In summary, the Liverpool Housing Market remains one of the most investable regional markets in the UK. Investors who target well-connected districts and regeneration zones will find a favourable balance between capital appreciation, affordability, and sustained rental demand.

Neighborhood Analysis

Liverpool’s property market is defined by a clear contrast between established rental zones, rapidly regenerating districts, and emerging fringe areas. For investors, choosing the right neighborhood is key to balancing yield, capital growth, and tenant stability.

The city’s diverse housing stock and postcode variation provide multiple entry points depending on investment strategy.

Baltic Triangle

Baltic Triangle remains Liverpool’s leading regeneration success story. Once a neglected warehouse district, it has become a hub for digital businesses, creatives, and young professionals. The area is now home to new-build flats, converted lofts, and high-spec BTR developments.

Prices average £200,000–£230,000, or around £3,000/sqm. Rental yields are strong at 6.0–6.5%, with consistent demand from young tenants working in the city centre or nearby tech hubs.

Anfield

Anfield has undergone major regeneration, including residential redevelopment and investment near the Liverpool FC stadium. It appeals to investors targeting high-yield HMO properties and long-term tenants.

Average property prices sit between £110,000 and £130,000, or around £1,700/sqm, with gross yields exceeding 7.5%. It is one of the most accessible areas in terms of entry cost and rental income performance.

Toxteth

Toxteth, historically overlooked, has become one of Liverpool’s most promising growth areas. With improved transport links, cultural revival, and ongoing refurbishment schemes, it is attracting younger tenants and investors seeking long-term capital growth.

Average prices are now around £150,000–£170,000, or £2,100/sqm, with rental yields typically in the 6.5–7.2% range.

Wavertree

Popular with students and young professionals, Wavertree remains a buy-to-let hotspot due to its proximity to the University of Liverpool and good public transport. It offers a strong balance between stable income and tenant turnover.

Prices average £160,000–£180,000, or approximately £2,200/sqm, with yields ranging from 5.5% to 6.5% depending on property type and condition.

City Centre (L1 & L3)

Liverpool’s city centre offers modern apartments, waterfront developments, and consistent demand from professionals, graduates, and short-term tenants. While capital growth is steady, yields are slightly lower due to premium pricing and higher service charges.

Prices range from £220,000 to £270,000, or £3,300–£3,800/sqm, with gross yields typically around 5.0–5.8%.

Neighborhood Median Prices and Price per Square Meter

Liverpool Rental Market Overview

The Liverpool rental market in 2025 remains one of the UK’s highest-yielding and most resilient urban markets. Backed by a large student population, growing graduate retention, and affordability-driven migration, rental demand continues to outpace available stock—driving consistent rental growth across most inner and outer districts.

Landlords in Liverpool benefit from strong tenant turnover, reliable demand, and yields that consistently outperform national averages—particularly in regeneration zones and value-focused neighborhoods.

Average Monthly Rent by Property Type (2025)

- 1-Bedroom Apartment: £675 – £850

- 2-Bedroom Apartment: £850 – £1,100

- 3-Bedroom Apartment: £1,100 – £1,400

- Central/New-Build Units: £1,400 – £1,750+

The average rent in Liverpool reached £841/month in Q2 2025, up 9.9% year-on-year, marking one of the highest rental growth rates among major UK cities.

Central districts such as L1, Baltic Triangle, and Ropewalks saw the sharpest increases, driven by the rising demand for city-centre living among professionals, students, and remote workers.

Rental Yields and Performance Zones

Gross rental yields in Liverpool typically range from 5.5% to 8.0%, with yields peaking in lower-entry neighborhoods such as Anfield, Kensington, and Everton, where investor interest is highest due to low capital barriers and consistent tenant demand.

- High-Yield Areas: Anfield, Walton, Kensington (7.0%–8.0%)

- Balanced Income Zones: Wavertree, Toxteth, Everton (6.0%–7.0%)

- City Centre & Premium Stock: Baltic Triangle, L1 Waterfront (5.0%–6.0%)

Rental demand is primarily driven by four core segments:

- Students from the University of Liverpool, LJMU, and LIPA

- Young professionals in healthcare, logistics, digital services, and construction

- Working families in outer boroughs with good transit links

- Remote workers occupying furnished, flexible-term flats in well-serviced areas

Moreover, rental properties in Liverpool are typically let on 12-month assured shorthold tenancy agreements, although there is increasing interest in mid-term leases (3–6 months) for mobile professionals. Furnished units, EPC-compliant renovations, and strong broadband are now essential to remain competitive.

Liverpool City Council operates Selective Licensing Schemes in many high-density letting areas, including Anfield, Toxteth, and Kensington. These require landlords to register their properties and meet defined safety and quality standards. While there are no rent caps, licensing non-compliance can result in fines, making landlord diligence critical.

Short-term rentals (e.g., Airbnb) remain legal but face greater regulatory scrutiny in city-centre postcodes. Most investors are advised to focus on long-term letting for security and regulatory alignment.

In summary, Liverpool’s rental market continues to deliver exceptional yield potential, driven by structural undersupply, strong tenant demand, and affordability advantages. Investors focused on income performance and portfolio stability will find Liverpool among the UK’s most reliable rental markets.

Factors Influencing the Liverpool Housing Market

The Liverpool Housing Market in 2025 is being shaped by a combination of economic growth, infrastructure investment, demographic change, and regeneration-driven demand. These factors collectively support both capital appreciation and rental performance across a wide range of property types and locations.

- Regeneration and Development Zones: Liverpool is undergoing one of the UK’s most ambitious urban transformations, with projects such as Liverpool Waters, the Knowledge Quarter, and the Ten Streets regeneration zone injecting billions into residential, commercial, and cultural development. These initiatives are boosting demand in nearby areas like Baltic Triangle, Vauxhall, and Kirkdale, where values remain below the national average despite increasing investor activity.

- Affordability Compared to Other UK Cities: With an average property price of £174,000, Liverpool remains significantly more affordable than Manchester, Leeds, or Birmingham. This affordability makes it an appealing entry point for both first-time buyers and portfolio investors seeking to maximise yield.

- Rental Demand Driven by Higher Education and Healthcare Sectors: Liverpool hosts more than 70,000 students across multiple institutions including the University of Liverpool, LJMU, and Liverpool Hope University. Combined with large NHS employers such as Royal Liverpool Hospital, this creates stable, year-round rental demand in areas like Wavertree, Kensington, and Edge Hill.

- Transportation and Connectivity Upgrades: Infrastructure projects like the Lime Street Station redevelopment, Merseyrail upgrades, and improved bus routes are making Liverpool more accessible, especially for outer boroughs and commuter zones. Investors targeting areas along these transit lines are seeing improved demand and price resilience.

- Tight Housing Supply and Low Construction Volumes: Despite visible cranes across the skyline, new-build delivery remains well below demand—particularly for mid-range, long-term rental stock. With land constraints in the city centre and complex planning approval processes, much of the capital appreciation in 2025 is occurring in the second-hand resale market, especially for upgraded terraced homes and converted flats.

- Yield-Driven Investment Migration: As yields in London and the South East compress, investors are increasingly targeting Liverpool for superior income performance. The combination of lower purchase costs and high rental demand has led to an influx of buy-to-let buyers from London, the Midlands, and overseas, particularly in value-growth zones like Anfield, Walton, and Kensington.

Liverpool Housing Market Forecast for 2026

The Liverpool Housing Market is expected to maintain upward momentum through 2026, driven by infrastructure-led regeneration, affordable pricing, and sustained rental pressure. While capital growth may moderate slightly compared to the post-pandemic rebound, Liverpool’s fundamentals continue to support strong investment conditions, particularly for yield-focused strategies.

For investors, 2026 presents an opportunity to benefit from stable price growth, expanding tenant demand, and favourable entry costs across Liverpool’s most active districts.

Property prices in Liverpool are projected to grow by 4.5% to 6.0% This growth will be led by areas benefitting from ongoing development and transport upgrades, including Baltic Triangle, Anfield, Toxteth, and parts of Kensington and Kirkdale. Continued regeneration in these neighbourhoods is expected to elevate both residential values and rental ceilings.

Liverpool’s affordability relative to other UK cities also supports consistent demand among first-time buyers and investors priced out of southern markets. Even as interest rates stabilise, the city’s average home price is forecast to reach approximately £182,000 to £185,000 by the end of 2026, assuming stable lending conditions and inflation control.

Prime central locations and city-centre apartments are expected to grow more modestly—by 3.0% to 4.0%—due to already-mature pricing and increased developer competition in the BTR sector.

Rental values are expected to increase by 5.0% to 6.5%, driven by persistent undersupply and a resilient tenant base. Growth will be strongest in Anfield, Kensington, Toxteth, and student-heavy districts such as Wavertree and Edge Hill, where competition for mid-range, energy-efficient flats remains intense.

- 1-bedroom flats in inner-city districts could reach £900/month

- 2-bedroom apartments are expected to average £1,150–£1,300/month, depending on location and finish

- Larger HMOs and terraced properties in Anfield and Walton may generate £1,600–£1,900/month in gross rental income

Gross yields are expected to remain in the 6.0% to 7.5% range for most value-growth districts, with lower returns of 4.5% to 5.5% in city-centre zones with higher upfront costs.

Development will remain limited relative to demand While BTR schemes and city-centre flats are in the pipeline, traditional resale stock—particularly terraced housing and converted HMOs—will continue to drive the bulk of rental investment activity. Limited land availability and planning delays are likely to constrain new housing starts outside key masterplans like Liverpool Waters.

Investor outlook remains positive. With limited policy friction, attractive price-to-rent ratios, and consistent population growth, investor sentiment toward Liverpool remains strong. Overseas investors, Northern-based landlords, and portfolio landlords are expected to remain active across the £100K–£250K segment.

In summary, the Liverpool Housing Market is forecast to deliver moderate capital appreciation and robust rental income throughout 2026. Investors targeting long-term buy-to-let strategies, especially in regeneration corridors, will continue to benefit from a stable, high-yield urban market with room for further price growth.

Is It Worth Buying a Property in Liverpool?

Yes—Liverpool remains a solid investment location for buyers prioritising high rental yields, long-term tenant demand, and low entry prices. However, while the fundamentals are strong, investors should be realistic about expected capital growth, regulatory complexity in licensing zones, and location-specific risks.

The city consistently ranks among the highest-yielding property markets in the UK, with gross returns ranging from 6.0% to 8.0% in key districts such as Anfield, Kensington, Walton, and Toxteth. Property prices in these areas typically sit well below £200,000, allowing investors to acquire income-producing assets with comparatively low capital outlay.

Rental demand is stable and growing, underpinned by student populations, NHS employment, and post-pandemic migration from more expensive UK regions. The ongoing regeneration of Liverpool Waters, Baltic Triangle, and the Knowledge Quarter is expected to enhance medium- to long-term value appreciation, particularly for investors entering early into up-and-coming areas.

That said, not all zones offer the same return profile. Investors must be mindful of:

- Slower capital growth in fully priced central areas with oversupply of new-build flats

- Selective licensing requirements, which apply to many high-yield districts and add compliance and admin costs

- Higher tenant turnover in student-heavy neighborhoods, which can affect vacancy rates and maintenance budgets

- Regulatory tightening on short-term lets and HMOs, especially in Kensington, Edge Hill, and Toxteth

For many landlords, the strongest opportunities lie in resale terraced housing or small blocks of flats in value-growth corridors, particularly in districts where rental demand exceeds available inventory. Cash buyers and those with value-add renovation experience will find especially attractive returns in the £100K–£160K range.

Other Market Forecasts & Overviews

London Real Estate Market Overview & Forecast

Manchester Real Estate Market Overview & Forecast

Bristol Real Estate Market Overview & Forecast

Derby Real Estate Market Overview & Forecast

FAQ

Is Liverpool a good place to invest in property in 2025?

Yes. Liverpool offers strong rental yields, low entry prices, and high tenant demand.

What is the average house price in Liverpool in 2025?

Around £174,000, significantly below the UK average.

Where are the best areas to invest in Liverpool?

Anfield, Kensington, Toxteth, Wavertree, and the Baltic Triangle offer the best yield-to-price ratios.

What rental yields can I expect in Liverpool?

Typical yields range from 6.0% to 8.0%, depending on location and property type.

Can foreigners buy property in Liverpool?

Yes. The UK has no restrictions on foreign ownership of residential property.

Are there rent caps in Liverpool?

No. Liverpool does not currently impose rent caps, but licensing applies in some areas.

Is short-term letting allowed in Liverpool?

Yes, but certain city-centre areas face increased regulation. Long-term letting is more stable.

Which property types perform best in Liverpool?

2-3 bedroom terraces and HMOs in high-demand districts typically offer the best returns.