Dubai’s real estate market in 2025 is entering a phase of calculated momentum, shaped by regulatory clarity, rapid infrastructure expansion, and shifting global capital flows. After a record-breaking 2023 and a slightly cooled—but still active—2024, the city has transitioned from a speculative surge into a more stable and strategic investment environment.

This shift is especially significant for institutional and high-net-worth investors. With the emirate recording over AED 430 billion in real estate transactions in 2024, and maintaining strong off-plan sales into Q2 2025, Dubai continues to offer a unique blend of high liquidity, zero property taxes, and strong yields—often between 6% and 9% net, depending on the asset class and location.

Furthermore, demand is increasingly driven by long-term residency incentives such as the Golden Visa, alongside a diversified influx of investors from Europe, Russia, India, and East Asia. Unlike previous cycles, the current market growth is being fueled by end-user demand and yield-seeking investors, rather than short-term flippers.

The 2025 market is also defined by a clear divergence: premium neighborhoods are witnessing capital preservation and appreciation, while emerging areas are providing strong rental income opportunities.

Table of Contents

Overview of The Dubai Real Estate Market

As of Q2 2025, the Dubai Real Estate Market continues to exhibit steady expansion, marked by high transaction volumes, resilient pricing, and a diversified investor base. The emirate recorded over AED 120 billion in residential sales during the first quarter alone—an 18% increase compared to Q2 2024—driven primarily by sustained demand in both the off-plan and ready property segments.

Average residential prices across the city rose by approximately 5.6% year-over-year, with apartment prices increasing more moderately at 4.2% and villa prices climbing by 7.9%. This upward movement is fueled by constrained supply in prime villa communities, and high absorption rates in emerging areas.

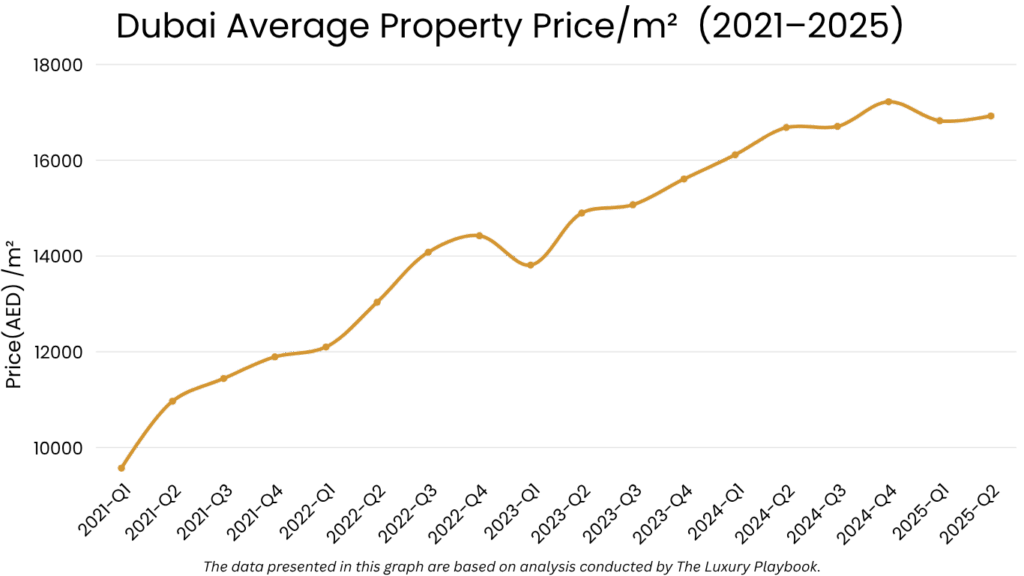

The average price per square meter for residential property in Dubai stands at approximately AED 16,924 (USD 4,580), though this varies considerably by area and asset class.

Premium zones like Downtown Dubai and Palm Jumeirah exceed USD 6,000/sqm, while suburban developments such as Dubailand and Jumeirah Village Circle offer opportunities closer to USD 2,200–2,800/sqm, attracting yield-driven investors.

Inventory remains healthy but tightening. The total number of new listings has plateaued compared to mid-2024 levels, as developers focus on phased project launches to align with actual buyer interest. Moreover, properties are selling faster—averaging 34 days on the market, compared to 46 days a year ago—indicating growing urgency among buyers.

Foreign investor participation remains dominant, accounting for nearly 58% of all residential transactions. Indian, Russian, British, Chinese, and German investors lead the pack, drawn by the UAE’s tax advantages, political stability, and lifestyle appeal.

The current investment climate is characterized by:

- Price Appreciation – Residential values up 5.6% YoY, with villas leading growth.

- High Foreign Demand – Over half of transactions involve international buyers.

- Market Liquidity – Over AED 120 billion in residential sales in Q2 2025.

- Tightening Supply – Average time-on-market reduced to 34 days.

- Strong Price/Square Meter Ranges – From USD 2,200 to 6,000/sqm, offering flexibility by submarket.

In summary, Dubai’s housing market in 2025 is transitioning into a mature, investor-oriented environment—balancing stable returns with moderate capital growth. For buyers, the key lies in submarket selection and asset strategy. For sellers, competitive pricing and value enhancement remain crucial in a market driven by data, yield, and global demand.

Neighborhood Analysis

Dubai is composed of a wide array of residential districts, each offering unique investment profiles, price points, and demand characteristics. These differences are essential for buyers and investors aiming to strategically position themselves in a market where value, yield, and long-term appreciation vary significantly from one neighborhood to another.

Downtown Dubai

Downtown Dubai remains one of the most iconic and high-performing districts in the city. Known for its proximity to the Burj Khalifa, Dubai Mall, and DIFC, it attracts institutional investors, executives, and affluent international buyers seeking long-term asset stability.

The median home price in Downtown Dubai is approximately AED 3.4 million, reflecting a 5.8% increase year-over-year. Properties in this area tend to transact near asking price, and demand remains resilient due to the limited availability of new inventory. Homes in Downtown typically sell quickly, supported by high liquidity and investor confidence. While gross rental yields are moderate, capital preservation is a primary draw for long-term investors.

Palm Jumeirah

Palm Jumeirah stands out as one of Dubai’s most exclusive beachfront communities. It continues to attract high-net-worth individuals from Europe, Russia, and the GCC, many of whom are purchasing for lifestyle or legacy reasons rather than yield alone.

The median property price on Palm Jumeirah is around AED 8.2 million, with a 4.1% year-over-year appreciation. Due to its luxury profile, properties often feature bespoke architecture, private beach access, and are frequently transacted in cash. While entry prices are high, rental demand for luxury villas and branded residences remains strong, offering stable mid-single-digit returns in addition to prestige-driven capital growth.

Dubai Marina

Dubai Marina is among the most popular residential hubs for expats and young professionals. With its waterfront promenade, retail options, and vibrant lifestyle, the area consistently ranks high for both owner-occupiers and rental investors.

The median home price in Dubai Marina is AED 2.1 million, with a 6.2% increase year-over-year. The area has strong rental absorption, especially for one- and two-bedroom apartments, and benefits from a dense mix of residential towers and hospitality assets. Dubai Marina is particularly attractive to investors focused on short-term leasing or serviced apartment strategies due to consistently high occupancy and turnover rates.

Business Bay

Adjacent to Downtown Dubai, Business Bay is rapidly transitioning into a mixed-use powerhouse. It features a blend of commercial towers, high-rise residences, and branded developments, making it a go-to location for professionals and executives.

The median property price in Business Bay is AED 1.8 million, increasing by 5.5% from Q2 2024. Strong infrastructure, canal views, and its adjacency to major business districts make it a preferred choice for those seeking a balance between residential and commercial appeal. New projects here are often aligned with modern design, smart technology, and hospitality-driven amenities, contributing to above-average appreciation potential.

Dubai Hills Estate

Dubai Hills Estate offers a suburban luxury lifestyle with golf course views, international schools, and hospital access. Developed by Emaar, it appeals to families and long-term residents looking for villa communities within proximity to central Dubai.

The median price in Dubai Hills is AED 3.7 million, reflecting a 4.6% increase year-over-year. The area benefits from its master-planned layout, wide green spaces, and consistently high build quality. Rental demand remains stable, especially among well-paid professionals and expatriates seeking long-term accommodation with lifestyle benefits.

Neighborhood Median Prices and Price per Square Meter

Dubai Rental Market Overview

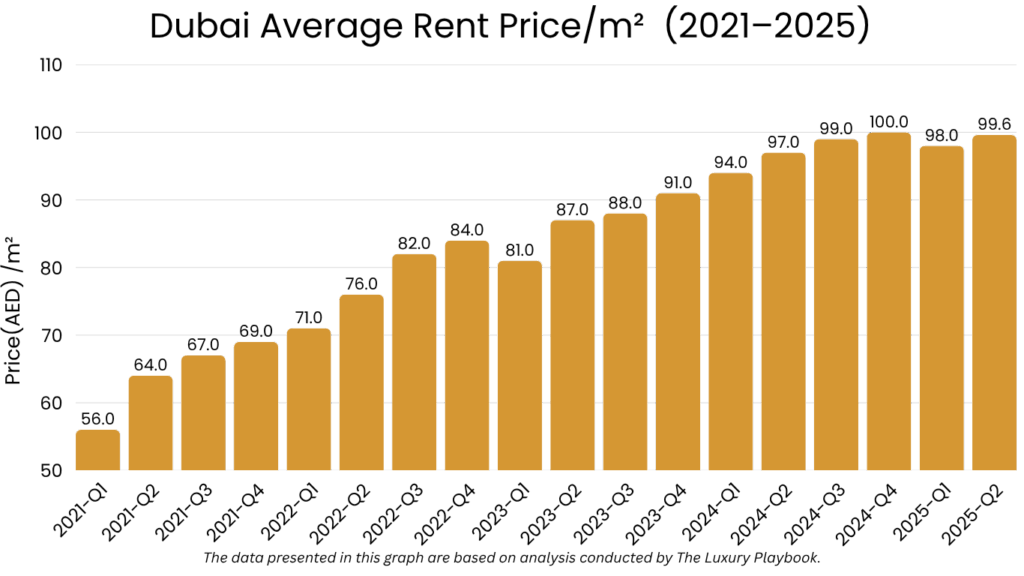

The Dubai rental market in 2025 continues to exhibit strong performance, underpinned by sustained population growth, limited housing supply in key segments, and elevated barriers to homeownership. Despite a moderation in rent growth compared to 2023’s sharp spikes, the market remains one of the most attractive globally for investors seeking high-yield rental returns.

As of Q2 2025, the average rent for residential units has increased by 4.2% year-over-year, driven largely by increased demand in both prime and mid-market neighborhoods. This growth is particularly noticeable in communities close to transit corridors, employment zones, and lifestyle hubs.

Average Rent Prices in Dubai

- Studio Apartments: AED 54,000 per year (USD ~14,700)

- One-Bedroom Apartments: AED 78,000 per year (USD ~21,200)

- Two-Bedroom Apartments: AED 115,000 per year (USD ~31,250)

- Three-Bedroom Apartments: AED 165,000 per year (USD ~44,800)

Notably, while premium communities such as Palm Jumeirah and Downtown Dubai have seen stabilization in rents, emerging areas like JVC and Al Furjan continue to experience consistent annual growth exceeding 5%, supported by affordability and new infrastructure developments.

Rent by Neighborhood

- Downtown Dubai: One-bedroom units average AED 115,000/year, supported by consistent executive-level demand and proximity to DIFC.

- Palm Jumeirah: Two-bedroom units average AED 220,000/year, driven by beachfront appeal and luxury lifestyle demand.

- Dubai Marina: One-bedroom apartments lease for around AED 100,000/year, benefiting from short-term rental turnover and expat appeal.

- JVC: One-bedroom units average AED 65,000/year, with rent growth of over 6.1% year-over-year due to demand for affordable modern living.

- Business Bay: Studios lease at around AED 65,000/year, supported by commercial proximity and hospitality-branded residences.

Vacancy Rates and Demand

Vacancy rates in Dubai’s residential market are averaging 5.4%, with rates below 4% in high-demand districts such as Dubai Marina, JVC, and Downtown. This marks a notable tightening compared to 2022–2023, when post-pandemic construction created temporary oversupply in fringe areas.

Landlords now have enhanced pricing power, particularly in master-planned communities and in projects offering amenities such as co-working spaces, gyms, and concierge services. Additionally, limited new affordable housing supply is reinforcing upward rental pressure in mid-tier communities.

Drivers of Rental Demand

Several key factors continue to drive demand in Dubai’s rental market:

- Affordability Gap: With average home prices exceeding AED 1.5 million in many districts, many residents opt to rent instead of buy—particularly among young professionals and expatriates.

- High Mortgage Rates: Borrowing costs between 5.25% and 5.75% have kept many prospective buyers in the rental segment.

- Visa Reforms: Long-term visas, including the Golden Visa, have incentivized skilled workers and business owners to relocate—without immediate homeownership.

- Job Market Expansion: Dubai’s continued growth in finance, tech, hospitality, and healthcare is drawing high-salaried professionals with mid-to-high-end rental needs.

Investor Outlook

For investors, Dubai remains a landlord-favorable market. Rental yields in mid-tier communities such as JVC and Arjan average between 7% and 8.5%, offering strong income-generating potential. Luxury districts continue to yield 4% to 5%, particularly when operated under regulated short-term rental or holiday home licenses.

With rent prices continuing to rise and vacancy rates falling in high-demand zones, landlords enjoy enhanced pricing leverage and stable occupancy. Furthermore, the city’s streamlined rental regulations and lack of property taxes contribute to net income preservation, making Dubai particularly attractive for buy-and-hold investors seeking both cash flow and long-term asset appreciation.

Factors Influencing The Dubai Housing Market

The Dubai housing market in 2025 is shaped by a combination of economic forces, demographic shifts, regulatory incentives, and global investment patterns. Understanding these key drivers is essential for investors seeking to optimize entry timing, evaluate long-term performance, and position assets within high-demand segments.

- High Mortgage Rates: Home financing costs in the UAE remain elevated, with rates hovering between 5.25% and 5.75%. These higher borrowing rates are discouraging many first-time buyers from entering the ownership market, while also delaying upgrades among existing homeowners. The result is increased rental market retention and a cooling effect on mid-tier resale activity.

- Supply Constraints; Although developers continue to launch new projects, actual handovers are limited, particularly in the mid-income and affordable housing categories. Most upcoming supply is concentrated in luxury or branded developments, leaving a gap between real demand and available product. This imbalance supports continued price strength in several mid-tier neighborhoods.

- Population Growth and Migration: Dubai’s population surpassed 3.65 million in early 2025 and continues to grow rapidly due to residency reforms and favorable living conditions. New residents—particularly from India, Russia, Europe, and China—are fueling both rental absorption and ownership interest, especially in centrally located or master-planned communities.

- Limited Delivery of Affordable Units: Despite high-profile launches in areas like Dubai Creek Harbour and Business Bay, construction timelines and developer focus remain skewed toward high-margin luxury inventory. The affordable housing gap continues to widen, driving strong demand in areas like JVC, Al Furjan, and Dubai South.

- High Rental Demand: Many residents are choosing to lease rather than buy, largely due to high interest rates and increasing property values. As a result, rental yields remain attractive, especially in mid-tier and emerging communities. Investors are capitalizing on short-term rental strategies and extended lease terms to enhance returns.

- Foreign Investor Activity: Dubai continues to attract a diverse base of foreign capital. Over 58% of property transactions in Q2 2025 were driven by international investors. Buyers from India, the UK, China, and Russia are acquiring assets across both primary and secondary markets, drawn by Dubai’s tax-free regime and long-term residency options.

- Regulatory Advantages: Dubai’s business-friendly regulatory framework—featuring no property tax, no capital gains tax, and streamlined visa policies—makes it a standout global investment destination. Ongoing improvements in digital transactions and tenancy laws have also increased transparency, reducing risk for overseas investors.

Dubai Housing Market Forecast for 2026

Looking ahead to 2026, the Dubai housing market is expected to remain resilient and competitive, though the pace of growth is likely to moderate. Rising interest rates, supply-demand imbalances in affordable segments, and a more mature investor base are contributing to a climate of cautious but confident expansion.

While Dubai’s long-term fundamentals remain strong, near-term projections suggest steady growth rather than speculative surges.

Home prices in Dubai are projected to increase by 3.5% to 5.2% over the next 12 months. With the current median home price near AED 1.7 million, this would translate to values ranging between AED 1.76 million and AED 1.79 million by early 2026. Appreciation will continue to be driven by strong end-user demand, international capital inflows, and supply shortages in mid-income communities.

Inventory will remain tight in most districts. Although several new developments are in progress, the majority of handovers in 2026 are expected to be in high-end segments. This imbalance will likely maintain pressure on prices in key mid-tier zones, where demand continues to outstrip supply—particularly for move-in-ready or community-integrated units.

Areas such as Jumeirah Village Circle, Al Furjan, and Arjan are expected to attract increased buyer activity due to their affordability and long-term development potential.

The rental market is also expected to strengthen. Rents are projected to rise between 3% and 4.5%, fueled by a shortage of new rental inventory, high borrowing costs, and continued population growth. One-bedroom units could average between AED 80,000 and AED 82,500 per year, while two-bedroom apartments may reach AED 125,000 in high-demand neighborhoods.

Vacancy rates are not expected to rise significantly due to the limited supply of affordable rentals. Most upcoming developments in 2025 and 2026 cater to the luxury segment, which does little to alleviate pressure in mid-market areas. This will likely result in continued rent inflation, especially in communities near employment hubs, transit corridors, and lifestyle infrastructure.

Economically, Dubai remains in a strong position. Strategic investments in infrastructure, growing job markets in finance, logistics, and tourism, and continued population growth all support long-term housing demand. This favorable environment is further bolstered by investor-friendly regulations and the absence of property taxes.

Demographic patterns also remain positive, with a steady influx of skilled professionals and high-income expatriates supporting demand across both ownership and rental markets—especially in districts offering strong yields and capital appreciation potential.

Is It Worth Buying a Property in Dubai?

Yes—purchasing property in Dubai in 2025–2026 remains a sound decision for investors and end-users with a long-term outlook. Despite rising home values and financing costs, the market’s fundamentals remain robust, offering reliable income potential, capital appreciation, and investor-friendly regulations.

Home prices are projected to rise by 3.5% to 5.2% through 2026, supported by tight inventory, continued foreign investor activity, and resilient demand across both luxury and mid-tier segments. Neighborhoods such as JVC, Arjan, and Dubai South are expected to outperform the broader market average, offering a combination of value entry points and strong upside potential.

Rental demand also remains a significant advantage. With vacancy rates between 4% and 5.4%, and annual rent increases forecast at 3% to 4.5%, landlords enjoy strong tenant retention and rising cash flow. One-bedroom apartments are leasing for over AED 80,000 per year in centrally located areas, while two-bedroom units in mid-tier communities are approaching AED 125,000—offering compelling yields in the 6% to 8.5% range.

While initial investment costs and service charges may be considerable in premium zones, delaying a purchase could result in higher acquisition prices if interest rates ease in 2026. Should mortgage rates decline, pent-up demand is expected to resurface, creating increased competition and accelerating price recovery.

In short, Dubai continues to be a high-barrier, high-reward market.

For investors who can manage the upfront cost and hold their asset for 5 to 10 years, the combination of long-term growth, rental yield, and market resilience makes buying property in Dubai a strategically sound move.

Other Market Forecasts & Overviews

Abu Dhabi Real Estate Market Overview & Forecast

Sharjah Real Estate Market Overview & Forecast

Al Ain Real Estate Market Overview & Forecast

FAQ

What is the current median home price in Dubai?

As of Q2 2025, the median home price in Dubai is approximately AED 1.7 million, with variations depending on neighborhood and property type.

Will Dubai property prices go up in 2026?

Yes, Dubai property prices are projected to increase by 3.5% to 5.2% in 2026 due to limited supply and sustained demand.

Is Dubai a good place to invest in rental property?

Yes, Dubai offers high rental yields averaging 6% to 8.5%, strong tenant demand, and landlord-friendly regulations.

Which areas in Dubai are best for property investment?

Top investment areas include Jumeirah Village Circle, Arjan, Dubai Hills Estate, and Business Bay for growth, and Palm Jumeirah for luxury stability.

Does Dubai have property tax?

No, Dubai has no property tax, capital gains tax, or inheritance tax, making it highly attractive for global investors.