Emerging markets have stormed back into investor consciousness in 2026 after years of underperformance that left many questioning whether the asset class deserved a place in your portfolio at all.

A weaker U.S. dollar, global rate-cut expectations, and strong fund inflows have pushed EM equities, currencies, and debt sharply higher. Reuters and EPFR data show capital flowing into these markets at rates not seen since the pre-pandemic era. If you were watching from the sidelines, you likely missed the opening move.

The performance gap that widened steadily in favor of developed markets through much of the 2010s and early 2020s has suddenly reversed. And for investors paying attention, the timing matters enormously.

As Reuters commentary notes: “Emerging market assets have been unexpected winners this year.”

Table of Contents

Key Takeaways

Navigate between overview and detailed analysisKey Takeaways

- Emerging markets staged a comeback in 2025, with equities, bonds, and currencies all rallying after years of underperformance.

- Weaker U.S. dollar and global rate cuts created the liquidity backdrop fueling flows into EM assets.

- Tech-heavy Asian markets (Taiwan, Korea, Vietnam) led equity gains, while Brazil and Mexico benefited from currency strength and earlier rate hikes.

- This rally looks different from past cycles thanks to proactive EM central bank policies, which built resilience compared to earlier boom-bust periods.

- Despite optimism, risks remain: capital flow volatility, commodity exposure divergences, and structural challenges in China.

The Five Ws Analysis

- Who:

- Global investors ranging from institutional funds to retail ETF buyers, with capital flowing into EM equities, bonds, and currencies.

- What:

- A broad rally across EM assets, with the MSCI EM Index up 18–24% YTD, bond ETFs like EMB returning 10.8%, and EM currencies up 12.7% versus the dollar.

- When:

- Acceleration began in early 2025, gaining momentum by late summer and early autumn as Fed cuts and dollar weakness took hold.

- Where:

- Key performers include Vietnam (+31–55%), Brazil (+21%), and India (positive but valuation-sensitive); Asia and Latin America lead, with mixed signals in Africa.

- Why:

- A combination of weaker dollar, global monetary easing, commodity demand, and EM tech sector strength revived flows—while proactive EM central bank policies enhanced credibility.

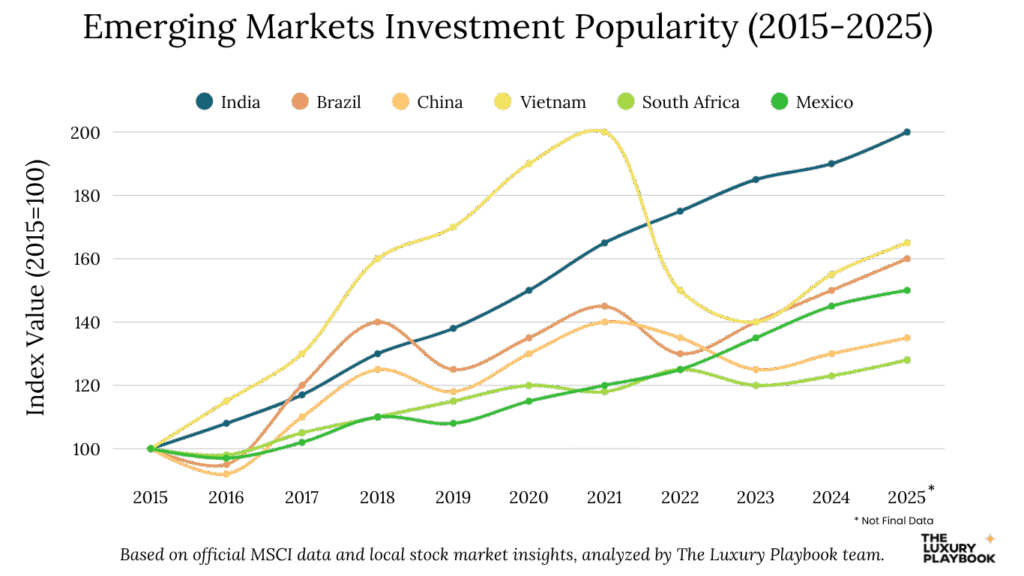

Emerging Market Performance in 2026

The equity rally has been broad but uneven across regions. MSCI data shows the MSCI EM Index delivering one-year returns in the 18% to 24% range depending on measurement dates through late September and early October. The standout gains have been concentrated in the index’s tech-heavy Asian components, so where you were positioned made all the difference.

Vietnam has been a breakout performer, with the VN-Index climbing between 31% and 55% depending on which index and measurement period you look at, as Reuters and countryeconomy.com report. Brazil’s Ibovespa rose roughly 21% year-to-date in local currency terms. India’s Nifty 50 posted positive but choppier returns, weighed down by valuation concerns that kept the more cautious money on edge.

Bond markets joined the equity rally. Yahoo Finance data shows the EMB ETF, which tracks dollar-denominated sovereigns using the J.P. Morgan EMBI as a proxy, gaining about 10.8% year-to-date through September 30. Local currency debt posted more modest gains, with one Curvo-tracked variant showing roughly 0.9% returns. That said, wide country-level dispersion means aggregate figures mask very different stories playing out market by market.

Currency appreciation has amplified returns for dollar-based investors in a meaningful way. The Financial Times reports EM foreign exchange as a basket strengthened 12.7% against the dollar in 2026 year-to-date. The Brazilian real and Mexican peso benefited from carry advantages and earlier rate hiking cycles that built in cushions before global easing began. If your exposure was unhedged, that currency tailwind added a layer of return you didn’t even have to engineer.

Asian markets with heavy technology exposure, think Taiwan and Korea components within the MSCI EM index, led the charge. Latin America delivered strong equity performance in Brazil alongside currency strength in both the real and the peso. South Africa presents a more mixed picture, though Reuters notes improving macro signals with PMI readings above 50 and load-shedding relief providing economic tailwinds that give the bulls something to point to.

Context matters here. East Capital data shows that in the first half of 2026, emerging markets outperformed the S&P 500 for the first time since 2017. But that gap narrowed later in the year as U.S. AI-led technology gains re-accelerated. It’s a reminder that EM outperformance can be fragile when developed market momentum kicks back in. You can read more about that developed market dynamic in our breakdown of whether the S&P 500’s march to 7,000 is sustainable.

Drivers Behind the Emerging Market Rally

Global rate cuts and renewed liquidity form the foundation of everything you’re seeing in EM right now. Fed rate-cut expectations throughout the year, followed by actual cuts delivered in the second half, supported risk appetite and triggered significant fund flows into EM allocations. When the cost of capital falls in developed markets, money goes looking for yield elsewhere.

EPFR and Reuters data show robust bond and equity inflows into EM investment vehicles during late August through October, suggesting institutional money has followed retail interest.

As the dollar drifted lower from earlier peaks, EM foreign exchange strengthened and unhedged EM equity returns benefited from favorable currency translation. Reuters tracking confirms this pattern clearly. The catch is that it also illustrates how EM performance stays partially dependent on developed market monetary policy rather than purely domestic economic strength.

Commodity dynamics have added another layer, though the picture is mixed. Copper and oil volatility has created clear winners and losers across the EM universe, and knowing which side of that trade your target markets sit on is essential.

Structural grid and electrification demand underpins copper pricing despite volatility, while oil trading near the mid-$60s with ample supply creates supportive conditions for importers while challenging exporters. These divergent commodity impacts mean resource-rich economies face very different dynamics than manufacturing-focused ones, and your regional allocation decisions need to account for that split.

Technology leadership and demographic advantages have concentrated in specific markets. MSCI data shows that EM index performance is heavily influenced by semiconductor and platform companies including TSMC, Tencent, Samsung, and SK Hynix, alongside the massive consumer bases in India and Southeast Asia. Elite investors protecting and growing capital in volatile markets have increasingly leaned into this technology concentration as a deliberate strategy rather than an accidental outcome.

This concentration means EM equity performance increasingly depends on technology sector health rather than broad-based economic development across those countries. That’s worth understanding before you size a position.

Are Emerging Markets Finally Delivering on Their Promise?

The history of EM boom-bust cycles casts a long shadow over current enthusiasm. Reuters notes that EM cycles have historically hinged on dollar cycles and global liquidity conditions, which means the 2026 rally coincides with familiar catalysts of dollar softening and monetary easing bias rather than a fundamental transformation of these economies. You’ve seen this pattern before.

What potentially distinguishes this rally from previous false dawns is timing and preparation. Financial Times analysis shows that earlier and more forceful rate hikes by many EM central banks during 2021 through 2023 created policy space to ease earlier in 2026. That move supported both bond markets and economic growth while allowing currencies to hold up better than in prior easing cycles.

This proactive monetary policy marks a real departure from past patterns where EM central banks lagged developed market policy shifts and paid for it with currency crises and capital flight. Whether it holds is the question you need to keep asking.

Still, IMF warnings highlight capital flow volatility and reform execution risks. Particular concern centers on China’s structural economic challenges, which ripple through the entire EM complex in ways that are difficult to hedge around.

Where Investors Are Placing Their Bets

How capital flows into these markets varies by investor type and risk tolerance. If you’re an equity investor, ETFs are the most practical entry point, giving you diversified exposure without requiring direct market access or complex custody arrangements across multiple jurisdictions.

ETF Express reports that global exchange-traded products saw $171 billion in inflows during August alone, the second-highest monthly figure of 2026, with EM-focused funds capturing renewed interest as strong performance attracted fresh attention. That flow data tells you where institutional money has been moving.

Bond investors are engaging through multiple channels. Dollar-denominated sovereign debt, tracked by vehicles like the EMB ETF, has attracted flows seeking yield pickup over U.S. Treasuries without taking on currency risk. Yahoo Finance data shows this strategy delivering approximately 10.8% year-to-date returns through September 30. For context on how alternative assets have stacked up alongside this, it’s worth checking out which alternative assets delivered the best returns this year.

More sophisticated investors are selectively adding local currency debt in countries where central bank easing cycles look credible. You accept currency risk in that trade, but the higher nominal yields compensate for it if you’ve done your homework on the macro backdrop.

Private equity and venture capital offer longer-horizon plays gaining serious traction in select markets. India’s technology ecosystem and Southeast Asian consumer markets have attracted substantial private capital from investors seeking growth opportunities that simply aren’t available in public markets at reasonable valuations.

These investments typically involve multi-year holding periods and far less liquidity than public market alternatives. But if you have the patience and the right manager relationships, the potential for outsized returns in successfully scaling companies makes the illiquidity premium worth considering.

Direct investment by multinational corporations keeps flowing into emerging markets for manufacturing and services operations. Vietnam’s manufacturing sector and India’s technology services industry show how corporate capital deployment differs from portfolio investment. The focus is on operational build-out rather than financial return optimization, and that distinction shapes the risk and return profile entirely. For investors looking at how regional equity stories like this one connect to broader market themes, our analysis of Southern Europe stocks leading the market rally offers a useful parallel on how regional momentum trades develop and eventually fade.