Investing can be a powerful tool for building wealth, but it comes with its own set of challenges and risks.

Whether you’re a seasoned investor or just starting out, asking the right questions before making investment decisions is crucial.

The right questions can help you avoid common pitfalls, maximize your returns, and align your investments with your financial goals.

This article will explore the most crucial questions every investor needs to ask, providing detailed insights and strategies to ensure you’re making informed and sound investment decisions.

Table of contents

- 1. What Are My Investment Goals?

- 2. What Is My Risk Tolerance?

- 3. How Diversified Is My Portfolio?

- 4. What Are the Costs and Fees Associated With My Investments?

- 5. What Is My Investment Time Horizon?

- 6. How Will This Investment Fit Into My Overall Financial Plan?

- 7. What Is the Historical Performance of This Investment?

- 8. What Are the Tax Implications of This Investment?

- 9. How Liquid Is This Investment?

- 10. What Are the Potential Risks of This Investment?

- 11. What Is the Management Style of This Investment?

- 12. How Will I Monitor and Review My Investments?

- 13. What Are My Exit Strategies?

- 14. What Impact Will Inflation Have on My Investments?

- 15. How Will Market Volatility Affect My Investments?

- Conclusion

1. What Are My Investment Goals?

The first and most important question every investor needs to ask is, “What are my investment goals?”

Understanding why you are investing will guide all other decisions, from the type of assets you choose to the level of risk you’re willing to take.

Investment goals can vary widely depending on your stage in life, financial situation, and personal aspirations.

For instance, if you’re saving for retirement, your investment strategy might focus on long-term growth with a diversified portfolio that includes stocks, bonds, and real estate.

On the other hand, if you’re saving for a shorter-term goal, such as buying a house, you might prioritize capital preservation and liquidity, investing in safer, low-risk assets.

Statistics show that investors who clearly define their goals are more likely to stick with their investment plan and achieve better outcomes.

A survey found that 70% of successful investors had a well-defined set of financial goals, compared to just 33% of those who struggled with their investments.

2. What Is My Risk Tolerance?

Risk tolerance is a critical factor in determining your investment strategy. It refers to your ability and willingness to endure market volatility and potential losses in pursuit of higher returns.

Investors with a high-risk tolerance may be more comfortable investing in volatile assets like stocks or cryptocurrencies, while those with a lower risk tolerance may prefer bonds or fixed-income investments.

Understanding your risk tolerance is essential because it helps you avoid making impulsive decisions during market downturns.

According to research, 55% of investors who experienced significant losses in a market downturn said they had overestimated their risk tolerance.

By accurately assessing your risk tolerance upfront, you can build a portfolio that aligns with your comfort level and helps you stay the course during market fluctuations.

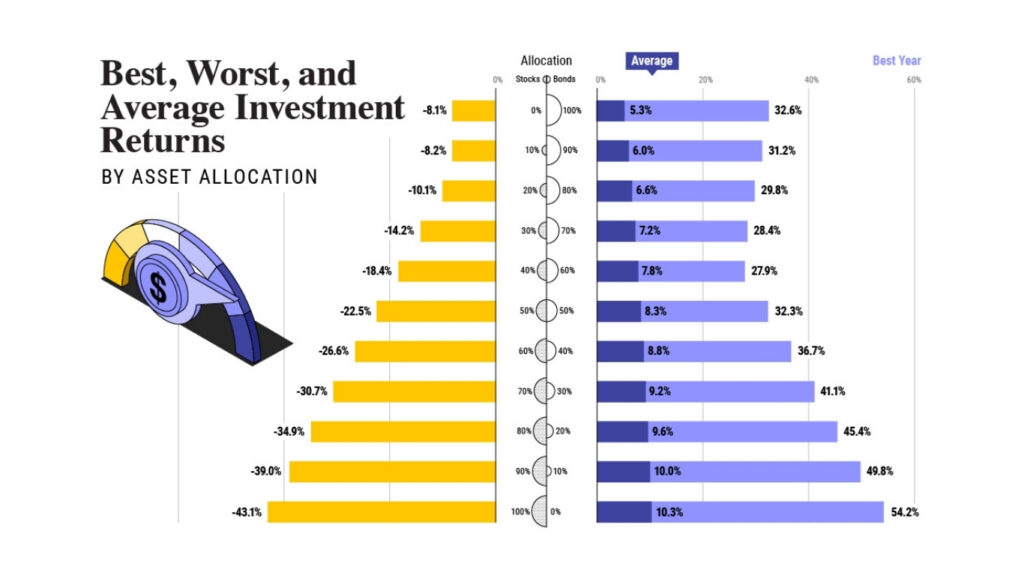

3. How Diversified Is My Portfolio?

Diversification is one of the fundamental principles of investing. It involves spreading your investments across different asset classes, industries, and geographic regions to reduce risk.

The idea is that a diversified portfolio is less likely to experience significant losses because the performance of one asset or sector is less likely to impact your entire portfolio.

A well-diversified portfolio typically includes a mix of stocks, bonds, real estate, and possibly alternative investments like commodities or private equity.

Data shows that diversified portfolios are more resilient during market downturns. For example, during the 2008 financial crisis, diversified portfolios that included bonds and real estate performed better than those concentrated solely in stocks.

Investors should regularly review their portfolios to ensure they remain diversified, especially after significant market movements.

Failing to diversify properly can expose you to unnecessary risk and limit your long-term growth potential.

4. What Are the Costs and Fees Associated With My Investments?

Investment costs and fees can have a significant impact on your overall returns. Even seemingly small fees can compound over time, eating into your profits.

Common fees include management fees for mutual funds or ETFs, trading commissions, and advisory fees if you’re working with a financial advisor.

Before making any investment, it’s crucial to understand all the associated costs. For instance, the average expense ratio for actively managed mutual funds is around 1%, while for passive index funds, it’s closer to 0.1%.

Over a 30-year period, that difference can add up to tens of thousands of dollars in lost returns.

Investors should also be aware of hidden costs, such as bid-ask spreads or fees associated with early withdrawals from retirement accounts.

A study found that investors who actively managed their fees by choosing low-cost investment options saved an average of 1.2% per year, which significantly enhanced their long-term returns.

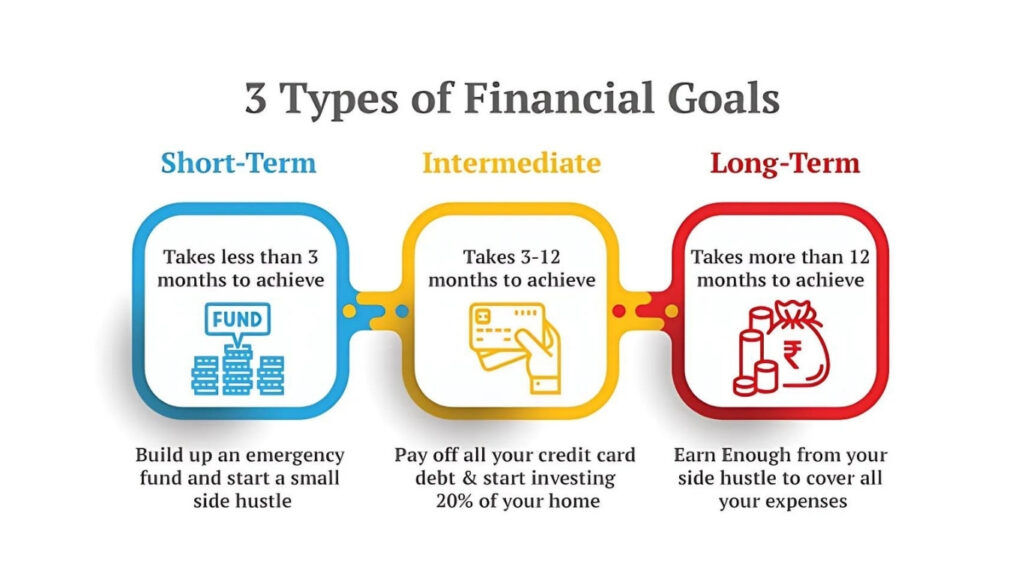

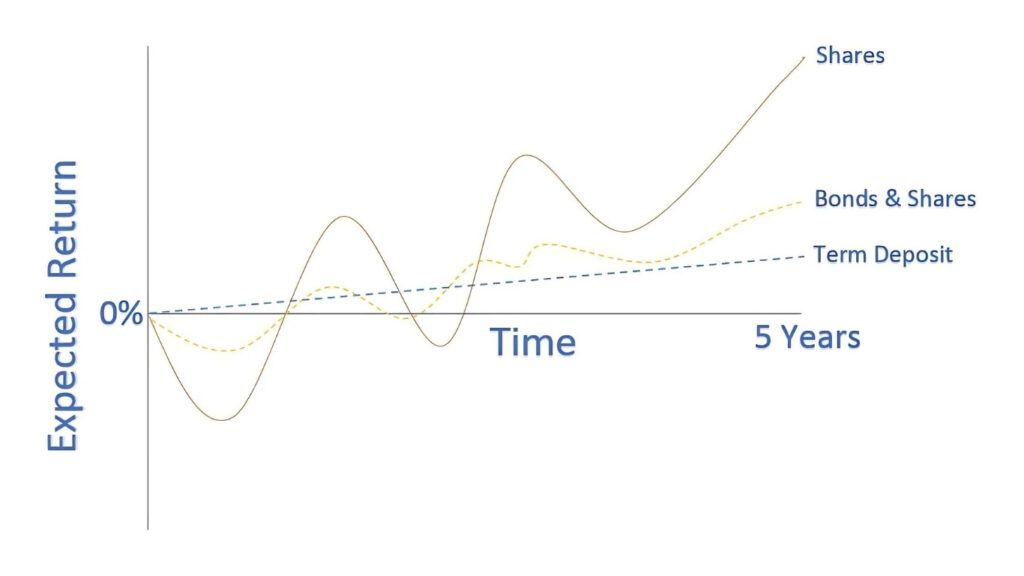

5. What Is My Investment Time Horizon?

Your investment time horizon is the length of time you expect to hold an investment before you need to access the funds. It is a critical factor in determining your asset allocation and risk level.

Generally, the longer your time horizon, the more risk you can afford to take, as you have more time to recover from potential losses.

For example, if you’re investing for retirement and have 30 years before you need the money, you might be more heavily invested in stocks, which have historically provided higher returns over the long term.

Conversely, if you need the money in five years, you might opt for a more conservative portfolio with a higher allocation to bonds or cash equivalents.

Research shows that investors with longer time horizons tend to achieve better returns because they can ride out short-term volatility.

A study found that investors who held onto their investments for 10 years or more were significantly more likely to achieve positive returns compared to those who invested for shorter periods.

6. How Will This Investment Fit Into My Overall Financial Plan?

Investing should be part of a broader financial plan that includes saving, budgeting, tax planning, and estate planning. Before making any investment, it’s important to consider how it fits into your overall financial strategy.

Does it help you achieve your long-term goals? Does it align with your risk tolerance and time horizon? Is it tax-efficient?

For instance, if you’re in a high tax bracket, you might consider tax-advantaged accounts like IRAs or 401(k)s, which offer tax-deferred or tax-free growth.

Alternatively, if you’re investing in taxable accounts, you might focus on tax-efficient investments, such as index funds or municipal bonds, which generate less taxable income.

A comprehensive financial plan can help you make more informed investment decisions and ensure that your investments are working in harmony with other aspects of your financial life.

Studies show that investors who follow a well-defined financial plan are more likely to achieve their financial goals and feel more confident about their financial future.

7. What Is the Historical Performance of This Investment?

While past performance is not indicative of future results, understanding the historical performance of an investment can provide valuable insights into its potential risks and returns.

Before investing, it’s essential to research how the investment has performed over different market cycles, including bull and bear markets.

For example, reviewing the historical performance of a stock or mutual fund can help you understand its volatility, average annual returns, and how it compares to its benchmark index.

It’s also important to consider the investment’s performance during market downturns, as this can give you an idea of how it might perform during future crises.

According to a study, investments with a strong track record of consistent returns and lower volatility tend to perform better over the long term.

However, investors should avoid chasing past performance alone and instead focus on the underlying fundamentals of the investment.

8. What Are the Tax Implications of This Investment?

Taxes can significantly impact your investment returns, so it’s crucial to consider the tax implications of any investment before you commit. Different types of investments are subject to different tax treatments, and your overall tax strategy should be aligned with your investment goals.

For example, capital gains taxes apply to the profits you make from selling an investment, with short-term gains taxed at higher rates than long-term gains.

Dividends and interest income are also taxed differently, depending on the type of investment and your tax bracket.

Tax-efficient investing strategies, such as holding investments in tax-advantaged accounts, using tax-loss harvesting, and selecting tax-efficient funds, can help you minimize your tax liability and maximize your after-tax returns.

A study found that investors who employed tax-efficient strategies increased their after-tax returns by an average of 1.5% per year, highlighting the importance of considering taxes in your investment decisions.

9. How Liquid Is This Investment?

Liquidity refers to how easily an investment can be converted into cash without significantly affecting its value.

Highly liquid investments, such as stocks and bonds, can be sold quickly at market prices, while less liquid investments, such as real estate or private equity, may take longer to sell and could require selling at a discount.

Before investing, it’s essential to consider your liquidity needs and whether the investment aligns with them.

For instance, if you anticipate needing access to your funds in the near future, investing in highly liquid assets is crucial.

On the other hand, if you have a long-term time horizon, you may be more comfortable investing in less liquid assets that offer higher potential returns.

Research shows that investors who fail to consider liquidity risk can face significant challenges during market downturns, when selling illiquid assets may result in substantial losses.

By carefully assessing the liquidity of your investments, you can ensure that you have access to funds when needed without compromising your financial goals.

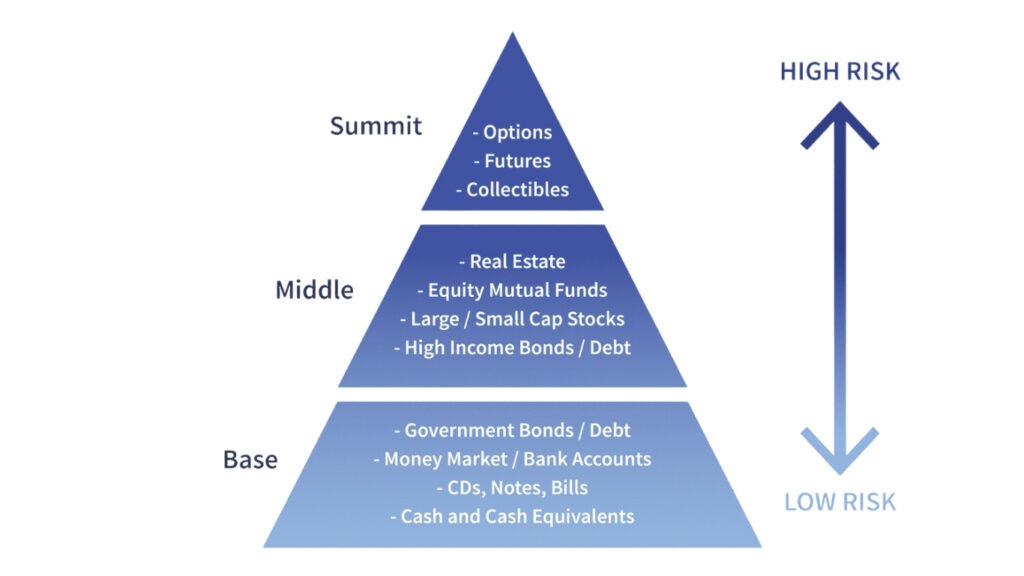

10. What Are the Potential Risks of This Investment?

Every investment carries some level of risk, and understanding these risks is essential for making informed decisions.

Before investing, it’s crucial to identify the potential risks associated with the investment, including market risk, credit risk, interest rate risk, and liquidity risk.

Market risk refers to the possibility of losing money due to fluctuations in the market, while credit risk is the risk that the issuer of a bond or other debt instrument will default on their payments.

Interest rate risk is the risk that changes in interest rates will affect the value of an investment, particularly bonds.

Liquidity risk, as mentioned earlier, is the risk of being unable to sell an investment quickly without incurring a loss.

According to studies, investors who conduct thorough risk assessments and diversify their portfolios are better equipped to manage these risks and achieve their financial goals.

By understanding the potential risks and how they may impact your investment, you can make more informed decisions and avoid unnecessary losses.

11. What Is the Management Style of This Investment?

The management style of an investment, particularly in mutual funds, ETFs, and hedge funds, can have a significant impact on its performance.

There are two primary management styles: active and passive. Active management involves a portfolio manager or team making decisions about which securities to buy and sell in an attempt to outperform the market.

Passive management, on the other hand, involves tracking a market index, such as the S&P 500, with the goal of matching its performance.

Active management often comes with higher fees due to the costs associated with research and trading. However, not all actively managed funds outperform their passive counterparts.

According to data, only about 20% of actively managed funds consistently outperform their benchmarks over the long term.

Before investing, it’s essential to understand the management style of the fund or investment and how it aligns with your investment goals and risk tolerance.

If you’re looking for lower costs and more predictable performance, passive investments may be a better choice. Conversely, if you’re willing to pay higher fees for the potential of outperforming the market, active management might be more suitable.

12. How Will I Monitor and Review My Investments?

Investing is not a set-it-and-forget-it activity. Regularly monitoring and reviewing your investments is crucial to ensure they continue to align with your goals and risk tolerance.

This involves tracking the performance of your investments, staying informed about changes in the market, and making adjustments as needed.

Many investors set up a regular schedule for reviewing their portfolios, such as quarterly or annually.

During these reviews, it’s important to assess whether your asset allocation still matches your risk tolerance, whether any investments have underperformed, and whether there are any new opportunities to consider.

A study found that investors who regularly reviewed and rebalanced their portfolios achieved better long-term returns compared to those who did not.

By staying engaged with your investments and making informed decisions based on current information, you can better navigate market changes and achieve your financial goals.

13. What Are My Exit Strategies?

Knowing when and how to exit an investment is just as important as knowing when to enter. An exit strategy is a plan for selling an investment, whether to lock in profits, limit losses, or free up capital for other opportunities.

Common exit strategies include setting a target price at which you’ll sell an investment, using stop-loss orders to automatically sell if the price drops below a certain level, and planning to exit when an investment no longer aligns with your financial goals.

Having a clear exit strategy can help you avoid emotional decision-making and ensure that you maximize your returns.

Research shows that investors who use disciplined exit strategies are more likely to achieve their financial goals and avoid significant losses during market downturns.

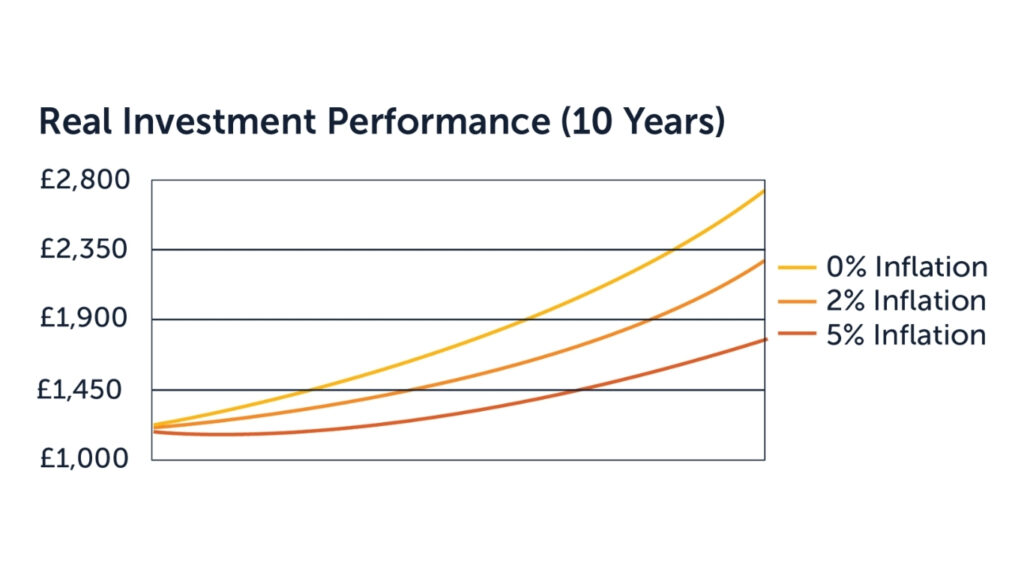

14. What Impact Will Inflation Have on My Investments?

Inflation erodes the purchasing power of your money over time, which can significantly impact the real returns on your investments. It’s essential to consider how inflation might affect your investments and to choose assets that can help protect against inflation.

For example, stocks have historically outpaced inflation over the long term, making them a good hedge against rising prices. Real estate and commodities, such as gold, are also considered inflation-resistant assets.

On the other hand, fixed-income investments like bonds may lose value in real terms if inflation rises significantly.

Investors should consider including assets in their portfolios that are likely to perform well in an inflationary environment.

A study found that portfolios with a mix of stocks, real estate, and commodities were better able to withstand the effects of inflation compared to those heavily weighted in bonds or cash.

15. How Will Market Volatility Affect My Investments?

Market volatility refers to the fluctuations in asset prices over time. While some level of volatility is normal, extreme volatility can lead to significant gains or losses in a short period.

Understanding how volatility might affect your investments is crucial for managing risk and staying on track with your financial goals.

During periods of high volatility, it’s essential to remain calm and avoid making impulsive decisions. Long-term investors who stick to their investment strategy during volatile times are often rewarded with better returns than those who panic and sell.

According to data, investors who stayed invested during the 2008 financial crisis and continued to contribute to their portfolios during the downturn saw significant gains during the recovery.

By maintaining a long-term perspective and focusing on your investment goals, you can better manage volatility and achieve your desired outcomes.

Conclusion

Investing is a complex and dynamic process that requires careful consideration and informed decision-making.

By asking the crucial questions outlined in this article, you can ensure that your investment strategy aligns with your financial goals, risk tolerance, and overall financial plan.

From understanding your investment goals and risk tolerance to considering the impact of taxes, fees, and inflation, these questions provide a framework for making sound investment decisions.

Remember, successful investing is not about predicting the future but about being prepared and making informed choices based on thorough research and a clear understanding of your financial objectives.

By staying disciplined and regularly reviewing your investments, you can navigate the uncertainties of the market and build a portfolio that supports your long-term financial success.