A dramatic reversal is sweeping through global energy policy. Governments worldwide are abandoning renewable-first strategies and doubling down on fossil fuel production at a pace few saw coming.

From the United States expanding coal mining to China accelerating coal-fired power plants and the Middle East ramping up gas exports, this is one of the most significant energy policy pivots in decades. And it’s happening all at once.

If you’re active across energy markets, commodities trading, or ESG portfolios, this government-led fossil fuel expansion puts both opportunities and genuinely complex challenges on your table. The decisions you make now could reshape your energy exposure for years to come.

Fossil-fuel allocation decisions still sit at the heart of institutional research. S&P Global publishes deep coverage of energy supply, demand, and capex cycles, and Goldman Sachs commodities research tracks how production discipline shapes the longer-run price floor.

The macro view sharpens the case. The IMF publishes regular fiscal-monitor research on oil-exporting economies, and Reuters covers the day-to-day production data that drives the actual share prices.

Key Takeaways

Navigate between overview and detailed analysisKey Takeaways

- Governments are prioritizing energy security and economic growth over climate commitments, marking a dramatic reversal in global policy.

- Fossil fuel expansion, coal, oil, and gas, is being directly supported through subsidies, favorable regulations, and infrastructure investment.

- For investors, this creates a paradox: short-term opportunities in oil & gas profitability versus long-term risks of oversupply and policy reversals.

- Renewable energy faces pressure from rising interest rates and capital outflows, while fossil fuels regain momentum as “reliable” assets.

- The global energy mix is entering a period of greater volatility, where policy shifts, geopolitics, and market cycles will heavily shape returns.

The Five Ws Analysis

- Who:

- National governments (U.S., China, Middle East) and major oil & gas corporations driving expansion.

- What:

- A global policy shift away from renewable-first strategies toward renewed fossil fuel investment.

- When:

- The pivot accelerated in 2025, fueled by energy security concerns and political decisions.

- Where:

- Key centers include U.S. coal/oil, China’s coal-fired plants, and Middle Eastern gas production.

- Why:

- Governments see fossil fuels as essential for reliable growth, geopolitical leverage, and domestic stability, even at the cost of climate goals.

The Global Policy Shift Toward Fossil Fuel Growth

The Trump administration has launched the most aggressive fossil fuel expansion program in recent memory. Executive orders to expand coal burning and mining are already signed, and development across oil and natural gas sectors is being actively promoted in a country that already leads the world in production.

The “Unleashing American Energy” executive order specifically encourages energy exploration and production on federal lands and waters, backed by $80 billion in fossil fuel industry handouts over the next decade, including $14.2 billion worth of enhanced carbon capture subsidies.

China’s policy reversal is perhaps the most striking of all. Despite previous climate commitments, Beijing is accelerating coal-fired power plant development at speed. The driver is simple: electricity market shortages have forced pragmatic energy security decisions over environmental goals.

Chinese coal production projections have climbed sharply. The anticipated decline that analysts once forecast is now expected to arrive later and from a much higher starting point than anyone predicted back in 2023.

Middle Eastern nations are positioning themselves as energy export powerhouses. The region is on track to become the world’s second-largest gas producing region in 2026, with production up 15% since 2020. Qatar alone plans to expand LNG capacity from 77 million tonnes annually to 142 million tonnes by 2030, and regional gas production is projected to rise 30% by 2030, adding another 20 billion cubic feet per day. The Financial Times has tracked this Gulf energy buildout closely, and the numbers are hard to ignore.

The political motivations behind all of this come down to energy security and economic competitiveness winning out over climate goals. National governments are throwing their weight behind fossil fuels through public infrastructure financing, subsidies, discounted royalties, and favorable tax regimes.

Geopolitical tensions and supply chain disruptions have only reinforced the push for domestic energy production. For most governments right now, economic growth and energy independence come first.

How Fossil Fuel Expansion Impacts Energy Markets

Oil pricing tells the story of a market awash in supply. Bloomberg’s energy desk has flagged the same trend that EIA forecasts confirm, with Brent crude averaging $74 per barrel in 2026, down 8% from 2024, and a further slide to $66 per barrel projected for the year after. HSBC projects a significant oil surplus of 1.7 million barrels daily from Q4 2026, growing to 2.4 million barrels daily the following year, creating real downward price pressure despite strong production growth.

Global production increases are outpacing demand growth, with oil production expected to rise 1.8 million barrels daily in 2025 and 1.5 million barrels daily in 2026.

Demand growth is slowing too, dropping to 680,000 barrels daily in 2026 from 860,000 barrels daily in 2024, largely due to a weaker economic outlook. That imbalance points to inventory builds averaging more than 2 million barrels daily from Q3 2026 through Q1 2027.

Natural gas tells a different story. Prices are expected to climb from an average of $4.10 to $4.80, reflecting stronger demand growth relative to oil. Middle East crude production is expected to hold steady around 26.6 million barrels daily, while U.S. production hit records at 13.2 million barrels daily in 2024 and is projected to reach 13.5 million barrels daily in 2026.

Are Fossil Fuel Stocks Still a Smart Buy?

The energy sector underperformed in 2024, but analysts broadly expect oil prices to stay in a $70 to $90 range that keeps corporate profitability intact. The sector has matured into a cash-generating machine. Many companies are maintaining strong positive cash flow and returning capital through dividends and share buybacks rather than chasing aggressive expansion.

If you’re looking at the difference between investing and speculating in markets, energy majors right now sit closer to the investing end of that spectrum.

Investment flows tell a more complicated story. The Energy Select Sector SPDR has seen roughly $7 billion in outflows year-to-date through 2026, making it the largest energy market ETF despite being heavily sold. Meanwhile, the Utilities Select SPDR has pulled in close to $3 billion in inflows, suggesting investors would rather have regulated utility exposure than the volatility of oil and gas producers.

The value versus growth positioning favors energy stocks in environments where commodity prices remain stable while production costs stay controlled.

That said, institutional investors are staying cautious about adding exposure. Most are waiting for clearer price trends before making significant allocation changes.

Winners and Losers on the Stock Market

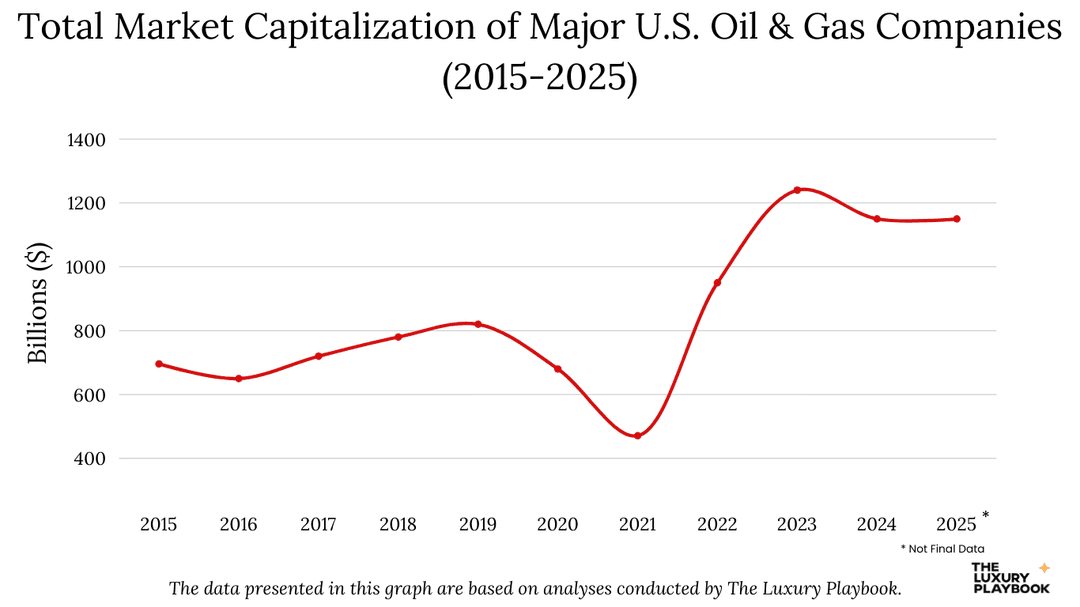

Oil majors are showing resilient fundamentals even when stock performance has been mixed. ExxonMobil holds a market cap around $480 billion with a 3.70% dividend yield. Chevron trades in the $251 to $310 billion market cap range with a 3.90% dividend yield.

These are not speculation plays. They’re income machines.

International majors like Shell and BP offer higher yields at 4.10% and 4.80% respectively, which reflects their clear priority of shareholder returns over growth investment. If yield is what you’re after, the European majors deserve a close look.

Service companies are showing divergent paths. Halliburton is outperforming relative to Schlumberger, which has seen more pronounced bearish trends. Both face mixed signals from the global fossil fuel expansion, which should theoretically increase demand for their drilling and completion services.

But the market isn’t pricing that in cleanly yet.

Renewable energy stocks have had a rough stretch. The global sustainable fund universe endured its worst quarter on record in Q1 2026, with net outflows of $8.6 billion. ESG funds have faced relative underperformance since 2022, partly because they tend to carry higher proportions of technology stocks while being underweight in fossil fuels and materials. Asking the right questions before any allocation matters more than ever in this environment.

Clean energy stocks face another headwind too. Rising interest rates punish future cash flows from capital-intensive renewable projects, and that pressure is not going away quickly.

Investor Flows and Market Sentiment

Hedge fund positioning has shifted fast. Equity-focused hedge funds have been mostly short oil stocks since October 2024, reversing bets that dominated the trade since 2021. These sophisticated players are winding back shorts on solar stocks while piling into bearish positions on oil equities.

The read they seem to be making is that current fossil fuel expansion could create oversupply conditions severe enough to hurt equity values even if production volumes rise. Reuters energy coverage has documented this positioning shift in detail.

Retail flows look different. U.S. ETF flows crossed $500 billion in June 2026, with Vanguard ETFs accounting for 37% of net flows, a reliable proxy for where retail money is moving. The energy sector showed a striking divergence, finishing as the top weekly performer while simultaneously recording net outflows of $104 million.

Retail investors are watching energy win but still pulling money out. That kind of disconnect is worth paying attention to. Understanding how brokers and market makers operate can help you read these flow signals more accurately.

ESG fund challenges reflect a broader investor uncertainty about where sustainability strategies go from here.

Despite record outflows, global ESG fund assets held steady at $3.16 trillion as of March 2026. But European sustainable funds saw net outflows for the first time since at least 2018, driven by geopolitical tensions and the Trump administration’s active rollback of climate policies. Forbes Finance Council contributors have noted that this may mark a structural inflection point for ESG allocation, not just a temporary pullback.

FAQ

Why are governments increasing fossil fuel output despite climate goals?

Energy security concerns and economic competitiveness have shifted political priorities away from climate commitments toward immediate economic growth.

Is oil and gas still a safe investment in 2025?

Oil and gas investments face mixed prospects. While government expansion policies support production growth, EIA forecasts show Brent crude declining from current levels to $66 per barrel by 2026 due to supply abundance.

Which sectors benefit most from fossil fuel expansion?

Oil service companies like Halliburton and Schlumberger should benefit from increased drilling activity, though performance has been mixed. Oil majors with strong balance sheets and dividend policies may outperform, particularly those with low-cost production assets.

We last reviewed this analysis in May 2026.

![]()

Alex Tzoulis

Alex Tzoulis is Co-Owner and Markets Analyst at The Luxury Playbook, specializing in equities, crypto, forex, and global financial markets. His work focuses on analyzing macroeconomic trends, geopolitical developments, and monetary policy, translating them into actionable insights across both traditional and digital asset classes. He leads the platform's financial market coverage, providing structured analysis across stock market investing, trading strategies, and cryptocurrency markets. His expertise strengthens the publication's authority in financial markets and capital allocation, bridging traditional finance with emerging digital investment ecosystems.