The U.S. luxury real estate market is entering a period where supply constraints are becoming a defining factor, and the slowdown in construction activity is at the heart of it.

According to the most recent data from the U.S. Census Bureau, residential construction starts dropped to their lowest point since 2020, with luxury developments facing some of the steepest delays due to rising material costs, labor shortages, and stricter zoning approvals.

This is not just a temporary hiccup in building schedules. It’s a structural shift that could shape prices for years to come. In the high-end segment, where you expect exceptional quality and prime locations, fewer new properties means heightened competition for existing listings.

As one of our property consultants recently put it, “In a market where the top 5% of homes already operate under scarcity, even small disruptions in supply can have an outsized impact on pricing power.”

For you as an investor, this slowdown creates a unique dynamic. Scarcity tends to protect and even elevate asset values in the luxury segment. But longer development timelines and increased costs could change the risk-reward equation for those funding new projects.

The result is a market where timing, location, and asset quality matter more than ever before.

Table of Contents

Understanding The Current U.S. Construction Slowdown

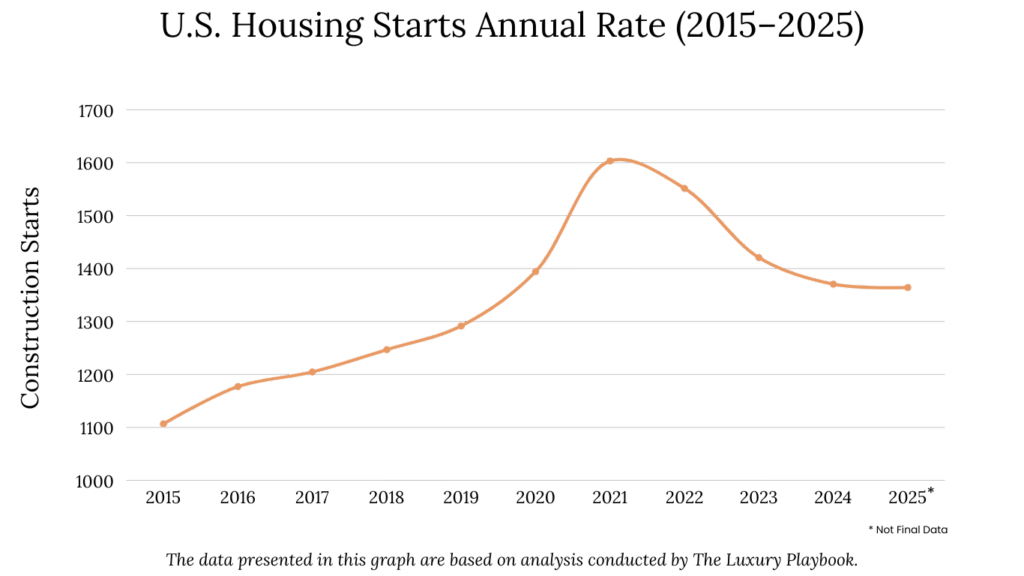

The slowdown in U.S. construction is not limited to one sector, but luxury real estate is feeling the impact in a sharp and immediate way. Data from the U.S. Census Bureau and Dodge Construction Network shows that overall residential building starts have fallen by more than 15% year-on-year as of mid-2026, with high-end developments seeing even steeper declines due to their complexity and financing needs.

Several factors are converging to create this bottleneck. Rising interest rates over the past two years have increased financing costs for developers, making large-scale luxury projects more expensive to fund.

At the same time, construction materials like steel, glass, and imported marble — staples in premium builds — have experienced price increases of 20 to 30% compared to pre-pandemic averages. Skilled labor is scarce, particularly in high-demand coastal and urban markets, pushing wages higher and extending project timelines.

There’s also a regulatory dimension. Prime locations for luxury housing often come with tighter zoning rules, environmental reviews, and community pushback, all of which add months and sometimes years to approval processes.

According to a recent report from the National Association of Home Builders, luxury projects in major metros now take 30 to 40% longer to reach completion compared to a decade ago.

This combination of economic and regulatory pressures is not only slowing the pipeline of new luxury homes but also reshaping development strategies. Many builders are scaling back on speculative projects, focusing instead on smaller, ultra-custom developments where buyer commitments are secured before construction even begins.

How Reduced Luxury Housing Supply Influences Pricing

In real estate, scarcity is one of the most powerful price drivers, and the U.S. luxury housing market is a textbook example of this principle in action. With fewer new properties entering the market, the limited inventory of high-end homes is creating a competitive environment where buyers like you are often willing to pay a premium to secure the right property.

According to Redfin’s 2026 Luxury Market Report, the number of available luxury listings in major metropolitan areas is down 18% year-over-year, while demand from affluent buyers — particularly those relocating from other states or countries — stays steady.

This imbalance has already pushed average luxury home prices in markets like Miami, Los Angeles, and Manhattan up by 6 to 10% in the past 12 months, even as broader housing markets have seen slower growth.

The psychology of scarcity plays a major role here. In luxury segments, buyers are less price-sensitive and more driven by uniqueness, prestige, and location exclusivity. When inventory drops, these factors become even more amplified.

As Jonathan Miller, president of Miller Samuel Inc., puts it, “Luxury buyers aren’t just purchasing a property — they’re purchasing a position in a market that may not give them another opportunity anytime soon.”

This pricing pressure is especially pronounced in ultra-prime areas. Think beachfront estates in Palm Beach, penthouses overlooking Central Park, or wine estate properties in Napa Valley. In these niche segments, even a small reduction in available listings can trigger aggressive bidding, driving final sale prices far above initial asking levels. If you’re working with an independent real estate analyst, now is exactly the time to lean on that expertise.

The result is a market where limited new supply is not only sustaining high prices but, in some cases, accelerating appreciation — making timing and strategic market selection critical for capturing long-term value.

Regional Markets Most Affected By The Slowdown

The impact of slower construction isn’t uniform. It’s showing up most clearly in a handful of luxury hubs where new supply is harder to bring to market, and where deep-pocketed buyers keep demand resilient.

New York City and Manhattan in particular tell a striking story. Luxury inventory in Manhattan fell sharply this spring even as non-luxury stock rose, a clear sign the pipeline at the top end is tight. Douglas Elliman’s Q2 2026 report shows luxury listing inventory down 21.2% year over year, while non-luxury inventory increased 9.1%. That scarcity helped push luxury pricing to new highs in mid-2026. A key structural driver here is the post-421a environment. As legacy sites get built out and developers wait on new incentive frameworks, the ultra-prime pipeline stays constrained.

South Florida tells a more nuanced story. Palm Beach’s top tier is tight, with Q2 2026 luxury inventory dropping 18.4% to just 40 listings, reinforcing pricing power for ultra-prime waterfront and estate properties. Miami is different. Years of robust development mean some segments, especially those priced between $6M and $10M and above $10M, show rising months of supply even as days-on-market stretch. That’s proof that past building booms can blunt the price effects of today’s slowdown.

Los Angeles, specifically the prime Westside and Malibu corridors, is seeing new high-end supply pinched by insurance availability, wildfire risk, and higher carrying costs. Sales volumes in LA County fell 7.9% year over year in May 2026 even as prices edged up, reflecting selective demand chasing scarce, well-insured properties. The wildfire aftermath, with insured losses estimated above $30 billion, is lengthening rebuild timelines and complicating new project underwriting, keeping near-term supply tight in coveted coastal zones.

The nationwide picture reinforces all of this. U.S. housing permits declined again in early 2026, with single-family permits down 4.7% year-to-date through April and multifamily off 1.5%, while 12-month residential starts were down 1%. Both figures point to a leaner pipeline over the next 12 to 24 months. In the luxury segment, where projects are complex, capital-intensive, and zoning-constrained, those headwinds translate into fewer completions and a stronger floor under prices in the most supply-constrained zip codes.

Buyer And Investor Behavior In A Low-Supply Luxury Market

When luxury housing supply tightens, buyer and investor behavior shifts in predictable yet telling ways. In 2026, these dynamics are playing out across key U.S. luxury hubs, and the slowdown in construction is amplifying every one of them.

Affluent buyers, especially those in the $5 million-plus bracket, tend to prioritize scarcity above almost everything else. In Manhattan, where Douglas Elliman reports a 21.2% drop in luxury inventory year-over-year, competitive bidding has returned in prime co-op and condo segments.

Buyers like you are less willing to wait for new developments, knowing delivery timelines are stretching further out. Instead, they’re snapping up existing turnkey properties, often with all-cash offers to sidestep financing delays entirely.

Institutional and family office investors are also showing heightened interest in trophy assets. In Palm Beach, the median luxury sale price climbed nearly 19% year-over-year, fueled in part by wealth migration from high-tax states. Many buyers are approaching acquisitions with a dual lens, seeking lifestyle benefits now and potential capital appreciation later.

Meanwhile, in markets like Los Angeles, buyer caution coexists with urgency. High-net-worth individuals are still active, but they’re more selective, prioritizing properties with strong insurability and proven liquidity on resale. Off-market transactions have become more common in ultra-prime neighborhoods, allowing deals to happen discreetly without inflating public listing data.

Overall, the psychology is shifting toward locking in rare assets early. Buyers and investors alike are increasingly treating luxury real estate not only as a status symbol, but as a finite commodity, one whose replacement cost is rising faster than most other asset classes.

This mindset is likely to persist as long as construction pipelines stay tight and borrowing conditions stay challenging.

Impact On Luxury Real Estate Developers

For luxury real estate developers, the slowdown in U.S. construction is creating a mix of challenges and opportunities. Reduced competition from new builds means that existing or nearly completed projects face less supply pressure when they hit the market. But extended timelines, higher costs, and regulatory hurdles are eroding margins and stretching balance sheets.

Material costs are a significant pain point. According to the U.S. Bureau of Labor Statistics, construction input prices for high-end finishes such as imported marble, custom millwork, and specialty glass have risen by more than 12% since 2023. Labor is another constraint. Luxury projects often require highly skilled craftsmen, and shortages in these trades can push completion dates back by months.

For developments in markets like Miami, delays are compounded by permitting bottlenecks and stricter hurricane resilience requirements.

Developers are responding in several ways. Some are scaling down unit counts or pivoting toward ultra-prime, lower-volume builds that command higher margins per square foot. Others are entering joint ventures with institutional capital partners to share risk and secure funding despite higher interest rates.

In markets like Aspen and Malibu, developers are increasingly pre-selling properties before breaking ground, leveraging the scarcity narrative to lock in high-net-worth buyers early. Understanding the difference between real estate agencies and developers matters here, especially if you’re evaluating where to place capital in a constrained market.

Long-Term Price Outlook for U.S. Luxury Properties

Looking ahead, the long-term price trajectory for U.S. luxury real estate is likely to stay upward, but with important nuances depending on location, macroeconomic conditions, and buyer demographics. The current construction slowdown has effectively reduced the pipeline of new luxury homes, which means that even if demand cools slightly, supply constraints will keep upward pressure on prices.

Historical patterns suggest that in high-demand markets such as New York, Miami, Los Angeles, and Aspen, limited supply often leads to above-average annual appreciation rates, sometimes exceeding 5 to 7% in premium neighborhoods. The ultra-prime segment, which includes waterfront estates, branded residences, and architecturally significant properties, could see even stronger performance due to their rarity and global appeal.

That said, this bullish outlook is not without potential headwinds. If interest rates stay elevated for several years, buyer financing costs could weigh on transaction volumes, particularly in secondary luxury markets. Any major macroeconomic shock, whether from geopolitical instability, changes in tax policy, or shifts in wealth distribution, could temporarily slow appreciation even in the most resilient markets.

The global buyer base also plays a critical role in price sustainability. Wealth migration trends, particularly from Asia and the Middle East, have supported strong pricing in cities like Miami and Los Angeles. As global wealth keeps expanding, especially among younger high-net-worth individuals, prime U.S. real estate is expected to stay a core part of their asset allocation strategies. This mirrors broader trends seen in other fast-moving luxury property markets, including the $759B UAE property boom reshaping luxury real estate globally.

As one senior analyst at Knight Frank recently noted, “Luxury property isn’t just about location anymore — it’s about scarcity, branding, and security. In a world with fewer prime homes coming to market, these factors become powerful price drivers.”

If construction stays slow through 2026 and beyond, it’s reasonable to expect that the top 5% of U.S. luxury homes could outperform the broader housing market in both price stability and capital appreciation.

Risks To Consider Before Investing in Luxury Real Estate Now

While the long-term outlook for U.S. luxury real estate stays promising, you should know that even this resilient asset class carries real risks, particularly in a market where supply is constrained and prices are already high.

One of the primary concerns is interest rate volatility. Although many luxury buyers purchase with cash, elevated borrowing costs can still influence broader market sentiment and slow transaction volumes. If rates rise further or stay high for an extended period, it could delay sales and pressure sellers to adjust pricing expectations in certain markets.

Economic downturns also present a challenge. Luxury real estate is less sensitive to recessions than mid-market housing, but it is not immune. During periods of economic uncertainty, high-net-worth buyers often become more selective, focusing on the rarest and most desirable properties while stepping back from speculative purchases. This can lead to a slowdown in appreciation, especially for luxury homes without unique location or design advantages.

Another risk worth watching is overvaluation. In markets that have experienced rapid price growth over the last few years, such as Miami, Austin, and Scottsdale, values may have outpaced the intrinsic long-term fundamentals. If demand softens, these markets could see sharper corrections than more established luxury hubs.

Geopolitical and regulatory changes should also be factored into your thinking. Policies affecting foreign ownership, property taxes, and capital gains can shift the dynamics of certain cities almost overnight. Increases in mansion taxes or new restrictions on non-resident buyers could limit demand from international investors, a critical segment in many luxury markets.

And then there’s liquidity risk, which is an inherent feature of high-end real estate. Selling a $20 million waterfront estate often takes far longer than selling a mid-market home, particularly if the global economy is under pressure. That makes timing and market entry strategy crucial for preserving your returns.