The Madrid Real Estate Market in 2025 continues to show strong fundamentals, driven by steady price appreciation, robust investor interest, and an evolving rental landscape. As Spain’s capital and economic hub, Madrid offers a strategic balance between liquidity, growth potential, and long-term asset stability—positioning it as one of the most attractive metropolitan markets in Southern Europe.

Madrid remains a focal point for both domestic and international buyers, thanks to its diverse housing stock, mature regulatory framework, and expanding infrastructure.

The city’s residential market has seen consistent growth, with prices rising by over 12% year-on-year, particularly in well-connected and gentrifying neighborhoods. Demand continues to outpace supply, reinforcing upward pressure on both purchase prices and rental rates.

While affordability concerns are emerging—particularly among first-time buyers—the city’s fundamentals remain sound. Low mortgage rates, favorable tax conditions, and ongoing investment in urban renewal projects continue to support capital inflow and occupancy resilience. Foreign investment, especially from Europe and Latin America, plays a key role in driving the high-end and new development segments.

Table of Contents

Overview of The Madrid Real Estate Market

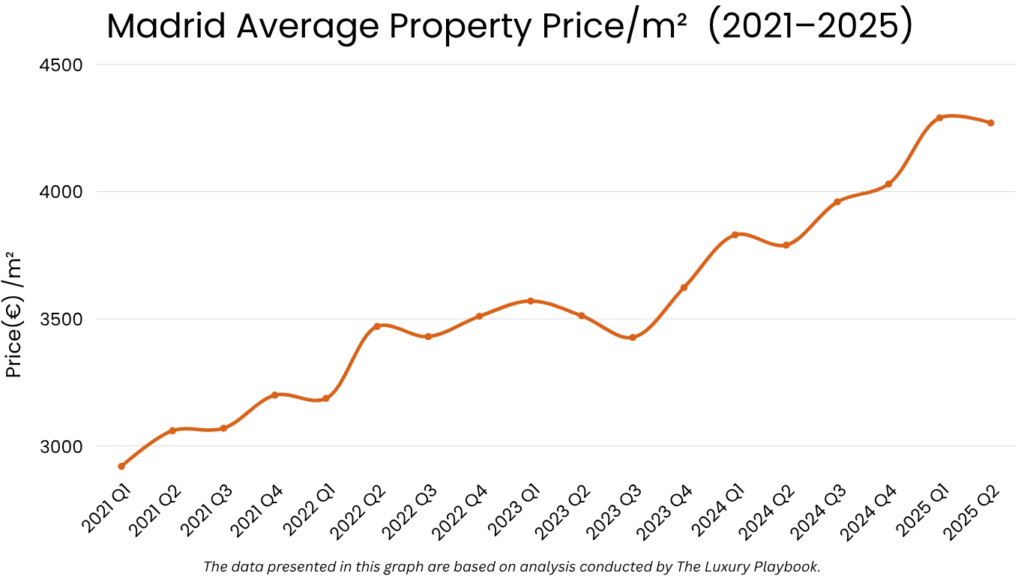

The Madrid Housing Market in 2025 continues to perform as one of Spain’s most robust and active real estate environments. With demand outpacing supply in both purchase and rental sectors, property values have risen steadily across nearly all districts. Price increases are driven by a combination of low interest rates, increased foreign investment, population growth, and renewed urban development.

As of Q2 2025, the average residential price in Madrid is approximately €4,270 per square meter, representing a 11.2% increase year-over-year.

New-build properties in prime districts such as Salamanca, Chamberí, and Retiro routinely exceed €6,000–€8,000 per sqm, while emerging areas like Carabanchel and Vallecas remain in the €2,500–€3,500 per sqm range, offering value-driven entry points for investors targeting medium-term appreciation.

Luxury and mid-tier segments have both expanded, with strong resale demand in central zones and an increasing volume of new developments along major transit corridors.

Notably, many districts undergoing gentrification—particularly Tetuán, Arganzuela, and Usera—are attracting both domestic buyers and foreign capital due to favorable price-to-rent ratios and infrastructure improvements.

Madrid’s investor profile has also diversified. While institutional players remain active in large-scale developments and PRS (private rented sector) portfolios, individual investors—particularly from Latin America, Northern Europe, and the UAE—have increased their footprint in the upper-middle segment of the market.

Key market characteristics as of 2025:

- Average property price: €4,270/sqm (citywide); >€6,500/sqm in central districts

- Annual growth rate: 11.2% (Q2 2024 to Q2 2025)

- New-build premium: Up to 30% above resale units in top-tier neighborhoods

- Buyer profile: Spanish nationals, Latin American investors, EU retirees, and institutional landlords

- Market driver: Supply constraints, demographic growth, and consistent rental demand

In summary, the Madrid Housing Market offers a mix of high-performance zones for appreciation and emerging districts for yield. Strategic positioning across gentrifying areas and core residential hubs remains essential for investors aiming to balance growth and cash flow.

Neighborhood Analysis

Madrid’s real estate market is shaped by distinct district-level dynamics, where pricing, demand drivers, and investment profiles vary significantly. Central neighborhoods maintain value due to heritage buildings and location scarcity, while peripheral zones offer growth potential through urban regeneration and infrastructure development.

Salamanca

Salamanca remains Madrid’s most prestigious district, known for its classical architecture, luxury boutiques, and diplomatic residences. It consistently ranks among the most expensive areas in the city.

Average property prices exceed €8,000 per square meter, with penthouses and historic buildings often priced above €10,000/sqm. Investor demand is driven by wealth preservation, particularly from Latin American and European HNWIs.

Chamberí

Chamberí offers a blend of residential charm and central location. It attracts affluent professionals, diplomats, and long-term renters seeking proximity to universities, embassies, and the financial district.

Prices in Chamberí average €6,200–€7,000/sqm, with refurbished apartments commanding a premium. The district is ideal for mid-to-long-term capital appreciation and secure tenancy.

Retiro

Adjacent to the city’s iconic park, Retiro offers high-end housing with strong owner-occupier and investor appeal. It is favored for its quiet streets, excellent schools, and long-term value stability.

Current prices average €6,000–€6,800/sqm, depending on proximity to the park. Rental demand is strong from executive families and corporate tenants.

Tetuán

Tetuán has emerged as a key regeneration zone. Once overlooked, it now attracts younger buyers and investors due to affordable pricing and increasing new development.

Average prices range from €3,500 to €4,200/sqm, with steady growth expected as infrastructure improves. It remains a top target for medium-yield residential investment.

Arganzuela

Located just south of the city center, Arganzuela benefits from its proximity to Atocha Station and the Madrid Río redevelopment. It offers a mix of modern apartments and converted lofts.

Prices average €4,200–€5,000/sqm, with consistent demand from young professionals and city commuters. The district is especially suited for long-term rental portfolios.

Neighborhood Median Prices and Price per Square Meter

Madrid Rental Market Overview

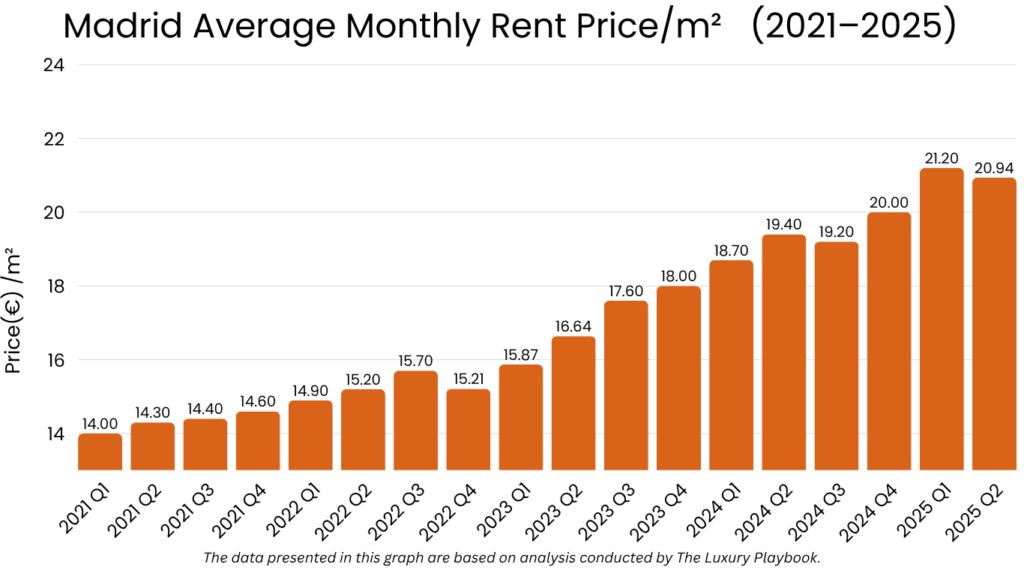

The Madrid rental market in 2025 is one of the most liquid and active in Europe. Strong population growth, a recovering labor market, and elevated mortgage barriers have intensified demand across all segments. While the market faces affordability pressures, rental properties in well-connected districts continue to deliver solid occupancy and stable gross yields.

Madrid’s rental landscape is characterized by long-term lease security, consistent tenant demand, and varied performance across central and emerging districts.

Average Monthly Rent by Property Type (2025)

- 1-Bedroom Apartment: €950 – €1,300

- 2-Bedroom Apartment: €1,300 – €1,800

- 3-Bedroom Apartment: €1,800 – €2,600

- Luxury Apartments (Salamanca, Chamberí): €3,500 – €6,000+

Rental growth has accelerated in central and gentrifying districts, driven by foreign professionals, remote workers, and rising local demand. Areas like Salamanca, Chamberí, and Retiro remain at the top of the price spectrum, while Tetuán, Arganzuela, and Vallecas offer more accessible entry points with competitive yields.

Yield Performance and Rental Segmentation

Gross rental yields in Madrid typically range between 3.5% and 6.0%, depending on district, property type, and management model:

- High-Yield Areas: Vallecas, Carabanchel, Usera (5.2%–6.0%)

- Balanced Core Areas: Arganzuela, Tetuán, Chamartín (4.2%–5.0%)

- Capital Preservation Zones: Salamanca, Retiro, Chamberí (3.5%–4.2%)

Well-managed units in transit-accessible locations continue to perform strongly, especially when equipped with energy-efficient upgrades and tenant-ready finishes. Corporate leases and student demand also provide stable, low-turnover occupancy in certain areas.

Moreover, Madrid’s rental market is governed by Spain’s Urban Lease Law (LAU), which protects tenant rights and regulates minimum contract durations. Rent increases are index-linked unless otherwise negotiated, and eviction procedures can be slow relative to other European cities.

Short-term rentals are subject to municipal licensing and regional tourism regulation. In the city center, moratoriums and license caps limit Airbnb-style offerings, pushing more investors toward long-term leasing strategies.

In summary, the Madrid rental market offers strong income potential with scalable portfolio options across a range of price points. Investors should align acquisition strategies with district-level yield performance and maintain compliance with evolving rental regulation.

Factors Influencing the Madrid Housing Market

The Madrid Housing Market in 2025 is influenced by a combination of macroeconomic recovery, demographic growth, regulatory adjustments, and infrastructure investment. These factors continue to shape both property values and rental performance across the capital.

- Population Growth and Urbanization: Madrid’s population continues to expand, driven by internal migration, international arrivals, and an increasing number of professionals relocating for work or education. This sustained growth fuels residential demand, particularly in well-connected and affordable districts.

- Foreign Investment and Capital Inflows: Madrid remains a top destination for foreign investors, particularly from Latin America, the EU, and the Middle East. Capital continues to target both luxury properties and value-seeking districts with yield potential. Political stability and favorable ownership laws add to its appeal.

- Infrastructure and Public Transport Expansion: Large-scale projects like Madrid Nuevo Norte and metro line extensions are increasing connectivity across the city. These upgrades raise the profile of peripheral districts such as Chamartín, Tetuán, and Valdebebas, enhancing long-term investment potential in these areas.

- Mortgage Affordability and Financing Conditions: Low interest rates and flexible mortgage products have stimulated local buyer activity. However, rising housing prices relative to income have pushed many would-be owners into the rental market, strengthening leasing demand and improving rental cash flows for investors.

- Regulatory Adjustments and Rent Control Proposals: Recent debates around rent caps and urban housing reform have created some uncertainty. However, Madrid currently maintains a landlord-favorable regulatory environment, particularly compared to regions like Catalonia. Long-term lease protections remain, but rent caps have not been widely implemented in the city.

- Gentrification and Urban Redevelopment: Districts such as Tetuán, Arganzuela, Usera, and Carabanchel continue to undergo transformation through new development, retail growth, and improved public services. These trends make them prime targets for yield-driven investors seeking medium-term capital gains.

- Tourism and Short-Term Leasing: Madrid remains a major tourism hub, but tighter short-let regulations have limited investor activity in the city center. As a result, more landlords are shifting toward long-term rental models, especially in areas with strong local demand and flexible leasing conditions.

Madrid Housing Market Forecast for 2026

The Madrid Housing Market is expected to continue its upward trajectory through 2026, supported by resilient domestic demand, steady foreign investment, and ongoing urban development initiatives. While rising interest rates and affordability concerns may temper growth in some submarkets, the city overall is projected to deliver stable price appreciation and solid rental performance.

Madrid remains a growth-oriented European capital, offering attractive long-term value, particularly in districts with ongoing regeneration and transport expansion.

Property prices in Madrid are forecast to increase by 4.5% to 6.0% in 2026. Core districts such as Salamanca, Chamberí, and Retiro will continue to command a premium, with prices expected to surpass €9,000 per square meter in the most sought-after areas. Meanwhile, emerging zones like Tetuán, Usera, and Carabanchel are likely to experience 5.0%–7.5% price growth, driven by affordability, infrastructure upgrades, and buyer migration from saturated central zones.

The citywide average is projected to reach approximately €4,500–€4,700/sqm by late 2026, assuming current demand trends and economic forecasts hold.

Rental prices are projected to increase by 3.0% to 4.5%, especially in mid-tier and commuter-friendly areas. The highest increases are expected in Tetuán, Chamartín, and Arganzuela, where a growing population and limited supply of rental units are pushing prices upward.

- 2-bedroom apartments in city-center districts may exceed €2,000/month.

- Units in outer districts such as Vallecas and Carabanchel are likely to remain below €1,300/month, offering higher yield potential and tenant liquidity.

No major correction is expected in 2026. Despite rising financing costs, Madrid’s housing supply remains below structural demand. New-build pipelines are concentrated in select areas (e.g., Valdebebas, Ensanche de Vallecas), but delivery remains slow relative to population growth. Investor appetite is likely to remain strong for both appreciation and rental income plays.

Foreign investment is expected to remain a key market driver. Interest from Latin America, the EU, and the Middle East will continue to support the luxury and mid-market sectors. Visa-related acquisitions, relocation-driven purchases, and lifestyle investments will sustain cross-border demand, particularly for well-positioned, energy-efficient properties.

In summary, the Madrid Housing Market in 2026 is forecast to deliver stable growth, healthy rental income, and continued capital inflow. With value gaps between central and peripheral districts narrowing, investors who target urban fringe areas with strong fundamentals may benefit from both appreciation and income generation.

Is It Worth Buying a Property in Madrid?

Yes—with caveats. The Madrid Housing Market in 2025–2026 offers solid long-term fundamentals, stable price growth, and relatively attractive yields compared to other Western European capitals. However, rising acquisition costs, regulatory uncertainty, and uneven submarket performance require a more selective investment strategy than in previous cycles.

Madrid continues to benefit from strong demographic growth, cross-border capital inflows, and structural housing demand.

Average prices remain competitive on a European scale, and gross yields of 3.5% to 6.0% remain achievable—especially in outer districts such as Vallecas, Usera, and Carabanchel. Investors focused on rental income and urban regeneration areas may find the best returns over a 5–10 year horizon.

However, it is essential to approach the market with realistic expectations:

- Price growth is slowing in mature areas like Salamanca and Chamberí, where upside is limited and entry costs are high.

- Affordability pressures are rising, which may increase political momentum for rent caps or intervention—particularly in city-center districts.

- Short-term rental restrictions have tightened, limiting flexibility for tourist-focused leasing models.

- Financing conditions are evolving, with interest rates rising moderately, impacting leveraged acquisition strategies.

That said, Madrid still compares favorably to other capitals in terms of price-per-square-meter, liquidity, and rental stability.

For long-term investors willing to target emerging areas, invest in energy-efficient upgrades, or build managed rental portfolios, the city presents clear opportunities.

Other Market Forecasts & Overviews

Barcelona Real Estate Market Overview & Forecast

Valencia Real Estate Market Overview & Forecast

Seville Real Estate Market Overview & Forecast

Zaragoza Real Estate Market Overview & Forecast

FAQ

Is Madrid a good place to invest in real estate?

Yes—for long-term income and capital growth. It offers strong rental demand, competitive pricing, and consistent appreciation in emerging districts.

Are rental yields in Madrid attractive for investors?

Yes. Yields range from 3.5% to 6.0%, depending on location, property type, and leasing strategy.

Can foreigners buy property in Madrid?

Yes. There are no legal restrictions on property ownership for foreign buyers.

Is the Madrid housing market expected to grow in 2026?

Yes. Prices are projected to rise by 4.5% to 6.0%, especially in gentrifying and well-connected neighborhoods.

Which neighborhoods offer the best investment potential?

Tetuán, Arganzuela, Carabanchel, and Vallecas offer strong rental yields and capital growth opportunities.

Are there rent caps or restrictions in Madrid?

Currently, Madrid has no rent caps, but policy changes are under discussion. Long-term leases remain investor-friendly.

Is short-term rental allowed in Madrid?

Yes—but licensing is required, especially in central districts. Many investors now favor long-term rentals for regulatory stability.