Structural decline differs fundamentally from cyclical downturns. While cyclical markets recover when economic conditions improve, structural decline reflects permanent demand shifts driven by demographic change, evolving health policy, and cultural transformation that reshape entire industries regardless of economic cycles.

These shifts operate on generational timescales, making them predictable yet difficult to reverse once momentum builds.

For decades, alternative asset investors viewed European wine, particularly Bordeaux, Burgundy, and Italian collectibles, as stable wealth preservation vehicles that delivered both enjoyment and portfolio diversification. These markets offered tangible assets with established provenance, limited supply from geographically constrained appellations, and consistent demand from sophisticated collectors worldwide who valued both drinking pleasure and investment potential.

However, the EU Agricultural Outlook 2025-2035 report challenges this traditional view with projections that represent expert consensus rather than temporary market sentiment or cyclical pessimism. The report’s forecasts, based on rigorous analysis of demographic data, consumption trends across age cohorts, and production economics at farm level, suggest European wine faces a fundamental reshaping that investors can no longer ignore.

Unlike previous downturns driven by economic recessions or vintage quality variations, this decline stems from permanent behavioral changes among younger generations who simply consume wine differently than their parents and grandparents did.

Table of Contents

Key Takeaways & The 5Ws

- European wine is facing structural, not cyclical, decline—driven by demographics, health policy, and changing drinking habits—so a simple “wait for the next boom” approach no longer works.

- France and Germany’s per-capita wine consumption is expected to fall steadily through 2035, creating persistent oversupply that pressures producers, weaker regions, and commodity red wines most of all.

- Farm-level economics are deteriorating: vineyard area is shrinking, income per work unit is falling, and marginal vineyards are being abandoned or converted, reshaping Europe’s wine map over the next decade.

- For investors, the rational response is selective de-risking—reducing exposure to volume-driven, undifferentiated regions while concentrating on genuinely premium, scarce estates that can benefit from trade-up behavior and supply contraction.

- Who is affected?

- Wine investors, family offices, and collectors with meaningful exposure to European wine, plus producers and estates whose long-term viability depends on adapting to structurally lower volumes and more selective demand.

- What is changing?

- A long-term shift away from high-volume European wine consumption toward lower-frequency, higher-quality purchasing—pressuring commodity reds while preserving and sometimes improving the economics of top-tier producers.

- When does it play out?

- From now through 2035, aligning with the EU’s 2025–2035 outlook horizon as declines in per-capita consumption, vineyard area, and farm income compound and permanently reshape the landscape.

- Where is the pressure concentrated?

- Across Europe’s traditional heartlands—France, Germany, Spain, and Italy—while export markets like the US and UK are no longer a reliable escape valve; only the strongest appellations and producers retain clear pricing power.

- Why is this structural?

- Because younger generations drink less and differently, health policy is becoming more anti-alcohol, and production economics no longer support Europe’s historic volume model—forcing a shift from broad “European wine beta” to focused exposure in scarce, blue-chip names.

Which Specific European Markets And Categories Are Experiencing The Steepest Declines?

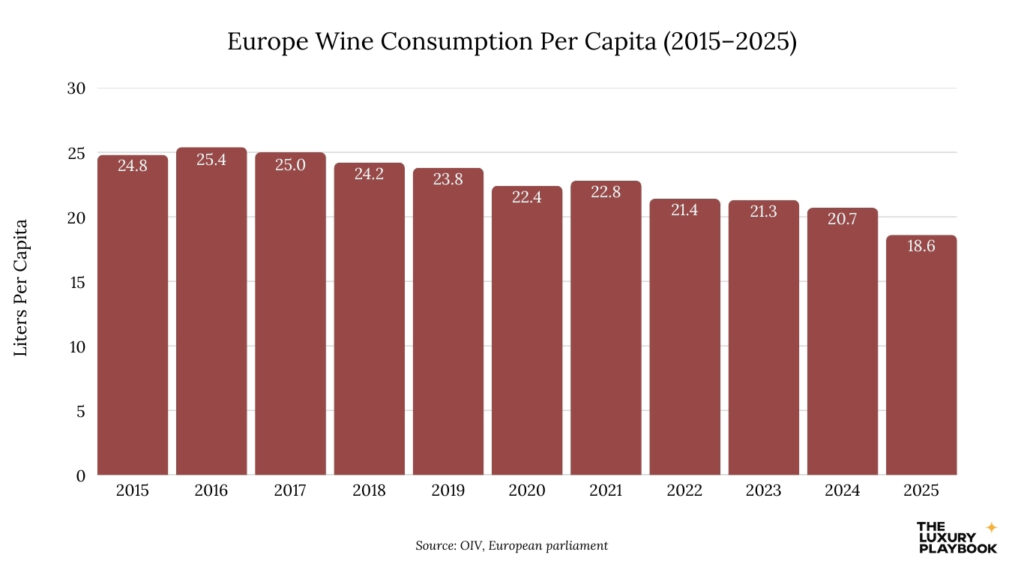

The consumption collapse in France and Germany, Europe’s two largest wine drinking markets, anchors the EU’s pessimistic outlook and signals broader continental trends.

These markets will see the steepest per capita consumption drops through 2035, falling from an average of 21.2 liters during 2021-2025 to 19.3 liters by 2035, representing a 0.9% annual decline that compounds relentlessly year after year.

This erosion stems from generational turnover as younger consumers drink substantially less wine than their parents, combined with increasingly aggressive government health messaging that frames alcohol consumption as a public health concern rather than cultural tradition deserving protection and celebration.

The French and German declines carry particular significance because these markets historically absorbed enormous volumes of domestic production while also importing premium wines from neighboring regions. Their retreat creates oversupply pressures that cascade through the entire European wine system.

Spain and Italy, while experiencing somewhat slower per capita declines, face similar demographic headwinds as their younger populations adopt consumption patterns more aligned with northern European moderation than Mediterranean tradition.

This demand deterioration directly impacts the production side, where EU wine output is projected to decline 0.5% annually, reaching 138 million hectoliters by 2035 from current levels above 145 million hectoliters. The production decline links directly to vineyard area reduction of 0.6% per year as unprofitable farms exit the market and labor shortages intensify across southern Europe.

Marginal vineyards that once remained economically viable during periods of stronger demand now face closure as the market contracts around them, unable to generate sufficient revenue to justify continued cultivation when alternative land uses or outright abandonment offer better economic outcomes.

Meanwhile, the category level data reveals even more granular erosion patterns that matter enormously for investors holding specific wine types. Euromonitor research shows red and rosé wines losing market share across Europe while sparkling wines gain ground and wine based drinks grow from a small base, capturing younger consumers who prefer lower alcohol, sweeter, and more mixable products.

This shift reflects a fundamental change from daily consumption habits, where Europeans once drank wine with lunch and dinner as a matter of routine, to occasional premium purchasing where consumers drink less frequently but trade up when they do buy. The implication for traditional red wine producers, which dominate investment grade European wine, is particularly concerning because their products face the steepest category level headwinds.

At the same time, export markets that once absorbed European overproduction and supported prices during domestic weakness are mirroring consumption declines rather than providing relief. The EU’s main export destinations, with the United States ranking first and the United Kingdom second, face their own wine consumption headwinds driven by similar generational preferences and health consciousness trends.

American wine consumption per capita has plateaued after decades of growth, while British consumers have reduced wine purchases amid economic pressures and changing drinking habits. Latin America and African growth markets, though showing positive momentum, remain too small in absolute volume terms to offset this weakness in major developed markets, leaving EU exports projected to decrease 0.6% annually through 2035.

These macro trends manifest most dramatically in specific regions, with southern France experiencing accelerated vineyard decline that reduces crop diversity and signals deeper structural challenges threatening traditional wine territories.

When vineyards disappear, the supporting infrastructure of cooperatives, bottling facilities, and distribution networks also deteriorates, making it progressively harder for remaining producers to operate efficiently even if they maintain individual viability.

What Should Wine Investors Do With European Allocations In Light Of These Projections?

Understanding these market dynamics requires examining the economics at farm level, where viability erosion tells a sobering story that aggregate statistics sometimes obscure. The EU projects wine farm income per annual work unit decreasing 2.5% between 2020-2035 as real output prices decline while input costs for equipment, chemicals, energy, and labor remain stable or increase.

This margin compression means the viable farm share falls from 87% to 83%, with the largest farms, often viewed as more resilient due to economies of scale, actually most exposed to margin compression because they cannot easily adjust production volumes downward without stranding fixed capital investments in equipment and facilities.

The farm income decline creates a vicious cycle where reduced profitability triggers deferred maintenance, underinvestment in quality improvements, and eventual exit decisions that further reduce supply but also damage regional reputations when wine quality deteriorates.

Younger generations inheriting family vineyards increasingly choose to sell land for development or agricultural conversion rather than continuing unprofitable wine production, accelerating the vineyard area contraction beyond what current economics alone would dictate.

However, within this broader decline lies a critical nuance that creates selective opportunities for discerning investors. Despite volume decline, consumer trade up behavior means buyers purchase less frequently but pay substantially more per bottle when they do make purchases.

This premiumization trend creates genuine opportunities in premium segments and established appellations with inherent scarcity value, where quality provides insulation from volume decline and actually supports pricing power. The challenge becomes identifying which producers genuinely benefit from premiumization versus those drowning in a shrinking commodity market where trading up means consumers abandon their products entirely in favor of higher quality alternatives.

This quality versus volume distinction suggests a geographic reallocation strategy for existing European wine investors who want to maintain exposure to the category while managing downside risk. Consider reducing exposure to volume dependent European regions where farm economics deteriorate relentlessly and vineyard abandonment accelerates beyond projections.

Focus reductions on areas producing commodity wines without strong appellation identity or quality differentiation that would support premium pricing. At the same time, maintain or even increase allocation to blue chip classified growth estates in Bordeaux, Grand Cru Burgundy, and Super Tuscans where scarcity combined with quality creates insulation from volume decline.

These top tier properties may actually benefit as marginal producers exit and supply concentrates among the most prestigious names that dominate collector attention and auction results.

Finally, implementing a comprehensive risk monitoring framework helps investors detect whether decline accelerates beyond EU projections or stabilizes better than expected, allowing for tactical adjustments before major portfolio damage occurs.

Watch for acceleration signals including faster than projected vineyard abandonment rates that would indicate farm economics are worse than modeled, export tariff developments particularly concerning the United States market where trade policy could compound consumption headwinds, oversupply inventory builds like Italy’s already substantial 53.3 million hectoliters that create price pressure when producers must liquidate stock, and generational wealth transfer dynamics creating forced liquidations as aging collectors pass extensive collections to heirs with less emotional attachment to wine who view holdings as assets to monetize rather than treasures to preserve.

These monitoring indicators provide early warning whether structural decline proceeds as projected or accelerates into something more severe that demands faster and more aggressive portfolio repositioning.