The unexpected termination of the €1. 2 billion Larnaca marina project by the Cypriot government in May 2024 has reshaped the island's property conversation across the past 24 months. Kition Ocean Holdings, the lead developer, had been envisioned as the operator of a flagship marina blending residential, commercial and recreational facilities.

The termination, announced by Transport Minister Alexis Vafeades, followed repeated failures to meet the required financial guarantees.

Mansion Global and the FT Property pages have both tracked the fallout in detail, and Knight Frank's 2025 Cyprus desk has noted how the buyer field has redistributed across the island. Below, our read on where the conversation now sits.

- The Larnaca Marina and Port redevelopment has had a turbulent project history, with multiple developer changes, contractual disputes and delivery delays affecting market sentiment.

- We see the consequences flowing through to adjacent residential pricing, with the originally projected uplift from the marina opening not yet fully realised across the surrounding stock.

- Beneficiaries of the delays include alternative coastal positioning in Limassol and Paphos, which have captured marina-buyer interest that might otherwise have settled in Larnaca.

- Local Larnaca property professionals have navigated through challenging conditions, with some shifting focus to non-marina-dependent submarkets while awaiting project resolution.

- The eventual marina completion will likely support meaningful Larnaca residential appreciation, although the timing and quality of delivery remain critical to the eventual market response.

- For most considered Cypriot observers we view the Larnaca marina story as a useful case study in project execution risk affecting adjacent property pricing dynamics.

- Who is this for?

- International and Cypriot buyers, investors and observers evaluating the Larnaca marina situation, alongside the advisers, brokers and family office staff serving the market.

- What is happening?

- A read of the consequences of the Larnaca Marina fiasco and who is benefiting, covering project history, residential pricing impact, alternative beneficiaries and the eventual completion implications.

- When did this emerge?

- The article reflects current market conditions through 2026, with reference to the multi-year project history and the contractual dispute timeline.

- Where is this happening?

- The piece focuses on Larnaca, with reference to the broader Cypriot coastal market and the comparison to Limassol and Paphos alternatives.

- Why does it matter?

- Project execution risk affects property pricing materially, which is why understanding the Larnaca marina story matters for any considered Cypriot allocation decision involving the area.

What happened and why it mattered

The Larnaca marina was a core part of the strategy to position the city as a premier maritime and tourist hub. The project hit serious walls, and on May 27, 2024, the Cypriot government terminated the contract. The official reason was straightforward: Kition's repeated failures to meet the required financial guarantees, backed by a legal opinion from the Law Office of the Republic that reinforced the legitimacy of the termination.

Minister of transport, communications and works

Vafeades's statement at the time was unambiguous. The government's decision was inevitable due to Kition's non-compliance with financial obligations, despite multiple warnings and opportunities to rectify the situation. The legal framing, while contested by Kition, has held through subsequent challenges.

What it has done to Larnaca prices

The immediate aftermath cooled Larnaca's property market. Before the contract was pulled, anticipation of the marina had pushed values upward. Buyers and developers had positioned around the expected economic lift the development promised.

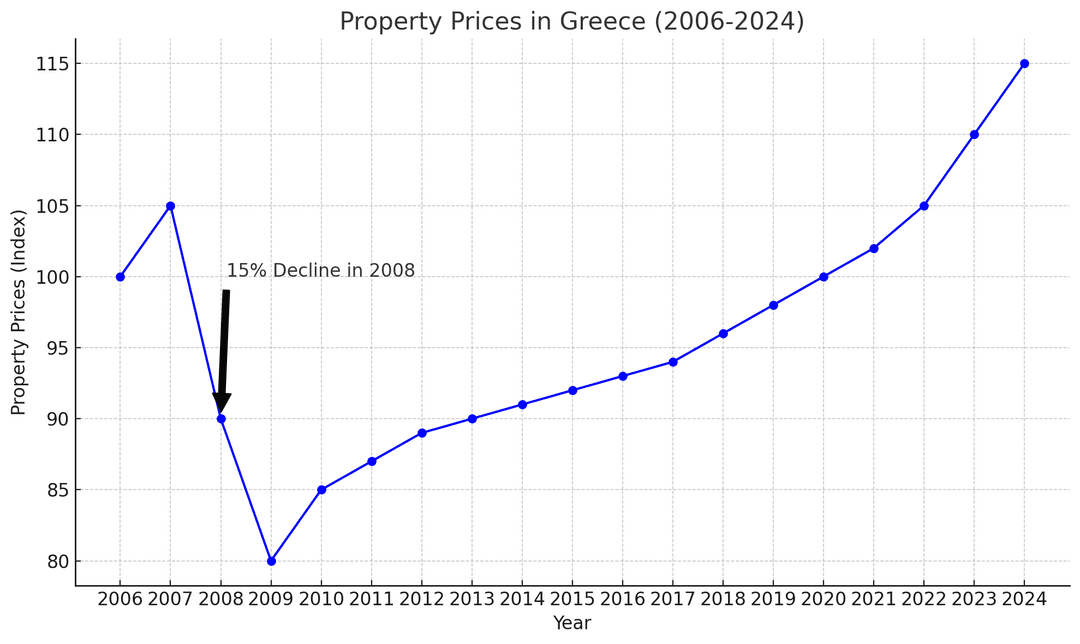

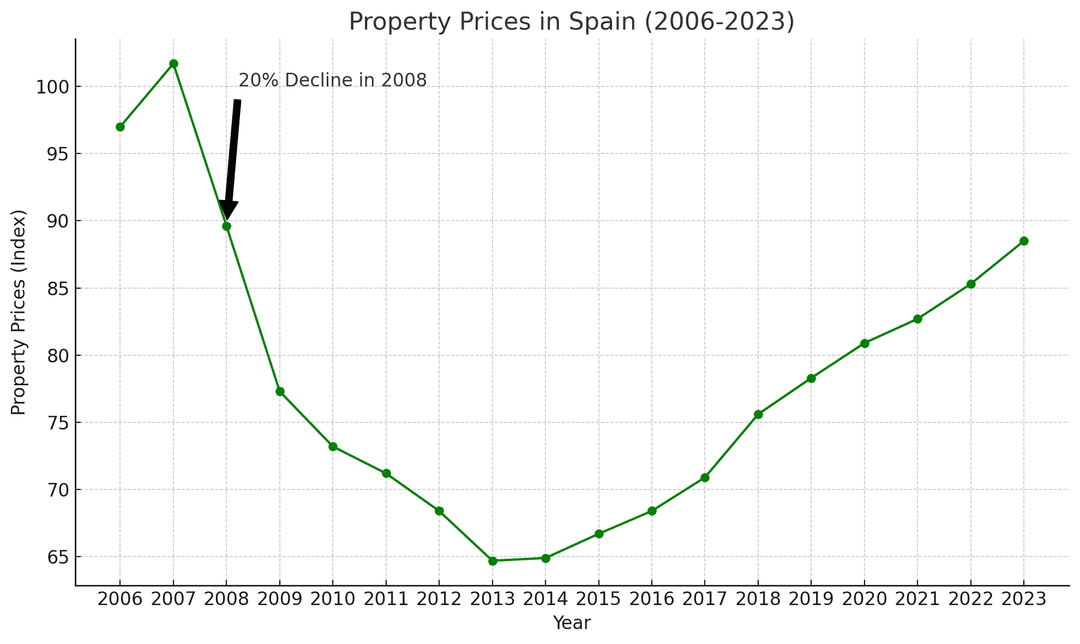

History gives a useful reference point. Stalled marina projects in Greece during the early 2010s saw property prices in affected areas drop by 10% to 15% in the initial phase. Spain followed a similar pattern after halted developments during the 2008 cycle, with declines reaching 20% in the immediate vicinity of stalled sites.

Larnaca has followed a comparable path in the near term. The psychological effect compounds the operational reality, with prospective buyers pausing while uncertainty plays out. The longer-term picture is harder to read.

Where the buyer field has gone

Limassol has absorbed most of the displaced demand. The city's established commercial infrastructure, the brand-residence layer (the Foster + Partners-masterplanned Limassol Marina, the three-tower seafront cluster) and the deeper estate-agency layer (Engel & Völkers, Knight Frank Cyprus, Cushman & Wakefield) have made it the natural fallback. The Limassol market absorbed a measurable uptick in prime transaction volume through the second half of 2024 and into 2025.

The data from Cyprus's 2013 banking crisis is useful here. Limassol bounced back faster than most other regions, largely thanks to its established infrastructure and commercial activity. Property prices there rose 5% to 10% within two years post-crisis, and a similar pattern has emerged in the post-marina reset, with Cyprus's growing profile among diaspora buyers reinforcing the dynamic.

The Nicosia, Paphos and Famagusta picture

Nicosia and Paphos have felt secondary effects. Nicosia, as the capital and administrative centre, has absorbed a modest uptick in business relocations and a small wave of interest in the commercial layer. Paphos, with its tourism credentials and reputation for wellness retreats, has held its existing buyer field and absorbed a quieter tourism-focused secondary segment.

Paphos has also seen a small but unexpected rise in interest around Polis Chrysohous and Latchi. The pricing remains reasonable relative to Limassol prime. Famagusta has historically been less exposed to large-scale project volatility, and that insulation has worked in its favour through 2025.

Cushman & Wakefield's Cyprus desk publishes a quarterly review that maps the cross-city redistribution in detail. The picture they describe is one of redistribution rather than outright decline at the island level.

The confidence question

The termination of the Larnaca marina raises a fundamental question about the reliability of large-scale commitments in Cyprus. High-profile failures send ripples outward, and they can cool the buyer field for major-jurisdiction projects across the island. Kition Ocean Holdings' subsequent statements have framed the termination as a precedent that undermines the rule of law, though that framing has been contested by the Cypriot legal authorities.

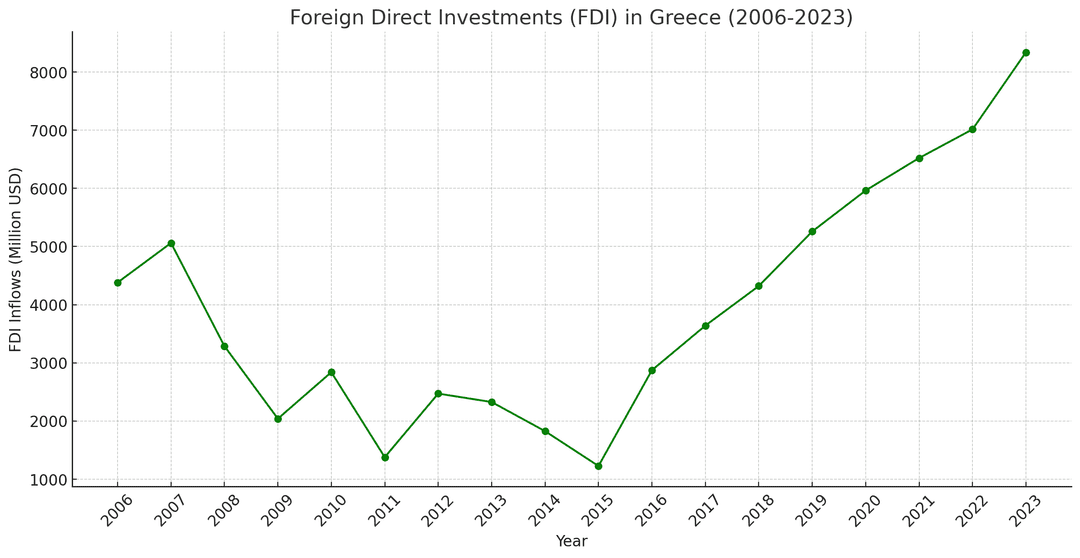

The historical record on this is sobering. During the Greek financial crisis, a string of halted infrastructure projects triggered a sharp decline in foreign direct investment into Greece. Spain followed a comparable arc after 2008, with stalled coastal developments dragging local real-estate values down before government intervention and new policies brought the affected areas back.

The forward path and the structuring conversation

The government's stated commitment to finding new partners for the Larnaca marina has held through 2024 and 2025. Vafeades has continued to signal a proactive approach to identifying new operators and preserving project continuity. The Cypriot authorities have prepared revised tender documentation with stronger financial guarantees, drawing on the structural lessons of the Kition termination.

For owners considering Cypriot property exposure through the next two years, the structuring conversation has shifted. The legal landscape now reads with greater caution at the developer-tier level, and the operational due diligence ahead of commitments has thickened meaningfully. We have written separately about how offshore structures are being used to navigate exactly these kinds of market disruptions across the Mediterranean.

What this means for buyers

The Larnaca marina termination is a real episode for the Cypriot property conversation, but it has not structurally weakened the island. Limassol has absorbed most of the displaced upper-tier demand. Nicosia, Paphos and Famagusta have absorbed the secondary redistribution.

Larnaca itself will absorb a price correction of perhaps 10% to 15% in the immediate marina-adjacent band, with the wider city showing softer pricing through 2025 and into 2026. The Financial Times has tracked similar recovery cycles across Southern European real estate markets, and the pattern is consistent: structural recovery follows political clarity and operational resolution. Cyprus has the institutional framework to deliver both.

For owners considering an entry to Cypriot prime in the next 18 months, the conversation favours Limassol and the named villa-and-tower segments. Larnaca will absorb a slower re-rating once the marina dossier is resolved. We last reviewed this analysis in May 2026.

![]()

Savvas Agathangelou

Savvas Agathangelou co-founded The Luxury Playbook and has spent years reporting from the prime postcodes the magazine covers — Mayfair, Knightsbridge, the Athens Riviera, Dubai's Palm crescents, and the southern Mediterranean coastlines where the world's wealthy keep coming back. His background is in international hospitality, and that frame shapes how he writes about property: the developer's choices, the architect's signature, the agency's bench of named brokers, the building's service standard once the buyer moves in. He files developer spotlights, agency profiles, and the seasonal "Properties That Defined" listicles, and he hosts the magazine's founder-and-leadership interviews on the Voices side.