The formula seems almost too simple. Take a luxury brand people already trust, pair it with an artist whose name carries real weight, and suddenly you’ve created something worth far more than the sum of its parts.

This alchemy has quietly become one of the most reliable ways to generate value in contemporary art, especially as traditional gallery systems struggle to provide the transparency that modern collectors demand.

What makes this shift genuinely interesting is how collaborations gained strength precisely when traditional art markets weakened, with global art sales falling 12% in 2024 while high-end auction lots above $10 million slid 39%.

When the top of the market struggles but your segment expands its audience and transaction volume, you’re watching genuine structural change. Not a cyclical fashion moment. Something deeper.

Table of Contents

Key Takeaways

Navigate between overview and detailed analysis- Brand–artist collaborations have become a structural growth segment just as the traditional art market softened, with global sales down 12% in 2024 and $10M+ lots falling 39%, showing demand is shifting rather than cycling.

- Limited editions now combine numbered runs, certificates of authenticity, and NFC/blockchain passports (e.g., Verisart, Aura), removing authentication friction and supporting stronger resale confidence.

- Secondary-market data shows a brand premium: collaboration portfolios achieve roughly 3.4× comparable non-branded street-art results, with examples like Supreme × Damien Hirst decks hammering full archives at around $800k.

- Liquidity is unusually high for an alternative asset—about 72.6% auction sell-through in H1 2025 and roughly 75% resale within 90 days on authenticated luxury platforms, mirroring fine-art norms with faster turnover.

- Prints and multiples, where most collaborations exist, act as low-beta art: $72.8M in modern prints in 2024 with roughly 35% lower volatility than evening sales. A growing online art market, projected from $11B in 2024 to nearly $19B by 2033, is expanding accessibility and collector participation.

- Who:

- Luxury brands such as Louis Vuitton, BMW, and Dom Pérignon; artists like Murakami, Hirst, Basquiat, Mehretu, and KAWS; and investors seeking authenticated, liquid cultural assets.

- What:

- Investment-grade brand–artist collaborations—limited editions that merge fashion credibility with art-market structure, backed by robust provenance and clear pricing.

- When:

- Momentum accelerated between 2024 and 2025, exactly as traditional high-end auction segments weakened and digital authentication became mainstream.

- Where:

- Global auction houses including Sotheby’s, Christie’s, and Phillips, as well as authenticated online platforms and blockchain registries that enhance transparency and trust.

- Why:

- Scarcity, brand credibility, and instant authentication create durable premiums and faster resale cycles, offering lower volatility and better timing for cultural investment strategies.

How Limited Editions Affect Resale Prices

The way limited editions create and sustain value has evolved well beyond just stamping numbers on prints and hoping scarcity does the heavy lifting. Modern collaboration editions combine numbered runs with certificates of authenticity and increasingly sophisticated technology that links physical works to tamper-proof digital records.

NFC chips and blockchain certificates through platforms like Verisart and Aura Blockchain Consortium let buyers verify authenticity with their phones rather than relying on expert opinions that might be wrong or conflicted.

This addresses one of the biggest fears preventing newcomers from buying art: getting stuck with something fake or impossible to authenticate when it’s time to sell.

The timed drop model borrowed from streetwear has transformed how editions establish their initial pricing. Tight release windows concentrate demand and create clearing prices that often become effective floors for secondary trading.

Brands routinely pair these drops with digital passports using NFC or QR codes, reinforcing confidence that what you’re buying will be recognizable as authentic when you eventually sell. The difference between hoping something is real and being able to prove it instantly matters enormously for resale value. And limited edition prints built on that kind of provenance have a track record of delivering liquidity that purely speculative art rarely matches.

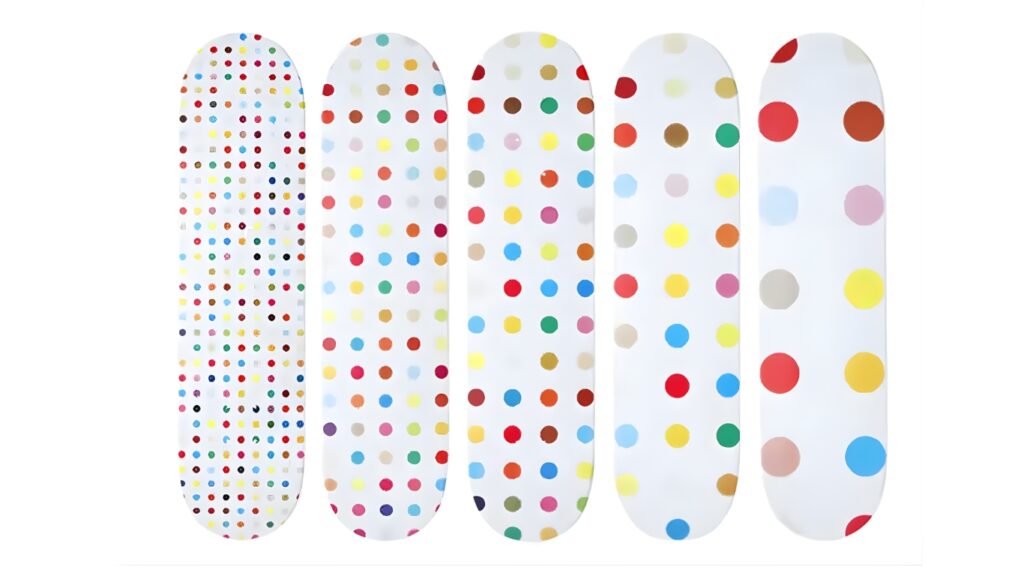

Supreme’s collaboration with Damien Hirst on Spin skateboard decks from 2009 shows exactly how this works in practice. Limited to 200 numbered pieces, these decks routinely hammer above estimates at major auction houses.

A complete set at Christie’s realized $15,000 against an estimate of $4,000 to $6,000, while Sotheby’s keeps placing Hirst and Supreme sets with multi-thousand dollar estimates that clear reliably.

This isn’t just about scarcity. It’s about how the combination of limited numbers, a blue-chip artist name, and cultural brand recognition creates demand that sustains pricing well above what similar unbranded prints ever achieve.

Secondary Market Performance of Luxury Collaboration Artworks

The premium that collaboration objects command relative to non-branded works can reach multiples rather than modest percentage uplifts. When Sotheby’s sold the complete archive of 248 Supreme skateboard decks in 2019 for roughly $800,000, it hit a price level rarely reached by non-branded street art prints regardless of quality or artist recognition.

Research from our analysts suggests collaboration pieces now command roughly 3.4 times what comparable non-branded street art portfolios achieve at auction, quantifying the brand premium in ways that make clear this represents measurable economic value rather than temporary hype.

Liquidity metrics reveal another dimension of collaboration strength that matters enormously if you’re thinking about these as investments rather than just collectibles. Across fine art auctions, sell-through in the first half of 2026 averaged roughly 72.6%, signaling steady absorption for the right pieces even in a softer overall market.

On the luxury side, authenticated pieces on The RealReal sell within 90 days about 75% of the time. Our analysts track what they call the Collab Liquidity Ratio, comparing resale turnover of collaboration works against fine art sell-through, which comes out at roughly 1.03.

That near parity means branded collaborations move almost as quickly as fashion items while commanding art-level pricing. That gives you something rare in alternative assets: genuine liquidity combined with real appreciation potential.

The prints and multiples market, where many collaborations naturally live, has shown remarkable resilience compared to headline evening sales of unique works. Modern prints totaled $72.8 million in 2024, outpacing Contemporary and Old Masters prints with volatility about 35% lower than those headline sales. Research suggests limited edition collaborations operate as low-beta art assets within collector portfolios, giving you exposure to contemporary art appreciation without the wild swings that make unique works difficult to hold with confidence during market stress. If you want a sharper look at how advisors approach this, the AVAA art advisory firm review covers how professional guidance shapes these decisions.

Best Luxury Collaborations Between Artists and Brands

Comprehensive market analysis of premium artist-brand partnerships including Louis Vuitton x Murakami (a search surge of over 1,100%), Supreme x Damien Hirst (now $15K at Christie’s), Dom Pérignon x Basquiat, Jeff Koons x NASA, BMW Art Cars, and more with collectibility insights and investment performance metrics.

| Brand / Project | Artist(s) | Year / Period | Market / Collectibility Insight |

|---|---|---|---|

| Louis Vuitton x Takashi Murakami | Takashi Murakami | 2003 (revived 2025) | Searches surged +1,119% YoY on resale platforms; now viewed as investment-grade collectibles; condition and provenance drive premiums |

| Supreme x Damien Hirst | Damien Hirst | ~2008 | Originally $3K–$5K, now reaching $15K at Christie’s; enduring demand from both streetwear and art collectors |

| Dom Pérignon x Jean-Michel Basquiat | Jean-Michel Basquiat | 2024 | Transformed branded Champagne into fine art collectibles; stratified tiers appeal to both entry-level and museum-grade collectors |

| Jeff Koons x NASA Intuitive Machines | Jeff Koons | 2024 | Combines space heritage + NFTs; built-in scarcity (lunar vs terrestrial editions); positioned for long-term cultural and collector relevance |

| BMW Art Car Series Julie Mehretu Edition | Julie Mehretu | 2025 | Represents institutional collaboration longevity; global museum exposure enhances artist visibility and long-term value |

| NOT A HOTEL x KAWS | KAWS | 2025 | Blends art, architecture, and experience; redefines collectibility through access and immersion rather than ownership |

| LEGO x Robert Indiana | Robert Indiana | 2025 | Democratizes fine art ownership; balances mass accessibility with limited licensing to maintain scarcity and long-term brand equity |

Key Market Trends

- Resale Market Explosion: Louis Vuitton x Murakami collaboration saw +1,119% YoY surge in search volume on resale platforms, establishing artist collaborations as legitimate investment vehicles

- Price Appreciation: Supreme x Damien Hirst pieces appreciated from original $3K-$5K retail to $15K at Christie’s auctions, demonstrating crossover appeal between streetwear and fine art markets

- New Collectible Categories: Dom Pérignon x Basquiat transformed branded Champagne packaging into fine art collectibles with stratified price tiers for different collector segments

- Scarcity Innovation: Jeff Koons x NASA project introduced lunar vs terrestrial edition scarcity combined with NFTs, creating new frameworks for limited-edition value

- Experience-Based Collectibility: NOT A HOTEL x KAWS redefined art collaboration through immersive access and architectural integration rather than traditional ownership models

How Investors Build A Collaboration Focused Collection With Lower Risk

Building a collection focused on collaborations with genuine investment potential rather than just fashionable objects requires systematic thinking about what actually drives durable value. Brand pedigree matters enormously because luxury brands have reputations to protect, and that naturally aligns their interests with yours as a collector who wants value maintained over time.

A collaboration with Louis Vuitton or BMW carries different weight than one with a brand that might not exist in ten years. Not because of snobbery, but because established luxury brands think in decades rather than quarters when building partnerships. Artist trajectory separates collaborations likely to appreciate from those that will fade once hype cycles end, and the key question is whether the artist’s broader market supports the collaboration or whether the collaboration is their only real source of demand.

Documented edition size, certificates of authenticity, and NFC or blockchain passports from providers like Aura and Verisart mitigate fraud risk while maximizing future liquidity. Being able to authenticate a piece instantly rather than requiring expensive expert opinions that might disagree makes the difference between something you can sell confidently and something that sits because buyers fear getting stuck with unresolved authentication questions.

Our analysts emphasize first-series status and condition as factors that create meaningful value differentials within collaborations, with initial releases typically commanding premiums over subsequent editions if brands repeat successful partnerships.

Portfolio tactics that reduce risk while maintaining upside involve blending headline capsules that everybody recognizes with under-the-radar editions that haven’t yet achieved full market recognition. The Louis Vuitton and Murakami bags or BMW Art Car ephemera provide liquidity and name recognition, while lesser-known but high-quality collaborations offer appreciation potential before broader markets discover them.

Targeting set-completion opportunities, like collecting full runs of Supreme artist skateboard decks, historically supports price floors because collectors building complete sets will pay premiums for the final pieces they need. Our analysts’ research shows this completionist behavior creates bid support roughly 20% to 40% above individual piece values for the items that finish sets.

Timing exits around anniversaries, museum shows, and major brand campaigns maximizes the prices you realize by selling into moments when attention and demand peak temporarily. A Murakami collaboration piece sells for more during a major retrospective than during quiet periods when nobody’s thinking about his work, not because the object changed but because buyer attention concentrates around cultural moments.

Private sale channels have become increasingly important as auctions shifted toward mid-price material, which means successful investors use both strategically rather than automatically defaulting to auction houses. The liquidity reality is that authenticated luxury collaborations show about 75% selling within 90 days on verified platforms, giving you genuine confidence about your ability to exit positions when needed rather than just hoping eventual buyers appear.

Red flags suggesting you should avoid a particular collaboration include over-issued runs where scarcity becomes meaningless, weak storytelling that doesn’t connect brand and artist in compelling ways, and license-only merchandise without genuine artist involvement that feels like corporate appropriation rather than creative partnership.

Collaborations that succeed as investments almost always involve real creative collaboration rather than just artists lending their names to existing product lines with minimal input. The difference between Murakami genuinely reimagining Louis Vuitton’s monogram and an artist simply signing off on someone else’s design matters enormously for long-term cultural relevance and the value that follows from it. The contemporary artists currently rewriting auction records share that same quality of genuine creative authorship, which is exactly what sustains collector interest across market cycles.

The market backdrop through 2024 and into 2026 actually creates favorable conditions for collaboration investment despite overall art market weakness. Even with $57.5 billion in 2024 sales down 12% year over year, transaction counts increased and new buyer percentages grew.

In 2024, 44% of dealer buyers were entirely new to the market while first-time buyers accounted for 38% of total sales. Those are prime conditions for collaborations offering recognizable narratives, transparent authentication, and approachable price points that lower barriers for newer collectors who feel uncomfortable navigating traditional gallery systems.

The online art market reached $11 billion in 2024 with projections pointing toward roughly $19 billion by 2033, representing compound annual growth of around 6.2%. And yet over 80% of collectors still finalize purchases offline, which tells you that physical authentication and branded provenance stay decisive regardless of how discovery happens digitally.