Forty percent of all working hours worldwide are exposed to large language models right now, not in a decade, not after some distant technological tipping point. Right now.

The AI impact on jobs is not a warning from futurists sitting in conference rooms. It is a documented, measurable economic event unfolding across your industry, your portfolio, and your paycheck simultaneously.

The uncomfortable question nobody in personal finance is asking clearly enough is this: which one bleeds out first? Your career or your capital?

The answer shapes every financial decision you make in the next five years, and getting it wrong means losing on both fronts while everyone around you argues about whether AI is overhyped.

Table of Contents

Key Takeaways & The 5Ws

- You should audit your current role against published AI displacement lists to understand how exposed your income stream really is right now.

- You need to review your index fund holdings to identify companies whose business models are being structurally hollowed out by AI automation.

- You should recognize that consumer spending contraction caused by mass job displacement will eventually drag down even your best performing stocks.

- You can reduce your portfolio risk by shifting some exposure away from legacy staffing, traditional media, and enterprise software companies slow to adopt AI.

- You must treat the AI impact on jobs as a simultaneous career and investment planning problem rather than two separate issues you address at different times.

- Who is this for?

- This topic is most relevant for working professionals and retail investors who depend on both a paycheck and a portfolio to build long term financial security.

- What is it?

- The main subject is the dual threat that AI automation poses to employment income and investment returns at the same time across multiple industries.

- When does it matter most?

- This matters right now because AI displacement of jobs and the portfolio risks tied to it are already measurable economic events happening between 2022 and 2025.

- Where does it apply?

- This applies most urgently across white collar industries in the United States and globally wherever generative AI adoption is accelerating inside major corporations.

- Why consider it?

- Understanding the AI impact on jobs matters because losing on both your career and your capital simultaneously is a financial setback most households cannot recover from quickly.

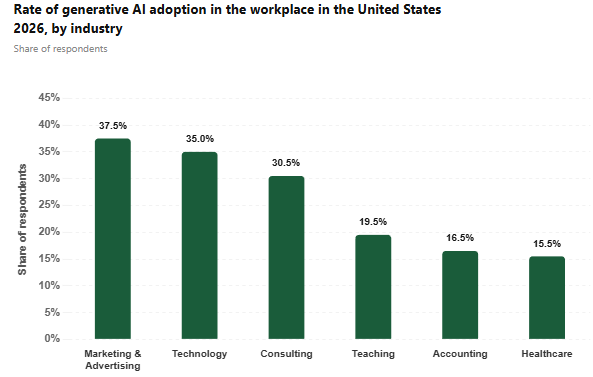

AI Impact On Jobs Is Already Here

The layoffs are not coming. They arrived, quietly, between 2022 and 2024, buried inside corporate earnings calls that celebrated “efficiency gains.” According to the McKinsey Global Institute, generative AI could automate tasks accounting for roughly 30 percent of hours worked across the United States economy by 2030.

That timeline keeps compressing as adoption accelerates. Customer service roles have already seen chatbot replacement at scale. Paralegal work, junior copywriting, basic financial analysis, entry level coding reviews, all of these categories face real contraction today.

The World Economic Forum’s 2023 Future of Jobs Report projected 83 million jobs displaced globally within five years, offset only partially by 69 million new roles. That is a net loss of 14 million positions, concentrated heavily in clerical, administrative, and repetitive cognitive work.

Which Job Categories Face the Fastest Elimination

Data entry clerks, payroll processors, and customer service representatives sit at the top of every credible displacement list. Goldman Sachs research estimated that roughly 300 million full time jobs globally face some degree of automation exposure from generative AI alone.

White collar workers who assumed automation only threatened factory floors are now watching their own task lists shrink. Graphic designers, junior marketers, and mid level accountants are all experiencing the same gradual erosion of billable hours and entry level hiring.

Your industry almost certainly appears somewhere on that list.

Percent of total US jobs lost to AI and automation

Forecast · Base year 2022

How AI Quietly Crashes Your Portfolio

Your retirement account does not care whether you personally lose your job. It does care when entire sectors stop generating the earnings that justified their valuations. AI job loss investments represent a category of risk most retail investors have not priced in.

When companies automate aggressively, the short term stock bump from cost cutting eventually collides with a longer term problem: displaced workers stop spending.

Consumer discretionary stocks suffer. Regional banks that lend to middle income households see loan quality deteriorate. Legacy media companies, traditional staffing agencies, and brick and mortar retail chains all face compounding structural headwinds that index fund holders absorb without realizing it.

Your S&P 500 index fund carries exposure to dozens of companies whose core business models are actively being hollowed out by AI efficiency gains passed on to shareholders today and extracted from consumers tomorrow.

Traditional staffing companies like Robert Half International have already reported declining revenues as businesses reduce contract hiring in favor of AI tools. Transcription services, translation platforms built on human labor, and legacy enterprise software companies that cannot integrate AI fast enough are all watching their moats drain.

You probably hold some of these through broad index exposure without knowing it.

Job Loss Or Wealth Loss Hits First

Here is the honest answer most financial writers avoid giving you. Wealth erosion from AI disruption almost certainly hits before direct job loss does, for most people, most of the time. Markets price in disruption years before layoffs appear on your street. The internet boom taught us exactly this pattern.

Between 1995 and 2000, retail investors poured money into companies that the market eventually repriced violently, while actual employment dislocations from digitization took until 2005 to register clearly in Bureau of Labor Statistics occupational data. AI is moving faster, which compresses that gap significantly.

Consider the sequencing side by side.

Portfolio erosion begins the moment markets reprice legacy sector valuations downward, which happens on a quarterly earnings cycle. Job displacement hits individuals on a contract renewal cycle, a performance review cycle, or a budget cut cycle, all of which lag market signals by months or years. You feel wealthier longer than you are, and you feel employed longer than your role is structurally secure.

The severity question cuts differently. Losing 20 percent of your portfolio value hurts. Losing your income entirely is catastrophic. Both risks are real, but the sequence means you likely have a window to act on investment exposure before the personal employment crisis becomes acute.

That window is not infinite. Sectors repricing right now will complete much of their correction within 24 to 36 months based on historical disruption cycles.

How To Protect Finances From AI Disruption

Knowing the threat is arriving is worthless unless you do something concrete before it lands fully. To protect finances from AI disruption, you need to act across three dimensions simultaneously: your income structure, your portfolio allocation, and your emergency reserves. On the income side, the most durable move is skill adjacency, not wholesale career reinvention.

You do not need to become a machine learning engineer. You need to become the person in your existing field who uses AI tools better than anyone else in your organization. That positioning raises your value while your peers become redundant. Emergency fund sizing deserves recalibration too. The traditional three to six month standard assumed a stable job market.

An AI disrupted labor market with compressed hiring cycles and longer unemployment spells for displaced mid career workers warrants nine to twelve months of liquid reserves.

First, reduce overconcentration in sectors with the highest automation exposure, including traditional media, legacy financial services, and labor intensive retail.

Second, rotate toward AI infrastructure plays such as semiconductor companies, data center operators, and energy providers serving compute demand, because someone profits enormously from every job AI eliminates.

Third, add exposure to sectors where human judgment remains legally or ethically required, including healthcare services, skilled trades, and high stakes professional advisory roles. These are not glamorous growth bets. They are structural hedges against an AI economy collapse in legacy industries.

Winning While the AI Economy Shifts

Every major technological disruption has produced a cohort of people who read the shift correctly and positioned ahead of the crowd. The internet did not kill commerce. It killed Borders Books and created Amazon. AI will not kill work. It will kill specific configurations of work while creating enormous demand for people who can orchestrate, audit, and apply AI systems in real world contexts.

Prompt engineering, AI output auditing, human oversight roles in regulated industries, and AI literacy training are all generating real income today. According to LinkedIn’s 2024 Workplace Report, AI related skills were among the fastest growing competencies on the platform, with demand outpacing supply in multiple sectors.

Capital is also flowing toward winners in this shift. Cybersecurity firms protecting AI infrastructure, biotech companies using AI for drug discovery, and climate technology companies leveraging AI for energy optimization are all absorbing both displaced investment dollars and newly skilled workers.

You sit at a rare historical inflection point where understanding the sequencing of these twin threats, portfolio erosion first, employment disruption second, gives you genuine advance notice most people will not use.

The workers and investors who treat AI as a background concern will absorb the full cost of disruption passively. The ones who act now will look back at 2025 as the year they made the decisions that protected and grew everything they had built.