Artificial intelligence has dominated markets, media, and investor imagination for the past two years. From chipmakers hitting trillion-dollar valuations to startups raising capital at dizzying multiples, the AI narrative has become the go-to explanation for almost everything in financial markets. And to be fair, much of the hype is rooted in real technological change.

But not every investor is buying in.

As we move through 2026, a quieter trend is gaining traction — one that favors stable, cash-flow-rich companies over futuristic promises. From industrials and insurance to consumer staples and utilities, so-called “boring” sectors are experiencing a renaissance among serious capital allocators.

These are companies that don’t need perfect macro conditions or exponential user growth to perform. They’ve been around for decades, often through multiple economic cycles, and they’ve built reputations not on hype but on discipline and durability.

AI isn’t going away. But as valuations stretch and volatility creeps in, more investors are rotating out of speculative positions and reallocating into businesses with real earnings, clear dividend policies, and predictable returns. The shift isn’t loud. But it’s measurable.

And in a world of rising rates, sticky inflation, and geopolitical noise, boring is starting to look like the new smart.

Table of Contents

Why Investors Are Losing Interest in AI Stocks

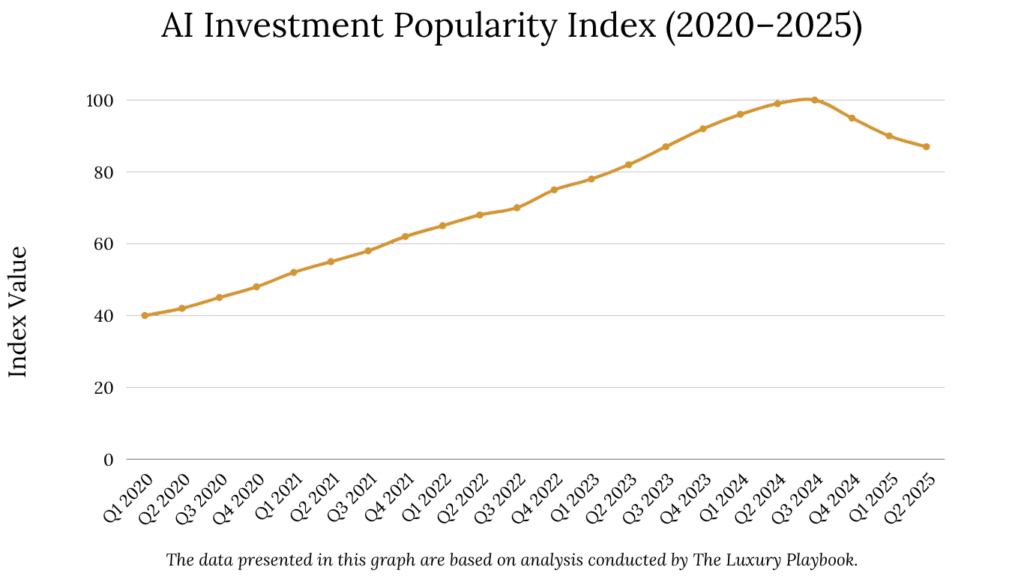

AI was the story of the year. From headlines about ChatGPT disrupting industries to soaring stock prices of chipmakers and software giants, artificial intelligence dominated investor conversations throughout 2023 and 2024. But stepping into mid-2026, a noticeable shift is underway. The AI narrative isn’t collapsing. It’s maturing. And for many investors, the shine is wearing off.

Over the past 18 months, AI-driven stocks posted explosive gains. Nvidia, for instance, surged by more than 240% in 2023 alone, fueled by demand for GPU chips. But valuations across the sector reached extremes, with some companies trading at 50x revenue multiples — a level that triggered concern even among seasoned bulls.

According to a recent report by FTI Consulting, “AI is undeniably transformative, but the capital flow into it outpaced actual revenue models. That gap is now being priced in.”

What followed was inevitable. A correction. In early 2026, tech-heavy indices began to slide. The Nasdaq lost 5% over a two-week span in Q1, while individual AI names fell harder. Hedge funds and institutional managers started pulling capital from overcrowded trades, reallocating into sectors with stronger fundamentals and lower volatility.

More telling than price action is what’s happening beneath the surface. Analysts at Morningstar noted that the equal-weighted S&P 500 index outperformed the cap-weighted version, signaling that smaller, non-tech companies are gaining ground while tech giants lose steam. Investors are no longer chasing the biggest story. They’re chasing consistent returns.

This shift is less about rejecting innovation and more about rebalancing. Just like a watch collector eventually stops chasing the latest limited-edition release and starts appreciating heritage pieces valued for craftsmanship and reliability, many investors are finding peace in what the market calls “boring” — companies with stable revenue, clear cash flows, and low drama.

And while AI stays a powerful long-term trend, the market is recalibrating expectations. As Vanguard’s Chief Economist Joseph Davis recently said, “AI will be a productivity tool, not a silver bullet. The real value might show up in traditional sectors that quietly absorb these tools and improve margins over time.”

What the Data Says About the Market Rotation

If you’ve been watching the market closely in 2026, you’ve probably noticed something subtle but important. The names powering the gains aren’t the same ones that dominated last year. While AI stocks still grab headlines, the real strength has shifted into sectors like energy, industrials, and even utilities — the kind of companies investors used to overlook in the heat of innovation cycles.

Look at the numbers. Between January and May 2026, the equal-weighted S&P 500 index outperformed the market-cap weighted version by over 2.5%, according to Morningstar. That means the average company in the index, rather than just the tech giants, is doing better.

Dig deeper and you’ll find that energy stocks are up roughly 8% year-to-date, while industrials have gained about 6.3%, compared to a modest 1.2% return for the tech sector.

In fact, six of the “Magnificent Seven” tech stocks — including Microsoft, Tesla, and Meta — have either stagnated or declined in early 2026. A report from MarketWatch noted that the broader market’s gains are coming from “companies with strong balance sheets, positive cash flow, and steady dividend history.” In other words, boring is working.

At the same time, bond yields are pushing past 5%, and that matters. Higher yields mean growth stocks, which rely on future earnings, are less attractive today. Traditional sectors, which generate strong earnings right now, become more appealing under these conditions. It’s a return to fundamentals — P/E ratios, margins, dividend yield — not just potential.

Institutional money is already moving. According to Bank of America’s fund manager survey, allocations to industrials and financials rose to a two-year high, while exposure to tech fell for the first time in 16 months. “The rotation is real,” the report said. “Investors want durability in a higher-for-longer rate environment.”

This isn’t a panic exit from tech. It’s a reallocation — a balancing act.

And just like someone diversifying a watch collection with a classic steel Datejust after buying flashy skeleton dials, investors are looking to anchor their portfolios with reliable, time-tested assets. If you’re thinking about how alternative assets fit into that picture, understanding how a wrap account works can give you a useful framework for managing a diversified strategy.

Why Traditional Companies Are Gaining Attention

As tech valuations cool off, investors are rediscovering something that used to be common sense. Steady profits, clean balance sheets, and predictable cash flows still matter.

Traditional companies — those operating in sectors like manufacturing, insurance, consumer staples, and industrial logistics — are back in favor.

What’s changed? Mostly the macro environment. In an era of elevated interest rates, stubborn inflation, and geopolitical uncertainty, investors are starting to prioritize resilience over speculation. These “boring” businesses may not promise exponential growth, but they offer something just as valuable. Reliability.

Take insurance companies, for example. Firms like Chubb and Travelers aren’t making AI breakthroughs, but they’re generating double-digit returns on equity, paying growing dividends, and benefiting from rising premium rates.

Or look at industrial giants like Caterpillar and Deere — companies tied to infrastructure and manufacturing trends. Their earnings may not double overnight, but they reflect real demand and tangible economic activity.

In a recent interview with Barron’s, Vanguard’s Joseph Davis put it plainly.

“As AI matures, the biggest gains may not come from the developers themselves, but from the businesses quietly using it to boost efficiency. Traditional sectors are where that productivity will show up first.”

That quote cuts to the heart of the trend. AI isn’t irrelevant. It’s becoming a tool, not a ticket. And the companies best positioned to benefit from that toolset are often the ones with the most operational discipline — logistics firms, supply chain players, banks, healthcare providers.

This shift also reflects a change in investor psychology. The emotional pull of “the next big thing” is giving way to a desire for long-term wealth preservation. Just like a seasoned watch collector eventually shifts from experimental modern pieces to timeless vintage models, investors are now looking for holdings that endure, not just excite.

And in markets like these, where earnings matter more than stories, those so-called “boring” companies are starting to look like the real stars.

Which Sectors Are Performing Well in 2026

So far in 2026, the best-performing sectors aren’t the ones making headlines. They’re the ones quietly delivering earnings, dividends, and long-term value. While AI and tech stocks have struggled under the weight of high expectations and interest rate sensitivity, sectors like energy, industrials, financials, and utilities are doing the heavy lifting.

Let’s break it down.

- Energy: After a shaky 2023 & 2024, the energy sector is making a comeback. Oil prices have stabilized around $85–$90 per barrel, and companies like ExxonMobil and Chevron are seeing strong free cash flows. Dividend yields remain attractive—often above 4%—and capital expenditure discipline is improving. The sector is up roughly 8% year-to-date, according to MarketWatch.

- Industrials: This category includes machinery, aerospace, and logistics firms that benefit from infrastructure spending and global trade normalization. Companies like Honeywell, UPS, and General Electric have reported solid earnings growth driven by both domestic and international demand. Year-to-date gains are hovering around 6.3%, outpacing most tech peers.

- Financials: Rising interest rates usually mean wider margins for banks and insurers—and 2025 is no exception. Regional banks are stabilizing, large banks are strengthening loan portfolios, and insurance companies are thriving in this yield environment. According to Bank of America’s latest sector review, financials are now the second-most overweight sector among institutional investors.

- Utilities and Consumer Staples: These “defensive” sectors are gaining traction as investors seek stability. Utilities offer predictable income, while consumer staples like food and hygiene brands maintain steady demand regardless of economic cycles. These sectors may not have big upside, but they offer reliable downside protection—especially valuable in volatile markets.

One of the more interesting trends this year is the return of dividend-focused investing. With bond yields pushing 5%, investors are demanding more from equities — and companies that pay reliable, growing dividends are winning attention. It’s no longer just about potential. It’s about payout.

How Inflation and Interest Rates Affect This Shift

To understand why boring companies are suddenly in fashion, you have to look at what’s happening with interest rates and inflation. These two macro forces are reshaping investor behavior in a big way, and they’re doing it fast.

Start with interest rates. After years of near-zero rates, central banks across the world — especially the U.S. Federal Reserve — have kept rates elevated to combat inflation. As of mid-2026, the U.S. benchmark rate sits around 5.25%, and many analysts, including those at Fidelity and Vanguard, now expect a “higher for longer” environment. That has serious consequences for equity markets.

When interest rates are high, borrowing becomes more expensive for companies. That directly affects growth stocks — especially those in the AI and tech space — because these businesses often rely on debt to fund expansion and don’t generate significant profits yet.

Suddenly, the promise of big returns five years from now isn’t as attractive when you can get 5% annually from a government bond today.

Inflation, although cooler than in 2022, stays persistent in key areas like housing, services, and wages. This erodes purchasing power and puts pressure on profit margins. In this environment, companies that can pass on costs, manage pricing, and maintain margins — think utilities, consumer staples, and energy — tend to outperform.

According to Barron’s, Vanguard’s Chief Economist Joseph Davis recently warned that bond yields could spike as high as 9% if inflation proves more stubborn than expected. If that happens, even more capital is likely to shift toward businesses with strong earnings visibility and dividend yield.

This is where boring companies shine. They don’t need a perfect macro backdrop to perform. Their products are often essential. Their costs are tightly managed. And many of them have decades of operational experience dealing with inflation cycles. This isn’t their first rodeo.

What Investors Like About Boring Stocks

- Consistent Cash Flow: Boring companies typically have reliable, predictable revenue streams. Utilities, insurance firms, and consumer goods companies serve essential needs, making their income less sensitive to economic cycles.

- Attractive Dividends: Many of these companies offer solid dividend yields that are especially appealing in a high-interest-rate environment. They often have long histories of not just paying, but steadily increasing dividends.

- Lower Volatility: These stocks usually exhibit less price fluctuation compared to high-growth or speculative sectors. This helps reduce overall portfolio risk during turbulent market conditions.

- High Earnings Visibility: Traditional businesses often operate with stable cost structures and demand, making it easier for analysts and investors to forecast future earnings and performance.

- Resilience Across Market Cycles: Many boring companies have demonstrated long-term resilience, performing well during recessions, inflationary periods, and rate hikes.

- Strong Balance Sheets: These firms often carry less debt and maintain healthy cash positions, giving them flexibility and downside protection.

- Sector Rotation Support: As capital rotates out of overvalued growth sectors, these undervalued or overlooked stocks benefit from renewed institutional attention and capital inflows.

What Risks Come With Investing in Boring Companies

Boring companies offer stability and resilience, but they come with their own set of limitations — especially when compared to high-growth, innovation-driven sectors. Understanding these risks is key to building a balanced portfolio.

One of the most obvious drawbacks is limited upside potential. These companies tend to operate in mature industries — think utilities, telecom, and consumer staples — where revenue growth is slow and often capped by regulation or market saturation. They might generate consistent profits, but they rarely produce the kind of explosive returns seen in tech or biotech.

Another risk is underperformance during bull markets, particularly those led by innovation. When capital floods into growth stocks and investor sentiment turns optimistic, boring stocks often lag behind. They offer security, but that can come at the cost of missed opportunities.

Valuation can also become a problem. In uncertain markets, many investors crowd into defensive sectors at once, pushing prices higher. This valuation compression means you might be buying low-growth stocks at historically high multiples — leaving less room for error and future returns.

There’s also the challenge of inflation and margin pressure. While these businesses are steady, not all of them have the pricing power to pass increased costs on to consumers. That’s especially true in industries like consumer staples or manufacturing, where profit margins are thin.

And while dividends are attractive, depending too heavily on income carries real risk. In a downturn, even the most reliable companies may be forced to cut or freeze dividend payments. Investors relying on that income stream could find themselves exposed. If you’re thinking about how to structure that income more efficiently, opening an IRA is worth understanding as part of your broader plan.

Focusing too much on defensive names can also leave your portfolio underexposed to innovation and long-term structural growth trends. If AI, green energy, or automation drives the next decade of returns, investors heavily weighted toward traditional businesses may miss the upside entirely. The same logic applies when you consider how macro shifts — like the ones explored in our look at silver’s historic crash — can blindside even the most conservative strategies.

Boring companies are useful. But like any strategy, leaning too far in one direction comes with consequences.