After years of dominating the housing conversation, home flipping is finally losing momentum across the United States. Recent data from ATTOM shows that flips accounted for only 8% of all home sales in early 2026, down from more than 10% at the same time the year before.

The slowdown marks a turning point for a strategy that once promised fast returns but is now being squeezed by tighter financing, higher renovation costs, and cooling demand in overheated markets.

This shift matters because flipping has been more than a niche investment strategy. It shaped supply, influenced prices, and altered affordability in neighborhoods across the country. When flippers were buying aggressively, competition for entry-level homes pushed out first-time buyers, while a steady flow of renovated properties added to overall supply.

Now, with activity slowing, the market is adjusting in ways that affect investors, end-users, and the overall housing cycle.

What you are beginning to see is not just a short-term dip in flipping activity but a broader reset in the US housing market.

As one of our Real Estate Analysts recently noted, “The decline in flips tells us that easy profits are gone, and that the market is recalibrating toward longer-term investment models.”

The implications are wide-ranging, from how homes are priced to who is driving demand. And they may reshape real estate in the US for years to come. If you want the full picture of where the US market stands right now, the US Real Estate Market Overview is worth your time.

Table of Contents

Why Home Flipping Is Slowing Down in 2026

The cooling of the flipping market has been building for some time, and by 2026 the pressures have become too large to ignore. The most immediate factor is the cost of borrowing. With mortgage rates still hovering around 6.5% to 7%, financing short-term purchases has become far more expensive than during the low-rate years when flipping thrived.

Many flippers rely on hard-money loans with even higher rates, often in the double digits, making quick resales much less profitable.

At the same time, renovation costs have surged. Materials that were already expensive during the pandemic have stayed elevated, and skilled labor shortages keep pushing wages higher. According to the National Association of Home Builders, construction labor costs rose by nearly 4% in 2024 alone, squeezing margins for investors who depend on efficient, predictable rehab timelines.

What once could be done quickly and cheaply is now slower, costlier, and riskier.

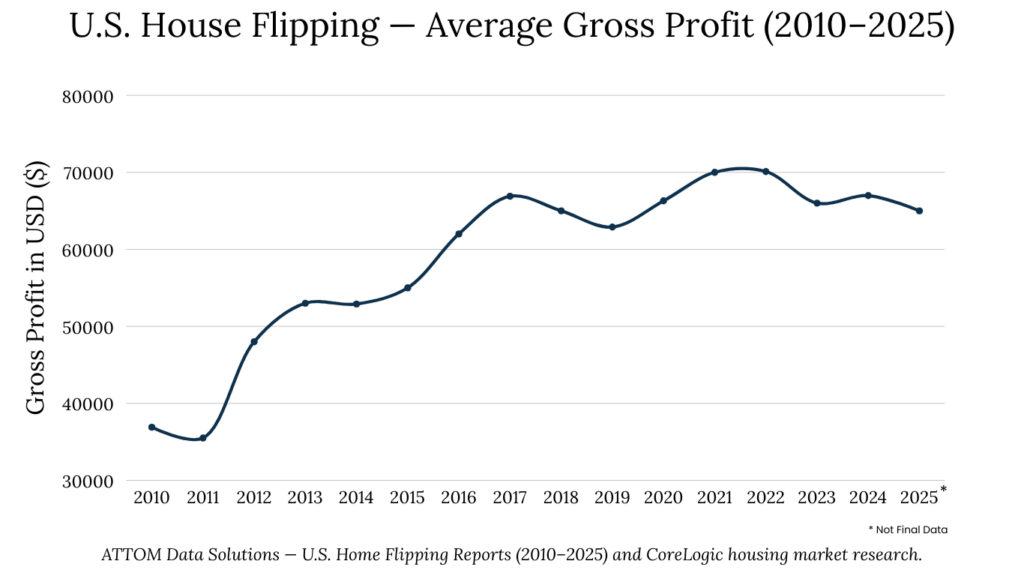

Shrinking profit margins are the natural result of these twin pressures. ATTOM data shows that the average gross profit on a flip in late 2024 fell to just under $67,000 per property, the lowest in nearly five years.

When those profits are adjusted for carrying costs, financing, and renovations, many flippers are seeing net returns that barely justify the effort. That is exactly why both small-scale investors and larger operators are pulling back at the same time.

Taken together, these forces make it clear that the flipping model, once seen as a straightforward way to generate double-digit returns, is no longer a sure thing.

For many investors, the risks now outweigh the potential rewards, prompting a serious reevaluation of strategies and contributing to the broader reset unfolding across the housing market.

Impact of the Slowdown on US Housing Supply

The decline in flipping is not only reshaping investor returns. It is also having visible effects on housing supply. When flipping activity was strong, renovated properties regularly came to market, often in entry-level price brackets. With fewer investors buying, updating, and reselling homes, the pipeline of move-in-ready inventory is shrinking.

According to ATTOM, completed flips fell by nearly 15% year-over-year in early 2025, reducing the number of homes available for buyers seeking turnkey options.

In markets like Phoenix and Las Vegas, where flipping was once a dominant force, the slowdown has led to a buildup of older housing stock that is not being renovated at the same pace. In contrast, Midwestern markets such as Cleveland or Indianapolis, where profit margins are still relatively healthy, are seeing far less disruption.

The uneven geography of the decline means affordability pressures vary widely, depending on how much local markets relied on flippers to refresh aging inventory.

On one hand, less investor competition at the lower end of the market creates an opening for you as an end-user, since fewer all-cash offers are pushing prices up. On the other hand, the reduced supply of updated homes means many buyers are left choosing between higher-priced new construction and older homes that need costly repairs.

This dynamic highlights how deeply flips were woven into the housing ecosystem. They not only created profits for investors but also shaped the buying experience for households across the country.

As the pace of flipping slows, the US housing supply is beginning to reflect a more natural balance, less influenced by speculative activity. But that balance comes at a cost. Fewer renovated homes are in circulation, and a greater burden falls on buyers to either pay for new construction or invest in renovations themselves.

How Falling Flip Activity Affects Home Prices

The slowdown in flipping is also starting to influence price dynamics across the housing market. In the years when flips were booming, investor competition often pushed up prices, especially in lower-cost neighborhoods where first-time buyers were already struggling to compete. With fewer flippers making aggressive bids, that upward pressure is beginning to ease.

According to Redfin, the rate of home price growth in markets with historically high levels of flipping slowed by nearly two percentage points in 2024, suggesting that the cooling trend is already visible.

In some metro areas, especially those that overheated during the pandemic, the absence of flipping is creating stabilization rather than outright declines. In Austin and Phoenix, two markets where flipping once accounted for more than 12% of all sales, home prices have leveled off after years of double-digit growth. Instead of continuous spikes, buyers and sellers are now facing more predictable conditions, which could restore a real degree of balance to local markets.

Other regions are seeing more complex outcomes. In parts of the Midwest, where affordability has stayed stronger, the reduction in flips is limiting the number of renovated homes available for sale. Prices for move-in-ready homes have stayed resilient, while older, unrenovated properties are lagging behind.

The divergence highlights how flipping not only influenced pricing but also created two tiers of inventory, renovated homes that commanded premiums and untouched stock that sold for less.

Taken together, these trends show that the decline in flipping is acting as a stabilizer in overheated markets and a divider in more balanced regions.

For investors, this signals a real shift. Easy appreciation driven by speculative demand is fading, and price movements are now more tied to local fundamentals like wages, migration, and long-term supply. If you are thinking about where to put capital next, understanding whether buying to rent still makes sense is a smart place to start.

The Role of Institutional and Individual Investors in the Reset

The reset in the housing market is being shaped not only by broader economic conditions but also by who is driving demand. During the peak of the flipping boom, both individual entrepreneurs and large institutional players were active, often competing in the same neighborhoods. Now, as returns compress, the paths these two groups are taking are starting to diverge.

Institutional investors, who once dipped into flipping as part of their real estate strategies, are shifting toward more stable income streams. Many large funds have pivoted to build-to-rent communities or long-term single-family rentals, where cash flow is more predictable and less exposed to short-term market cycles.

Companies such as Invitation Homes and American Homes 4 Rent have expanded their rental portfolios, a clear signal that institutional capital is less interested in short-term flips and more focused on scalable, recurring income. Bloomberg has covered this institutional pivot in depth, and the trend is only accelerating.

Individual investors face different pressures. Smaller flippers, often reliant on higher-cost loans, have been the most exposed to shrinking margins. Many of them are stepping back from the market or exiting altogether.

Seasoned operators with access to cash and long-standing contractor relationships are better positioned, but even they are adjusting strategies. The focus is shifting to selective projects in markets with stronger fundamentals rather than spreading capital across multiple speculative buys.

The shift in participation is changing the profile of demand in US housing. With institutions focusing on rentals and smaller investors pulling back, end-users and long-term landlords are regaining some ground in markets that had been dominated by short-term speculation.

This change reinforces the idea that the housing market reset is not only about prices or supply, but also about the people and institutions steering capital. The decline of flipping is accelerating a broader realignment, where long-term strategies are gaining ground and short-term speculation is fading. You can see a similar dynamic playing out when you look at how elite investors are protecting and growing capital in volatile markets.

Opportunities Emerging From the Flip Market Decline

The retreat of home flippers signals the end of easy profits. But it is also creating new opportunities for investors willing to adapt. As speculative buying fades, less competition in certain segments of the market is opening space for alternative strategies that emphasize stability and long-term value rather than quick gains.

One of the clearest growth areas is build-to-rent housing. With homeownership still out of reach for many households due to high mortgage rates and affordability challenges, demand for rental homes stays robust.

Institutional investors have already recognized this trend, with the National Rental Home Council reporting a 12% increase in build-to-rent activity in 2024. Smaller investors who pivot toward long-term rentals can also benefit, especially in markets where strong job growth pairs with tight housing supply.

Another opportunity comes from the easing of competition for entry-level homes. During the height of the flipping boom, first-time buyers often found themselves priced out by all-cash offers from investors. With many flippers stepping back, you now have more negotiating power as an end-user, and buy-and-hold investors are better positioned to acquire properties without bidding wars.

This shift could strengthen rental yields and stabilize acquisition costs for landlords who take a patient approach.

For investors still interested in flipping, the current environment rewards skill and selectivity rather than volume. Those with deep local knowledge, established contractor networks, and access to cheaper capital can still find profitable deals in specific metros where housing demand stays strong. The Financial Times has noted that disciplined, well-capitalized operators are actually gaining market share as weaker flippers exit.

Taken together, these developments show that the decline of flipping is less the end of opportunity and more a redirection of capital. The market is moving away from short-term speculation and toward models that prioritize cash flow, tenant demand, and long-term appreciation. For investors who can adapt, the reset is not a setback. It is an opening.