Interest rates are one of the most powerful forces shaping the world of real estate investments. Whether you’re financing a single rental unit, managing a commercial property portfolio, or developing multifamily housing, the direction and level of interest rates can directly affect returns, pricing, and risk.

When interest rates shift—even by a fraction—it ripples through the entire real estate ecosystem. Borrowing costs rise or fall, influencing demand for housing, the value of income-producing assets, and the feasibility of new construction.

For investors, these rate changes can present both threats and opportunities, depending on the structure of their holdings and the strategies they use.

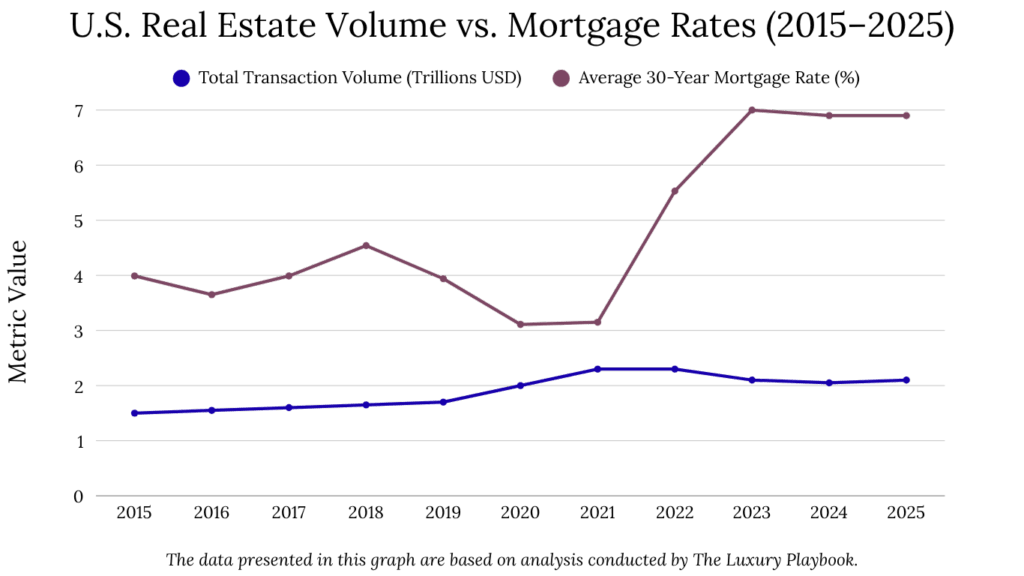

In recent years, real estate markets have been tested by rapid rate increases. Between early 2022 and mid-2024, central banks around the world raised benchmark rates at one of the fastest paces in modern history. In the United States, for example, the Federal Reserve pushed the federal funds rate from near-zero to over 5.25%.

As a result, 30-year fixed mortgage rates climbed above 7%, up from under 3% just two years earlier. This shift had a direct impact on homebuyer affordability, investor cash flows, and asset valuations across both residential and commercial sectors.

But it’s not all downside. Investors who understand how interest rates interact with real estate investments can adjust their strategies, identify value plays, and even capitalize on changing market conditions.

Table of Contents

What Are Interest Rates and How Do They Work?

At their core, interest rates represent the cost of borrowing money. When you take out a mortgage, finance a real estate development, or use leverage to acquire a property, the interest rate determines how much you’ll pay the lender in addition to the loan principal. That rate, however, doesn’t appear out of thin air—it’s influenced by a wide range of economic factors and monetary policy decisions.

Central banks like the Federal Reserve, the European Central Bank (ECB), or the Bank of England set what are known as benchmark interest rates—in the U.S., this is the federal funds rate. These benchmarks serve as the base cost of borrowing for financial institutions. When the Fed raises its rate, banks typically follow by increasing the rates they charge for everything from business loans to 30-year fixed-rate mortgages.

In the real estate world, this matters because nearly every transaction involves some form of borrowing. Whether you’re purchasing a single-family rental or funding a large-scale commercial development, your financing terms are directly influenced by the current interest rate environment.

When interest rates are low, borrowing is cheaper, which tends to increase demand for properties. On the flip side, higher interest rates increase financing costs, which can put downward pressure on both property values and investor returns.

To illustrate this, consider a $500,000 mortgage. At a 3% interest rate, monthly payments would hover around $2,100. At 7%, that same loan jumps to over $3,300. That’s a 57% increase in monthly debt service—a significant hit to cash flow, especially for investors relying on tight NOI margins.

Interest rates also affect yield expectations. In a low-rate environment, investors may accept lower cap rates because the cost of capital is cheap. But when rates rise, they often demand higher returns to justify the increased risk, which can depress asset prices.

Why Interest Rates Matter in Real Estate Investing

Interest rates are more than just numbers on a loan agreement—they shape how real estate investors think, plan, and act. From acquisition decisions to long-term holding strategies, rates directly influence the cost of capital, expected returns, and the overall feasibility of a deal.

For starters, the most immediate impact of rising interest rates is on financing costs. A small change in the rate can dramatically shift an investor’s monthly outlay. For example, a $1 million loan at 4% interest results in roughly $4,775 in monthly payments. If the rate climbs to 6%, that payment increases to about $5,995—an annual difference of nearly $15,000.

For investors operating on slim margins or relying on aggressive projections, this increase can make the difference between a profitable investment and a negative cash flow scenario.

But the effects go deeper than loan payments. Net Operating Income (NOI) is often pressured when landlords face higher interest costs on variable-rate loans or refinancing. If rental income doesn’t keep pace with debt service, returns shrink, and property valuations can decline.

This is particularly relevant in commercial real estate, where short-term debt is more common, and many investors rely on refinancing as part of their value-add strategy.

Another key area where interest rates matter is cap rate compression. In a low-rate environment, investors are willing to accept lower yields (lower cap rates) because financing is cheap and risk-free alternatives like government bonds offer little competition. But when interest rates rise, cap rates typically expand.

That means asset values often drop, even if rental income remains stable. For instance, a property generating $100,000 in annual NOI would be worth $2 million at a 5% cap rate, but only $1.66 million at 6%—a 17% decline simply due to changing rate expectations.

Furthermore, Loan-to-Value (LTV) ratios are influenced by rate shifts. Lenders may lower LTV thresholds when rates rise, making it harder for investors to borrow as much capital. This forces many to bring more equity to the table or walk away from deals that no longer pencil out under stricter lending standards.

How Rising Interest Rates Affect Property Prices

When interest rates rise, property prices often feel the pressure first. That’s because rising rates increase the cost of borrowing, which directly reduces what buyers can afford. Whether it’s a homebuyer using a mortgage or an investor financing a commercial property, higher interest payments lower purchasing power—and when buyers can’t pay as much, prices tend to adjust downward.

Let’s break that down. Suppose a buyer can afford $3,000 per month in mortgage payments.

At a 4% interest rate, they could borrow approximately $628,000. But if the rate increases to 6.5%, that same monthly budget only allows for a loan of about $473,000. That’s a difference of $155,000 in buying power. Multiply this effect across an entire market, and it’s easy to see why property prices can stagnate or decline as rates climb.

This effect isn’t limited to residential real estate. In the commercial world, pricing is often based on capitalized income, meaning properties are valued based on their net operating income (NOI) and prevailing cap rates. As we’ve seen, higher interest rates usually lead to higher cap rates. Since property value = NOI ÷ cap rate, any increase in the denominator (cap rate) reduces the overall valuation.

For example, a retail center generating $200,000 in NOI might be valued at $4 million using a 5% cap rate. But if market cap rates rise to 6.5% due to rate hikes, that same asset could be worth just over $3 million—a drop of nearly 25% in theoretical value.

Rising rates can also cool speculative demand. In a low-rate environment, investors often stretch on price, betting that future appreciation or rent growth will deliver returns. But when borrowing costs rise and appreciation slows, the appeal of overpaying fades quickly. This can lead to longer days on market, more price reductions, and a general softening in investor sentiment.

That said, not every market reacts the same way. Locations with strong fundamentals—such as low vacancy, high job growth, or limited housing supply—may still see price resilience. But overall, when interest rates rise, the direction of property prices tends to follow a downward or flattening trend, especially in highly leveraged segments of the market.

The Link Between Interest Rates and Mortgage Costs

Interest rates and mortgage costs are directly connected—when one goes up, so does the other. For real estate investors, this relationship can have a huge impact on cash flow, deal viability, and long-term profitability.

Most property purchases are financed using either a fixed or variable-rate mortgage. The interest rate on that mortgage determines how much you’ll pay each month in interest, on top of repaying the loan principal. So, even a small increase in rates can translate into significantly higher monthly expenses.

To illustrate this, consider a $400,000 loan. At a 3% fixed interest rate, the monthly principal and interest payment would be about $1,686. At 6.5%, that same loan costs around $2,528 per month—a jump of nearly $850. Over a 30-year term, that adds up to over $300,000 in additional interest paid. That’s not a rounding error—it’s a game-changer for investment planning.

For investors using leverage, these higher mortgage costs reduce Cash-on-Cash Return and overall Return on Investment (ROI). If the property doesn’t generate enough rental income to cover the increased debt service, net operating income (NOI) suffers. In some cases, deals that once looked promising can quickly become negative cash flow traps.

Mortgage costs also influence investment strategy. In low-rate environments, investors may favor longer-term fixed-rate loans to lock in cheap capital. But when rates are high—or rising—some may opt for adjustable-rate mortgages (ARMs) or interest-only loans in hopes that rates will drop in the near future. These options offer lower initial payments but carry more risk if rates stay elevated or continue climbing.

Moreover, Debt Service Coverage Ratio (DSCR) requirements become tougher to meet when mortgage payments increase. Lenders typically require a DSCR of at least 1.2x, meaning a property must generate 20% more income than its debt obligations.

As interest rates rise, reaching that threshold becomes harder—especially in markets where rents aren’t rising fast enough to offset higher financing costs.

How Interest Rates Influence Rental Yields and NOI

When interest rates change, it’s not just mortgage costs that shift. Rental yields and Net Operating Income (NOI)—two core metrics for real estate investors—also feel the impact. And in many cases, the connection isn’t immediate, which makes it all the more important to track and plan for.

Rental yield, put simply, is the annual rental income as a percentage of the property’s value. For example, a property earning $24,000 in annual rent and valued at $400,000 has a 6% gross yield.

But as interest rates rise, a few things tend to happen: borrowing costs increase, which can compress profits, and investor expectations for higher yields also rise. This puts pressure on sellers to lower prices—or on landlords to raise rents.

However, raising rents isn’t always easy. Tenants also face affordability constraints, especially in high-rate environments where the overall cost of living tends to climb. If renters can’t absorb higher monthly costs, landlords may struggle to grow income, leading to stagnant or declining yields. This is particularly challenging in highly competitive rental markets where supply outpaces demand.

At the same time, higher interest rates often slow property appreciation. When values stagnate but operating expenses (like taxes, insurance, and maintenance) continue rising, NOI growth slows—or in some cases, reverses. Investors relying on NOI growth to justify their purchase price or underwriting assumptions can quickly find themselves in a bind.

Let’s put some numbers behind that. Assume you own a multifamily property generating $120,000 in gross income, with $30,000 in expenses. Your NOI is $90,000. If interest rates push up your property taxes and insurance premiums by $5,000 annually, your NOI drops to $85,000, reducing your property’s theoretical value (at a 6% cap rate) by over $83,000. That’s a meaningful hit to equity.

What’s more, rental income isn’t always quick to respond to macro shifts. Lease terms, especially in long-term rentals, delay rent adjustments. In contrast, short-term rentals (like Airbnb units) are more responsive to market changes but are also more sensitive to economic slowdowns caused by rate hikes.

In this kind of environment, preserving NOI requires careful expense management, accurate market rent assessments, and avoiding overleveraging. Investors need to focus on asset classes or markets with strong demand, where rent growth can at least partially outpace rising interest-related expenses.

Interest Rates and Cap Rate Movements Explained

One of the most important dynamics real estate investors watch closely is the relationship between interest rates and capitalization rates, or cap rates. Cap rates are used to value income-producing properties and to compare return potential across different asset classes. But when interest rates change, cap rates tend to move with them—and that has real consequences for property values.

At its core, a cap rate is calculated by dividing Net Operating Income (NOI) by the property’s current market value. So, if a property generates $100,000 in annual NOI and is worth $2 million, the cap rate is 5%. It tells investors what percentage return they can expect on an unleveraged investment. But when interest rates rise, investors typically expect higher returns to compensate for the increased cost of capital and higher risk.

This expectation causes cap rates to expand. And when cap rates go up, property values go down—assuming NOI stays the same. Let’s look at a practical example. Imagine a commercial building with an NOI of $150,000:

- At a 5% cap rate, its market value is $3 million

- At a 6.5% cap rate, that same property is now worth about $2.31 million

That’s a $690,000 drop in valuation, purely due to changes in rate expectations.

Cap rate movements don’t always happen immediately when interest rates shift. Sometimes there’s a lag as buyers and sellers adjust to new market conditions.

But over time, the direction becomes clear. In periods of rate hikes—such as in 2022–2024, when central banks aggressively raised rates to fight inflation—cap rates rose across nearly every real estate sector. Investors started demanding higher yields, and many institutional buyers pulled back on acquisitions, waiting for prices to reset.

Some asset classes are more sensitive to these movements than others. For instance, office buildings—especially in urban areas—have seen notable cap rate expansion due to both interest rate pressure and changing demand patterns.

Meanwhile, industrial properties and multifamily housing in high-growth markets have remained more stable, thanks to resilient rental income and strong fundamentals.

Investing in High vs Low Interest Rate Environments

Investing in real estate during high or low interest rate environments comes with very different risks, rewards, and strategies. Each scenario affects how deals are underwritten, what types of assets attract capital, and how investors structure financing.

Let’s start with low-rate environments. When borrowing is cheap, investors can access leverage at favorable terms. This means lower monthly payments, which improves Cash-on-Cash Return and overall Return on Investment (ROI). It also allows buyers to be more aggressive with pricing, since the cost of capital is manageable.

During the 2020–2021 period, for example, 30-year fixed mortgage rates in the U.S. dropped below 3%—a historic low. As a result, transaction volumes surged and many investors pursued buy-and-hold or BRRRR strategies, banking on both rental income and appreciation.

But there’s a downside. Low interest rates often lead to cap rate compression, meaning property values rise while yields fall. In other words, you’re paying more for less return. This creates a competitive market where even modestly cash-flowing properties can command premium prices. Investors chasing yield in this setting may feel forced to take on more risk—like investing in secondary markets or class B/C assets—just to meet return targets.

Now let’s flip the scenario. In high interest rate environments, the cost of borrowing increases. This reduces buyer demand and often pushes property prices down, especially in overleveraged sectors. However, for investors with access to cash or creative financing (like bridge loans or private money lending), it can be a rare chance to acquire assets at a discount. Fewer buyers mean more negotiation power and less bidding competition.

Take 2023, for example. As rates climbed above 7%, many institutional investors pulled back. But some private equity groups and seasoned investors saw opportunity in distressed multifamily and value-add commercial properties, acquiring them at 10–20% below prior-year valuations. These acquisitions were underwritten with more conservative assumptions but had greater long-term upside.

Another difference lies in exit strategy. In a low-rate cycle, holding long term or refinancing can unlock equity and improve returns. In high-rate cycles, however, investors often focus on shorter timelines, aiming for IRR-driven strategies that capitalize on operational improvements or market timing. Timing matters more, and patience becomes a competitive advantage.

How Central Bank Policies Drive Real Estate Cycles

To really understand how interest rates move—and why they matter for real estate—you need to look at central banks. Institutions like the Federal Reserve, the European Central Bank, or the Bank of England play a direct role in shaping the cost of borrowing, and by extension, the entire real estate cycle.

Central banks adjust interest rates to either cool down or stimulate economic activity. When inflation is high, they typically raise rates to reduce spending and borrowing. When the economy slows or unemployment rises, they lower rates to encourage growth. These changes don’t just affect consumer spending—they ripple straight into real estate.

For instance, when the Fed began increasing rates aggressively in 2022 to fight inflation, mortgage rates in the U.S. doubled within months. That spike immediately cooled the housing market.

According to industry data, home sales dropped by over 35% year-over-year in several regions, and new construction permits declined by nearly 25%. It wasn’t just homeowners who paused. Developers, syndicators, and institutional buyers all adjusted their strategies based on central bank cues.

These policy decisions also shape investor sentiment. When rates are expected to stay low, investors feel more confident leveraging capital into long-term real estate assets—especially multifamily, student housing, or mixed-use developments with stable income.

But when rate hikes are on the table, there’s more hesitation. Investors demand higher yields, and deal underwriting becomes more conservative.

Central banks don’t act in isolation. They also influence other economic indicators like inflation, GDP growth, and employment rates, which further shape real estate performance. For example, tight monetary policy can slow GDP, which affects job growth—eventually influencing rental demand, occupancy, and NOI.

That’s why experienced investors keep an eye on central bank meetings and policy announcements. Even the hint of a rate shift can move the markets. Those who track macro signals closely often find themselves better positioned to adjust pricing models, debt structures, and exit timelines ahead of broader market movements.

Strategies to Protect Real Estate Investments from Interest Rate Risk

When interest rates start moving—especially upward—real estate investors can’t afford to stay passive. The good news is that there are several effective strategies to shield your investments from rate-related risks while preserving long-term growth potential.

One of the most important strategies is choosing the right financing structure. In a rising rate environment, fixed-rate loans offer stability. Locking in rates early can protect you from sudden spikes in borrowing costs. On the other hand, when rates are high but expected to drop, adjustable-rate mortgages (ARMs) or interest-only loans can give you flexibility and lower payments in the early years—especially if you plan to refinance later.

Another smart move is managing your loan-to-value ratio (LTV). Keeping LTV lower—say under 65%—gives you more breathing room. It also makes refinancing easier and reduces the risk of being underwater if cap rates expand and property values dip. Lenders often reward conservative LTVs with better terms and more leverage options down the road.

On the operations side, boosting Net Operating Income (NOI) becomes even more critical. Investors should focus on value-add strategies such as improving tenant retention, upgrading units, or optimizing property management. A $100 monthly rent increase on 10 units translates to an extra $12,000 annually—and at a 6% cap rate, that’s $200,000 in added property value. Small changes can have a big impact on performance when financing costs are rising.

Refinancing timing is also key. If you expect rates to fall in the next 12–24 months, positioning your current debt to mature just beyond that window gives you the opportunity to reset your terms at more favorable levels. This is where bridge loans or short-term private lending can come in handy, especially for transitional assets.

Some investors take it a step further with interest rate hedging tools like rate caps or swaps. These are common in larger commercial transactions and syndications. While they involve upfront costs, they protect against extreme interest rate volatility—especially for variable-rate loans tied to SOFR or other benchmarks.

Finally, diversification matters more than ever. Investing across different asset types—such as single-family rentals, multifamily, and commercial properties—or across different markets can spread exposure. Some markets, especially those with strong job growth and population inflows, tend to be more resilient when borrowing costs rise.

FAQ

How do interest rates influence real estate cash flow?

Higher interest rates increase borrowing costs, which can reduce cash flow unless rental income rises proportionally.

Is it better to invest in property when interest rates are high or low?

Low rates offer better financing terms, while high rates can create buying opportunities due to price softening. Timing depends on your strategy and risk tolerance.

Can interest rates impact property values directly?

Yes. As interest rates rise, cap rates typically expand, which can decrease property values if net income doesn’t increase.

What types of properties are more resilient to rising interest rates?

Multifamily units and affordable housing tend to hold value better due to consistent demand and stable income streams.

Should investors refinance during high-rate periods?

Only if necessary. It’s often better to wait for rate normalization unless the current loan terms are unsustainable.