As 2025 unfolds, the financial environment presents investors with both complexity and opportunity. Market cycles are shifting more rapidly, inflationary pressures remain a central concern, and geopolitical dynamics are influencing asset behavior in unprecedented ways. In this volatile economy, the concept of choosing your ideal asset allocation strategies has never been more vital. It is not merely a matter of dividing capital across investment categories—it is a strategic discipline that shapes the very architecture of wealth creation and preservation.

Investors today are confronted with a universe of choices: equities that range from stable dividend-payers to speculative growth stocks, bonds affected by central bank policy pivots, alternative assets like real estate and private equity, and an increasingly mature digital asset ecosystem. Navigating this expanse requires not only insight but also structure. And that is precisely what asset allocation offers—a framework to align capital with both risk appetite and long-term objectives.

The key to mastering asset allocation in 2025 lies in understanding the different methodologies available and knowing how to apply them under current market conditions.

Table of Contents

What Is Asset Allocation

At its core, asset allocation refers to the disciplined process of distributing an investor’s capital among different asset classes—such as equities, fixed income, cash equivalents, real estate, commodities, and alternatives—to achieve a balance between risk and reward. It is the most fundamental principle of portfolio construction and arguably the most influential determinant of long-term investment outcomes.

Unlike stock picking or market timing, asset allocation focuses on how much capital is placed in each type of investment, based on individual goals, time horizons, and risk tolerances. The idea is straightforward: different assets perform differently under various economic conditions.

When executed correctly, asset allocation reduces volatility, smooths returns, and protects against systemic risks.

Numerous studies over the past two decades have reinforced the significance of this strategy. Research has consistently shown that over 90% of a portfolio’s long-term performance variability is driven by asset allocation decisions, rather than the selection of individual securities.

The asset allocation process typically begins with a detailed investor profile. This includes understanding one’s financial goals—whether they involve capital preservation, income generation, or aggressive growth—as well as liquidity needs and psychological thresholds for market swings. From there, investors or advisors assign percentage weightings to various asset classes, adjusting them as needed based on life events, market movements, or shifts in macroeconomic outlook.

In 2025, asset allocation takes on even greater complexity. With interest rates remaining elevated, global equities displaying sector-specific divergence, and alternative assets offering new avenues of return, investors must be deliberate and agile. Furthermore, access to institutional-grade strategies, such as private credit and real assets, is increasingly available to individual investors, necessitating a more nuanced approach.

Modern asset allocation is no longer limited to just stocks and bonds. It is about engineering a portfolio that is both resilient and responsive, capable of withstanding shocks while seizing growth across a range of market scenarios

Strategic Asset Allocation

Strategic asset allocation represents the cornerstone of long-term investing. It is a disciplined, structured approach in which an investor sets target allocations for various asset classes—such as equities, bonds, real estate, and cash—and maintains them over time, regardless of market volatility. The philosophy underpinning this strategy is simple yet powerful: over the long haul, markets reward consistency and patience more than reactionary behavior.

In 2025, strategic asset allocation remains highly relevant, particularly for investors focused on wealth preservation, retirement planning, or generational wealth transfer. Its effectiveness lies in its emphasis on long-term capital markets assumptions, rather than short-term fluctuations. For instance, an investor might adopt a model allocation of 60% equities, 30% fixed income, and 10% alternatives, based on expected risk and return projections across these categories.

This approach requires periodic rebalancing, typically on a quarterly or annual basis. When one asset class outperforms—such as equities during a bull market—it may exceed its original allocation. Strategic asset allocation dictates that the portfolio be realigned to its initial targets, locking in gains and reestablishing risk balance. This practice reinforces discipline and prevents the portfolio from becoming overexposed to a single asset class.

Statistically, portfolios constructed using a strategic allocation framework have demonstrated less volatility and more consistent returns over time. For example, between 2014 and 2024, portfolios following a classic 60/40 equity-bond split returned an annualized average of 6.5%, with a standard deviation notably lower than portfolios attempting to time markets.

Even in 2022’s downturn, rebalanced strategic portfolios recovered faster due to their structured nature.

A significant advantage of strategic allocation is its immunity to behavioral biases. Investors often succumb to fear during downturns or overconfidence during rallies, both of which can derail performance. Strategic allocation, by design, removes emotion from the equation and replaces it with a rule-based framework.

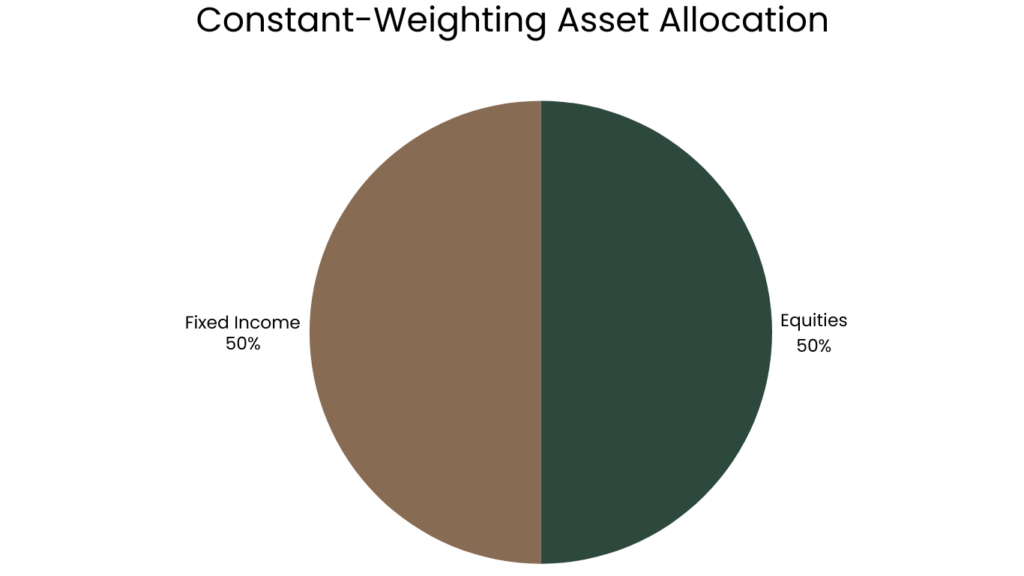

Constant-Weighting Asset Allocation

Constant-weighting asset allocation shares foundational similarities with the strategic approach, yet introduces a more responsive mechanism through regular rebalancing to fixed target weights. The essence of this method lies in maintaining a predetermined allocation—regardless of market movements—by continually adjusting the portfolio back to its original proportions.

While strategic allocation might tolerate longer intervals between rebalancing events, constant-weighting is inherently more dynamic, often requiring attention quarterly or even monthly.

Consider a portfolio set at 50% equities and 50% bonds. Should equities outperform and shift the balance to 60/40, the investor systematically sells a portion of equities and reallocates the proceeds into bonds. This behavior not only ensures risk levels remain in check but also inherently enforces a buy-low, sell-high discipline, as investors are routinely taking profits from outperforming sectors and reinvesting in undervalued areas.

This approach is especially useful in volatile or sideways-trading markets, where short-term movements can significantly distort asset weightings. As global markets contend with fragmented sector recoveries, inflationary pulses, and rapid shifts in monetary policy, constant-weighting allows investors to consistently capture opportunities without attempting to forecast macroeconomic events.

This method has also gained popularity with institutional investors and high-net-worth individuals, who benefit from the risk-adjusted performance improvements it can deliver. Research shows that portfolios rebalanced on a monthly constant-weighting basis can outperform passive strategies by 0.5% to 1.5% annually, especially during periods of elevated volatility.

However, the strategy is not without its trade-offs. Constant rebalancing may incur higher transaction costs, particularly for portfolios with numerous holdings or for investors operating within taxable accounts. As such, successful implementation requires a balance between discipline and cost-efficiency, often facilitated by tax-aware portfolio management tools or automated investment platforms that optimize rebalancing thresholds.

In the current economic cycle, where market dispersion remains high across geographies and asset classes, constant-weighting asset allocation offers a compelling way to maintain strategic intent while dynamically capitalizing on price fluctuations.

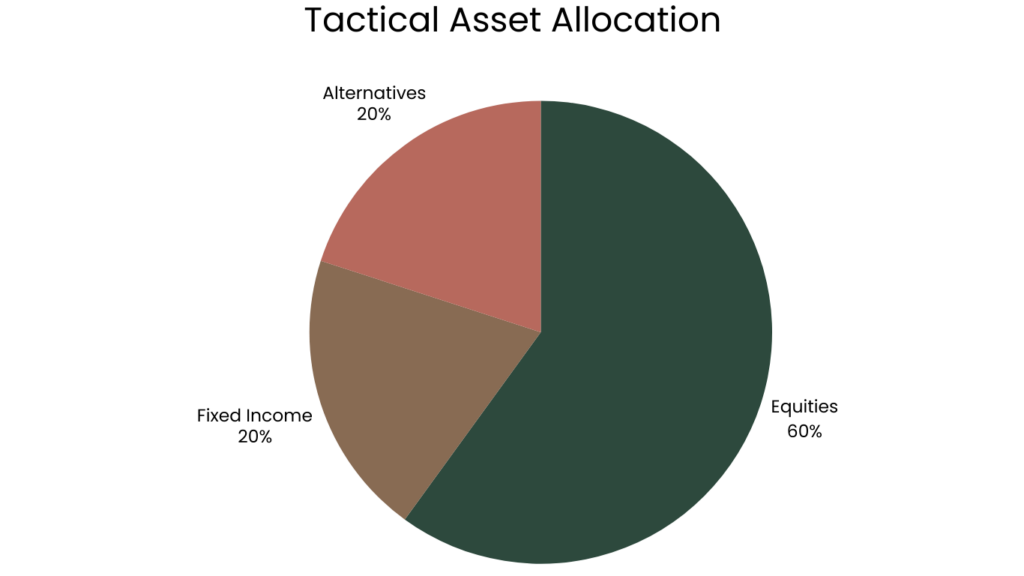

Tactical Asset Allocation

Tactical asset allocation represents a more flexible, active approach to portfolio management. It allows investors to deviate from their long-term strategic allocation to take advantage of short- to medium-term market opportunities. Unlike constant-weighting, which seeks to maintain a set structure, tactical allocation embraces calculated shifts based on macroeconomic trends, market valuations, and technical indicators.

In essence, it merges the stability of strategic planning with the adaptability of market timing—though the latter is executed within disciplined risk parameters.

In 2025, this strategy is gaining renewed attention as investors confront uneven global growth, regional inflation divergence, and sector-specific rotation. With central banks adjusting rates at different paces and certain economies entering recession while others expand, tactical asset allocation enables investors to capitalize on cyclical dislocations.

For example, overweighting energy equities during a commodities supercycle or underweighting long-duration bonds in anticipation of interest rate hikes can significantly enhance returns.

Institutional research suggests that portfolios incorporating tactical tilts—within a 5% to 20% band from the core allocation—have historically outperformed purely passive portfolios during transitional market periods. In a 2024 study, multi-asset portfolios employing tactical overlays outperformed their static counterparts by an average of 2.1% annually over a 10-year horizon, particularly during periods of economic inflection.

However, tactical allocation demands deep market insight, strong analytical frameworks, and emotional discipline. It can easily become counterproductive if driven by sentiment or overreaction. As such, it is most effective when supported by quantitative models and fundamental macroeconomic research, often managed by professional advisors or experienced investors with a keen understanding of market dynamics.

A practical example of this in 2025 involves reallocating capital from overvalued U.S. technology stocks to emerging market debt, where favorable currency valuations and central bank easing are creating tailwinds. Another example includes temporarily increasing exposure to floating-rate securities or real asset funds in anticipation of persistent inflationary pressure in specific regions.

Tactical asset allocation is not intended to replace a long-term strategy but to enhance it through selective and time-bound deviations.

For investors seeking a performance edge while retaining a diversified core, this approach offers an opportunity to outperform benchmarks—provided the timing, research, and execution are precise.

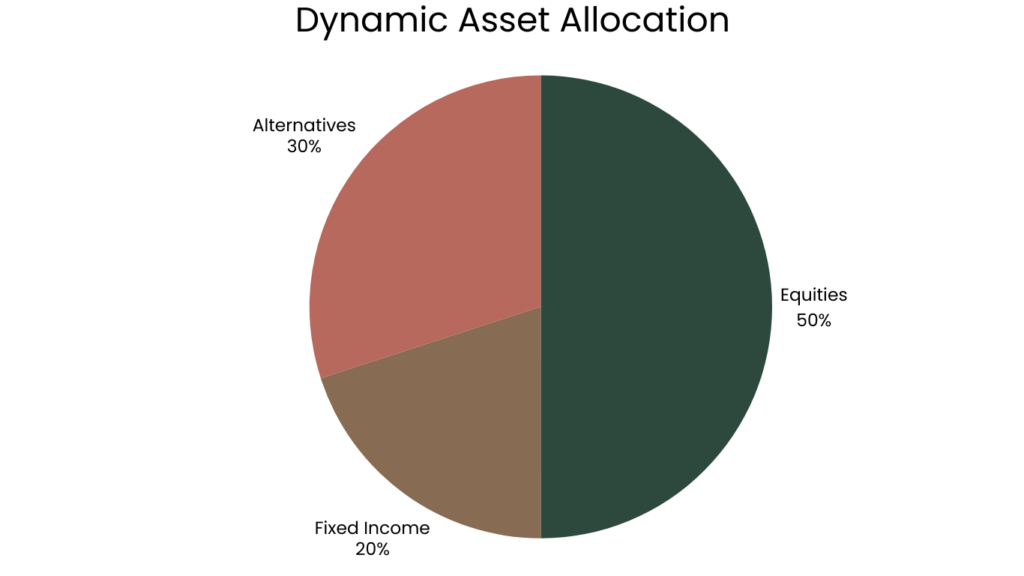

Dynamic Asset Allocation

Dynamic asset allocation takes a fully adaptive approach to portfolio management, continuously adjusting exposure to asset classes based on changing market conditions, economic indicators, and risk assessments. Unlike strategic or constant-weighting models that adhere to preset targets, dynamic allocation is fluid and responsive, allowing for substantial reallocation across assets in real time.

At the heart of this strategy is the belief that asset class performance is cyclical, and that proactive adjustments—when done methodically—can mitigate downside risk while enhancing upside potential. A dynamic asset allocator may shift from a high equity exposure in a bull market to a defensive stance emphasizing fixed income, commodities, or cash equivalents during a downturn.

These moves are not tactical in the short-term sense but are often made with a medium-term horizon, informed by both quantitative models and macroeconomic analysis.

In the current climate, where investors must contend with interest rate uncertainty, inflation persistence, and geopolitical volatility, dynamic allocation is gaining traction among institutional funds, family offices, and high-net-worth individuals. For instance, several global asset managers have shifted significant allocations toward infrastructure, private credit, and low-duration fixed income, responding to both tightening credit cycles and renewed interest in real asset exposure.

Data supports the efficacy of this method in volatile periods. A 2024 performance review of dynamic multi-asset portfolios showed that those managed with systematic reallocation frameworks achieved annualized returns of 7.8% with lower drawdowns, compared to static portfolios of similar risk profiles.

These outcomes are particularly attractive in 2025, where traditional 60/40 models are being challenged by structural changes in both equity and bond markets.

Dynamic allocation also offers investors a hedge against behavioral biases, as the framework is typically guided by pre-established signals rather than discretionary decision-making. Many dynamic portfolios rely on momentum indicators, earnings revisions, valuation multiples, and macroeconomic data, such as inflation surprises or interest rate spreads, to inform asset shifts.

One of the most compelling aspects of dynamic allocation is its ability to integrate non-traditional asset classes, such as hedge funds, real assets, and even digital assets, based on prevailing risk-return expectations.

For example, in early 2025, some dynamic strategies began incorporating tokenized real estate funds and yield-bearing crypto instruments, responding to increased investor interest and regulatory clarity in these markets.

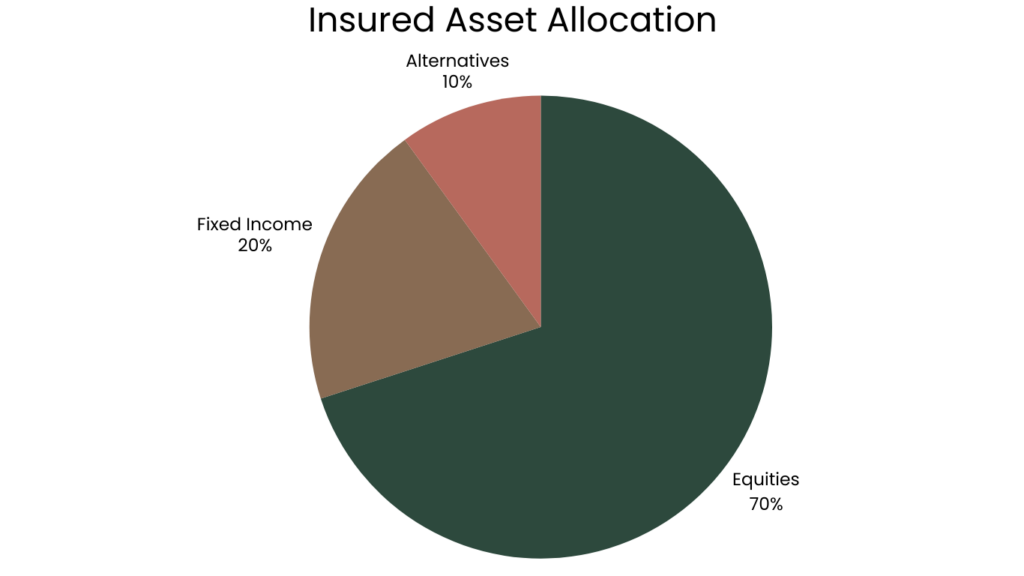

Insured Asset Allocation

Insured asset allocation is a strategy that integrates investment with risk management by establishing a portfolio’s value “floor” below which the investor is not willing to allow the total asset value to fall. It combines elements of strategic allocation with a built-in safety mechanism, ensuring that if the value of the portfolio declines toward a predetermined threshold, the investor reallocates assets to preserve capital, typically shifting funds into more conservative instruments such as Treasury securities or cash equivalents.

Amid continued volatility in equity markets, concerns over global debt levels, and inconsistent central bank signals, many investors are seeking capital preservation without completely sacrificing growth potential.

Insured allocation provides a solution by actively managing downside risk while retaining exposure to upward-trending markets.

The implementation of this strategy begins with a carefully defined investment floor. For instance, an investor might set a minimum acceptable value of $950,000 on a $1 million portfolio. As long as the market value remains well above this level, the portfolio might hold a more aggressive mix—such as 70% equities, 20% fixed income, and 10% alternatives. However, if market performance deteriorates and the portfolio approaches the floor, a preemptive reallocation toward capital-preserving assets is triggered.

What distinguishes insured allocation from standard stop-loss or hedging techniques is its built-in decision framework, often automated through portfolio insurance models or algorithmic rebalancing systems. These systems allow for gradual, data-informed transitions rather than abrupt sell-offs.

This discipline helps reduce the emotional pitfalls of investing, especially during bear markets when panic can lead to irrational decisions and permanent capital loss.

Insured asset allocation gained popularity in the wake of the 2008 financial crisis and has once again come into focus as investors respond to rising recession forecasts, credit tightening, and inflation volatility. In 2024, a notable increase in the use of this strategy was observed among retirees and institutional endowments, both of which face non-negotiable spending requirements and therefore prioritize capital stability alongside moderate returns.

An illustrative example in 2025 might involve a retiree with a fixed annual withdrawal requirement, who employs an insured allocation strategy that transitions more aggressively into municipal bonds, TIPS (Treasury Inflation-Protected Securities), or money market funds once their equity portfolio incurs a 10% drawdown. This pivot not only locks in the remaining capital but also maintains liquidity for income needs.

While insured asset allocation may not capture the full upside of a roaring bull market, it excels in its asymmetric return profile—offering limited downside exposure with the ability to participate in gains during favorable conditions.

Integrated Asset Allocation

Integrated asset allocation represents the most comprehensive and multifaceted approach among contemporary investment strategies. It differs from other models in that it considers not only the investor’s long-term goals, risk tolerance, and time horizon, but also the prevailing economic environment and the investor’s evolving personal financial situation.

In effect, it merges elements of both strategic and dynamic asset allocation, while integrating macro forecasts, capital market expectations, and behavioral finance considerations into a single cohesive framework.

This approach is gaining traction among investors who recognize that financial markets do not operate in a vacuum. The global economy is navigating the complexities of deglobalization, structural inflation, energy transition, and central bank policy divergence—conditions that demand a strategy capable of flexibly adapting while maintaining alignment with personal investment objectives.

Integrated asset allocation is often built on a core-satellite model, where the core represents a diversified mix designed to meet long-term needs—typically through low-cost index funds or ETFs—while the satellite component dynamically adjusts based on market conditions, sector opportunities, or tactical themes.

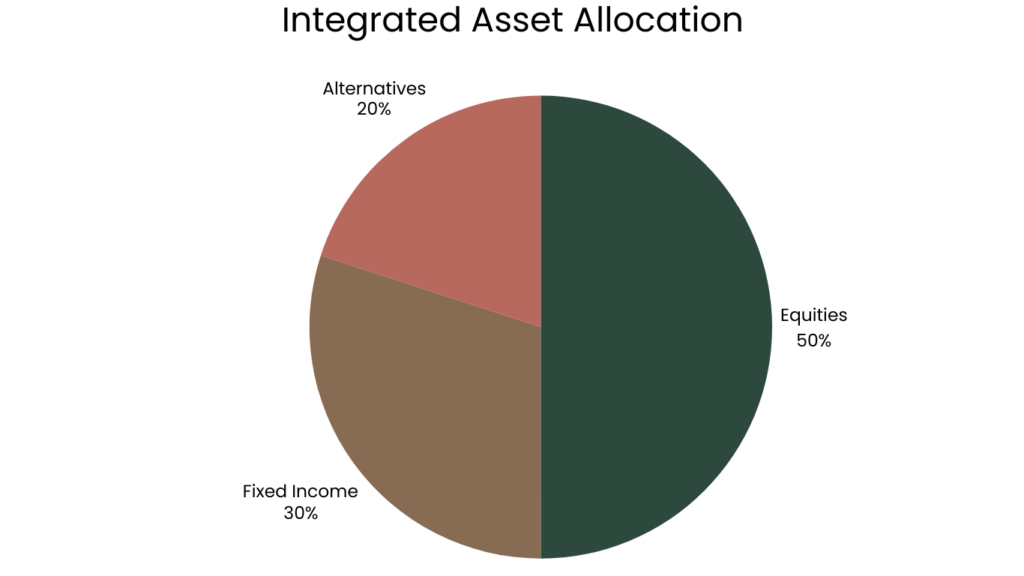

For instance, while a portfolio’s core may remain steady at 50% global equities and 30% fixed income, the satellite 20% might rotate among commodities, hedge strategies, or alternative assets such as private credit or infrastructure, depending on market signals.

One of the most distinguishing features of integrated allocation is its capacity to factor in real-life variables, such as career risk, future liabilities, or business ownership. For example, a tech entrepreneur heavily exposed to the NASDAQ through their company might hold a more conservative liquid portfolio emphasizing real assets and fixed income, thereby achieving balance when viewed holistically.

Statistical analysis from multi-asset strategy funds in 2024 reveals that integrated portfolios delivered higher Sharpe ratios and lower drawdown volatility, even when benchmark performance was erratic.

The strength of the approach lies in its layered flexibility, where no single variable dictates decision-making but rather a continuous interplay of multiple economic and personal factors.

What Is a Good Asset Allocation by Age?

While asset allocation should always reflect individual goals and risk tolerance, age remains a practical guideline in determining the right mix of assets. As investors progress through different life stages, their portfolios typically evolve to balance growth, income, and capital preservation.

Here is a simplified framework for 2025, tailored to current market conditions:

- Ages 20–35 – This stage is defined by long investment horizons and a high tolerance for risk, making it optimal for portfolios heavily weighted toward equities. A typical allocation may include 90% equities and 10% fixed income or cash, with a focus on high-growth sectors such as technology, emerging markets, and innovation-focused ETFs.

- Ages 35–50 – Investors in their mid-career years often face increasing financial obligations, leading to a more balanced portfolio structure. Allocations might shift to 70% equities, 25% fixed income, and 5% alternatives, reflecting a gradual shift toward stability while maintaining a strong growth component.

- Ages 50–65 – As retirement approaches, capital preservation takes precedence over aggressive growth. A common allocation during this phase might be 60% equities, 30% fixed income, and 10% alternatives, with a growing emphasis on dividend-paying stocks, bonds, and inflation-sensitive assets like infrastructure.

- Age 65+ – The retirement phase typically centers on income generation and portfolio stability. Investors in this group often transition to a conservative allocation of 40–50% equities, 40% fixed income, and 10% in cash or low-volatility instruments to ensure consistent income and minimal drawdowns during the distribution years.

In 2025, a more nuanced approach is gaining ground, where allocation strategies are adjusted dynamically to reflect not just age, but also personal factors like health status, employment income, and legacy planning. This evolution marks a move away from outdated formulas toward a more personalized and flexible framework.

FAQ

What is the best asset allocation strategy in 2025?

Integrated and dynamic asset allocation strategies are most effective in 2025. They adapt to market shifts while aligning with individual goals and risk tolerance.

How often should I rebalance my portfolio?

Rebalance annually for strategic allocation, quarterly for constant-weighting, and as needed for tactical or dynamic strategies based on market signals.

Can tactical asset allocation outperform passive investing?

Yes. Tactical allocation can outperform passive strategies by 1–2% annually when applied with discipline and market insight.

Is the 60/40 portfolio still effective in 2025?

Partially. The 60/40 model is now often supplemented with alternatives like real estate and private credit to improve diversification and inflation protection.

Should young investors avoid bonds?

No. While equities dominate early portfolios, a small bond allocation adds stability and liquidity during market downturns.