It wasn’t too long ago that the UK stood proudly as a global economic powerhouse, often revered for its industrial might, political stability, and financial influence.

The image of bustling London streets filled with well-dressed professionals, the hum of innovation, and economic growth now feels like a distant memory.

Fast forward to today, and the narrative has shifted dramatically. What was once an empire that held sway over a quarter of the world is now battling deep-seated economic woes, struggling to maintain the high standard of living that its citizens had long taken for granted.

You wouldn’t be the first to scoff at the idea of the UK being compared to a “third world country,” but when you peel back the layers and take a hard look at the facts, the situation becomes a lot less laughable.

From stagnant productivity, rising inflation, and an unmanageable national debt, to a workforce that’s increasingly inactive, the UK’s economy is deteriorating at an alarming rate.

This article analyzes the profound economic challenges facing the UK, taking an in-depth look at the statistics, the causes, and the very real consequences of these issues.

Table of Contents

A Brief Overview of the UK’s Economic Decline

To accurately assess the severity of the United Kingdom’s ongoing economic deterioration, it’s essential to start with a clear baseline: real disposable income—the income households have left after taxes and essential expenses—has remained virtually stagnant for more than a decade.

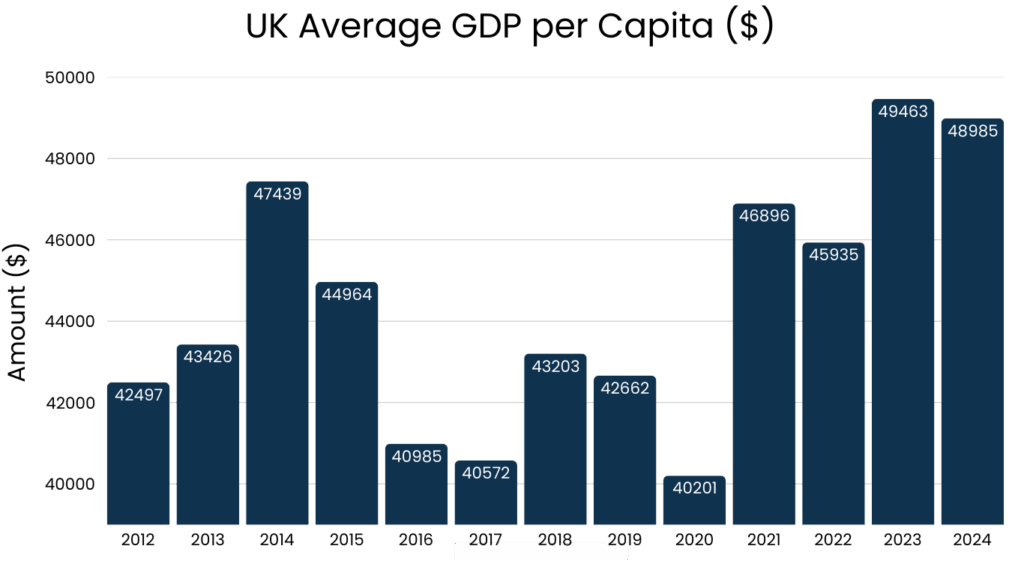

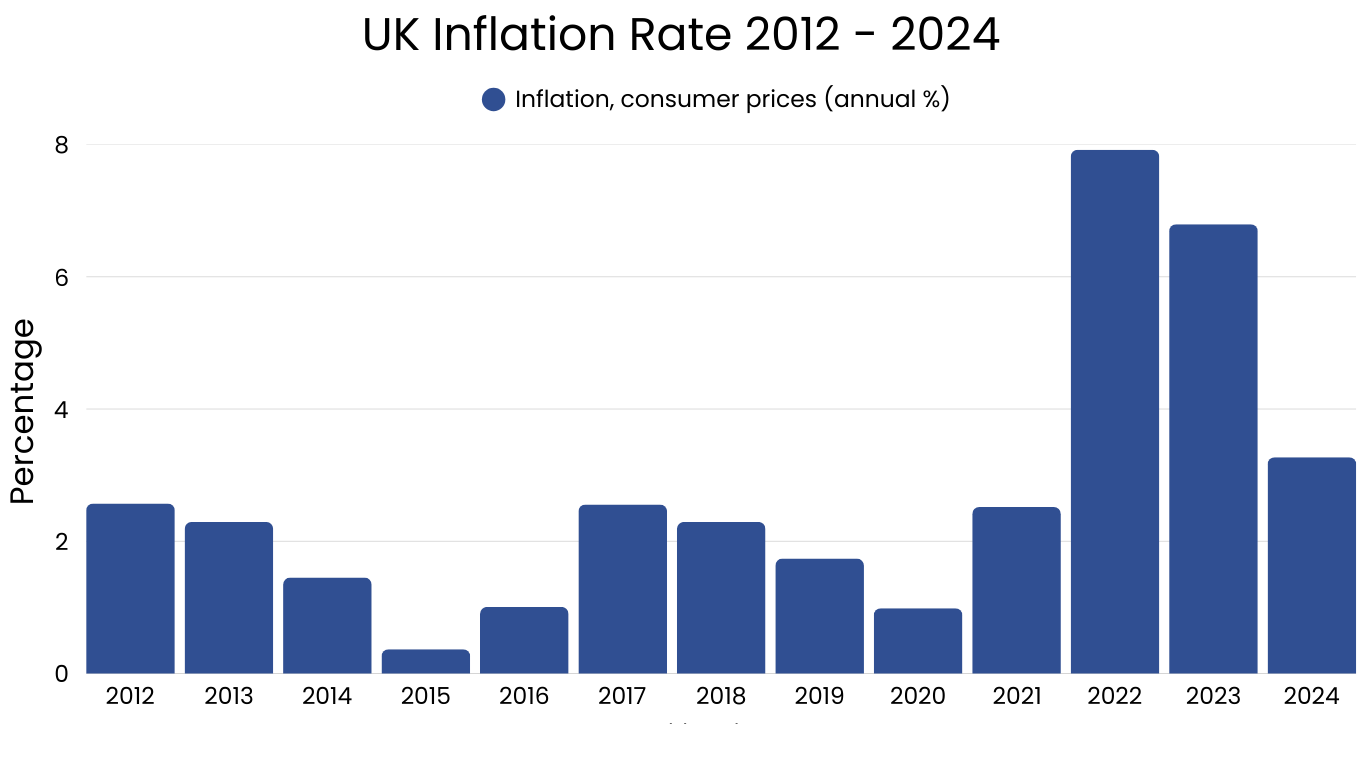

According to the Office for National Statistics (ONS), between 2010 and 2025, inflation-adjusted household incomes have grown by less than 0.5% annually, a rate that lags far behind rising living costs.

Simultaneously, the Consumer Prices Index (CPI) has surged, with inflation peaking at 11.1% in October 2022, the highest in over 40 years. Although inflation eased slightly in 2025, many essential goods—such as energy, food, and housing—remain significantly more expensive than they were just a few years ago. This price pressure has eroded purchasing power, pushing millions of UK households toward financial instability.

What’s more alarming is that London, long considered the UK’s economic powerhouse, is not immune to these macroeconomic headwinds. While the capital still contributes disproportionately to national GDP—accounting for nearly 23% of it—it is increasingly disconnected from the economic realities faced by the rest of the country.

The City of London and Canary Wharf continue to serve as major global finance hubs, but there are signs of stress beneath the surface.

Despite higher nominal wages, real wage growth has been minimal once adjusted for inflation and the capital’s inflated housing and transport costs. According to ONS data, median annual earnings for full-time employees in London stood at approximately £44,370 in 2024, but this income is quickly absorbed by high living expenses.

Additionally, there’s a deepening economic rift between the capital and the rest of the country.

Southeast England, which includes London, produces almost half of the UK’s GDP while representing just a third of its population. In contrast, regions such as the North East, West Midlands, and parts of Wales have seen little to no real growth, with lower wages, higher unemployment rates, and deteriorating public infrastructure.

As a result, the UK is becoming increasingly economically polarized. While pockets of affluence remain in London and its surrounding commuter belts, large swathes of the country face stagnation or decline. Nationally, real household income has been flat for nearly 15 years, meaning that despite modest nominal wage increases, British workers are experiencing no meaningful rise in living standards.

In comparative terms, UK households are falling behind international peers. Research from the Resolution Foundation shows that typical British middle-class households are now poorer than their counterparts in France, Germany, and the United States, with Norwegian households enjoying significantly higher levels of disposable income and wealth accumulation.

The deterioration in living standards is particularly stark for the British middle class—once the engine of economic stability. Today, more families are struggling to afford essentials, battling rising energy bills, expensive childcare, unaffordable housing, and stagnant wages. This erosion of middle-class security reflects a broader structural decline in the UK’s economic resilience.

The UK’s Productivity Crisis

One of the most critical—and often underreported—drivers of the UK’s long-term economic stagnation is its persistent productivity crisis.

In economic terms, productivity refers to the efficiency with which goods and services are produced. It is a key determinant of a nation’s competitiveness, wage growth, and standard of living.

Unfortunately, the UK has experienced one of the sharpest productivity slowdowns in the developed world.

Before the 2008 global financial crisis, the UK’s productivity was increasing at a healthy pace of around 2% per year, in line with G7 averages. However, since 2008, productivity growth has slowed dramatically—averaging just 0.5% annually between 2010 and 2025, according to data from the Office for National Statistics (ONS).

This decline has placed the UK second-to-last among G7 economies in terms of productivity performance, ahead of only Italy. By comparison, Germany and the United States have maintained significantly stronger productivity trajectories over the same period.

Stagnant productivity is not just a statistical concern—it has real-world economic consequences. When output per worker fails to improve, businesses face higher unit costs, making it harder to compete globally. This undermines the UK’s ability to attract foreign direct investment (FDI), expand exports, and support long-term industrial growth.

- For example, British manufacturers in the automotive and aerospace sectors—once pillars of UK industrial strength—have struggled to keep pace with their German and French counterparts, due in part to lower capital investment and slower adoption of automation and digital infrastructure.

- Sectors like construction, retail, and public administration continue to report some of the lowest productivity per hour worked in Western Europe, highlighting inefficiencies that remain unresolved.

The UK’s productivity malaise also directly impacts wage growth. In most advanced economies, productivity and wages typically rise in tandem. However, in the UK, real wage growth has decoupled from productivity gains. With businesses facing slim profit margins and elevated input costs, many are reluctant to raise wages—even in a tight labor market.

According to the Institute for Fiscal Studies (IFS), real wages in the UK in 2025 remain lower than they were in 2008, making this one of the worst stretches of wage stagnation in post-war history. This stagnation feeds into lower household consumption, weakens domestic demand, and further drags down GDP growth.

The UK’s productivity crisis is both a cause and a symptom of its broader economic decline.

Poor productivity leads to stagnant wages, which reduce consumer spending and limit tax revenues. This, in turn, results in underfunded public services and insufficient investment in the very sectors—infrastructure, education, and innovation—that are needed to revive productivity.

With capital investment in the UK ranking lowest among G7 countries as a share of GDP (according to OECD data), the underlying drivers of productivity—technology adoption, skills training, and R&D—remain significantly underfunded.

Public sector productivity, especially within the NHS and local government, has also been declining, further stressing the economy and increasing fiscal burdens on the state.

Brexit’s Economic Bombshell

The decision to leave the European Union in 2016 sent shockwaves through the UK’s economy, and the full impact of Brexit is still being felt today.

The most immediate consequence of Brexit has been a sharp decline in foreign investment. Investors, both domestic and international, are wary of the political and economic uncertainty that Brexit has introduced.

Between 2016 and 2021, foreign investment in the UK fell by 25%, a massive blow to an economy that was already grappling with sluggish growth and stagnant productivity.

The long-term economic impact of Brexit is even more concerning. By severing its ties with the EU, the UK has effectively cut itself off from one of the largest and most important trading blocs in the world.

This has led to a significant reduction in trade, which has further weakened the country’s already fragile economy.

Trade barriers, tariffs, and regulatory hurdles have made it more expensive for UK companies to do business with their European counterparts, and this has led to job losses in key industries such as manufacturing, finance, and agriculture.

But the damage doesn’t stop there. Brexit has also contributed to a 6% reduction in the UK’s Gross Value Added (GVA), a measure of the value of goods and services produced in the country.

This is equivalent to a loss of £140 billion from the UK’s economy – a staggering figure that highlights just how severe the economic consequences of Brexit have been.

London, in particular, has been hit hard, with the city losing £30 billion in economic output and nearly 300,000 jobs. The financial services sector, which was once the crown jewel of the UK’s economy, has been decimated by the exodus of firms seeking more stable environments within the EU.

COVID-19’s Contribution to Economic Destruction

Just as the UK was beginning to grapple with the full economic consequences of Brexit, the COVID-19 pandemic struck, plunging the country into an even deeper economic crisis.

The government was forced to borrow an additional £280 billion during the pandemic to provide relief for businesses and individuals.

While this massive influx of government spending helped to prevent a total economic collapse, it has also pushed the UK’s national debt to unsustainable levels.

At first, low interest rates made it relatively easy for the government to manage its growing debt. However, as inflation has surged and interest rates have risen, the cost of servicing this debt has become increasingly burdensome.

The government is now paying over £100 billion annually in debt repayments – a figure that is crowding out spending on essential public services like healthcare, education, and social welfare.

The impact of COVID-19 on the UK’s workforce has also been devastating. Millions of jobs were lost during the pandemic, and while many of those jobs have since returned, a significant portion of the population remains “economically inactive.”

This includes retirees, students, and individuals with caregiving responsibilities, but it also includes a growing number of people who have simply given up on finding work.

As of 2025, there are 11 million people in the UK who are considered economically inactive – a figure that should alarm anyone concerned with the country’s long-term economic health.

Inflation and Rising Debt

Inflation has been another significant challenge for the UK in recent years. The cost of goods and services has risen dramatically, eroding the purchasing power of consumers and making it more difficult for businesses to operate.

High inflation has also made it more expensive for the government to service its national debt, creating a vicious cycle in which rising prices lead to rising debt, which in turn leads to more inflation.

One of the most visible impacts of inflation has been on energy prices. Due to global factors, including the war in Ukraine, energy prices in the UK have skyrocketed.

British households are now paying three times more for heating than they were just a few years ago. In an attempt to mitigate this crisis, the government borrowed an additional £60-100 billion for energy support, further exacerbating the national debt problem.

Workforce Challenges and Immigration

The UK’s workforce challenges have been compounded by demographic shifts and changing social dynamics. As the population ages, fewer people are available to work, while many younger people are opting out of traditional employment paths in favor of further education or alternative lifestyles.

The government has attempted to address this labor shortage by opening its borders to immigrant workers, particularly from South Asia and Sub-Saharan Africa.

However, this influx of immigrant workers has not come without its own set of challenges. Social tensions have risen dramatically in recent years, with protests and riots becoming a regular occurrence in parts of the country.

Many British citizens feel that their economic struggles have been worsened by the large numbers of immigrants entering the workforce, which has fueled resentment and division.

The immigration debate is a double-edged sword. On the one hand, these workers are essential to filling the gaps in sectors such as healthcare, agriculture, and construction, where domestic labor is either unavailable or unwilling to take up the roles.

Many industries would grind to a halt without the influx of immigrant labor.

On the other hand, this large-scale immigration has led to increased strain on public services, particularly housing, healthcare, and education, creating tensions in local communities that feel overwhelmed by the sudden demographic changes.

The social fabric of the UK is being tested. While the government has attempted to strike a balance between meeting labor market demands and addressing social concerns, the current approach has been largely reactive, rather than proactive.

Policies aimed at integrating immigrants more effectively into the social and economic framework have been inadequate, leaving both newcomers and long-standing citizens feeling disenfranchised.

The result? A deepening social divide that further complicates the already fragile economic landscape.

Moreover, the political climate surrounding immigration has become increasingly hostile, with anti-immigration sentiment fueling the rise of far-right movements and protests across the country.

While it is clear that the UK needs immigrant labor to sustain certain sectors of its economy, the challenge lies in managing the societal impact of these demographic shifts.

Without a well-structured immigration policy that addresses both the economic need for workers and the social concerns of local populations, this issue will continue to simmer, adding yet another layer to the UK’s growing list of problems.

Forecasting Continued Economic Decline

Looking ahead, the economic outlook for the UK remains grim. Without significant policy changes, the country is on course for further economic decline.

By 2035, the UK’s real Gross Value Added (GVA) is projected to be £311 billion lower than it would have been without the economic challenges it now faces.

London, which has historically been the driver of the UK’s economic success, is expected to see its GVA shrink by £63 billion during this same period.

This forecast underscores just how deeply the current economic crisis has embedded itself in the country’s long-term trajectory.

The job market is another area where the future looks particularly concerning. If no meaningful interventions are made, job losses will continue to mount.

Industries such as financial services and manufacturing, which have already been hit hard by Brexit and the post-pandemic recovery, are expected to suffer further as businesses relocate to more stable and economically viable countries.

This will exacerbate the already widening gap between London and the rest of the UK, with regional economies falling further behind.

The cost of living crisis is also set to worsen in the coming years. Inflation shows no signs of abating, and household incomes are unlikely to rise fast enough to keep up with the increasing cost of basic necessities.

Food prices, in particular, are expected to continue their upward trajectory, placing even more pressure on struggling families.

This will further reduce disposable incomes and dampen consumer spending, creating a vicious cycle that could plunge the UK into a prolonged economic downturn.

There is also the looming specter of energy prices. Although the UK government has taken steps to support households through temporary measures, such as energy subsidies, these efforts are not sustainable in the long run.

As global energy markets remain volatile, the UK could find itself facing an even more severe energy crisis in the near future. If energy costs continue to rise, they will have a ripple effect throughout the economy, pushing more households into poverty and placing further strain on businesses that are already operating on tight margins.

Is There Any Hope?

It’s easy to become disheartened when looking at the current state of the UK’s economy and the forecast for the future. But is there any hope for a turnaround?

While the situation is undoubtedly bleak, history has shown that economic crises can sometimes act as catalysts for meaningful reform. The UK has a long history of overcoming adversity, and it’s possible that this period of economic hardship could spur the country to take bold, innovative steps to reverse its decline.

The key to any potential recovery lies in addressing the root causes of the UK’s economic woes. First and foremost, productivity must be improved.

This requires investment in education, skills training, and infrastructure. The government must create an environment that encourages businesses to innovate and invest in new technologies that can drive productivity growth.

Without such investment, the UK will continue to lag behind other major economies.

Secondly, the housing crisis must be tackled head-on. The UK’s housing market is in desperate need of reform. The government needs to take steps to increase the supply of affordable housing, particularly in urban centers where demand is highest.

This would not only alleviate the strain on the housing market but also provide a much-needed boost to the construction industry, which could create jobs and stimulate economic growth.

Thirdly, the UK needs to address its workforce challenges. This means not only creating jobs but also ensuring that those jobs are accessible to a broader portion of the population.

Flexible working arrangements, better childcare support, and retraining programs could help bring more people back into the labor market.

At the same time, immigration policies need to be rethought to ensure that the UK is able to attract the talent it needs while also addressing the social tensions that large-scale immigration can create.

Additionally, the government must confront the national debt problem. While borrowing has been necessary to address the short-term impacts of the pandemic and energy crises, a long-term plan is needed to reduce the national debt to more sustainable levels.

This will require difficult choices about public spending and taxation, but without such a plan, the UK risks being trapped in a cycle of rising debt and sluggish economic growth.

Energy policy will also play a crucial role in any potential recovery. The UK must invest in sustainable, renewable energy sources to reduce its reliance on volatile global energy markets.

Not only would this help mitigate the impact of future energy price shocks, but it would also position the UK as a leader in the green economy, creating jobs and new industries that could drive future growth.

Is the UK Truly Becoming a “Third World” Country?

The notion that the UK is becoming a “third world country” might seem hyperbolic to some, but when you look at the data, the comparison starts to seem disturbingly apt.

High levels of debt, sluggish productivity, rampant inflation, a shrinking workforce, and growing social inequality are all characteristics of economies that are struggling to keep pace with the developed world.

While the UK may not be there yet, it is undoubtedly on a path that, if left unchecked, could lead to further economic and social deterioration.

London remains a global financial hub and a center of wealth, but beyond the capital, the picture is far less rosy.

Regional disparities are growing, and for many people living outside of London, the economic opportunities that once defined the UK as a prosperous nation are slipping away.

If these issues are not addressed, the UK risks becoming a country divided – with a wealthy capital city surrounded by regions that are increasingly reminiscent of struggling economies in less developed parts of the world.

FAQ

Why do some people say the UK is becoming a ‘third world’ country?

The phrase reflects deep concerns about the UK’s economic decline—marked by stagnant wages, poor productivity, rising inflation, and growing inequality. While the UK is still classified as a high-income country, structural issues such as regional poverty, public service erosion, and a shrinking middle class have drawn comparisons to struggling economies.

How has productivity affected the UK’s economic performance?

UK productivity growth has slowed dramatically since the 2008 financial crisis—averaging just 0.5% annually versus 2% before. This stagnation has weakened wage growth, reduced business competitiveness, and placed the UK near the bottom of the G7 for productivity.

What economic impact has Brexit had on the UK?

Brexit triggered a 25% drop in foreign investment between 2016 and 2021, increased trade barriers, and caused significant job losses in sectors like finance and manufacturing. The UK’s Gross Value Added (GVA) has declined by £140 billion, with London alone losing an estimated £30 billion in economic output.

How did COVID-19 worsen the UK’s financial situation?

The UK government borrowed £280 billion during the pandemic, pushing national debt to record levels. As of 2025, £100+ billion is spent annually on debt servicing. Meanwhile, over 11 million people are now classified as economically inactive, contributing to labor shortages and reduced productivity.

What’s driving the UK’s inflation crisis?

Inflation surged to 11.1% in 2022, driven by global energy shocks, supply chain disruptions, and domestic policy responses. Although inflation has eased in 2025, essential costs like housing, energy, and food remain significantly elevated, squeezing household budgets and eroding real income.

How serious is the UK’s national debt problem?

The UK’s public debt now exceeds £2.5 trillion, with interest payments alone costing over £100 billion per year. High inflation and rising interest rates have made debt servicing increasingly unsustainable, limiting the government’s ability to invest in public services or stimulate growth.

Is the UK still considered a developed country?

Yes. The UK remains part of the OECD and G7 and is classified as a high-income economy. However, several long-term indicators—like low real wage growth, rising poverty, and declining regional investment—are eroding its position relative to other developed nations.

What does the future look like for the UK economy?

Without significant policy reform, forecasts show that the UK’s GVA could be £311 billion lower by 2035 than pre-crisis projections. Continued pressure on household incomes, public services, and key industries suggests a slow, uneven recovery unless structural issues are addressed head-on.