The Al Ain real estate market in 2026 is entering a phase of steady evolution, driven by targeted government housing initiatives, improved infrastructure, and growing interest from investors seeking long-term value in the UAE’s more traditional urban centers. Often overshadowed by Abu Dhabi and Dubai, Al Ain is now gaining traction for its price stability, sustainable rental demand, and alignment with broader national housing goals.

As the UAE’s fourth-largest city, Al Ain offers an alternative real estate profile, one that favors consistent performance over rapid speculation.

In 2024, Al Ain recorded a modest but reliable growth rate of approximately 4% in residential capital values, outperforming early-year projections that forecast market stagnation. Key residential districts, particularly Al Hili, Zakher, and Al Jimi, have seen rising transaction volumes and improved occupancy across both apartments and villas.

Much of this activity is supported by government-driven housing programs and enhanced connectivity via inter-emirate transport links.

For investors, the market’s appeal lies in its low volatility, affordable price per square meter, and dependable yields in villa submarkets. With limited speculative building and a predominantly end-user-driven buyer base, Al Ain presents a distinctly different but no less strategic opportunity in the UAE real estate market. If you want to understand how to model these kinds of opportunities properly, real estate investment modeling is worth getting familiar with before you commit capital.

Table of Contents

Overview of The Al Ain Real Estate Market

As of early 2026, the Al Ain real estate market is exhibiting measured growth, marked by price resilience and localized demand across its residential segments. Unlike the high-volume markets of Dubai and Abu Dhabi, Al Ain’s real estate market is dominated by end-users and government-supported housing allocations, resulting in slower but steadier appreciation.

The median listing price for residential properties currently sits at approximately AED 970,000, with median sold prices averaging AED 940,000. That narrow pricing spread tells you something important. Buyer and seller expectations are closely aligned, which points to a healthy, balanced market.

Demand has stayed stable for family villas in Al Hili, Al Yahar, and Al Jimi, where new infrastructure and planned community developments are actively taking shape.

Transaction volumes across Al Ain have held firm, supported by steady government-backed housing activity and local purchasing. While total deal numbers stay lower than those in the major emirates, sales have become more consistent, particularly in mid-tier villa communities. Homes are selling within 45 days on average, a slight acceleration from the 50-day benchmark observed in Q2 2024.

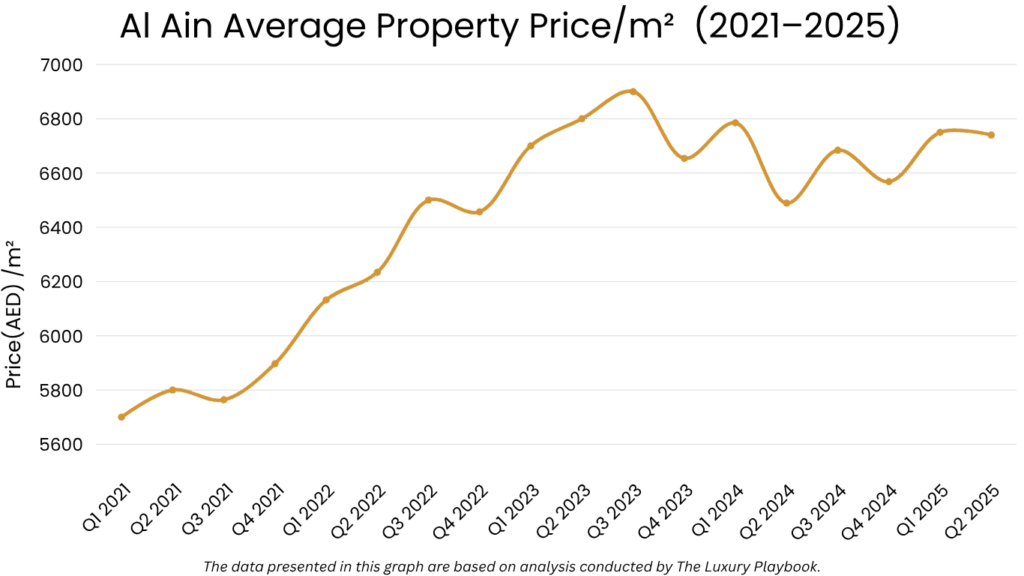

The average price per square meter across Al Ain currently sits at AED 6,740 (USD 1,840). Prices vary by district and property type. Apartments in central zones like Al Mutaredh are priced at around AED 6,000 per sqm, while newer villas in suburban areas can range between AED 7,200 and AED 8,000 per sqm, depending on finishes and location.

Inventory levels stay limited, particularly in high-demand villa submarkets where construction pipelines are relatively modest. That constrained supply continues to support price stability and prevents downward pressure on resale values.

- Median residential price at AED 970K, with strong buyer-seller alignment.

- Average homes selling in 45 days, up from 50 days in early 2024.

- AED 6,750 per square meter average, with higher prices in villa zones.

- Sales activity concentrated in family-oriented villa districts like Al Hili and Al Jimi.

- Inventory remains tight, especially in suburban freehold areas.

The Al Ain housing market in 2026 is defined by controlled growth, limited speculative activity, and a strong foundation of owner-occupier demand. For investors, the market offers price stability, consistent transaction patterns, and reliable long-term positioning. You can see how this compares to a more mature Gulf market by reading our Abu Dhabi real estate market overview.

Neighborhood Analysis

Al Ain’s housing market is defined by a distinct set of neighborhoods that vary in price, demand, and development stage. Unlike the high-rise urban environments of Dubai and Abu Dhabi, Al Ain’s communities are primarily low-density, villa-based districts with strong ties to family living and cultural identity. Each neighborhood carries its own investment profile, whether you’re targeting rental income, long-term occupancy, or land appreciation.

Al Hili

Al Hili stands out as one of Al Ain’s most sought-after residential areas, known for its spacious villas, proximity to key schools, and well-developed infrastructure. It consistently draws mid-to-upper-income Emirati families, as well as long-term expatriates.

The median home price in Al Hili sits at approximately AED 1.4 million, reflecting a 4.2% year-over-year increase. Properties tend to transact quickly due to limited supply and high end-user demand. Investor interest centers around newer villa compounds offering modern layouts and private gardens.

Al Jimi

Located near key government institutions and shopping centers, Al Jimi ranks as one of Al Ain’s most central and active residential neighborhoods. You’ll find a balanced mix of traditional homes and new-build townhouses here.

The median home price in Al Jimi sits at AED 1.15 million, with prices growing 3.8% over the past year. Demand stays consistent for well-maintained resale villas and three-bedroom townhomes with proximity to Al Ain Mall and healthcare facilities.

Zakher

Zakher is a well-established community in western Al Ain, popular among Emirati households and increasingly among younger expatriate families due to its affordability and easy access to city entry roads.

The median price in Zakher sits at AED 980,000, with a 4.1% increase year-over-year. The area features older villas with larger plots, which investors often upgrade to boost value and rental yield. Rental demand is driven by tenants seeking space and privacy at competitive rates.

Neighborhood Median Prices and Price per Square Meter

| Neighborhood | Median Listing Home Price |

|---|---|

| Al Hili | AED 1.4M |

| Al Jimi | AED 1.15M |

| Zakher | AED 980K |

| Al Yahar | AED 810K |

| Al Mutaredh | AED 720K |

Al Ain Rental Market Overview

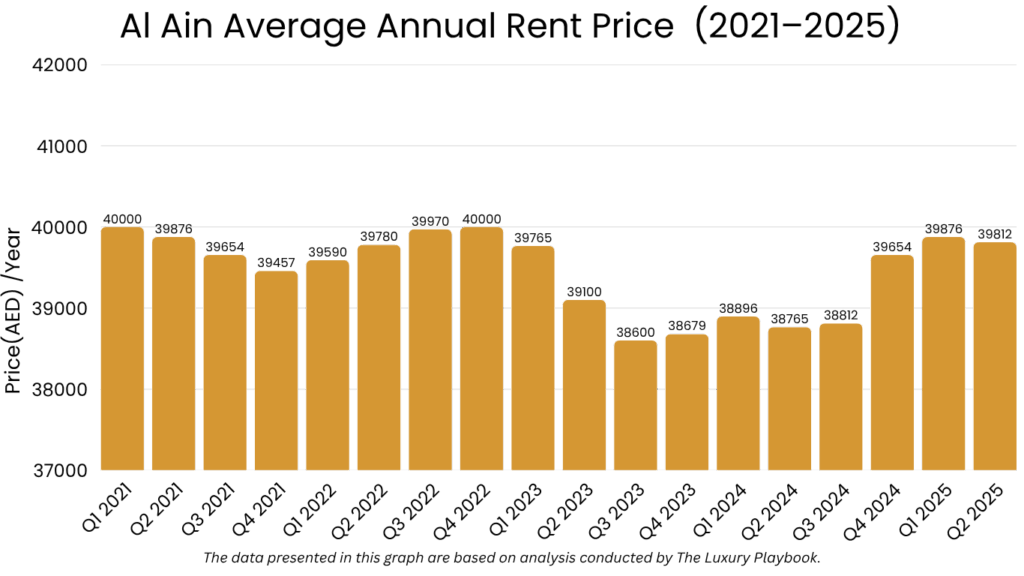

The Al Ain rental market in 2026 stays steady, supported by long-term tenancy demand, government-linked employment, and an overall shortage of quality mid-size family housing. Unlike larger UAE cities, Al Ain’s tenant base is primarily composed of residents seeking stable, multi-year leases rather than transient, short-term arrangements.

Average rental rates across the city increased by 3.4% year-over-year, driven by moderate inflation and limited new supply. The most active leasing segments include three- and four-bedroom villas in established family neighborhoods and compact apartment units in centrally located zones such as Al Mutaredh.

Average Rent Prices by Unit Type

- Studio Apartments: AED 18,000/year (USD ~4,900)

- 1-Bedroom Apartments: AED 28,000/year (USD ~7,620)

- 2-Bedroom Apartments: AED 38,000/year (USD ~10,330)

- 3-Bedroom Villas: AED 65,000/year (USD ~17,680)

- 4-Bedroom Villas: AED 78,000/year (USD ~21,200)

Villa communities stay the strongest performing segment, with family-sized homes in Al Hili and Zakher frequently leasing within 30 days of listing. In Al Mutaredh, demand for smaller apartment units is rising due to proximity to city services and consistent occupancy from local professionals and students.

Rent by Neighborhood

- Al Hili: Four-bedroom villas lease for AED 80,000/year on average, supported by high tenant retention and low turnover.

- Al Jimi: Three-bedroom villas average AED 62,000/year, with solid demand from mid-income local families.

- Zakher: Older villas lease for AED 55,000–60,000/year, offering competitive yields for value-focused landlords.

- Al Yahar: Two-bedroom units lease for AED 35,000/year, supported by affordability and access to city outskirts.

- Al Mutaredh: One-bedroom apartments average AED 28,000/year, with consistent leasing activity near retail corridors.

Vacancy Rates and Market Dynamics

Vacancy rates in Al Ain are currently estimated at 5.8%, slightly above national averages due to the slower turnover of owner-occupied properties. That said, leasing velocity stays healthy in districts with updated housing stock and access to public services. Most tenants sign 12 to 24-month leases, reducing volatility and enhancing income reliability for landlords.

The rental market is largely driven by the public sector, education professionals, and long-term expatriate families. As a result, the city experiences less seasonality compared to major commercial hubs, giving investors more predictable cash flow patterns throughout the year.

Al Ain’s rental market offers stable returns, especially in villa communities where supply stays tight and tenant loyalty is high. For investors targeting steady yields with low management turnover, Al Ain’s long-lease culture and affordability provide compelling advantages. For a broader perspective on how rental property stacks up against other asset classes, take a look at this comparison of real estate vs stock investing performance.

Factors Influencing The Al Ain Housing Market

The Al Ain housing market in 2026 is being shaped by a mix of demographic shifts, infrastructure investments, affordability dynamics, and a stable local economy. These factors contribute to the city’s slow but consistent pace of residential activity and distinguish it from the volatility seen in larger emirates.

- Government Housing Initiatives: Al Ain continues to benefit from targeted Emirati housing programs, including land grants and villa allocations for nationals. These programs have supported demand in suburban communities and contributed to the growth of new residential zones like Al Yahar and Zakher. These developments provide end-user stability and prevent speculative overbuilding.

- Price Accessibility: Compared to Abu Dhabi and Dubai, Al Ain offers a significantly lower price point for both ownership and rental. The average price per square meter remains under AED 7,000, making it one of the most affordable villa-dominated markets in the UAE. This accessibility encourages family formation, long-term leasing, and mid-income investment activity.

- Infrastructure and Community Expansion: Ongoing upgrades to roads, schools, and healthcare facilities have enhanced the liveability of Al Ain’s outer neighborhoods. Improved road access to Abu Dhabi city and the Al Ain–Dubai corridor supports demand in fringe areas while facilitating commuting and economic integration with larger employment hubs.

- Low Speculative Pressure: Al Ain’s market is dominated by end-users and long-term holders rather than speculative investors. This has resulted in a low-volatility environment where prices adjust gradually and are less sensitive to macroeconomic swings or global interest rate cycles. Stability makes the market more appealing to conservative investors and family buyers.

- Public Sector Employment: A large portion of Al Ain’s workforce is employed in government, education, healthcare, and defense. These sectors offer income security and stable leasing demand. Communities located near hospitals, universities, and municipal offices consistently report low vacancy and high tenant retention.

- Rental Dependability and Yield Potential; Although Al Ain does not offer the highest capital gains in the UAE, it provides reliable rental yields ranging from 6% to 8%, particularly in villa districts with limited new supply. The long-term nature of tenancy contracts supports landlords seeking lower turnover and predictable income streams.

Al Ain Housing Market Forecast for 2026

Looking ahead through 2026, the Al Ain housing market is expected to maintain its pattern of slow but stable growth. Market momentum will likely be shaped by continued government housing support, population growth, and improved infrastructure connectivity to other emirates.

The pace of appreciation is not expected to accelerate dramatically. But Al Ain will likely stay a reliable residential market for long-term investors who know what they’re buying into.

Residential property prices in Al Ain are projected to increase by 3% to 4.5% by the end of 2026. With the current median home price near AED 970,000, that would place average values between AED 1 million and AED 1.014 million, depending on location and property type. Family-oriented villa districts such as Al Hili, Zakher, and Al Jimi are expected to outperform smaller apartment zones due to constrained supply and consistent demand.

Inventory will stay limited in most districts. Although a few pipeline projects exist on the outskirts, most developers are focusing on government partnerships or small-scale expansions. The absence of overbuilding will help maintain price stability across both the primary and resale markets.

Districts with planned infrastructure investments and access to employment centers are likely to lead in price resilience and absorption.

Rental rates are also expected to grow moderately. Lease prices across the city are forecast to increase by 2.5% to 4%, as tenant demand stays strong in villa communities and small-unit apartment zones. Two-bedroom apartments may average AED 39,500 to AED 41,000 per year, while four-bedroom villas could approach AED 82,000 per year in high-demand areas.

Vacancy rates are expected to stay low, particularly in districts with proximity to public sector institutions and university zones. Leasing stability will likely continue to define Al Ain’s rental sector, giving landlords consistent returns with minimal turnover.

From an economic standpoint, Al Ain’s reliance on public employment, education, and medical infrastructure will act as a buffer against market volatility. Speculative upside is limited, but so is downside risk, making the market genuinely attractive for income-oriented investors and long-term residents.

Demographic trends also support slow but steady expansion. The city’s growing population and young family base will continue to drive demand for affordable, villa-based housing in community-oriented neighborhoods. IPS 2026 is worth tracking if you want a broader view of where smart real estate capital is flowing across the region.

Is It Worth Buying a Property in Al Ain?

Buying property in Al Ain in 2026 can be a sound decision for investors prioritizing long-term stability, consistent rental income, and conservative market exposure. But returns are generally slower compared to the UAE’s larger urban centers, and the investment case depends largely on your goals and holding strategy.

Property values in Al Ain are forecast to rise by 3% to 4.5% through 2026, driven by steady end-user demand, limited speculative pressure, and a tight supply of family-sized villas. Districts such as Al Hili and Al Jimi are expected to perform well in terms of capital preservation, with modest appreciation over time. Knight Frank’s annual wealth report consistently highlights the UAE as a top destination for capital preservation among high-net-worth buyers.

Rental yields stay a key advantage here. Gross annual returns range between 6% and 8%, especially in villa communities and mid-market apartment zones. Tenants in Al Ain tend to sign longer leases, often 12 to 24 months, leading to reduced turnover and reliable occupancy. That’s an appealing factor for any income-focused landlord.

Still, you should weigh the market’s limitations carefully. Liquidity is lower than in Dubai or Abu Dhabi, and resale cycles can be slower. Capital appreciation tends to be gradual, and the market is highly dependent on public sector employment, which limits exposure to private-sector demand drivers. Bloomberg’s coverage of UAE real estate has noted this structural dependency as both a stabilizing force and a ceiling on upside.

Al Ain also lacks the global visibility and transactional scale seen in other emirates. For international investors or those seeking faster asset rotation, the market may feel conservative in both pace and volume.

All things considered, Al Ain is a viable market for investors who value low volatility, steady income, and affordable entry points. It won’t deliver rapid gains. But it offers consistent long-term value, particularly for those focused on stable residential portfolios. The Financial Times’ Middle East real estate coverage offers useful context on how secondary UAE markets are being evaluated by global capital. And if you’re comparing strategy across borders, Reuters Real Estate tracks the macro forces shaping property markets across the Gulf.

Other Market Forecasts & Overviews

Dubai Real Estate Market Overview & Forecast

Abu Dhabi Real Estate Market Overview & Forecast

Sharjah Real Estate Market Overview & Forecast

FAQ

Are property prices in Al Ain expected to rise in 2026?

Yes. Prices are forecast to increase by 3% to 4.5% over the next year.

Is Al Ain a good place to invest in real estate?

Yes, if you’re seeking stable rental income, affordable entry, and low market volatility.

Which areas are best for property investment in Al Ain?

Top investment zones include Al Hili, Al Jimi, Zakher, Al Mutaredh, and Al Yahar.

Is now a good time to buy property in Al Ain?

Yes, especially for long-term investors targeting income and capital preservation.