Once known for sun-kissed beaches and a laid-back Mediterranean lifestyle, Limassol is now making headlines for something far less relaxing — its relentlessly rising rents. As the city’s economy expands, so does the hunger for living space, pushing rental prices to levels that would have seemed unthinkable a decade ago. But before you write it off as simply expensive, it’s worth asking the harder question. Are Limassol rents actually unjustified, or do the cold numbers tell a different story?

We’re going to break it all down, looking at Limassol’s property market from both sides of the equation. What tenants are facing, and what landlords actually need to make the math work.

Understanding Limassol’s Real Estate Market

Everything starts with property prices. Limassol’s real estate market has turned into a hotbed for both local and international buyers. And the entry price? Far from modest.

A basic two-bedroom apartment in Limassol now hovers around €300,000, a figure that has surged sharply over the past few years. Just five years ago, that same apartment would have set you back around €240,000, which works out to roughly a 25% price jump in a short window. Much of that climb is fuelled by surging demand, with Limassol pulling ahead of other Cypriot cities at pace. To put it in perspective, the average two-bedroom apartment in Nicosia, Cyprus’s capital, sits closer to €200,000. That’s a 50% premium just for the postcode.

Cyprus Property Index by The Luxury PlaybookSeveral forces are pushing prices higher. Limassol has quietly built itself into a premier business hub, with the Cyprus Statistical Service (CYSTAT) reporting that roughly 75% of the country’s financial services companies are based here. The city’s business-friendly climate makes it a natural magnet for corporates. And beyond the local economy, foreign investment has flooded in. According to the Cyprus Land Registry, overseas buyers accounted for 37% of all real estate transactions in Limassol in 2024, adding consistent upward pressure on prices.

Buyers from Russia, Israel, and the UK are particularly active, drawn by the Mediterranean lifestyle, low tax rates, and a strategic location that bridges Europe and the Middle East. These international buyers regularly pay a premium, which feeds directly into rising valuations. The luxury end of the market tells an even sharper story, with properties along the seafront or at the Limassol Marina routinely exceeding €1 million for larger units and villas.

So what does all of this mean for renters? The logic is straightforward. High property prices translate directly into higher rents. A landlord who pays €300,000 for an apartment needs to service a mortgage, cover maintenance, and pay property taxes. Those costs don’t disappear. They get passed on to you as the tenant.

How Do Landlords Calculate Rent?

Put yourself in the landlord’s position for a moment. You’ve just bought a two-bedroom apartment in Limassol for €300,000. Most investors don’t have that sitting in cash, so a mortgage is the obvious route. In Cyprus, a competitive interest rate sits around 4% if you have a solid banking relationship. At that rate, monthly repayments on a €300,000 loan come out to roughly €1,430, depending on the mortgage term. Over a full year, that’s around €17,160 heading straight to the bank.

But the mortgage is just the start. Layer on top of that property taxes, insurance, regular maintenance, and the occasional repair that always seems to arrive at the worst time. Budget around €3,000 per year for those, and your total annual outgoings climb to roughly €20,160.

Now factor in the return. Serious property investors typically target a 7% to 10% yield to make the numbers worthwhile. Apply a 7% yield to a €300,000 property and you’re looking at around €21,000 per year in rental income. Notice how closely that tracks the combined cost of the mortgage and maintenance. That’s not a coincidence. Property investors across markets work from the same basic equation. It explains why landlords in Limassol need to charge somewhere between €1,750 and €2,000 per month just to break even and pocket a modest return. Anything less, and the property becomes a liability rather than an asset.

And landlords aren’t doing these calculations in isolation. Inflation adds another layer of complexity. Cyprus has seen inflation rise sharply in recent years, eroding the real value of money over time. The €300,000 you invest today won’t carry the same purchasing power in a decade. That’s a big part of why the 7% to 10% yield target exists. Anything below that, and you might as well have left the capital in a high-yield savings account. Add in the natural volatility of the property market, and the math gets even tighter.

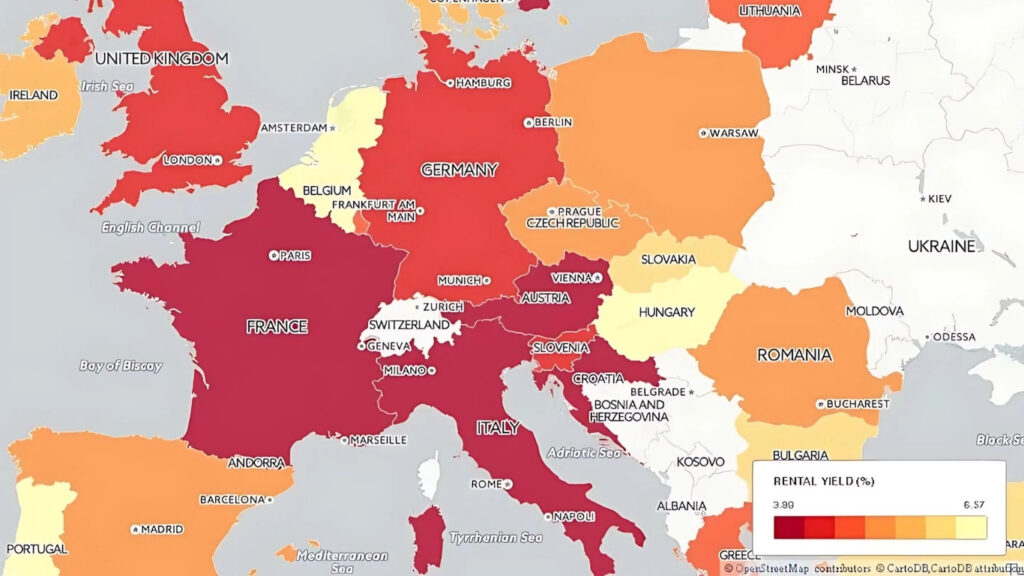

Real Estate Yield: How Does Limassol Compare to Other Cities?

So is a 5% to 7% rental yield in Limassol actually reasonable? To answer that properly, you need to stack it up against some of Europe’s most sought-after investment destinations.

London, UK

Take London. It’s often cited as one of the world’s most expensive real estate markets. But for all that prestige, London’s rental yields tell a sobering story. In prime areas like Chelsea or Kensington, investors are typically looking at yields of just 3% to 4%.

A £1 million property in Chelsea might generate around £30,000 per year in rent, landing at a 3% yield. Even stepping away from the most central postcodes doesn’t move the needle much above 4%, because property prices stay sky-high across the board. That forces London investors to bet heavily on long-term capital appreciation rather than rental income, which is a much riskier game if prices stagnate or correct.

Limassol, by contrast, offers rental yields in the 5% to 6% range, with some high-demand pockets nudging up toward 7%. Property prices here have climbed sharply, but they’re still well below London’s stratosphere, which makes it easier to generate strong rental income relative to what you paid. A €300,000 two-bedroom apartment in Limassol could realistically bring in €1,800 per month, delivering a net yield of around 6% after accounting for foreseeable maintenance costs. For investors who want real cash flow rather than a paper gain sitting on a balance sheet, that’s a compelling proposition.

Barcelona, Spain

Barcelona pulls in enormous international attention thanks to its Mediterranean lifestyle and a growing expat scene. But rental yields there tend to be more moderate. Across the city, yields average out between 4% and 5%. In prime central neighbourhoods like Eixample or the Gothic Quarter, where property prices are steeper, yields often sit closer to 4%. You can find better returns further from the centre, but even those outlying areas struggle to match the consistent 5% to 6% that Limassol delivers.

Barcelona Average price sale (€/m²) by The Luxury PlaybookBrussels, Belgium

Brussels occupies a unique position as the de facto capital of the European Union, giving its real estate market a stable, institutionally driven foundation. But that stability comes with modest returns. Central Brussels typically yields between 3% and 4%, with some outer districts reaching 5%. The market hasn’t seen the same rapid appreciation as Limassol, which keeps yields predictable but leaves little room for upside. If you’re chasing growth and stronger cash flow, Limassol’s more dynamic market starts to look considerably more appealing.

Paris, France

Paris tells a story very similar to London. The prestige of owning property in the French capital is hard to argue with, but the rental yield picture is notoriously thin. In the central arrondissements, yields rarely break 3%, and many properties deliver returns in the 2% to 2.5% range. Investors in Paris are largely playing a long-term capital appreciation game, banking on the city’s global status rather than rental income.

Even in the outer districts, yields rarely push beyond 4%. Stacked against Limassol’s 5% to 6%, the gap is hard to ignore for any investor whose primary goal is generating real rental revenue rather than simply holding a prestigious asset.

Berlin, Germany

Berlin has earned a reputation as something of a sweet spot in European real estate, driven by a property market that has appreciated sharply over the past decade. Yields range from 3% to 4.5%, with neighbourhoods like Kreuzberg and Neukölln offering relatively better returns thanks to strong rental demand. But the German market comes with a significant catch. Strict tenant protection laws and rent caps can seriously limit your ability to grow rental income over time. Even as property values have climbed, those legal constraints keep yields in a fairly narrow band.

Investor’s Perspective

Limassol operates with considerably more flexibility. Landlords can adjust rents in line with actual market demand, without the kind of regulatory ceiling that constrains German landlords. That freedom to respond to the market is a real advantage for yield-focused investors.

The comparison is pretty clear when you lay it all out. According to Knight Frank’s global property research, yield compression in major European capitals has been a consistent trend. Limassol bucks that trend with yields of 5% to 6%, comfortably ahead of London’s 2% to 4%, Barcelona’s 4% to 5%, Brussels’ 3% to 5%, Paris’s 2% to 4%, and Berlin’s 3% to 4.5%. For investors chasing genuine cash flow from rental income rather than just betting on price appreciation, Limassol stands out from the crowd.

The yield advantage isn’t the only thing Limassol has going for it. Rental demand is underpinned by a thriving business environment, with a steady flow of expatriates and international companies keeping occupancy rates high. Property prices, while elevated, haven’t reached the impossible levels of London or Paris, which keeps rent-to-price ratios in more sensible territory. And unlike Berlin or Paris, where rent controls can freeze your income potential, Limassol’s market lets landlords price in line with genuine demand.

That said, higher yields do come with a trade-off you shouldn’t overlook. Cities like London and Paris offer long-term capital stability that Limassol simply can’t match at this stage. They’re deeper, more liquid markets with decades of institutional support behind them. Limassol is a smaller market that leans heavily on foreign investment, which means any shift in investor sentiment, geopolitical turbulence, or economic headwinds could hit property values and rents harder than they would in a larger, more diversified city.

For investors who are comfortable with that risk profile, Limassol genuinely delivers. The combination of rising property values, strong rental demand, and a light regulatory touch allows landlords to capture returns that most European cities simply can’t offer right now. The trade is clear enough: higher yields in exchange for a market that can move quickly in either direction.

The Role of Investors in Maintaining Market Balance

It’s easy to cast investors as the problem when rents climb and housing feels out of reach. But the reality is more nuanced than that. Investors play a genuine structural role in keeping supply and demand in balance. Without them, the market doesn’t just slow down. It can seize up entirely.

Think about what actually happens if investors step back. Without a financial incentive to buy and rent out properties, they won’t. Fewer investors means fewer rental properties on the market. And with fewer properties available, tenants face even more intense competition for what’s left, pushing rents higher on the remaining stock. You end up in a cycle where a lack of investment creates a housing shortage, and a housing shortage creates unaffordable rents. The very outcome people feared from high investor activity ends up being worse without it.

Investors also provide liquidity and actively grow the overall housing stock. They fund new builds, buy older properties and renovate them into rentable homes, and take on the financial risk that comes with ownership. Strip them out of the equation and a large share of new residential development simply doesn’t happen.

And the risks investors take on are real. As the Financial Times has covered extensively, smaller property markets like Limassol can be volatile in ways that large gateway cities are not. If the economy softens, property prices can drop below what was paid. Cyprus’s dependence on foreign capital means that any geopolitical disruption or financial shock abroad can ripple through local valuations faster than most investors expect.

For the market to stay healthy, it has to work for both sides. Landlords need returns that justify the risk they’re absorbing, and tenants need rents they can actually afford. If either side gets squeezed too hard, the whole system starts to crack. That’s why the 5% to 7% yield range matters. High enough to keep serious investors engaged, but not so extractive that it prices out the tenant base that makes those yields possible in the first place.

Is Limassol Rent Really Expensive?

Let’s bring it all together. On the surface, €2,000 a month for a two-bedroom apartment sounds steep. But once you work through the numbers, it starts to make sense. Landlords aren’t plucking figures from the air. They’re pricing based on mortgage repayments, maintenance costs, and the need to generate a return that justifies buying the asset in the first place.

For tenants, that’s cold comfort, especially if you’re planning to rent long-term and watching your outgoings climb each year. But from a pure investment standpoint, those rents reflect what landlords genuinely need to keep their properties viable. Cyprus’s growing international profile is a big part of why the pressure on rental prices shows no signs of easing.

What does this mean for the wider economy? High rents are a signal of a city on the rise, one that’s attracting talent, capital, and ambition. But they also create real pressure for locals and expats who are earning salaries that haven’t kept pace with the cost of living. That tension is one of the defining features of Limassol right now.

What to Expect in the Coming Years

So where does the market go from here? Will rents keep climbing, or is a ceiling somewhere in sight?

There’s no clean consensus. On one side, continued foreign investment and business growth could sustain demand and push rents even higher through 2026 and beyond. On the other, rising interest rates, a global economic slowdown, or regulatory shifts could take some heat out of the market. Bloomberg’s real estate coverage has pointed to similar crosscurrents playing out across Southern European markets.

As Limassol gets more expensive, some businesses and residents will inevitably start looking at more affordable cities elsewhere in Cyprus. That natural pressure valve could cool things down if the price gap becomes too wide to justify.

Whether Limassol rent feels expensive or justified really comes down to where you’re sitting. If you’re a tenant, it almost certainly feels expensive, especially when wage growth isn’t keeping up with the cost of living. If you’re a landlord or investor, those rents are the baseline you need to make the whole exercise worthwhile.

Limassol’s real estate market is ultimately a mirror of its economic momentum. As long as demand keeps outrunning supply, prices will stay elevated. Whether that dynamic is sustainable over the next decade is the real question, and the honest answer is that nobody knows for certain. What you can do is go in with clear eyes and a solid understanding of the numbers.