The London Real Estate Market in 2025 presents a mixed yet strategically positioned environment for property investors. As the UK’s financial and cultural capital, London continues to offer long-term investment potential despite recent macroeconomic headwinds.

While sales price growth has stabilized, rental values have accelerated, positioning the city as a yield-driven market in the near term.

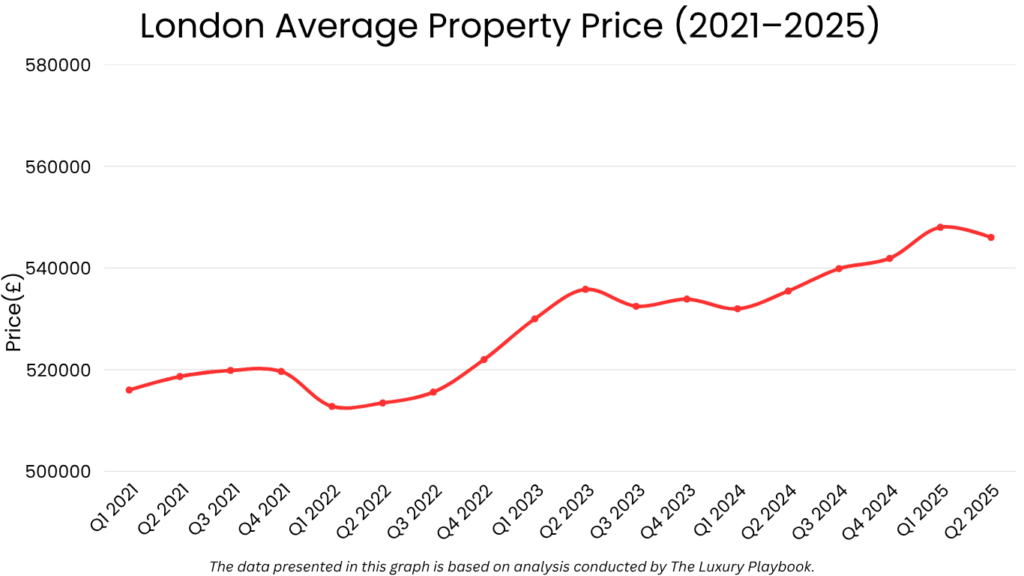

As of Q2 2025, the average residential property price in Greater London stands at approximately £546,000, following a year of marginal recovery after broader national declines. High inflation and interest rate pressures over the past 18 months have cooled the sales market, but underlying fundamentals—including limited supply, continued inward migration, and consistent international interest—continue to underpin demand.

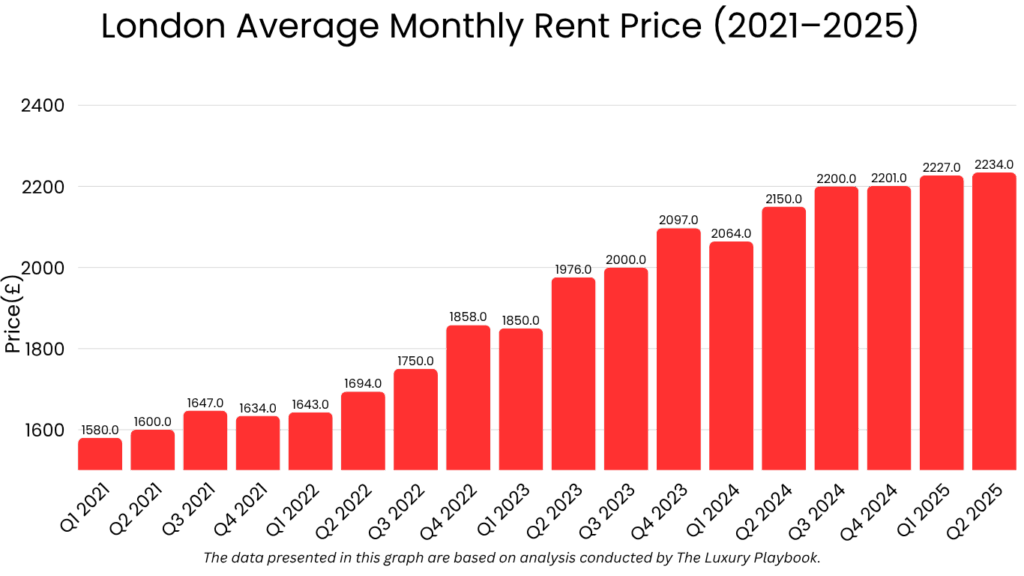

The rental segment, by contrast, has seen double-digit growth.

Average monthly rents across London have now reached £2,227, up 11% year-on-year, driven by undersupply, professional relocation, and returning student demand. Core central zones as well as outer commuter boroughs are seeing increased rental activity, pushing gross yields higher and improving cash flow potential for new landlords.

Table of Contents

Overview of The London Real Estate Market

The London Real Estate Market in 2025 is stabilizing after several years of economic uncertainty, inflationary pressure, and fluctuating interest rates. While the broader UK property market has softened, London’s status as a global financial hub and safe-haven destination continues to support resilient demand—particularly in the rental sector and select sales submarkets.

As of Q2 of 2025, the average property price in Greater London sits at approximately £546,000, following a minor decline in 2023 and subsequent plateauing through 2024.

Recovery has been more visible in prime central locations such as Kensington, Chelsea, and Westminster, where international capital and limited supply maintain pricing floors. These areas now command values exceeding £1.2M, while outer boroughs like Barking, Newham, and Croydon maintain averages between £350,000 and £450,000.

Transaction volumes remain below pre-pandemic norms, largely due to affordability constraints and tightened lending standards. However, the Bank of England’s anticipated rate softening in the second half of 2025 is expected to stimulate mortgage approvals and unlock latent buyer activity—particularly among first-time buyers and investors in emerging boroughs.

New-build activity remains uneven. Developers are slowing construction starts in central areas due to rising material and labor costs, while outer boroughs are seeing stronger construction pipelines—primarily in Build-to-Rent (BTR) and affordable housing schemes.

As a result, resale stock in well-located areas is attracting increased attention, particularly from yield-seeking landlords.

Key market characteristics in 2025:

- Average London house price: £546,000

- Annual price movement: ~+1.0% (stabilized after prior declines)

- Prime central boroughs: £1.2M+ (Chelsea, Westminster, Kensington)

- Outer boroughs (value segments): £350K–£450K (Barking, Croydon, Enfield)

- Buyer profile: International investors, domestic upgraders, long-term renters entering ownership

- New supply: Limited in core; concentrated in outer zones and regeneration corridors

In summary, the London Housing Market in 2025 remains bifurcated—offering capital preservation in prime areas and yield-oriented entry points in outer boroughs. Investors with mid- to long-term horizons will benefit from steady pricing, improving mortgage conditions, and deepening rental strength across the capital.

Neighborhood Analysis

London’s housing market remains highly segmented, with pricing and investment potential varying widely by borough. From ultra-prime central postcodes to up-and-coming commuter districts, the city offers diverse entry points tailored to capital preservation, yield generation, or long-term growth strategies.

Kensington & Chelsea

Kensington & Chelsea is London’s premier luxury market, known for heritage architecture, embassies, and global buyer interest. Despite softening in 2023, the area rebounded in early 2025, driven by international capital and a shortage of high-spec resale stock.

Average prices exceed £1.5M, or £13,000/sqm. Properties here function primarily as long-term wealth preservation vehicles. Yields are modest, typically below 3%, but demand from high-net-worth individuals remains stable.

Canary Wharf

Once dominated by financial tenants, Canary Wharf has diversified to attract younger professionals and renters seeking proximity to offices, retail, and new developments. The area is undergoing residential repositioning, especially in Build-to-Rent (BTR) projects.

Prices average £620K, or £7,000/sqm, with strong leasing demand and mid-tier yields of 4.0–4.5%. It suits investors targeting long-term tenants and professional renters.

Walthamstow

Located in East London, Walthamstow has transitioned from a fringe market to a sought-after district for first-time buyers and landlords. Its appeal lies in lower prices, good transport links, and a growing creative and professional community.

Properties are priced around £480K, or £5,000/sqm. Yields range from 4.5% to 5.5%, making it one of the city’s most attractive neighborhoods for rental-focused strategies.

Battersea & Nine Elms

This riverside regeneration corridor has attracted major developer activity, offering luxury flats and improved infrastructure. Buyer demand is led by overseas investors and urban professionals.

Average prices fall between £850K and £1M, or £9,000–£10,500/sqm. Yields are moderate but improving as occupancy levels rise. Strong capital appreciation prospects are tied to infrastructure like the Northern Line extension and Battersea Power Station.

Barking & Dagenham

Among the most affordable boroughs, Barking continues to benefit from city-led regeneration and demand spillover from priced-out central renters. It attracts investors seeking low entry points and robust yields.

Typical pricing is £375K, or £4,000/sqm, with gross yields between 5.5% and 6.5%. It offers strong rental performance, particularly in 2-bedroom units targeted at working-class families and young professionals.

Neighborhood Median Prices and Price per Square Meter

London Rental Market Overview

The London rental market in 2025 is outperforming the sales segment, driven by limited housing supply, high borrowing costs, and a growing population of renters. With mortgage affordability still constrained, demand for rental units has surged—especially in well-connected outer boroughs and newly built mid-market developments.

Rental demand in London continues to intensify across nearly all segments, making the capital one of the most consistent income-producing real estate markets in Europe.

Average Monthly Rent by Property Type (2025)

- 1-Bedroom Apartment: £1,700 – £2,200

- 2-Bedroom Apartment: £2,200 – £2,900

- 3-Bedroom Apartment: £2,900 – £3,800

- Luxury Central Units (Zone 1–2): £4,500 – £7,000+

The average monthly rent in Greater London now stands at £2,234, representing an 11% year-on-year increase. This reflects a prolonged mismatch between tenant demand and unit availability—particularly in central zones and inner commuter districts.

The strongest rental growth has occurred in areas like Hackney, Walthamstow, Stratford, and Croydon, where mid-range rents and transport accessibility drive consistent occupancy.

Yield Performance and Leasing Segmentation

Gross yields across London vary widely depending on location, property type, and tenant profile:

- High-Yield Districts: Barking & Dagenham, Croydon, Southall (5.5%–6.5%)

- Balanced Markets: Walthamstow, Stratford, Hackney (4.5%–5.2%)

- Capital Zones with Lower Yields: Kensington, Westminster, Southbank (2.5%–3.5%)

Most landlords are shifting toward long-term tenancy models, targeting young professionals, families, and remote workers. There is also a growing trend toward mid-stay leases (3–6 months) in well-furnished, central units—offering a balance between yield and legal simplicity.

Furnished units, energy-efficient appliances, and high-speed internet are now considered minimum standards in most segments, especially in boroughs with strong corporate or academic populations.

Moreover, The rental market operates under increasing scrutiny, with recent policies aimed at improving tenant protections, energy standards, and rent transparency. While there is currently no national rent cap, London landlords must comply with right-to-rent checks, deposit protections, and EPC rating minimums.

Short-term lets remain legal under the 90-day limit rule for entire properties, but enforcement in central boroughs has tightened. Investors are advised to focus on compliant long-term models to reduce exposure to fines or licensing issues.

In summary, the London rental market in 2025 offers high demand, rising returns, and diverse entry points across boroughs. Investors can optimise performance by prioritising location, lease duration, and property readiness, with a growing emphasis on tenant quality and legal alignment.

Factors Influencing the London Housing Market

The London Housing Market in 2025 is shaped by a combination of macroeconomic conditions, structural supply constraints, policy interventions, and lifestyle-driven tenant shifts. As one of the most scrutinised and globally exposed real estate markets, London responds acutely to both domestic economic policy and international capital flows.

- Interest Rate Stabilisation and Lending Conditions: Following aggressive interest rate hikes in 2023 and 2024, the Bank of England is now signalling a period of monetary easing, with base rates expected to decline marginally through late 2025. This shift is improving mortgage affordability, particularly for first-time buyers and investors in outer boroughs. Eased lending criteria are likely to unlock latent demand in mid-priced zones such as Stratford, Croydon, and Southall.

- Structural Undersupply and Planning Delays: London continues to face a severe housing supply shortage, particularly in Zones 1–3. Planning bureaucracy, rising construction costs, and limited land availability have restricted both new-build and refurbishment pipelines. This has created persistent upward pressure on rents and maintained price floors in key boroughs—especially in Hackney, Walthamstow, and Kensington & Chelsea.

- Population Growth and Urban Density: Greater London’s population is expected to surpass 9.2 million by the end of 2025, driven by natural growth, international migration, and student inflows. The continued rise in renter households is increasing long-term demand across all tenures, particularly for affordable, well-connected apartments in commuter belts and regeneration zones.

- 4. International Investment and Currency Advantage: Sterling depreciation has enhanced foreign investor purchasing power, especially from USD- and EUR-based buyers. Demand from Middle Eastern, North American, and Southeast Asian investors remains focused on high-value real estate in Zone 1, including Mayfair, Knightsbridge, and Belgravia, while others target BTR portfolios in suburban markets.

- Regulatory and Taxation Pressures: While London offers strong legal protections for landlords, the sector faces increased regulatory oversight, including evolving Energy Performance Certificate (EPC) requirements, changes to Section 21 eviction laws, and a possible reform of council tax valuation bands. Investors must factor in potential cost escalations and compliance risks when assessing long-term viability.

- Transport and Infrastructure Improvements: Continued upgrades to Crossrail (Elizabeth Line) and expansion of cycling infrastructure are boosting accessibility in fringe districts, particularly in Ilford, Woolwich, and Abbey Wood. These transport-linked locations are seeing stronger buyer interest and rental absorption as commuting patterns evolve post-pandemic.

London Housing Market Forecast for 2026

The London Housing Market is expected to continue stabilising in 2026, with moderate price growth returning to both central and outer boroughs. Easing mortgage rates, improved buyer sentiment, and chronic undersupply will drive renewed interest across multiple segments. However, capital growth will remain uneven, with rental yields continuing to lead short-term returns.

London is forecast to deliver a balanced investment environment in 2026, with gradual capital appreciation and sustained rental inflation—particularly in value-driven districts.

Property prices in London are forecast to rise by 2.5% to 4.0% in 2026. Growth will be led by outer boroughs such as Croydon, Barking & Dagenham, and Southall, where affordability gaps and infrastructure upgrades attract first-time buyers and investors. These zones are expected to see appreciation of 4.0% to 5.5%, outperforming the citywide average.

Prime Central London (PCL) areas like Kensington, Westminster, and Mayfair will likely experience lower annual growth—between 1.5% and 2.5%—due to pricing maturity, higher entry thresholds, and transaction friction. However, these areas continue to serve as capital preservation zones with deep liquidity and international appeal.

Citywide, the average property price in Greater London is projected to reach £565,000 to £575,000 by the end of 2026, assuming macroeconomic conditions remain stable and lending terms improve.

Rental prices are expected to increase by 4.0% to 6.0%, driven by chronic undersupply, wage growth, and net inward migration. The fastest rent growth is forecast in areas with constrained supply and enhanced transport connectivity, including Walthamstow, Hackney, Stratford, and parts of West London near Heathrow.

- 2-bedroom apartments in central districts may surpass £3,000/month

- Mid-tier boroughs like Croydon and Barking are expected to see average rents reach £1,800–£2,100/month

Rental yield performance will remain strongest in peripheral districts, where entry prices remain accessible and tenant demand is rising. Gross yields of 5.5% to 6.5% are expected in these boroughs, while PCL returns will remain subdued at 2.5% to 3.5%.

Development pipelines will stay constrained. Rising construction costs, labour shortages, and planning delays will continue to limit new housing delivery, particularly in Zones 1–2. Most new inventory will come from BTR schemes and mixed-use regeneration in outer boroughs, further increasing competition for existing resale stock in undersupplied areas.

International investment will gradually return to pre-Brexit levels. Currency advantage, UK legal transparency, and easing visa-related barriers will support increased international activity—particularly in PCL and institutional rental portfolios across outer boroughs.

In summary, the London Housing Market in 2026 is forecast to deliver slow but steady price appreciation and strong rental performance. Investors focused on yield, long-term tenancy, and regeneration-linked growth will find value in transport-oriented outer boroughs, while core London remains attractive for capital stability and liquidity.

Is It Worth Buying a Property in London?

Yes—with the right timing, strategy, and location, London remains a viable investment market, especially for investors seeking rental income stability and long-term capital protection. However, expectations should be adjusted to reflect today’s pricing maturity, yield compression in premium districts, and heightened regulatory oversight.

The current average price of £548,000 positions London well above the national average, limiting short-term upside in some boroughs. But select outer districts like Barking, Croydon, and Walthamstow offer stronger rental yields (5.5%–6.5%) and room for growth as infrastructure expands and affordability pressures shift tenants further outward.

Meanwhile, Prime Central London (PCL) continues to function as a capital preservation zone, supported by deep international demand. While yields remain modest (2.5%–3.5%), price resilience, liquidity, and global appeal make PCL attractive to buyers prioritising stability over income.

Investors should also be mindful of:

- Transaction costs, including stamp duty surcharges and legal fees, which remain high by global standards.

- Evolving regulation, particularly for EPC standards, mid-term letting models, and taxation on foreign-owned property.

- Financing challenges, as interest rates—though easing—remain elevated compared to the 2010s average.

For most investors, the best opportunities lie in undervalued fringe boroughs, mid-sized rental units near transport nodes, and newly developed BTR schemes designed to meet long-term tenant demand.

Strategic purchases in these segments are more likely to generate consistent returns without overexposure to market volatility.

Other Market Forecasts & Overviews

Manchester Real Estate Market Overview & Forecast

Liverpool Real Estate Market Overview & Forecast

Bristol Real Estate Market Overview & Forecast

Derby Real Estate Market Overview & Forecast

FAQ

What is the average property price in London in 2025?

Around £548,000, with higher prices in central zones and lower prices in outer boroughs.

Are rental yields strong in London?

It depends on location. Yields are low in central areas (2.5%–3.5%) but higher in outer boroughs (5.5%–6.5%).

Where are the best areas to invest in London property?

Barking, Croydon, Walthamstow, and Southall offer strong yields and growth potential.

Can foreigners buy property in London?

Yes. There are no restrictions on foreign ownership in the UK.

Are short-term rentals legal in London?

Yes, but entire properties are limited to 90 days per year without a special license.

What type of property performs best for rental income?

2- and 3-bedroom flats in outer boroughs near transport lines provide the best balance of cost, yield, and tenant demand.

Will London property prices increase in 2026?

Yes, modest growth of 2.5%–4.0% is expected, with stronger gains in regeneration zones.