Tax-loss harvesting is a savvy approach for investors aiming to fine-tune their taxes. It involves selling investments at a loss to neutralize earned profits elsewhere.

This method works best for optimizing taxes, reducing the amount owed on investment gains.

By doing so, investors not only decrease their taxable income but also redirect these funds into new ventures. This keeps their investment goals on track while sustaining growth opportunities.

Understanding Tax-Loss Harvesting

Tax-loss harvesting means selling securities at a loss to counterbalance realized gains. It’s a potent tax management tool, capable of deferring capital gains taxes.

If losses outpace gains, you can reduce up to $3,000 of regular income. For separate filers in a marriage, the cap is $1,500. This brings notable tax relief, especially for those in higher brackets.

The core idea behind tax-loss harvesting hinges on using losses to negate both short and long-term gains. With short-term gains taxed as high as 37%, applying losses here can be incredibly advantageous. Conversely, long-term gains face a gentler tax rate, usually between 15% and 20%.

It’s vital to recognize the yearly limit and carryforward provisions. Should capital losses surpass gains, up to $3,000 can offset general income. The remaining losses are carried forward without expiry, offsetting future gains.

However, strategy and timing are imperative. Be mindful of the wash-sale rule, which restricts deductions for buying a very similar security 30 days around the sale of the loss-generating investment.

How Tax-Loss Harvesting Works

Tax-loss harvesting is a strategy investors use to offset their capital gains and reduce their overall tax liability.

This approach leverages the fact that capital losses can be used to counterbalance capital gains, potentially lowering the amount of taxes owed on those gains.

Capital Gains and Losses

A capital gain occurs when an investor sells an asset for more than its purchase price, known as the cost basis.

The difference between the selling price and the cost basis is the gain, which is taxable in the year the asset is sold.

For example, if an investor buys stock for $25,000 and later sells it for $27,000, they realize a capital gain of $2,000. This gain would be subject to capital gains tax, which varies depending on the investor’s income and the holding period of the asset.

Conversely, a capital loss occurs when the sale price of an asset is lower than its cost basis. Using the previous example, if the investor sold the stock for $23,000 instead of $27,000, they would realize a capital loss of $2,000.

Implementing Tax-Loss Harvesting

Tax-loss harvesting comes into play when an investor deliberately sells an asset at a loss to offset a gain realized from the sale of another asset.

For instance, if the investor who realized a $2,000 gain also has another investment that has decreased in value—say, they purchased another stock for $30,000 but its value dropped to $25,000—they could sell this second stock and “harvest” the $5,000 loss.

This $5,000 loss would not only offset the $2,000 gain, eliminating the tax liability on that gain, but the remaining $3,000 of the loss could be used to offset other gains or even ordinary income, up to a certain limit.

As per IRS rules, investors can deduct up to $3,000 ($1,500 if married filing separately) of net capital losses against their ordinary income each year. Any excess losses can be carried forward to future years, allowing for continuous tax advantages.

Timing and Strategic Considerations

While tax-loss harvesting can technically be done at any time throughout the year, many investors focus on this strategy as the year-end approaches. December 31 is the critical deadline for realizing losses that can be applied to that year’s tax return.

However, there’s a risk in waiting until the end of the year; the value of an asset that could have been sold at a loss earlier might recover, reducing or eliminating the potential loss that could have been harvested.

Advocates of tax-loss harvesting suggest monitoring the portfolio throughout the year. Regularly reviewing and adjusting the portfolio can prevent missing out on potential tax-saving opportunities.

For instance, if a stock drops significantly in value during the summer, it may be wise to sell then, rather than waiting and risking a market rebound by year-end.

Compliance with IRS Regulations

It’s crucial to note the wash sale rule, which the IRS enforces to prevent investors from claiming a tax loss on a sale if they repurchase the same or a “substantially identical” security within 30 days before or after the sale.

If this rule is violated, the loss is disallowed for tax purposes and is instead added to the cost basis of the repurchased security.

This rule ensures that the tax benefit of harvesting a loss is not abused by immediately buying back the same asset.

Practical Example

Consider an investor who has made several trades throughout the year. They realized $10,000 in capital gains from selling high-performing stocks.

To offset these gains, they look at their portfolio and identify a stock that they bought for $40,000, which is now worth only $30,000. By selling this underperforming stock, they can harvest a $10,000 loss, which fully offsets the capital gains, resulting in zero taxable gains for that year.

If the investor also had another stock where they incurred a $5,000 loss, they could use this additional loss to reduce their taxable income by $3,000 and carry the remaining $2,000 forward to the next tax year.

Important Considerations for Tax-Loss Harvesting

Tax-loss harvesting can be a useful tool for reducing your tax burden, but it comes with several key considerations that can significantly impact your financial strategy.

Understanding these factors is crucial for effectively managing your capital gains and losses.

1. Short-Term vs. Long-Term Tax Rates

One of the most important aspects of tax-loss harvesting is understanding how capital gains and losses are classified by the IRS. Gains and losses are categorized as either short-term (on assets held for less than a year) or long-term (on assets held for more than a year).

- Short-Term Capital Gains: These are taxed as ordinary income, with tax rates that can reach up to 37%, depending on your income bracket. This makes short-term gains more expensive from a tax perspective.

- Long-Term Capital Gains: For most taxpayers, long-term capital gains are taxed at a lower rate, typically 15% to 20%. If your income is below certain thresholds—$44,625 for single filers or $89,250 for married couples filing jointly in 2024—your long-term gains may be taxed at 0%.

Given these differences, it’s often more beneficial to use capital losses to offset short-term gains first, as this can result in greater tax savings.

For high-income investors, offsetting income with capital losses may also be a strategic move, as it could reduce taxable income at higher marginal rates.

2. Delayed Tax Obligation

Tax-loss harvesting doesn’t eliminate your tax liability; it defers it. This strategy is effective only for taxable investment accounts and mirrors the tax-deferral benefits of accounts like IRAs and 401(k)s.

- The Benefit of Deferral: By deferring taxes, investors can reinvest the saved money, potentially allowing it to grow over time. The idea is that the compounded returns from reinvesting tax savings will outweigh the eventual tax bill when the investment is sold.

However, this strategy relies on the assumption that future gains and tax rates will remain favorable, which is not guaranteed. Therefore, while deferring taxes can be beneficial, it’s essential to weigh the long-term implications.

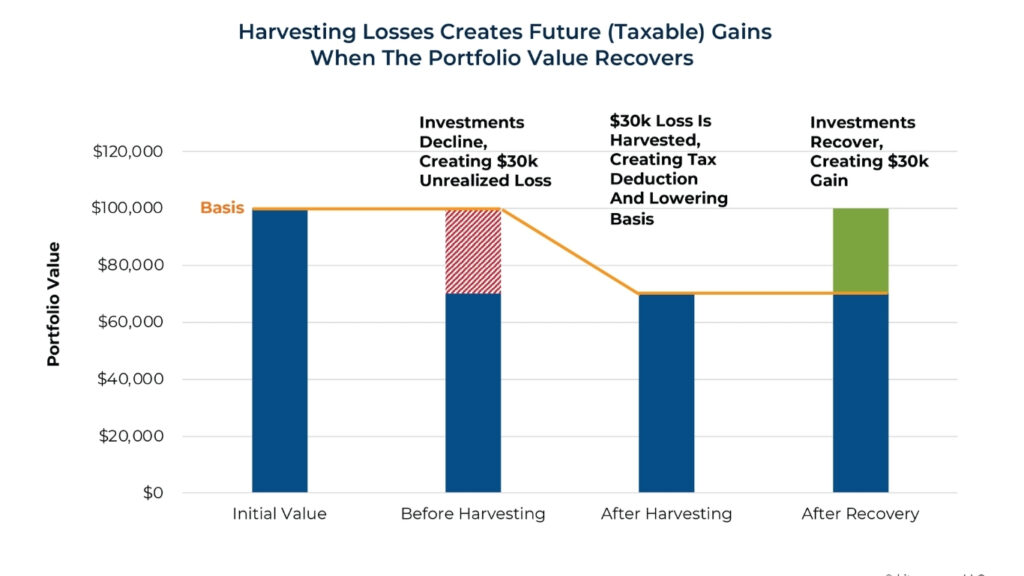

3. Impact on Cost Basis

Another critical consideration is how tax-loss harvesting affects the cost basis of your investments. The cost basis is the original value of an asset for tax purposes, which is used to calculate capital gains when the asset is sold.

- Lowering the Cost Basis: When you sell an asset at a loss and reinvest in a new security, the cost basis of the new investment will be lower than the original. This means that while you might save on taxes this year, you could face a higher tax bill in the future if the new investment appreciates.

For example, if you sell a stock with a cost basis of $30,000 for $25,000, you incur a $5,000 capital loss. If you then reinvest the $25,000 in another asset that appreciates back to $30,000, your future capital gain will also be $5,000.

Assuming a constant 15% tax rate, the $750 you saved in taxes today could lead to a $750 tax bill when you sell the new investment.

If the value increases further, say to $35,000, your future tax bill could be even higher, potentially offsetting the initial tax benefit.

This highlights the importance of understanding that tax-loss harvesting lowers your cost basis, which could lead to a higher tax liability down the line.

4. Market and Tax Rate Changes

Investors must also consider the potential for changes in market conditions and tax rates. The benefits of tax-loss harvesting depend on future market performance and the stability of current tax rates.

- Market Fluctuations: The market value of reinvested assets can increase or decrease, affecting future capital gains or losses. A significant market downturn could provide additional opportunities for tax-loss harvesting, but relying on market timing is risky.

- Tax Rate Changes: Future changes in tax policy could alter the effectiveness of your tax-loss harvesting strategy. If tax rates increase, your deferred tax bill could be higher than anticipated, reducing the net benefit of the strategy.

Given these uncertainties, it’s essential to approach tax-loss harvesting as part of a broader, long-term investment strategy rather than as a short-term tax-saving tactic.