UK house prices spent much of 2025 trapped in an uncomfortable holding pattern, with buyers and sellers frozen by wave after wave of uncertainty. Political questions loomed large ahead of Labour’s autumn Budget, and speculation about potential property tax changes was enough to stop even the most motivated movers in their tracks.

Mortgage affordability was another weight on the market. Interest rates stayed elevated compared to the near-zero environment that defined the 2010s, and broader economic headwinds including stubborn inflation and weak GDP growth kept transaction volumes subdued. Price growth was minimal compared to the wild post-pandemic years, when values surged and crashed in rapid succession.

Then January 2026 arrived and shattered that cautious stagnation with a price surge that caught even seasoned market analysts off guard.

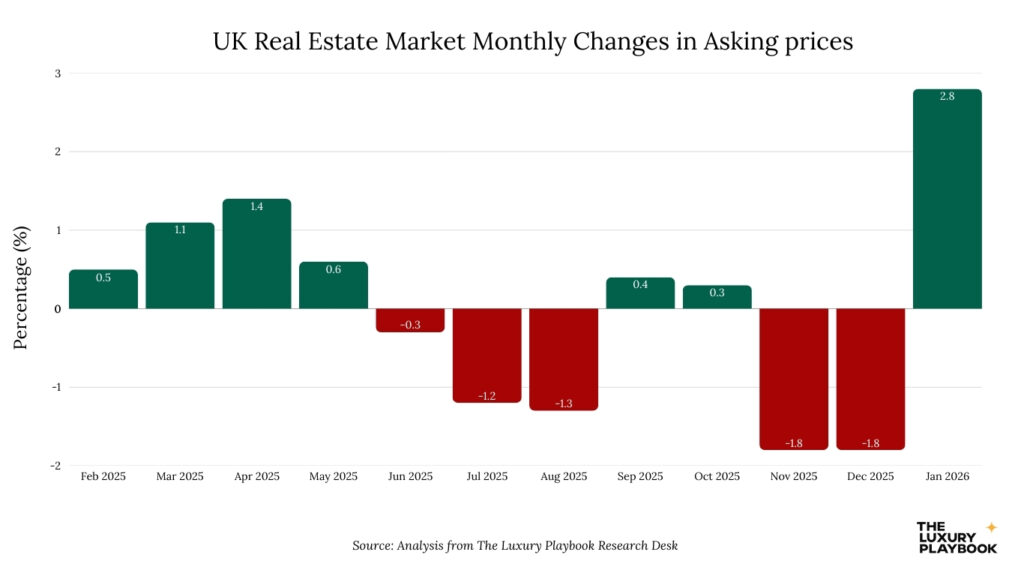

Nearly £10,000 was added to the average UK property asking price in just five weeks. That makes it the largest month-on-month increase recorded in a decade, reversing months of cautious pessimism that had defined the final quarter of 2025.

This dramatic acceleration came from a combination of forces. Budget uncertainty finally resolved, mortgage affordability improved, and pent-up demand from buyers who had delayed decisions throughout the previous year poured into the market with renewed confidence that the worst-case scenarios they feared simply would not materialize.

Table of Contents

Key Takeaways & The 5Ws

- UK asking prices jumped £9,893 (+2.8%) between December 2025 and January 2026, the biggest January rise in 25 years, snapping the market out of its 2025 freeze.

- Nationwide’s completed-sale data confirms real price growth, not just optimistic listings, with annual gains edging up to 1.0%.

- The move looks like a V-shaped rebound from Budget-driven weakness, taking prices back to mid-2025 levels rather than to new all-time highs.

- Northern England is leading, with roughly 4%–5.5% annual rises, while London and the South East are stagnating or slipping.

- Political clarity, cheaper mortgage rates, and months of pent-up demand support a baseline outlook of 2%–4% UK house price growth in 2026.

- Who is this for?

- UK homebuyers, sellers, landlords, and property investors tracking the 2026 UK housing market outlook and the widening gap between northern growth markets and weaker southern performance.

- What is happening?

- A sharp January 2026 rebound that added nearly £10,000 to average asking prices and was backed by improving completed-sale data—signaling a shift from stagnation to moderate, broader-based growth.

- When did the market turn?

- The key inflection is January 2026, after the November 2025 Budget and as mortgage rates eased—unlocking demand that had been stuck on the sidelines during the 2025 freeze.

- Where is the strength?

- Across the UK, but with Northern England hotspots (including Liverpool, Manchester, and Rochdale) outperforming, while London and the South East lag as affordability and weaker momentum cap upside.

- Why does it matter?

- Because Budget clarity plus improving mortgage deals released pent-up demand and reset sentiment, replacing 2025’s paralysis with a cautious baseline of 2%–4% growth for UK house prices in 2026—while regional dispersion becomes the real story.

£10,000 Added in Five Weeks and Record January Performance

The UK property market got a clear signal from Rightmove, the country’s largest property portal tracking asking prices across hundreds of thousands of active listings. Average prices jumped 2.8% month-on-month between December 2025 and January 2026. That £9,893 increase brought the typical UK property to £368,031, which is the largest price increase ever recorded for the month of January in Rightmove’s 25-year dataset stretching back to the early 2000s.

More telling is the context. This surge marked the biggest single-month rise since June 2015, a period when post-financial crisis recovery was still accelerating and the UK housing market was riding extraordinarily loose monetary policy and Help to Buy schemes that artificially stimulated demand.

Rightmove tracks asking prices, but Nationwide Building Society’s parallel index tracks actual completed sale prices. That distinction matters, and Nationwide’s data confirmed genuine market momentum rather than simply sellers getting ahead of themselves with optimistic listings.

Their index recorded a 0.3% monthly increase, bringing the average to £270,873, while annual growth accelerated from 0.6% in December 2025 to 1.0% in January 2026.

To understand this surge properly, you need to recognize that the recovery directly reversed a sharp November to December 2025 decline driven by Budget-related uncertainty. Asking prices had fallen from an August 2025 peak of around £368,000 to a trough near £358,000 by December, as buyers paused while awaiting Labour’s tax policy announcements on potential capital gains changes, mansion taxes, and stamp duty modifications that might reshape their purchase economics.

So January’s surge largely restored prices to mid-2025 levels rather than pushing the market into record high territory. What you’re looking at is a V-shaped recovery, where the Budget announcement broke the logjam and unleashed delayed transactions that would have happened earlier without the political uncertainty hanging over the market.

Buyer demand metrics confirmed this was genuine market activity rather than sellers raising prices in a vacuum. Demand rebounded with a 57% increase in buyer activity during the two weeks immediately after Christmas compared to the two weeks before the holiday. Rightmove also recorded its highest-ever Boxing Day website traffic, as property-hungry Britons spent their holiday browsing listings and scheduling viewings.

But beneath these encouraging national figures, regional disparities intensified in ways that reshape where real value and opportunity sit within the UK property market.

Northern England led growth, with cities including Liverpool, Manchester, and Rochdale recording annual gains of 4% to 5.5%. Relative affordability, strong local employment in technology and professional services, and a steady migration of younger professionals priced out of southern markets all fuelled that momentum.

London and Southeast markets told a very different story, with the capital recording negative 1% annual growth and some southern cities experiencing outright declines.

What Changed and What It Means for UK House Prices

The decisive factor that broke the market’s paralysis was the resolution of Budget uncertainty, which had frozen a substantial portion of potential movers throughout late 2025.

Labour’s November Budget introduced a new Mansion Tax imposing £2,500 annual charges on properties valued above £2 million, escalating to £7,500 for homes exceeding £5 million, with implementation scheduled for 2028. Additional property tax changes included modifications to capital gains treatment and adjustments to stamp duty thresholds affecting various market segments.

But the final measures proved substantially less punitive than the worst-case scenarios that had circulated through property industry circles. Analysts widely described the outcome as “better than feared,” and that shift in sentiment mattered enormously for buyer psychology.

Once buyers understood actual policy rather than worst-case speculation, roughly 20% of potential movers who had been waiting for clarity could finally proceed with transactions they had already mentally committed to but held back pending policy confirmation.

The result was an immediate demand spike as months of pent-up activity compressed into a few weeks. Estate agents reported viewing requests surging, and mortgage brokers fielded a wave of serious inquiries from buyers who had done their research and were ready to transact, not just explore options.

Mortgage affordability also played its part. Competitive pressure among lenders drove rates downward even as the Bank of England held base rates at levels that might otherwise suggest expensive borrowing. Average two-year fixed mortgage rates fell to 4.29% by late January 2026, down from 5.03% the year before. The most competitive deals available to borrowers with substantial deposits offered rates as low as 3.50% for two-year fixed terms and 3.72% for five-year products, which is the best affordability picture you’ve seen in three years.

Looking forward, market predictions for 2026 cluster in a remarkably narrow 2% to 4% growth range. That tells you professional forecasters expect steady appreciation rather than the boom-bust volatility that characterized recent years. If you’re thinking about evaluating a UK property move, this kind of consensus outlook is worth factoring into your timing.

Nationwide forecasts 2% to 4% growth, Rightmove predicts precisely 2%, while Savills expects 2% for the year with cumulative 25% growth through 2030 as the market enters a sustained but moderate upward trajectory. Even typically cautious Zoopla anticipates 1.5% appreciation, suggesting that even the bears have accepted at least modest growth as the base case.