The Manchester Real Estate Market in 2025 offers a stable and high-performing investment environment, positioning the city as one of the UK’s most attractive regional property markets. As the unofficial capital of the North, Manchester benefits from a diverse economic base, growing population, and rapid infrastructure development—factors that continue to drive sustained demand in both the sales and rental sectors.

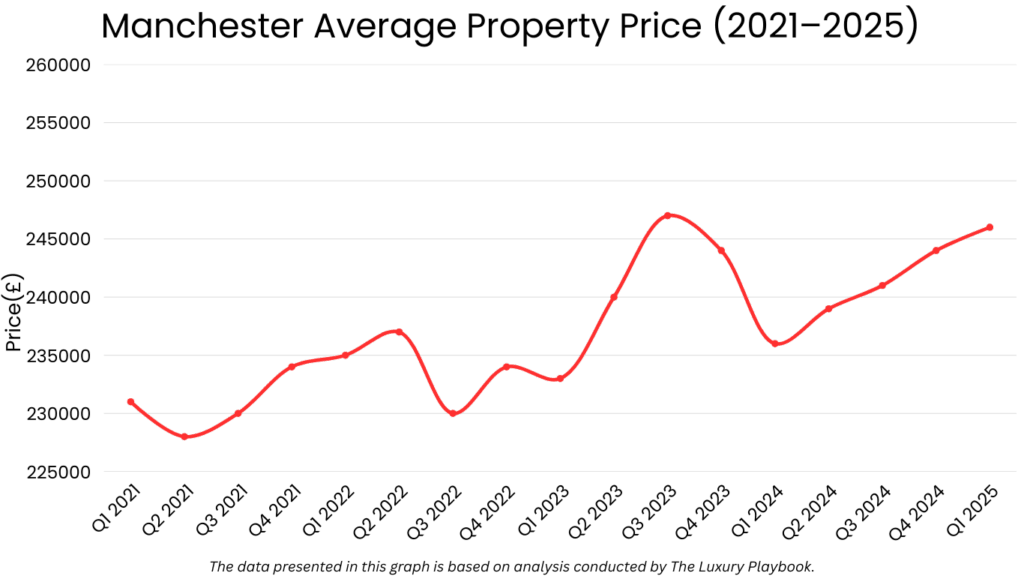

As of Q2 2025, the average residential property price in Manchester stands at approximately £241,000, marking a 5.3% increase year-over-year. This growth reflects a combination of limited housing supply, regeneration-led appreciation in city centre zones, and a strong pipeline of private and public investment in housing, commercial space, and transport.

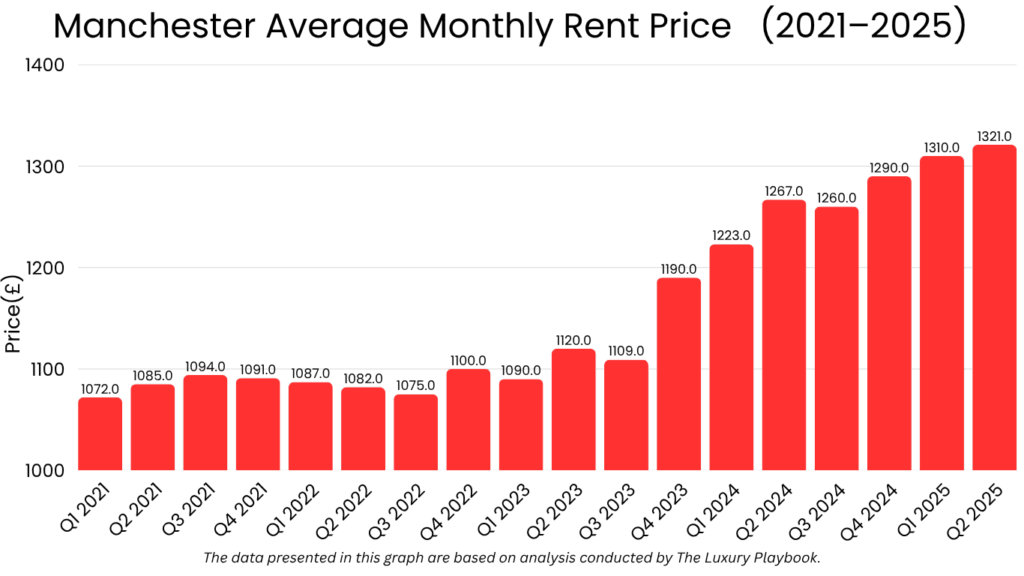

Rental market performance remains robust. Average rents now exceed £1,300/month, following a 10.2% annual increase, with high occupancy levels across both professional and student segments. Demand is strongest in areas near business districts, universities, and new-build developments, pushing yields well above the national average in several boroughs.

The Manchester Housing Market in 2025 presents a resilient opportunity for investors seeking high rental returns, long-term appreciation, and exposure to one of the UK’s most economically dynamic cities.

Table of Contents

Overview of The Manchester Real Estate Market

The Manchester Real Estate Market in 2025 is characterised by steady capital growth, rising tenant demand, and a continued shortage of quality housing across key districts. As a core city of the Northern Powerhouse, Manchester’s property market remains resilient, supported by economic diversification, inward migration, and large-scale development projects spanning residential, commercial, and transport sectors.

As of Q2 2025, the average property price in Manchester is approximately £241,000. This reflects a 2.3% annual increase, outperforming the national average and sustaining a multi-year trend of upward price momentum. Core growth areas include Ancoats, Salford Quays, and parts of South Manchester, where modern housing stock and proximity to amenities continue to drive buyer and tenant interest.

Demand remains strongest in the city centre and inner-ring suburbs, where regeneration schemes and infrastructure improvements are unlocking new residential capacity. New-build activity continues, but supply remains below current demand levels, particularly in the affordable and mid-range price segments.

This imbalance is supporting capital values and pushing up rents, making Manchester especially attractive to income-focused investors.

First-time buyers, buy-to-let landlords, and institutional players remain active, with foreign capital also targeting long-term lettings and build-to-rent (BTR) schemes. Mortgage availability is improving after a volatile interest rate cycle, adding further upward pressure to both transaction volumes and entry-level pricing.

Key market characteristics in 2025:

- Average citywide property price: £241,000

- Annual price growth: 2.3% (2024–2025)

- Prime growth zones: Ancoats, Salford Quays, Castlefield, Chorlton

- Buyer mix: Owner-occupiers, UK-based landlords, institutional BTR investors

- New supply: Focused on high-density flats and mid-rise schemes in regeneration areas

- Sales volume trend: Stable, with upward movement in secondary districts

In summary, Manchester’s housing market in 2025 remains a regional outperformer, offering a compelling mix of affordability, growth, and rental demand. Investors targeting mid-tier capital appreciation and strong income yields will find Manchester well-positioned within the UK’s property market.

Neighborhood Analysis

Manchester’s property market is built on diverse submarkets, each offering a distinct investment profile. From city-centre regeneration hotspots to high-yield commuter zones, the city’s neighborhoods vary significantly in pricing, tenant mix, and growth potential.

Ancoats

Ancoats continues to be one of the most desirable residential areas in central Manchester. Known for its industrial heritage, converted mills, and upscale new-builds, it attracts young professionals and remote workers.

Average prices are around £320,000, or £4,700/sqm, with consistent rental demand and strong liquidity. Yields are moderate, but capital growth remains reliable due to limited supply and sustained gentrification.

Salford Quays

Salford Quays has matured into a self-contained residential and commercial hub, anchored by MediaCityUK. It attracts both professionals and students working in tech, media, and creative industries.

Properties range from £260,000 to £300,000, or £4,200–£4,600/sqm. Rental yields are strong, averaging 5.5%, especially for modern 1- and 2-bedroom flats in purpose-built schemes.

Northern Quarter

The Northern Quarter is Manchester’s creative district, offering loft-style apartments, nightlife, and independent retail. It appeals to younger renters and city-centre buyers looking for walkable convenience.

Typical prices hover around £310,000, or £4,800/sqm, with high rental turnover and competitive yields near 5%. Properties here benefit from cultural cachet and long-term tenant appeal.

Chorlton

Chorlton is a suburban, lifestyle-led neighborhood in South Manchester popular with families and professionals seeking greenery and schools without leaving city limits.

Property prices are approximately £370,000, or £4,500/sqm, with slower appreciation but low vacancy and strong owner-occupier interest. It offers lower yields (~4%) but long-term value stability.

Hulme

Hulme remains an underpriced inner-city district undergoing gradual regeneration. With proximity to the city centre and university zones, it is attracting price-sensitive investors.

Average prices are around £220,000, or £3,200/sqm, with gross rental yields ranging from 5.5% to 6.2%, among the best in central Manchester.

Neighborhood Median Prices and Price per Square Meter

Manchester Rental Market Overview

The Manchester rental market in 2025 is outperforming the national average, supported by a young, mobile population, a growing student base, and strong employer presence across finance, technology, and media. With limited new rental supply and rising mortgage barriers, rental demand continues to intensify—pushing average rents to record highs across both central and suburban districts.

High occupancy, double-digit rent growth, and a resilient tenant base make Manchester one of the UK’s strongest rental markets for income-oriented investors.

Average Monthly Rent by Property Type (2025)

- 1-Bedroom Apartment: £950 – £1,200

- 2-Bedroom Apartment: £1,200 – £1,450

- 3-Bedroom Apartment: £1,450 – £1,800

- Premium City Centre Units: £2,000 – £2,500+

The average rent across Manchester is now £1,321/month, driven by constrained supply and increased competition among renters. The highest rental growth has been observed in Salford Quays, Ancoats, and Castlefield, where regeneration and tenant amenities attract professionals and digital nomads.

University-driven areas like Fallowfield and Ardwick remain highly competitive, delivering reliable turnover and strong seasonal occupancy, while South Manchester suburbs like Didsbury and Chorlton cater to long-term tenants and family renters.

Yield Performance and Tenant Segmentation

Manchester continues to deliver above-average gross rental yields, typically ranging from 4.5% to 6.5%, with outer and up-and-coming districts offering the highest returns:

- High-Yield Zones: Hulme, Ardwick, Fallowfield (5.7%–6.5%)

- Balanced Performance: Salford Quays, Castlefield, Northern Quarter (4.8%–5.5%)

- Lower-Yield Stability: Didsbury, Chorlton (3.9%–4.2%)

Tenant demand is strongest for modern 1- and 2-bedroom units, preferably furnished and located within walking distance of transit or employment hubs. Lease terms average 12 to 24 months, though mid-stay demand is growing in high-amenity developments near MediaCityUK and the Spinningfields business district.

Moreover, Manchester’s rental market remains legally stable, with no city-wide rent caps currently in place. Landlords must comply with standard national regulations, including deposit protection, HMO licensing, and EPC minimum standards (E).

Energy-efficient upgrades are increasingly prioritised as landlords seek to remain competitive and meet future compliance targets.

Short-term letting is permitted, but local councils are introducing stricter oversight on transient rentals in city-centre buildings, particularly those used for Airbnb or serviced accommodation models.

In summary, Manchester’s rental market offers income resilience, structural undersupply, and strong tenant fundamentals. Investors targeting long-term rentals in regeneration corridors or student-dense zones are well-positioned to achieve above-market returns in 2025 and beyond.

Factors Influencing the Manchester Housing Market

The Manchester Housing Market in 2025 is shaped by a convergence of demographic shifts, economic growth, infrastructure investment, and policy conditions. These combined forces continue to reinforce Manchester’s appeal as one of the UK’s top-performing regional property markets, especially for yield-focused and long-hold investors.

- Strong Economic Fundamentals: Manchester remains the economic engine of the North West, with a diverse base in finance, media, tech, education, and life sciences. With over 1.4 million jobs in Greater Manchester and a growing number of FTSE employers relocating outside London, the city continues to attract skilled professionals—boosting both owner-occupier demand and the rental pool.

- Population Growth and Urban Density: The city’s population is expected to surpass 600,000 by 2026, with wider Greater Manchester approaching 3 million. In-migration from other parts of the UK, along with a substantial student population of over 100,000, has created long-term housing pressure across multiple price points.

- Regeneration and Transport Infrastructure: Flagship regeneration zones such as Victoria North, Mayfield, and St. John’s are adding thousands of homes and reshaping urban living. Investment in Metrolink expansion, HS2 rail connectivity, and green public space is making districts like Ancoats, Eastlands, and Newton Heath more accessible and attractive to renters and buyers alike.

- Limited Supply and Developer Constraints: While Manchester has a visible skyline of cranes, new-build delivery is not keeping pace with demand. Construction delays, cost inflation, and local planning bottlenecks have constrained new housing starts. As a result, resale apartments—particularly in central areas—continue to appreciate, and rental supply remains tight.

- Institutional Investment in Build-to-Rent (BTR): Major institutional players continue to commit capital to Manchester’s BTR market, favouring high-density urban assets with long-term lease profiles. These professionally managed units are reshaping tenant expectations and putting pressure on traditional private landlords to modernise and compete.

- Mortgage Rate Stabilisation: After 18 months of volatility, lending conditions are gradually improving, with mortgage availability and rate normalisation supporting both first-time buyers and leveraged investors. LTVs remain favourable on rental stock with strong EPC ratings, and fixed-rate products are regaining popularity.

Manchester Housing Market Forecast for 2026

The Manchester Housing Market is forecast to maintain a steady upward trajectory into 2026, with moderate price growth and sustained rental inflation driven by ongoing regeneration, demographic expansion, and constrained supply. While the rate of appreciation may level off from previous peaks, rental income and long-term value preservation remain strong.

For yield-driven investors and long-hold buyers, Manchester is expected to remain one of the UK’s most consistent urban real estate markets in 2026.

Property prices in Manchester are projected to grow by 4.0% to 5.5%. This forecast is supported by continued undersupply, improving mortgage affordability, and strong inward migration. Growth will be most pronounced in emerging districts such as Hulme, Ardwick, Newton Heath, and areas adjacent to Victoria North, where regeneration is accelerating.

Established hotspots like Ancoats, Salford Quays, and Castlefield are expected to grow more modestly—between 3.0% and 4.5%—due to maturing pricing and saturation of high-end stock. However, these zones will continue to offer long-term security and tenant appeal.

Citywide, the average price is expected to reach £258,000 to £265,000 by Q4 2026, depending on inflation, borrowing costs, and local supply responses.

Rents are forecast to increase by 5.0% to 6.5%, led by pressure from new graduate renters, incoming professionals, and the limited release of newly built stock. The highest rental growth will likely occur in inner-city districts like Fallowfield, Ardwick, MediaCity, and parts of Northern Quarter, where rental supply remains low and tenant competition is intense.

- 2-bedroom flats in Ancoats, Salford Quays, and Castlefield could exceed £1,500/month

- 1-bedroom apartments in regeneration zones are expected to average £1,250–£1,400/month

Gross yields will remain competitive, ranging from 4.5% to 6.5%, with older resale stock outperforming in areas undergoing active redevelopment or benefiting from improved transport links.

New development pipelines will be uneven. While BTR-led projects and institutional blocks will continue to reshape the skyline, private sector completions will remain below demand—especially in mid-range, owner-occupier-focused housing. The lag in affordable supply will keep pressure on both prices and rents.

Investor sentiment remains positive. With improved mortgage terms, steady population growth, and no imminent regulatory shocks, Manchester is expected to retain its position as the top UK regional market for diversified portfolios. Foreign capital will continue targeting city-centre buy-to-let and BTR partnerships, while domestic investors will seek high-yield properties in regeneration corridors.

In summary, Manchester’s housing market in 2026 is forecast to offer stable, sustainable growth with reliable rental upside. Investors who prioritise tenant-ready assets in rising zones will benefit from consistent returns and mid-tier capital appreciation.

Is It Worth Buying a Property in Manchester?

Yes—with the right property type and location, Manchester remains one of the UK’s most investable regional cities in 2025 and 2026. Its combination of above-average rental yields, consistent population growth, and ongoing regeneration makes it attractive for income-focused and long-term investors. However, price growth is becoming more segmented, and not all districts offer the same upside.

The average gross rental yield across Manchester ranges between 5% and 6.5%, outperforming many UK cities. Neighborhoods like Hulme, Fallowfield, and Ardwick continue to provide strong cash flow due to lower purchase prices and high rental demand. Meanwhile, central locations such as Ancoats, Castlefield, and Salford Quays offer stronger capital preservation but lower yields—better suited for capital-stable portfolios.

That said, investors should consider:

- Capital growth will be modest in mature zones, as some prime areas near saturation.

- New development competition is growing in the BTR sector, particularly in city-centre towers.

- Energy efficiency and EPC compliance are increasingly vital, with older stock requiring upgrades to remain legally lettable by 2028.

- Student HMO areas (like Fallowfield) are under tighter scrutiny, with local councils considering density controls and registration schemes.

The best-performing opportunities will likely be in value-growth corridors undergoing infrastructure and urban renewal—such as Newton Heath, Miles Platting, and around Victoria North—where entry prices remain accessible and long-term demand is increasing.

Other Market Forecasts & Overviews

London Real Estate Market Overview & Forecast

Liverpool Real Estate Market Overview & Forecast

Bristol Real Estate Market Overview & Forecast

Derby Real Estate Market Overview & Forecast

FAQ

Is Manchester a good place to invest in property in 2025?

Yes. Manchester offers high rental yields, strong tenant demand, and long-term growth supported by regeneration and economic expansion.

What is the average property price in Manchester in 2025?

Approximately £246,000, with higher prices in central neighborhoods like Ancoats and Castlefield.

Where are the best areas to invest in Manchester?

Hulme, Fallowfield, Ardwick, and Salford Quays offer a strong mix of yield and capital growth potential.

Are rental yields strong in Manchester?

Yes. Yields range between 4.5% and 6.5%, outperforming the national average, especially in value-growth districts.

Can foreigners buy property in Manchester?

Yes. There are no restrictions on foreign property ownership in the UK.

Are rent caps or price controls in place in Manchester?

No. Manchester does not currently enforce rent controls, but landlords must comply with national tenancy laws and local licensing in some areas.

What kind of property performs best for investment in Manchester?

1- and 2-bedroom apartments in regeneration areas or close to transit hubs deliver the best balance of price, yield, and demand.

Is short-term letting legal in Manchester?

Yes, but it’s regulated, and local councils are tightening enforcement, particularly in city-centre developments.

Will Manchester house prices rise in 2026?

Yes. Prices are forecast to increase by 4.0% to 5.5%, with stronger growth in emerging districts and regeneration zones.