Estate planning for serious wealth comes down to two heavyweights: Family Limited Partnerships and Trusts. Both are built to preserve, protect, and pass on wealth across generations. Both offer asset protection, tax advantages, and estate planning power. But they work very differently under the hood, and picking the wrong one for your situation can cost you more than you’d expect.

Financial markets are more complex than ever, and as global wealth grows, so does the pressure on high-net-worth families to make the right structural decisions. FLPs and Trusts each have real strengths and genuine limitations. Choosing the right one, or knowing when to combine both, can make or break your long-term estate planning strategy.

This guide gives you a clear, side-by-side look at Family Limited Partnerships and Trusts. You’ll see how each one works, what benefits it delivers, where it falls short, and which scenarios it’s best suited for. Whether you’re an investor, a business owner, or simply someone serious about securing your family’s financial future, understanding these two structures is non-negotiable.

Here’s what we’ll cover across this guide

- How each structure operates

- When each is most effective

- The key differences that set them apart

- Which option might be best suited for high-net-worth individuals

By the time you finish reading, you’ll have a clear picture of which structure fits your financial goals, your risk tolerance, and your long-term estate planning vision.

Table of Contents

What Is a Family Limited Partnership (FLP)?

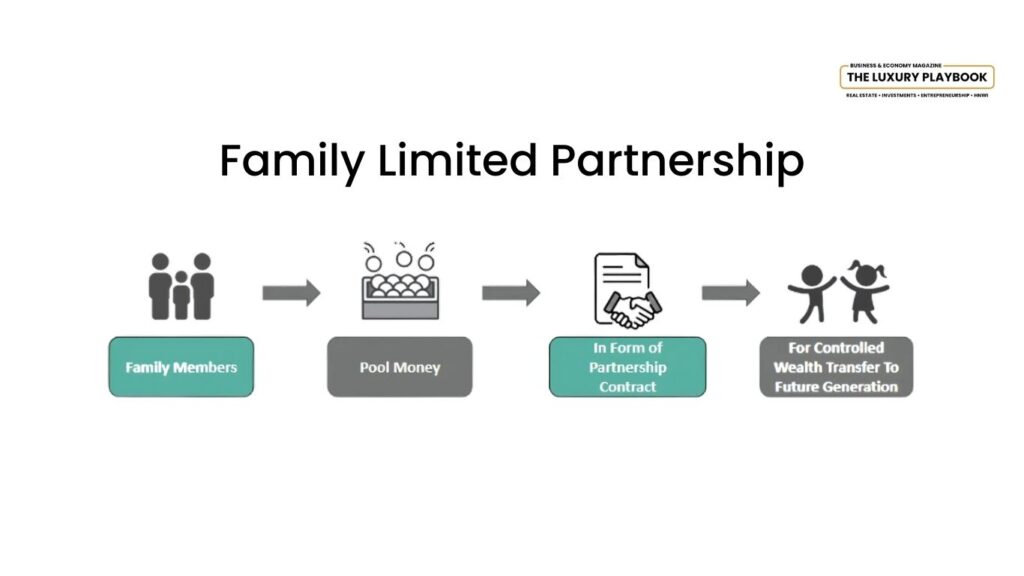

A Family Limited Partnership is a legal structure built specifically to protect family wealth, simplify estate planning, and provide asset protection that spans generations. It lets family members pool their assets into a single legal entity, with clearly defined roles for managing and distributing those assets. High-net-worth families, business owners, and individuals with substantial real estate or investment portfolios use this structure regularly.

Structure of a Family Limited Partnership

An FLP is built around two primary roles

- General Partners (GPs): Typically, senior family members who control and manage the assets within the partnership. They make investment decisions, handle operations, and oversee day-to-day activities. General Partners also bear unlimited liability for the partnership’s debts and obligations.

- Limited Partners (LPs): Usually, younger family members or heirs who own a percentage of the partnership but have no say in daily operations or decision-making. Limited Partners’ liability is restricted to their capital contribution, protecting their personal assets from any partnership-related debts.

Core Purpose of an FLP

The core purpose of a Family Limited Partnership is to preserve and transfer family wealth efficiently while keeping taxes low and protecting assets from potential creditors.

The key objectives of an FLP include

- Asset Protection: FLPs safeguard family wealth by making it harder for creditors to access partnership assets.

- Estate Tax Reduction: By transferring partnership interests to heirs, families can minimize estate and gift taxes.

- Centralized Management: General Partners maintain control over assets, even as ownership interests are distributed among family members.

- Wealth Transfer: FLPs facilitate generational wealth transfer without triggering excessive tax liabilities.

- Privacy: FLPs are not publicly disclosed, allowing families to keep their financial details private.

Types of Assets Typically Held in an FLP

FLPs can hold a wide variety of assets, including

- Real estate properties

- Investment portfolios (stocks, bonds, mutual funds)

- Family-owned businesses

- Cash reserves

- Intellectual property

Family members contribute these assets, and they are managed collectively under the partnership agreement.

FLPs are governed by state partnership laws and must comply with both federal and state tax regulations. Partnerships are pass-through entities, so the partnership itself pays no taxes. Profits and losses flow directly to individual partners, who report them on their personal tax returns.

When ownership interests are transferred to limited partners such as younger family members, those interests may qualify for valuation discounts based on lack of control or lack of marketability. That discount reduces the taxable value of those interests for estate and gift tax purposes, which is one of the structure’s most powerful financial benefits.

Advantages of a Family Limited Partnership

- Control: General Partners retain decision-making authority.

- Asset Protection: Creditors face significant legal hurdles in accessing FLP assets.

- Tax Benefits: Potential discounts on estate and gift taxes through valuation strategies.

- Efficient Wealth Transfer: Allows gradual transfer of assets while maintaining control.

- Privacy: Financial details remain confidential.

Disadvantages of a Family Limited Partnership

- Complexity: Establishing and maintaining an FLP requires legal and financial expertise.

- Unlimited Liability for GPs: General Partners are personally liable for partnership obligations.

- IRS Scrutiny: Aggressive valuation discounts may invite audits and legal challenges.

- Ongoing Compliance Costs: Annual filings, administrative costs, and legal fees can add up.

How Does a Family Limited Partnership Work?

A Family Limited Partnership operates as a legal and financial entity built to consolidate, protect, and manage family wealth while making tax-efficient transfers across generations much smoother. Its structure creates a clear divide between those who control the assets (General Partners) and those who benefit from them (Limited Partners). Here’s a close look at how an FLP actually functions.

1. Formation of an FLP

Creating an FLP starts with formal legal documentation, typically prepared with estate planning attorneys and financial advisors. The steps usually include

- Drafting a partnership agreement outlining roles, responsibilities, and operational guidelines.

- Defining the roles of General Partners (GPs) and Limited Partners (LPs).

- Registering the partnership with the appropriate state regulatory body.

- Contributing assets to the partnership, which may include real estate, investment portfolios, cash reserves, or family-owned businesses.

Once established, the partnership becomes a legal entity separate from the individual partners, providing a layer of liability protection and operational clarity.

2. Role of General Partners (GPs)

General Partners, often senior family members, retain control over the management and decision-making within the FLP. Their responsibilities include

- Overseeing day-to-day operations and investments of the FLP.

- Making decisions about asset allocation, property management, and financial strategies.

- Managing financial records and annual tax filings.

- Ensuring the FLP remains compliant with legal and regulatory requirements.

That said, General Partners bear unlimited liability for the debts and obligations of the partnership.

3. Role of Limited Partners (LPs)

Limited Partners, often younger family members or heirs, act as passive investors in the FLP. They

- Contribute capital or assets to the partnership.

- Receive proportional shares of profits or distributions from the FLP.

- Have no control or voting rights regarding management decisions.

- Enjoy limited liability, which restricts their financial risk to their capital contributions.

4. Asset Transfer and Ownership Structure

Assets contributed to the FLP are legally owned by the partnership itself, not by individual family members. This creates a legal barrier that protects those assets from creditors and helps avoid probate upon the death of General Partners.

General Partners can also gradually transfer ownership shares to Limited Partners, often children or grandchildren, through gifting strategies. These transfers are frequently eligible for valuation discounts based on lack of control and lack of marketability, effectively lowering estate and gift tax liabilities in the process.

5. Income and Profit Distribution

FLPs are pass-through entities for tax purposes, meaning the partnership itself pays no taxes. Instead

- Profits and losses are passed on to the individual partners based on their ownership percentage.

- Limited Partners typically receive passive income from the partnership.

- General Partners can allocate profits strategically to optimize tax outcomes for the family.

6. Asset Protection Mechanisms

One of the strongest advantages of an FLP is asset protection. Assets within the partnership are generally shielded from creditors, since Limited Partners’ ownership interests are considered illiquid and difficult to value.

- Creditors cannot directly seize partnership assets.

- They can only obtain a “charging order”, allowing them to claim distributions if and when they are made to a Limited Partner.

This creates a meaningful deterrent for litigation and significantly enhances the security of family wealth.

7. Estate and Gift Tax Advantages

The FLP structure opens the door to tax-efficient wealth transfer strategies, including

- Valuation Discounts: Limited Partnership shares often qualify for discounts (typically 15%–35%) due to their lack of control and limited marketability.

- Annual Gifting Exclusions: General Partners can transfer partnership shares to heirs each year up to the annual gift tax exclusion limit without incurring taxes.

These strategies can dramatically reduce the taxable value of an estate, preserving far more wealth for your heirs.

8. Ongoing Maintenance and Compliance

For an FLP to keep its legal and tax benefits intact, it must meet ongoing administrative requirements, including

- Filing annual tax returns for the partnership.

- Maintaining accurate financial records.

- Following partnership agreement terms without blurring the lines between personal and partnership assets.

- Conducting regular partnership meetings and recording minutes.

Take this scenario as an example. A family owns a $5 million commercial property. Rather than holding it outright, they transfer the property into an FLP

- The parents become General Partners and retain control over property management.

- The children become Limited Partners and own shares in the FLP.

- Over time, the parents gift shares of the FLP to their children, leveraging valuation discounts to reduce taxable gift values.

- Rental income from the commercial property flows through the FLP and is distributed according to ownership shares.

In this scenario, the family keeps control, minimizes estate taxes, and protects their assets, all while building a clean mechanism for generational wealth transfer.

When Are Limited Partnerships Generally Used?

Family Limited Partnerships are powerful tools in estate planning, wealth preservation, and asset protection. Their flexibility, combined with real tax advantages, makes them highly attractive to families and individuals with substantial financial assets. But their effectiveness depends on specific situations where the structure genuinely aligns with a family’s financial goals and long-term plans.

One of the most common uses of an FLP is estate planning. High-net-worth families often face steep estate taxes when passing wealth to the next generation. Through an FLP, you can systematically transfer ownership interests to your heirs while keeping control over the assets. Valuation discounts are the key mechanism here, reducing the taxable value of transferred shares. A limited partnership interest passed to your children, for example, may be valued at a discount due to restrictions on control and marketability, which can meaningfully lower estate and gift tax liabilities.

Asset protection is another major application. Assets held within an FLP are generally shielded from creditors. If a family member faces a lawsuit, creditors cannot directly seize partnership assets. Instead, they are limited to obtaining a charging order, which only entitles them to any distributions made to that specific partner. That layer of protection discourages litigation and keeps family wealth intact even when the financial environment gets difficult.

FLPs are also widely used for business succession planning. Family-owned businesses often hit serious turbulence during generational transitions. Without a clear structure in place, those transitions can trigger disputes, loss of control, or outright mismanagement. An FLP gives you a formalized mechanism for passing ownership and decision-making authority to the next generation while allowing senior family members to maintain operational control as General Partners, ensuring continuity and stability for the family business.

Beyond estate planning, asset protection, and business succession, FLPs are effective tools for managing family investment and real estate portfolios. Families with large real estate holdings, investment portfolios, or other valuable assets often use FLPs to consolidate ownership under one entity. This simplifies management, improves efficiency, and creates a more organized structure for financial reporting and taxation. Rather than managing multiple rental properties separately, for instance, a family can pool them under a single FLP for centralized management and streamlined tax filings. If you’re weighing whether buying property to rent out fits your strategy, an FLP can make the holding structure far more efficient.

FLPs are also used in philanthropic planning. Families with charitable goals often structure their FLPs to include a giving component. By gifting limited partnership shares to charitable organizations, you can generate tax benefits while supporting causes that matter to your family. This approach lets you leave a legacy beyond financial wealth in a structured, tax-efficient way.

There are also legal and regulatory reasons families choose an FLP. In jurisdictions with favorable partnership laws, FLPs offer legal protections that simply aren’t available under other estate planning tools. Some states provide stronger defenses against creditor claims for assets held within an FLP, making them especially attractive for families concerned about potential litigation.

FLPs are not a one-size-fits-all solution. They work best for families with significant assets, typically several million dollars or more. Smaller estates may find that the administrative costs, legal fees, and regulatory requirements outweigh the benefits. FLPs also attract increased IRS scrutiny, particularly when aggressive valuation discounts are applied to transferred shares. Proper documentation, compliance, and professional oversight are essential to keeping everything clean.

In short, FLPs are most commonly used for estate planning, asset protection, business succession, investment management, and philanthropic goals. They shine when families need centralized control, tax efficiency, and legal protection for complex assets. But their effectiveness depends entirely on proper structuring, disciplined administration, and alignment with your family’s financial objectives. When implemented thoughtfully and managed professionally, an FLP becomes one of the most powerful tools available for preserving and transferring family wealth across generations.

What is a Trust?

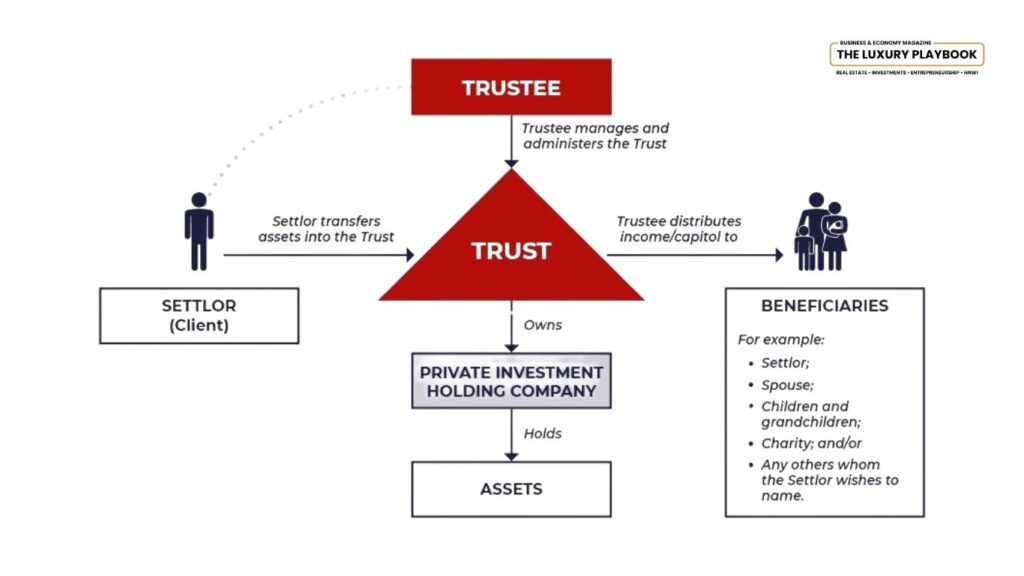

A Trust is a legal arrangement where a person, known as the Grantor or Settlor, transfers ownership of assets to a Trustee who manages them for the benefit of designated Beneficiaries. Trusts are widely used for estate planning, asset protection, and wealth management, offering flexibility, privacy, and meaningful tax advantages. They are essential tools for individuals and families who want real control over how their assets are distributed and managed, both during their lifetime and after their death.

At its core, a Trust creates a fiduciary relationship between the Grantor, the Trustee, and the Beneficiaries. The Grantor establishes the terms of the Trust, laying out exactly how the assets should be managed, distributed, and protected. The Trustee is legally bound to follow those instructions while acting in the best interests of the Beneficiaries. That legal obligation ensures the assets are handled responsibly and precisely according to the Grantor’s intentions.

Core Components of a Trust

Every Trust is built around three primary components

- Grantor: The individual who creates the Trust and transfers assets into it. The Grantor defines the terms and conditions under which the assets will be managed and distributed.

- Trustee: The party responsible for managing the Trust’s assets and ensuring compliance with the Grantor’s wishes. The Trustee can be an individual, a professional trustee, or a financial institution.

- Beneficiaries: The individuals or entities designated to benefit from the Trust’s assets. Beneficiaries can include family members, charities, or even future generations not yet born.

The primary purpose of a Trust is to provide control, protection, and strategic distribution of assets. Trusts are highly customizable and can be tailored to meet specific objectives, such as

- Avoiding Probate: Assets held in a Trust bypass the probate process, ensuring a faster, private, and more cost-effective transfer of wealth to beneficiaries.

- Reducing Estate Taxes: Certain types of Trusts can reduce estate tax liabilities, preserving more wealth for beneficiaries.

- Asset Protection: Trusts can shield assets from creditors, lawsuits, or divorce settlements.

- Providing for Minor Beneficiaries: Trusts can be set up to manage and distribute assets to minors until they reach a specified age or milestone.

- Supporting Charitable Goals: Charitable Trusts allow Grantors to contribute to causes they care about while enjoying tax benefits.

When a Grantor transfers assets into a Trust, legal ownership of those assets moves to the Trust itself. This separation of ownership serves two key purposes

- Asset Protection: Assets within the Trust are often protected from creditors or legal claims against the Grantor or Beneficiaries.

- Structured Distribution: The Trustee follows the instructions set forth in the Trust agreement to distribute income or principal to Beneficiaries.

For example, a Grantor may set up a Trust stipulating that assets are distributed to their children when they reach age 25. In the meantime, the Trustee manages and invests those assets, and may distribute income as per the Trust’s terms.

Types of Assets Typically Held in Trusts

Trusts can hold a variety of assets, including

- Real estate properties

- Investment portfolios (stocks, bonds, and mutual funds)

- Cash and savings accounts

- Life insurance policies

- Intellectual property

The flexibility of Trusts lets Grantors manage diverse asset types under a single structure, simplifying estate planning and ensuring cohesive management across the board.

Tax Implications of Trusts

Trusts can deliver real tax benefits depending on how they are structured. For instance

- Irrevocable Trusts can reduce estate tax exposure by removing assets from the Grantor’s taxable estate.

- Charitable Trusts offer both income and estate tax benefits when assets are transferred to a charitable organization.

- Grantor Trusts may allow income generated by Trust assets to be taxed at the Grantor’s individual tax rate, often resulting in favorable tax treatment.

But Trusts are also subject to complex tax rules, and improper structuring can create unintended tax consequences. Working with experienced estate planning professionals when setting up a Trust is not optional. It’s essential.

Benefits of a Trust

Trusts offer several distinct advantages in estate planning and wealth management

- Control Over Asset Distribution: Grantors can set conditions on when and how assets are distributed to Beneficiaries.

- Probate Avoidance: Assets bypass probate, resulting in faster and private distribution.

- Estate Tax Reduction: Properly structured Trusts minimize estate tax exposure.

- Protection from Creditors: Assets in certain Trusts are shielded from creditor claims.

- Support for Minor Beneficiaries: Assets can be managed until minors reach a specified age.

Limitations of a Trust

Despite their benefits, Trusts come with certain limitations

- Costly Setup and Maintenance: Establishing and maintaining a Trust involves legal fees, administrative costs, and ongoing compliance requirements.

- Complexity: Trusts can be legally and administratively complex, requiring professional oversight.

- Limited Flexibility (for Irrevocable Trusts): Once assets are placed in an Irrevocable Trust, changes are typically not allowed.

Types of Trusts

Trusts are among the most versatile tools in estate planning, offering a wide range of options tailored to specific financial, legal, and personal goals. Understanding the different types of trusts is critical for choosing the right structure to protect your assets, minimize taxes, and ensure a seamless transfer of wealth across generations. Below, you’ll find the most common types of trusts, their features, and the situations where each one excels.

1. Revocable Trusts. A Revocable Trust, also known as a Living Trust, lets the Grantor retain control over the trust assets during their lifetime. You can modify, amend, or revoke the trust at any time as long as you remain mentally competent.

Key Features:

- The Grantor can act as the initial Trustee, managing their own assets within the trust.

- Assets in the trust bypass probate upon the Grantor’s death, ensuring a quicker and more private transfer to beneficiaries.

- The trust becomes irrevocable upon the Grantor’s death, locking in the distribution terms.

Best For: Anyone who wants to avoid probate, maintain privacy, and keep control over their assets during their lifetime.

2. Irrevocable Trusts. An Irrevocable Trust cannot be modified or revoked once established without the consent of the beneficiaries and, in many cases, court approval. Once assets are transferred in, they are legally removed from the Grantor’s estate.

Key Features:

- Provides significant estate tax benefits by reducing the taxable estate.

- Offers strong asset protection against creditors and lawsuits.

- Income generated by the trust assets is taxed separately from the Grantor’s income.

Best For: Individuals seeking tax-efficient wealth transfer, strong asset protection, and reduced estate tax liability.

3. Testamentary Trusts. A Testamentary Trust is created through a will and only comes into effect after the Grantor’s death. It allows you to specify exactly how your assets should be distributed to beneficiaries.

Key Features:

- Established as part of a will and becomes active upon probate completion.

- Often used to manage assets for minor children or dependents.

- Provides control over the timing and conditions of distributions.

Best For: Anyone who wants structured asset distribution after their death, especially when minor children are involved.

4. Charitable Trusts. A Charitable Trust is designed to benefit charitable organizations while providing tax advantages to the Grantor. These trusts can be structured as either Charitable Remainder Trusts or Charitable Lead Trusts.

Key Features:

- Grants estate and income tax deductions for the Grantor.

- Allows assets to benefit both charitable organizations and designated beneficiaries.

- Provides ongoing support for causes aligned with the Grantor’s values.

Best For: Individuals with philanthropic goals who also want estate and income tax benefits.

5. Special Needs Trusts. A Special Needs Trust is designed to provide financial support to an individual with physical or mental disabilities without jeopardizing their eligibility for government assistance programs like Medicaid or Supplemental Security Income.

Key Features:

- Funds can be used for medical care, education, and personal needs.

- Preserves the beneficiary’s access to government benefits.

- Managed by a Trustee who ensures funds are used appropriately.

Best For: Families with dependents who require lifelong care or support.

6. Asset Protection Trusts. An Asset Protection Trust is designed to shield your assets from creditors, lawsuits, or legal claims. These trusts are often established in jurisdictions with favorable asset protection laws.

Key Features:

- Provides strong legal protection for trust assets.

- Often irrevocable to ensure protection.

- Common in offshore jurisdictions but also available domestically in certain U.S. states.

Best For: Individuals in high-risk professions or anyone facing a serious threat of litigation.

7. Spendthrift Trusts. A Spendthrift Trust prevents beneficiaries from burning through their inheritance by limiting their access to the trust principal. The Trustee controls distributions and can restrict access if a beneficiary shows signs of financial irresponsibility.

Key Features:

- Protects assets from creditors of the beneficiary.

- Prevents beneficiaries from making poor financial decisions.

- Trustee has control over asset distribution.

Best For: Parents or Grantors who are concerned about beneficiaries mismanaging inherited wealth.

8. Dynasty Trusts. A Dynasty Trust, also known as a Generation-Skipping Trust, is built to preserve wealth across multiple generations while minimizing estate taxes at each point of transfer.

Key Features:

- Assets remain in the trust for generations without incurring additional estate taxes.

- Provides long-term financial security for future heirs.

- Typically irrevocable and managed by a Trustee.

Best For: Families with significant wealth looking to lock in multi-generational financial stability.

9. Qualified Terminable Interest Property (QTIP) Trust. A QTIP Trust lets a Grantor provide for a surviving spouse while ensuring the remaining assets ultimately pass to other designated beneficiaries, such as children from a previous marriage.

Key Features:

- Provides income to the surviving spouse during their lifetime.

- Ensures remaining assets are distributed according to the Grantor’s wishes.

- Offers estate tax advantages.

Best For: Individuals in blended families or anyone who wants precise control over wealth distribution after the death of a spouse.

The right Trust depends on factors like your financial goals, family structure, asset types, and risk tolerance. For example

- A Revocable Trust is ideal for individuals seeking flexibility and control.

- An Irrevocable Trust works well for estate tax reduction and asset protection.

- A Special Needs Trust is essential for families with dependents requiring long-term care.

How Does a Trust Work?

A Trust operates as a legal arrangement where assets are transferred from a Grantor to a Trustee, who manages them for the benefit of specific Beneficiaries. This arrangement lets the Grantor control how assets are distributed, protect them from creditors, and potentially reduce tax liabilities. The way it functions depends on its type, terms, and objectives, but the core principles are consistent across all variations.

1. Establishing the Trust

The process begins with the Grantor creating the trust document, a legally binding agreement that outlines

- The assets being transferred into the trust (e.g., real estate, cash, investments).

- The roles and responsibilities of the Trustee in managing those assets.

- The beneficiaries and their entitlements (who gets what and under what conditions).

- Any specific instructions or restrictions on how the assets should be managed or distributed.

The trust document is the foundation of the entire arrangement. It defines exactly how the Trustee must act and what powers they hold in managing trust assets.

2. Transferring Assets into the Trust

Once the trust is legally established, the Grantor transfers ownership of their chosen assets into it. These assets might include real estate, financial accounts, stocks, or valuable personal property. The transfer process varies depending on the asset type

- Real Estate: Ownership deeds are reissued in the trust’s name.

- Bank Accounts: Accounts are retitled under the trust’s ownership.

- Investment Portfolios: Brokerage accounts are updated to reflect trust ownership.

This transfer is critical because only assets legally titled in the name of the trust are protected and governed by its terms.

3. Role of the Trustee

The Trustee is the individual or institution responsible for managing the trust’s assets according to the instructions set out in the trust agreement. Trustees can be

- Individuals: Such as a trusted family member or friend.

- Professional Trustees: Banks, law firms, or financial institutions.

The Trustee’s responsibilities typically include

- Managing and investing assets prudently.

- Ensuring compliance with trust terms and legal requirements.

- Distributing income or principal to beneficiaries based on the terms of the trust.

- Keeping accurate financial records and preparing tax filings.

Trustees have a fiduciary duty to act in the best interests of the beneficiaries at all times, prioritizing their needs and adhering strictly to the trust’s directives.

4. Beneficiaries and Asset Distribution

Beneficiaries are the individuals or entities who will benefit from the assets held within the trust. The trust agreement specifies

- Who the beneficiaries are (e.g., children, grandchildren, charities).

- When and how distributions will occur (e.g., upon reaching a certain age, achieving a milestone, or under specific conditions).

- The type of benefits provided: Income from investments, lump-sum payments, or ongoing financial support.

For example, a trust might stipulate that a child receives monthly distributions for living expenses until they turn 25, at which point they gain access to a portion of the trust’s principal.

5. Taxation of Trusts

Trust taxation varies depending on whether the trust is Revocable or Irrevocable

- Revocable Trusts: Income generated by assets in the trust is taxed as part of the Grantor’s personal income.

- Irrevocable Trusts: The trust is considered a separate legal entity and is taxed separately.

Charitable trusts and special needs trusts may also qualify for unique tax deductions or exemptions. Smart tax management within a trust can meaningfully reduce estate taxes, income taxes, and capital gains taxes. For a broader look at managing wealth efficiently, understanding how to invest during inflation is a useful complement to trust planning.

6. Probate Avoidance

One of the most compelling advantages of a trust is its ability to bypass the probate process entirely. Assets held in a trust are not subject to probate upon the Grantor’s death, allowing for

- Faster asset distribution.

- Greater privacy, as probate proceedings are public records.

- Reduced legal costs associated with estate settlement.

This feature is especially valuable for families who want efficient and private wealth transfers without public court proceedings.

7. Asset Protection

Trusts offer varying degrees of asset protection depending on their structure and jurisdiction. For example

- Irrevocable Trusts protect assets from creditors and lawsuits.

- Spendthrift Trusts safeguard beneficiaries from poor financial decisions and external claims.

The ability to shield assets from external threats makes trusts a popular choice among individuals in high-risk professions or those sitting on substantial personal wealth.

8. Ongoing Trust Management

Trusts require ongoing management and oversight, which includes

- Regular financial audits and reviews to ensure assets are performing optimally.

- Timely distributions to beneficiaries in line with the trust’s instructions.

- Compliance with legal and regulatory requirements, including annual tax filings.

Professional Trustees or financial advisors are often brought in to ensure the trust stays compliant and continues to serve its intended purpose effectively.

Picture a wealthy individual who establishes a Revocable Trust and transfers their assets, including property and an investment portfolio, into it. During their lifetime, they act as Trustee, managing the assets and using them for personal needs. Upon their death, the trust automatically becomes Irrevocable, and their appointed successor Trustee takes over.

The successor Trustee follows the trust’s instructions, distributing regular income from the investment portfolio to the Grantor’s children while preserving the principal for future generations. Because the assets bypass probate entirely, the children receive their inheritance quickly and privately.

Key Differences Between Family Limited Partnerships vs. Trusts

When you’re deciding between a Family Limited Partnership and a Trust, you need a clear picture of how they differ in structure, purpose, management, and benefits. Both tools are effective for wealth preservation, asset protection, and estate planning. But they operate under distinct legal frameworks and serve different purposes. Here’s a breakdown of the key differences to help you understand the unique role each one plays.

1. Structure and Roles

Family Limited Partnership. An FLP is a legal business entity with two primary types of partners: General Partners and Limited Partners. General Partners manage the partnership and carry unlimited liability, while Limited Partners are typically passive investors with liability limited to their capital contribution.

Trust. A Trust is a fiduciary arrangement where a Trustee holds and manages assets on behalf of Beneficiaries. The Grantor sets the terms, and the Trustee ensures compliance with those instructions. Unlike an FLP, Beneficiaries generally have no management authority.

Key Difference. FLPs are managed by General Partners with real decision-making authority, while Trusts are overseen by Trustees who must follow the trust agreement to the letter.

2. Purpose

Family Limited Partnership. FLPs are primarily used for asset protection, tax-efficient wealth transfer, and centralized management of family assets. They are especially powerful for families with significant real estate, businesses, or investment portfolios.

Trust. Trusts focus more on estate planning, probate avoidance, privacy, and tax efficiency. They are commonly used to control distributions to beneficiaries, protect vulnerable heirs, or reduce estate tax exposure.

Key Difference. FLPs put the emphasis on control and asset protection, while Trusts lean toward distribution, privacy, and long-term estate planning.

3. Control Over Assets

Family Limited Partnership. Control stays in the hands of General Partners, even when ownership interests are transferred to Limited Partners. This lets senior family members retain authority over decisions and management while gradually handing ownership to heirs.

Trust. Control over assets depends on the type of Trust. In a Revocable Trust, the Grantor can retain control during their lifetime. In an Irrevocable Trust, control transfers fully to the Trustee.

Key Difference. FLPs offer active management by General Partners, while Trusts either keep control with the Grantor (Revocable) or fully hand it to the Trustee (Irrevocable).

4. Tax Treatment

Family Limited Partnership. FLPs can offer valuation discounts typically ranging from 15% to 35% when transferring partnership shares to Limited Partners, reducing estate and gift taxes. Profits and losses pass through to partners and are taxed at their individual income tax rates.

Trust. Taxation depends on the type of Trust

- Revocable Trusts: Income is taxed at the Grantor’s personal tax rate.

- Irrevocable Trusts: Income is taxed as a separate entity, often at higher trust tax rates.

Key Difference. FLPs often deliver valuation discounts, while Trusts offer a mix of income tax flexibility and estate tax reduction depending on their structure.

5. Asset Protection

Family Limited Partnership. Assets within an FLP are generally protected from creditors. Creditors cannot directly seize those assets but may obtain a charging order, which only allows access to distributions made to a debtor-partner. This makes FLPs a robust structure for shielding family wealth from lawsuits and financial liabilities.

Trust. Asset protection in Trusts varies based on the type. Irrevocable Trusts provide strong protection since assets are no longer considered part of the Grantor’s estate. Revocable Trusts, on the other hand, offer little to no asset protection because the Grantor retains control.

Key Difference. FLPs create legal barriers through charging orders, while Irrevocable Trusts shield assets by removing them from the Grantor’s ownership entirely.

6. Flexibility

Family Limited Partnership. FLPs offer real flexibility in management, asset allocation, and wealth transfer strategies. General Partners can make investment and operational decisions without needing sign-off from Limited Partners.

Trust. Flexibility depends on the Trust type. Revocable Trusts are highly flexible, allowing changes during the Grantor’s lifetime. Irrevocable Trusts are rigid and generally cannot be altered once established.

Key Difference. FLPs are more flexible in management and investment strategies, while Revocable Trusts are flexible in structure but Irrevocable Trusts are not.

7. Probate Avoidance

Family Limited Partnership. FLPs do not inherently bypass probate. But assets owned by the partnership are not considered part of an individual’s personal estate and may avoid probate if ownership interests are properly structured.

Trust. Trusts, especially Revocable and Irrevocable Living Trusts, are specifically designed to bypass the probate process. Assets held within a Trust transfer directly to beneficiaries without public probate proceedings, saving time and costs.

Key Difference. Trusts are far more effective at avoiding probate, while FLPs require careful structuring to achieve similar results.

8. Costs and Maintenance

Family Limited Partnership. FLPs tend to have higher initial setup costs due to legal and administrative fees. Ongoing management, annual filings, and regulatory compliance add to those maintenance costs over time.

Trust. The cost of establishing a Trust varies based on complexity. Revocable Trusts are generally less expensive to maintain, while Irrevocable Trusts may require ongoing legal and financial oversight, especially when a professional Trustee is involved.

Key Difference. FLPs often carry higher initial costs and ongoing compliance requirements, while Trusts have variable costs depending on their type and complexity.

9. Privacy

Family Limited Partnership. FLPs offer a moderate level of privacy, as financial details are not typically disclosed publicly. But legal disputes or creditor claims can pull details into public view.

Trust. Trusts, especially Living Trusts, offer greater privacy because they avoid probate, which is a public process. The terms of the Trust and its assets stay confidential.

Key Difference. Trusts, and Living Trusts in particular, offer stronger privacy protection compared to FLPs.

10. Ideal Use Cases

Family Limited Partnership

- Effective for multi-generational wealth transfer while retaining control.

- Ideal for managing family-owned businesses, real estate portfolios, or large investment assets.

- Suitable for families concerned about creditor protection and tax efficiency.

Trust:

- Ideal for avoiding probate and ensuring privacy in estate distribution.

- Suitable for protecting vulnerable beneficiaries, such as minors or dependents with special needs.

- Effective for families focused on estate tax minimization and philanthropic goals.

Key Difference. FLPs are better suited for families managing complex assets that need centralized control, while Trusts excel in estate planning, probate avoidance, and tailored beneficiary protections.

| Aspect | Family Limited Partnership (FLP) | Trust |

|---|---|---|

| Structure | Managed by General Partners and owned by Limited Partners | Managed by a Trustee for beneficiaries |

| Control | General Partners retain active control | Depends on Trust type (Grantor or Trustee-controlled) |

| Tax Treatment | Pass-through taxation with valuation discounts | Varies (Grantor or separate entity taxation) |

| Asset Protection | Strong protection through charging orders | Stronger in Irrevocable Trusts |

| Flexibility | High operational flexibility | Flexible in Revocable Trusts, rigid in Irrevocable Trusts |

| Probate Avoidance | Requires careful structuring | Automatically bypasses probate |

| Cost & Maintenance | Higher initial and ongoing costs | Varies by Trust type |

| Privacy | Moderate privacy | Strong privacy in Living Trusts |

| Best For | Asset management, business succession, creditor protection | Estate planning, specific beneficiary goals, probate avoidance |

Which Is Ideal for High Net Worth Individuals?

Both Family Limited Partnerships and Trusts are valuable tools for high-net-worth individuals looking to manage, protect, and transfer wealth efficiently. But each structure serves distinct purposes, and choosing the right one depends on your specific financial goals, the types of assets you hold, and the dynamics of your family.

FLPs tend to appeal to individuals who want to keep control over their assets while gradually transferring ownership to heirs. General Partners in an FLP maintain authority over management and investment decisions, even as limited partnership shares are gifted to family members. This is especially valuable for families with complex assets like real estate portfolios, family businesses, or substantial investment holdings. Building a real estate portfolio through structured ownership is one area where FLPs consistently outperform simpler arrangements. FLPs also deliver real estate tax benefits through valuation discounts, which can reduce the taxable value of transferred ownership interests by as much as 15% to 35%. That translates into significant tax savings while keeping senior family members firmly in the driver’s seat. The asset protection side is equally compelling. Creditors are generally limited to a charging order, meaning they can only access distributions made to a debtor-partner rather than seizing partnership assets outright. The catch is that FLPs carry higher administrative costs, ongoing compliance requirements, and potential IRS scrutiny if valuation discounts are pushed too aggressively.

Trusts bring a different set of strengths, with a sharper focus on structured wealth transfer, asset protection, and estate tax minimization. Revocable Trusts are the go-to for probate avoidance and privacy, since assets held within them bypass the public probate process upon the Grantor’s death. That means faster, more cost-effective, and more private transfers to your beneficiaries. Irrevocable Trusts go further, offering strong asset protection and estate tax advantages by removing assets from the Grantor’s estate entirely. That shield makes them ideal for long-term wealth preservation and creditor protection. Trusts also give you far more flexibility in designing distribution terms. You can set milestone-based access for beneficiaries, such as funds released at a certain age or tied to achieving specific educational goals. Still, Irrevocable Trusts can be rigid, and changing them after the fact often requires court approval or beneficiary consent.

From a tax perspective, both structures offer unique advantages. FLPs let income pass through to partners and be taxed at individual rates, while Trust taxation depends on whether the trust is revocable or irrevocable. Irrevocable Trusts are treated as separate tax entities, often taxed at higher rates in the short term but delivering long-term estate tax advantages. Privacy is another point of separation. FLPs offer moderate confidentiality but can become subject to public scrutiny in creditor or legal disputes. Trusts, especially Living Trusts, keep asset details and distribution plans out of the public record entirely.

For high-net-worth individuals focused on multi-generational wealth transfer, both structures can deliver, but they excel in different ways. FLPs are better suited for families with substantial, active assets requiring centralized management, such as real estate or business interests. Understanding how dividend-generating assets work within a structured entity can sharpen your FLP strategy considerably. Trusts, and Dynasty Trusts in particular, are ideal for preserving wealth across multiple generations while minimizing estate taxes at each transfer point. FLPs give you ongoing control and operational flexibility, while Trusts deliver structured asset protection and distribution tailored precisely to your wishes.

Ultimately, the choice comes down to your priorities. If control, active management, and tax-efficient transfer of complex assets are your primary goals, an FLP is likely the stronger option. If probate avoidance, asset protection, privacy, and long-term structured inheritance are what matter most, a Trust, and particularly an Irrevocable Trust, is probably more suitable. But the most effective strategy for high-net-worth individuals often combines both. An FLP can centralize and manage your assets, while shares of the FLP can be transferred into an Irrevocable Trust for added estate tax efficiency and creditor protection. This hybrid approach draws on the strengths of both tools, giving you control, flexibility, asset protection, and tax advantages in one cohesive plan. Looking ahead at which industries will dominate U.S. investment can also help you decide which asset types to prioritize within these structures.

For high-net-worth individuals navigating these decisions, professional guidance is not optional. Estate planning attorneys and financial advisors can craft a strategy that fits your unique family dynamics, asset mix, and long-term financial goals. Both Family Limited Partnerships and Trusts offer real power, but their success depends entirely on careful planning, strict compliance, and consistent ongoing management. With wealth preservation facing increasing legal, tax, and economic complexity, choosing the right structure, or the right combination of both, is how you ensure financial security and a lasting legacy for the generations that follow you.

FAQ

What type of trust is best for a family?

The best trust for a family depends on their goals. A Revocable Living Trust is ideal for flexibility, probate avoidance, and privacy, while an Irrevocable Trust offers asset protection and tax benefits. For families with dependents requiring special care, a Special Needs Trust ensures ongoing financial support without affecting government aid.