Historically, stocks have shown higher performance than real estate. The S&P 500 has delivered an average annual return of around 10%, rising to about 12% when including dividends.

In comparison, real estate returns have generally ranged from 4% to 8%, with growth that only slightly exceeds inflation.

In the past decade, from 2014 to 2024, the S&P 500 rose by 313.7%, while the Vanguard Real Estate Index increased by only 42%.

This gap highlights the differing potential of stocks and real estate as investment options over time.

Each asset class offers distinct advantages and disadvantages. Real estate provides tax benefits, tangible asset value, and serves as a stable, less volatile investment, often acting as a hedge against inflation.

Stocks, on the other hand, offer greater potential for growth but come with higher risk and volatility.

Table of Contents

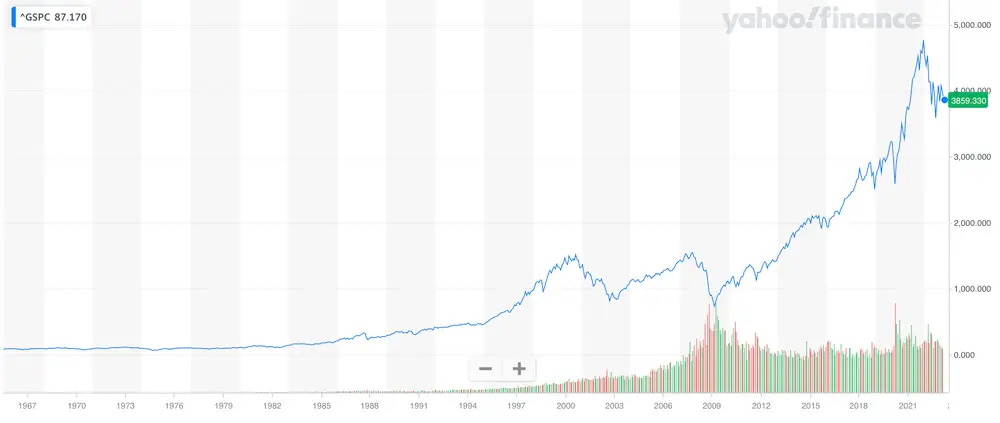

Historical Performance of the Stock Market

The stock market serves as a crucial economic indicator, with the S&P 500 reflecting its health.

It offers insights into balancing risk and potential rewards for investors. By examining its history, we gain valuable knowledge for strategic investment.

Stock Market Volatility and Returns

- Long-Term Average Annual Return: Between 1978 and 2024, the S&P 500 achieved an average annual return of approximately 12.25%.

- Recent Decade Growth: From 2013 to 2024, the index experienced a cumulative growth of about 404.47%, equating to an annualized return of 14.66%.

This growth is accompanied by volatility, influenced by various economic factors, including inflation, interest rates, geopolitical events, and corporate earnings, which can significantly impact the index’s performance.

When including dividends, the annualized return of the S&P 500 over long periods reaches around 14.66%.

This underscores the importance of considering total returns, as dividends add significant value to long-term gains, especially when reinvested.

Key Stock Market Indices

Various indices measure market performance. Historically, small-cap stocks have outperformed large-cap stocks, with an average annual return of approximately 12.1% from 1928 to 2024.

In the same period, U.S. home prices increased by about 5.4% annually. This data highlights the higher growth potential of stocks compared to real estate.

| Index | Annualized Return | Period |

|---|---|---|

| S&P 500 | 11.9% | 1928-2023 |

| Treasury Bills | 3.3% | 1928-2023 |

| Small-Cap Stocks | 12.1% | 1928-2023 |

| Vanguard Real Estate Index | 7.0% | 2013-2023 |

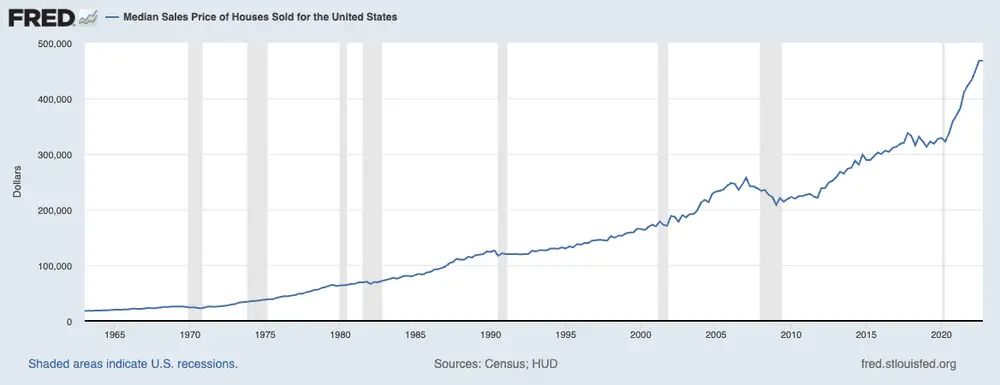

Historical Performance of the Real Estate Market

The real estate market has shown distinct trends over time, especially when comparing residential and commercial property returns.

Since 1965, residential property values have increased significantly relative to income, with an average annual return of 10.6% when including rental income. This trend highlights real estate’s potential as both a hedge against inflation and a source of appreciation.

These returns are calculated without leverage. In comparison, commercial real estate has delivered a steady average annual return of 9.5%, according to data from NCREIF.

This consistency emphasizes the stable and reliable nature of the commercial real estate market.

Residential vs. Commercial Real Estate Returns

From 1991 to 2024, U.S. single-family homes experienced an average annual appreciation of approximately 4.3%.

In contrast, commercial real estate provided average annual returns of about 9.5% during the same period.

This growth was influenced by factors such as population increases, rising homeownership rates, and inflation-driven appreciation.

Commercial properties encompass office buildings, retail spaces, industrial facilities, and warehouses.

Moreover, real estate cycles significantly impact market performance through expansion and contraction periods. These cycles greatly influence investment results.

For instance, the 2007-2008 housing crash severely reduced real estate values.

Although generally offering lower risk-adjusted returns than stocks, real estate isn’t completely shielded from downturns. Investments in real estate closely align with inflation rates, preserving value but not always exceeding inflation by a large margin.

Geographical Variations in Real Estate Performance

Geographical differences significantly influence real estate investment outcomes. Various factors, like local economic conditions and regional policies, cause growth rates to vary by region.

Cities like New York or San Francisco, for instance, often see higher appreciation and rental incomes than rural areas. This showcases the critical role of location in achieving optimal real estate investment returns.

| Aspect | Residential Real Estate | Commercial Real Estate |

|---|---|---|

| Annual Returns (1965-Present) | 9.7% (including rental income) | 9.03% |

| Market Volatility | Moderate | Lower |

| Growth Rate (1980-2023) | 8.6% | 9.2% |

| Impact of Real Estate Cycles | Significant (e.g., 2007-2008 crash) | Steady performance |

| Geographical Influence | High (varies by region) | Present (location-dependent) |

Comparing Returns: Real Estate vs Stock Investing

Historically, the S&P 500 has delivered stronger returns compared to real estate, primarily due to the growth potential of stocks.

On average, the S&P 500 index has achieved an annualized return of around 10% over the long term, a figure that surged to about 12% between March 1980 and September 2023.

When factoring in dividends, these returns increase even further, reaching over 14% annually. This makes stocks particularly appealing for investors seeking high growth over extended periods, driven by both capital appreciation and reinvested dividends.

In contrast, real estate has offered solid, though more modest, growth rates. The annualized growth rate for real estate investments over the same period was 8.6%, still a respectable figure, but generally lagging behind the performance of the stock market.

While real estate often provides more stable and tangible assets, especially in times of economic uncertainty, it typically lacks the explosive growth potential seen in equities, particularly in bull markets.

However, real estate offers other advantages such as leverage, tax benefits, and passive income through rental properties, which can boost its overall attractiveness depending on the investor’s strategy and goals.

It’s also important to consider that stocks tend to be more liquid, allowing for easier buying and selling, while real estate investments can be more illiquid and require a longer-term commitment.

Real estate returns are often less volatile than stocks, offering steady income through rental yields, whereas stock markets can experience significant short-term fluctuations.

For many investors, a well-diversified portfolio that includes both asset classes can provide a balance between growth potential and income stability.

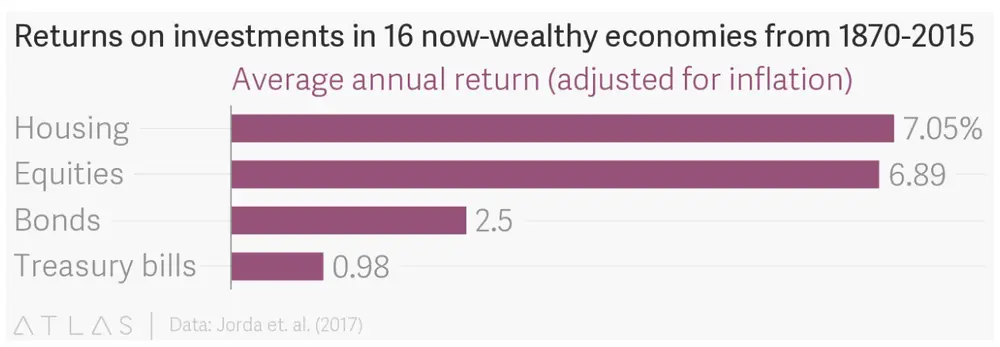

The 145-Year Study

A team of economists from the University of California, Davis, the University of Bonn, and the German central bank set out to answer these questions by analyzing a stunning amount of data collected over a 145-year period of time.

The lead authors of the study — Oscar Jorda, Katharina Knoll, Dmitry Kuvshinov, Moritz Schularick, and Alan M. Taylor — reported the findings of their massive study in a paper entitled “The Rate of Return on Everything, 1870-2015.”

In it, researchers looked at 16 advanced economies over the past 145 years to find what offers the best return on investment. They compared returns on several asset classes, including equities, residential real estate, short-term treasury bills, and longer-term treasury bonds.

To better compare apples to apples, with each asset type, they adjusted for inflation and included all returns, not just appreciation. Dividend income was included for equities, and rental income was included for residential real estate.

Their findings, in short: Residential real estate was the better investment, averaging over seven percent per annum. Equities weren’t far behind, at just under seven percent.

Then came bonds and bills with a far lower rate of return, surprising no one.

Risks Associated with Stock Market Investing

Investing in the stock market is exciting but comes with significant risks. Volatility is a major concern for investors. The S&P 500’s performance, for instance, has shown dramatic fluctuations.

While it returned approximately 12% annually from 1980 to 2023, there were notable downturns.

Managing these risks is critical in an unpredictable market. Market swings can result from various factors such as economic cycles and global events.

The sentiment of investors and corporate performance also influences market trends. Although rare, stock market crashes can severely impact investment portfolios.

Even with positive returns, the stock market is prone to drastic changes. The economic environment plays a big role in market trends.

For example, small cap stocks offer higher but riskier returns, with an average of 12.5% annually from 1968 to 2022.

Investors need to be alert and well-informed. They should watch global and economic developments that might cause market volatility. This insight, along with strategic risk management, can help navigate the challenges of stock market investing.

Risks Associated with Real Estate Investing

Investing in real estate offers potential high rewards but comes with significant risks. These challenges are distinct from those in the stock market, and understanding them is crucial for informed investment decisions.

- Market Liquidity and Asset Liquidity: Real estate lacks market liquidity, making it harder to sell properties quickly compared to stocks. Selling can take weeks or even months, posing challenges during financial emergencies or market downturns when rapid access to capital is needed.

- Maintenance and Management Costs: Real estate investments come with ongoing costs for maintenance, repairs, and tenant management. These expenses, which include property upkeep, periodic renovations, and dealing with tenant-related issues, can erode profit margins if not planned and budgeted effectively.

- Legal and Regulatory Risks: Real estate investors must navigate complex zoning laws, building codes, and tenant rights regulations. Non-compliance or sudden regulatory changes can lead to fines, legal complications, or increased operational costs, significantly affecting the profitability of investments.

- Market Volatility: Real estate markets are subject to cyclical trends and economic conditions. Property values and rental demand can be heavily influenced by factors such as local employment rates, interest rates, and overall economic stability. Market downturns in specific regions can have a prolonged negative impact on returns.

- Financing Risks: Many real estate investors rely on mortgages or financing, which exposes them to interest rate fluctuations. Rising mortgage rates can increase loan repayment costs, reduce profitability, or make refinancing less viable, creating additional financial pressure.

- Geographic Risks: Location plays a critical role in the success of real estate investments. Properties in areas with declining populations, poor infrastructure, or economic stagnation may struggle to maintain their value or attract tenants, leading to lower returns over time.

| Risk Category | Description |

|---|---|

| Market Liquidity | Longer time frames required to sell properties compared to stocks. |

| Maintenance Costs | Ongoing expenses for property upkeep and tenant management. |

| Regulatory Risks | Compliance with laws and regulations, which can impact operations. |

| Market Volatility | Economic cycles and downturns can significantly impact property values. |

| Financing Risks | Mortgage rate changes can increase costs or reduce profitability. |

| Geographic Risks | Location-dependent factors may affect property appreciation and demand. |

Case Studies: Stocks vs Real Estate Historical Returns

Analyzing historical data sheds light on real estate and stock market behaviors during significant economic downturns. Market crashes serve as vital lessons, showing the impacts and tendencies within varying financial climates.

The Great Recession of 2008

The 2008 Great Recession deeply impacted the stock and real estate markets. Property values plunged due to high leverage and flawed mortgage practices.

The stock market experienced severe losses, worsening the situation in real estate. These events highlight the linkage between these investment areas, showing the importance of history in understanding market dynamics.

The Dot-Com Bubble

The Dot-Com Bubble burst in the early 2000s, exposing the volatility of the stock market. Though mainly affecting the tech sector, its aftermath was felt widely, causing major losses. The real estate market remained less affected, pointing out the distinct risks associated with different assets during downturns.

The Housing Market Boom and Bust (1990-2006)

The era from 1990 to 2006, known as the Great Moderation, saw housing outperform stocks. But a drastic bust followed, showing the volatile nature of real estate. This downturn, caused by overvaluation and risky loans, contrasts with the stock market’s steadier, although potentially lower, returns.

Historical crash analyses provide crucial insights for investors. They help in understanding how different financial disturbances affect real estate and stocks. This knowledge is key in creating robust investment strategies.

FAQ

What makes more millionaires stocks or real estate?

Historically, real estate has created more millionaires than stocks. This is largely due to the leverage involved—people can use mortgages to buy real estate with a fraction of the total value, allowing for significant returns on a smaller initial investment.

Real estate also offers cash flow opportunities (rent), tax benefits, and long-term appreciation. On the other hand, stocks require more upfront capital for substantial gains and are subject to higher volatility.