After more than 15 years of private equity dominance, institutional investors are making a dramatic shift. University endowments, pension funds, family offices, and sovereign wealth funds are cutting their private equity allocations and moving capital back into hedge funds.

This is a complete reversal of the trend that defined institutional investing since the financial crisis, when private equity became the default choice for sophisticated investors seeking higher returns than public markets could offer.

The timing is no accident. Private equity’s core mechanics have stopped working as interest rates rose and exit markets froze. Meanwhile, hedge funds have quietly delivered strong performance, cleaned up their operations, and proven the real value of liquidity in uncertain markets.

Table of Contents

Key Takeaways & The 5Ws

- Institutional capital is rotating away from private equity and back into hedge funds after more than 15 years of PE dominance, driven by broken exit mechanics and prolonged holding periods.

- Private equity is facing an exit logjam: IPOs have collapsed, debt remains expensive, holding periods have stretched past six years, and a $3T+ backlog of unsold portfolio companies is weighing on realized returns.

- LPs are feeling the squeeze through negative net cash flows, valuation write-downs, and secondary sales at discounts to NAV, while still paying near “2%” management fees on committed capital.

- Hedge funds have looked comparatively attractive, delivering mid-single to mid-teens annual returns in 2023–2025 with more frequent liquidity, better transparency, compressed fees, and strategy dispersion that diversifies equity risk again.

- For large allocators, liquidity, flexibility, and daily-marked performance now compete strongly against illiquid PE vehicles whose paper values depend on exits that may not arrive on time.

- Who is reallocating?

- Large institutional allocators—university endowments, pension funds, sovereign wealth funds, and sizable family offices—reducing maxed-out private equity exposure and increasing allocations to hedge funds and other liquid alternatives.

- What is changing?

- A structural repositioning of alternatives: dialing down illiquid buyout exposure with clogged exits and high fees, and adding more liquid, actively managed hedge fund strategies that can adapt quickly and mark to market daily.

- When did the shift accelerate?

- Post-2022, as higher rates, frozen IPO markets, and higher debt costs broke the classic PE playbook, while hedge funds posted strong results in 2023–2025 and re-established themselves as an “all-weather” allocation.

- Where is it most visible?

- Across global institutional portfolios, especially among US and European allocators that heavily overweighted North American and global buyout funds and are now reallocating toward large multi-manager and specialist hedge fund platforms.

- Why is liquidity winning again?

- Because the old assumptions—cheap leverage, easy exits, and smooth private equity marks—no longer hold. Investors increasingly prize liquidity, transparency, and the ability to rebalance quickly over the theoretical illiquidity premium PE once promised.

What’s Actually Going Wrong With Private Equity Right Now?

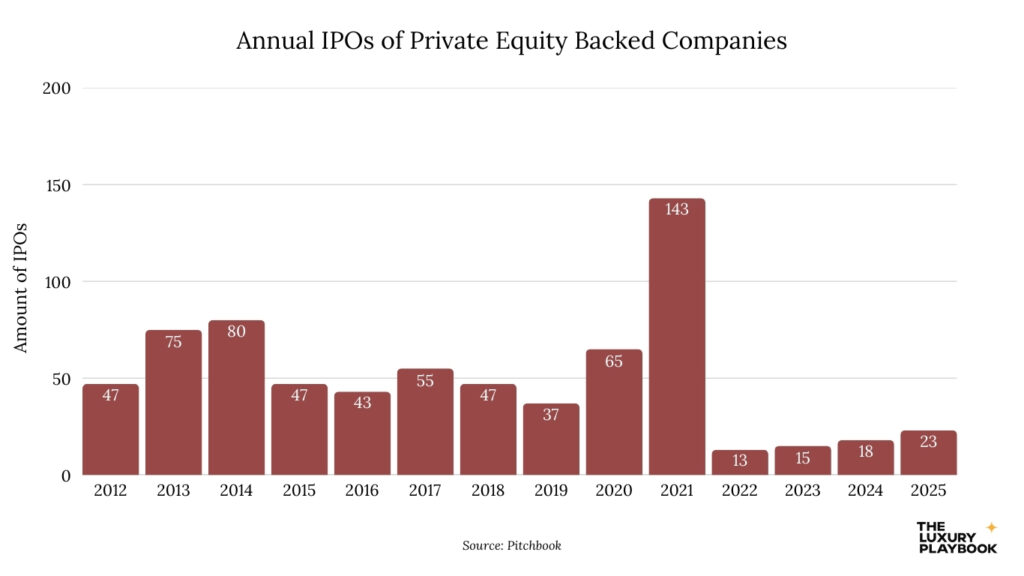

The exit problem is destroying private equity’s business model. With economic uncertainty weighing on markets, PE-backed IPOs in the U.S. were on pace for roughly 27 listings in 2026 versus 143 in 2021 according to S&P Global data, an 81% collapse from peak levels. That matters because private equity funds make money by buying companies, improving them, and selling them within a few years. When the exit door slams shut, the whole model breaks down.

When the exit door closes, the entire strategy breaks down.

Strategic buyers who might acquire portfolio companies face their own problems. Commonfund data shows the average cost of debt on PE deals hit approximately 8.2% in 2024, down from a 9.7% peak but still high enough to make acquisitions prohibitively expensive. When corporate buyers need to borrow at 8% instead of 3%, they can afford to pay far less for the same company.

That financing headwind hits both traditional M&A exits and secondary buyouts where one PE firm sells to another.

The result is that private equity funds are holding companies much longer than planned. S&P Global analysis shows average buyout holding periods reaching around 6.28 years in consumer discretionary, well beyond the classic three to five year playbook. Every extra year of holding means more management fees extracted from your capital and lower returns, even if the underlying business performs well.

This creates an enormous backlog choking the entire industry. Reporting based on Bain data describes over 28,000 unsold PE-owned companies valued at more than $3 trillion, with many already overdue for exit. General partners cannot raise new funds successfully when existing investors are still waiting for distributions from funds raised years ago.

The capital recycling that private equity depends on has essentially stopped working.

The valuation issues compound these exit problems. Major academic research found that in a typical quarter, almost 25% of buyout investments get marked down versus roughly 16% for venture capital. These write-downs force funds to reduce the reported values of portfolio companies, eroding the paper gains that justified high allocations to the strategy in the first place.

The gap between what companies were valued at during 2021 to 2022 fundraising and what they’re actually worth today creates performance pressure that only grows as more valuations get stress-tested.

For you as an investor, this shows up as brutal cash flow dynamics. Reuters Breakingviews citing Preqin data shows buyout firms called $130 billion more from investors than they returned between 2022 and early 2024. You’re funding capital calls into deteriorating conditions while receiving nothing back, and that dynamic cannot continue indefinitely.

The secondary market offers an escape valve but at a steep price. Investors sold a record $162 billion of PE stakes in secondary markets during 2024, with buyout stakes clearing around 6% below reported net asset value on average. Weaker strategies and older vintages trade at much steeper discounts, confirming that the reported valuations don’t reflect what sophisticated buyers are actually willing to pay.

Fee structures add insult to injury. Preqin data shows buyout funds raising in 2024 carried mean management fees around 1.74%. These fees get charged on committed capital regardless of whether exits happen, meaning funds collect tens of millions in fees while holding companies for years beyond planned timelines and delivering no cash back to you.

Hedge Funds vs Private Equity

Hedge Funds Scorecard

Private Equity Scorecard

Why Are Hedge Funds Suddenly Attractive to Sophisticated Investors Again?

The performance story is straightforward. The HFRI Fund Weighted Composite posted 7.5% in 2023 and 10.01% in 2024, a two-year run that compares favorably to many PE vintages without requiring decade-long lockups. And these aren’t paper gains dependent on optimistic valuations. They’re daily marked returns that you could have redeemed at any point. Understanding how hedging strategies protect your portfolio helps explain why that distinction matters so much right now.

The momentum carried through 2026 with results that make allocation committees comfortable shifting capital back to the strategy. Goldman Sachs reported stock-picking hedge funds averaged approximately 16.24% for 2026. When hedge funds deliver mid-teens returns in liquid strategies, the case for locking up your capital in illiquid alternatives for similar or lower returns becomes very hard to justify.

Liquidity has become genuinely valuable as market uncertainty has grown. The Hedge Fund Journal cites average redemption frequency of approximately 3.7 months in the U.S. and roughly 1.2 months in Europe. Many hedge funds can be fully rebalanced within a year, the complete opposite of private equity’s ten-year lockups. When geopolitical tensions escalate or market conditions deteriorate, the ability to exit positions in months rather than waiting years provides real portfolio protection.

That flexibility matters more than many investors realized during the low-rate era when markets moved steadily higher and illiquidity seemed costless. The past few years have reminded allocators that conditions can change fast and capital trapped in illiquid strategies offers no way to adapt. Diversifying into international stocks is one way to restore that adaptability, and hedge funds are another. Both restore your ability to respond to changing conditions rather than simply hoping that decade-old investment decisions still make sense years later.

Diversification benefits have returned as strategy dispersion widened. HFR’s main strategy indices in 2024 showed meaningful differences, with Equity Hedge finishing around 12.3% while Macro strategies delivered approximately 5.95%. That differentiation is exactly what you need when trying to reduce correlation to equity markets. The low-rate era saw hedge fund strategies compress toward similar exposures, but higher volatility has restored the strategy diversity that made hedge funds genuinely valuable.

Fees have compressed from the stereotypical two and twenty structure. Preqin reporting shows average hedge fund management fees around 1.38% as of September 2024, much closer to mutual fund pricing than the premium fees that were standard for years. That makes the strategy more competitive on a net-of-fee basis, especially when performance justifies paying for active management.

The best platforms can still command premium fees when they deliver consistent results. A BNP Paribas investor survey reported average hedge fund management fees rising to approximately 1.54% in 2024 with performance fees at 17.82%, driven by demand for large multi-manager platforms. Allocators are choosing to pay these fees for strategies that offer daily risk management, immediate liquidity, and diversification across dozens of portfolio managers rather than betting on single general partners with ten-year lockups.

Operational improvements address many concerns that drove institutions away from hedge funds after the financial crisis. Quarterly liquidity has become standard rather than exceptional. Transparency has improved with better reporting on positions and risks. Founder capital co-investment ensures alignment in ways that private equity’s fee structures sometimes fail to achieve when general partners collect management fees for years regardless of whether exits ever happen.

The shift from private equity back to hedge funds reflects changing market realities rather than fashion or panic. The assumptions that justified massive PE allocations during the 2010s no longer hold. Exit markets have frozen, valuations face downward pressure, and liquidity has a value that you simply cannot ignore.

Hedge funds have addressed the performance and operational issues that made them less attractive during the low-volatility era. For you as an allocator building a portfolio today, the choice increasingly favors strategies offering genuine liquidity, transparent pricing, and the ability to adapt quickly over illiquid vehicles that may not exit for years and whose valuations stay questionable until actual transactions prove them out. The Financial Times has tracked this institutional rotation closely, and the direction of capital flow tells a clear story.