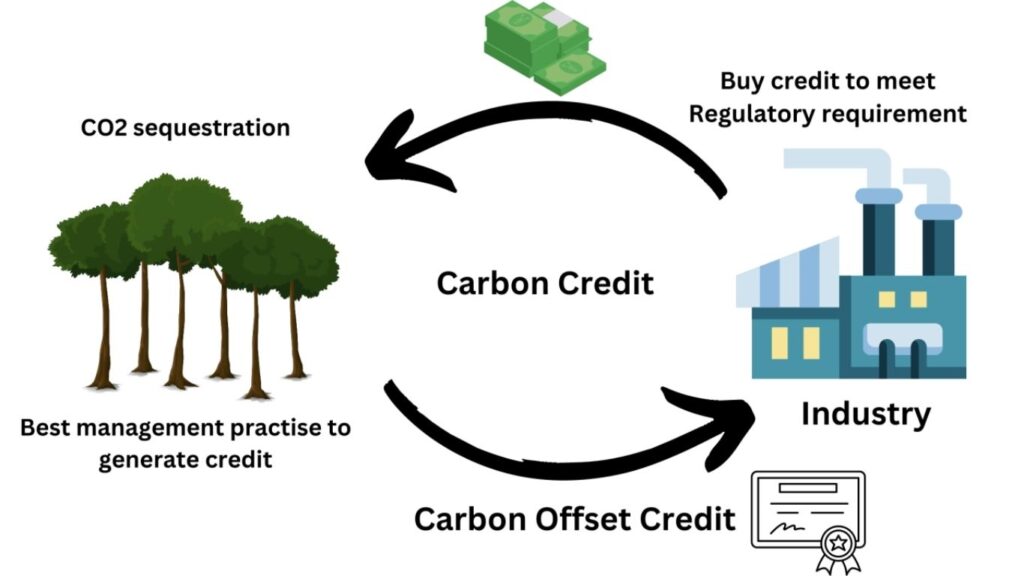

Carbon credits are key in the global fight against climate change by minimizing greenhouse gas emissions. These credits function like permits, allowing entities a certain level of CO2 emissions.

Issued by governments and shaped by international pacts like the Kyoto Protocol and the Paris Agreement, they aim for environmental sustainability.

Through cap-and-trade systems, these credits enable firms to meet tightening emissions goals, encouraging them to lessen their carbon output.

The system allows for the trading of credits, enabling companies that emit less than their allowance to sell their surplus. Last year, the voluntary carbon market was worth about $400 million and may hit $10-25 billion by 2030.

As the climate crisis deepens, the utility and complexity of carbon credits in emission reduction and offsets are growing, offering both possibilities and hurdles toward a sustainable future.

How Carbon Credits Work

Carbon credits are a financial mechanism designed to incentivize the reduction of greenhouse gas emissions.

Essentially, a carbon credit represents the removal or reduction of one metric ton of carbon dioxide (CO2) or its equivalent in other greenhouse gases from the atmosphere.

These credits are generated through various projects, such as renewable energy initiatives, reforestation, or improving energy efficiency in industrial processes.

To understand how carbon credits work, it’s important to differentiate between the two main markets: compliance and voluntary.

- Compliance Markets: These are established by governments or multi-government bodies. The European Union’s Emissions Trading System (EU ETS), for instance, is the largest and oldest compliance market, covering around 10,000 facilities in sectors like energy and manufacturing.

In 2021, the global compliance market was valued at approximately $850 billion. In these markets, companies must hold enough credits to cover their emissions; if they exceed their cap, they must buy additional credits, incentivizing them to reduce emissions to avoid extra costs. - Voluntary Markets: These markets are not regulated by governments but are driven by companies and individuals looking to offset their carbon footprint. Voluntary markets are smaller, valued between $1 billion and $2 billion in 2021, but they are rapidly growing.

In these markets, companies purchase credits to meet environmental, social, and governance (ESG) goals or in response to consumer pressure. Major buyers include tech giants like Microsoft and automotive companies like Tesla.

Cap-and-Trade System

The cap-and-trade system is a market-based approach to controlling pollution by providing economic incentives for achieving reductions in the emissions of pollutants. Here’s how it works:

- Setting the Cap: The government sets a cap on the total amount of a specific pollutant that can be emitted by all companies covered by the system.

This cap is often reduced over time to decrease total emissions. For example, California’s cap-and-trade program, initiated in 2013, targets large emitters like power plants and fuel distributors, progressively tightening the cap to encourage reductions in emissions. - Trading Allowances: The cap is divided into allowances, each permitting the holder to emit a certain amount of the pollutant (typically one ton of CO2 equivalent). Companies that reduce their emissions below their allowance can sell their excess allowances to other companies that exceed their limits.

This creates a financial incentive for companies to invest in cleaner technologies to reduce their emissions and potentially profit from selling their unused allowances.

The cap-and-trade system has proven effective in various regions.

For instance, the European Union’s ETS has been instrumental in reducing emissions across the EU, and China’s national carbon market, launched in 2021, is expected to be the world’s largest, covering over 2,600 companies initially.

How Carbon Credits Are Created and Traded

Carbon credits play a critical role in global climate efforts by providing a financial mechanism to reduce greenhouse gas emissions.

The creation and trading of these credits occur in two primary markets: regulatory (compliance) and voluntary. Each market serves different purposes and involves unique actors, regulations, and dynamics.

Regulatory Markets

Regulatory Carbon Markets are established by government mandates, where entities must comply with emission caps set by law.

One prominent example is the European Union Emissions Trading System (EU ETS), the world’s largest carbon market, which covers over 11,000 installations in power and industrial sectors across 31 countries.

The EU ETS uses a cap-and-trade system where the total number of carbon allowances is capped, and companies must either reduce emissions or purchase additional credits.

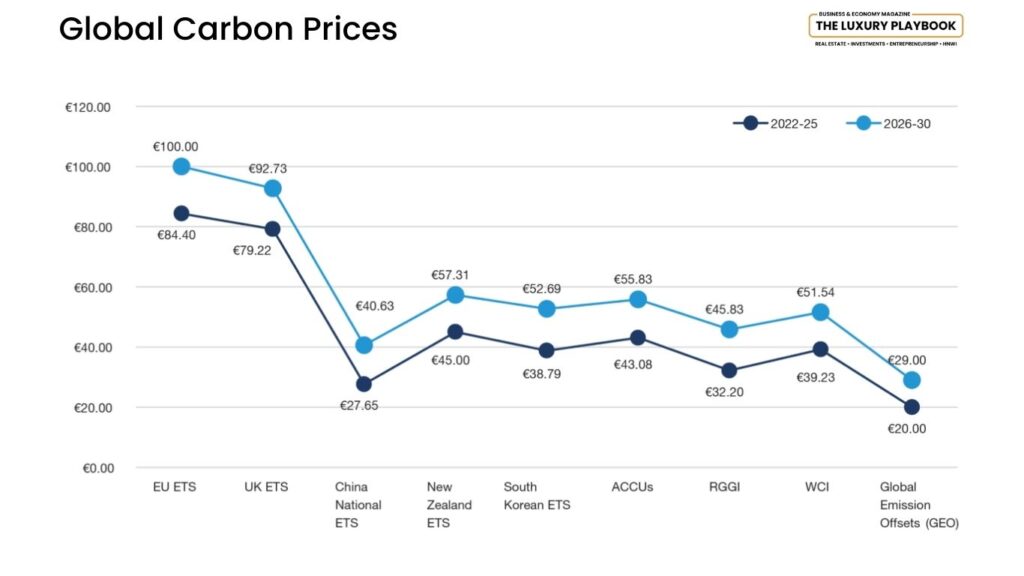

This system helped cut the EU’s greenhouse gas emissions by 43% below 2005 levels by 2023.

In the United States, California’s Cap-and-Trade program is another significant regulatory market, which has seen prices rise from $34 per ton in 2023 to an expected $46 per ton in 2025 due to stricter caps and rising demand for allowances.

Voluntary Markets

Voluntary Carbon Markets allow businesses and individuals to purchase carbon credits to offset their emissions on their own accord, often to meet corporate sustainability goals or consumer expectations.

Companies like Shell and Microsoft have been major players in this market, voluntarily buying offsets to achieve net-zero targets.

The voluntary market is projected to reach $10 billion by 2030, driven by increased corporate commitments and consumer awareness.

Unlike compliance markets, voluntary markets are not regulated by government bodies but are overseen by third-party standards such as the Verified Carbon Standard (VCS) and the Gold Standard, which ensure that projects are genuine and effective.

Role of Government and International Agreements

Governments and international frameworks are pivotal in shaping both regulatory and voluntary carbon markets.

The Kyoto Protocol and the Paris Agreement set the groundwork for carbon trading by establishing international carbon markets and encouraging countries to meet their emission reduction targets.

For example, the Paris Agreement has spurred the growth of carbon markets globally, with over 80 countries now implementing carbon pricing mechanisms, including carbon taxes and emissions trading systems (World Bank, 2024).

China’s Emissions Trading System (ETS) is another significant example. Launched in 2021, it initially focused on the power sector but is expected to expand to other sectors in the coming years.

The Chinese market, currently the world’s largest in terms of covered emissions, provides a cap-and-trade platform similar to the EU ETS but tailored to the country’s unique economic and industrial context.

Examples from the U.S. and Worldwide

In the United States, the Regional Greenhouse Gas Initiative (RGGI), covering 12 Northeastern and Mid-Atlantic states, and California’s Cap-and-Trade program are key examples of state-level regulatory markets.

These programs require power plants and large industrial emitters to purchase allowances for their emissions, thereby creating a financial incentive to reduce emissions over time.

The U.S. carbon credit market is projected to grow significantly due to rising energy demands and tightening state regulations.

Globally, the European Union Emissions Trading System (EU ETS) has played a significant role since its establishment in 2005.

It currently includes over 11,000 entities and covers 45% of the EU’s total greenhouse gas emissions.

Meanwhile, Singapore aims to position itself as a carbon trading hub, leveraging its strong financial sector and strategic location to facilitate regional carbon trading initiatives.

Future Trends and Challenges in Carbon Credits

The future of the carbon credit market is set for rapid growth but faces several hurdles. The market could reach over $4.4 trillion by 2031 due to regulatory changes, technological advancements, and increased corporate commitments.

However, supply constraints, price volatility, and questions about the credibility of credits present significant challenges.

Demand Surge and Supply Constraints

Demand for carbon credits is expected to grow dramatically, potentially reaching 1.6 billion credits annually by 2030 and 5.1 billion by 2050.

However, supply is tight; credit issuance fell by 25% in 2023, the lowest in three years, driven by a decline in nature-based and renewable energy projects.

This mismatch between demand and supply creates a volatile market environment.

Price Volatility and Credibility Issues

Carbon credit prices fluctuate widely, driven by regulatory changes and market dynamics.

For instance, California’s prices are expected to rise from $46 per ton in 2025 to $93 by 2030, while EU prices could reach $163 per ton by 2030.

Concerns over the quality and integrity of credits, such as accusations of greenwashing, continue to undermine market confidence.

Technological and Policy Developments

Technologies like blockchain and AI offer potential solutions to improve transparency and trust in carbon transactions.

Meanwhile, policy changes, including the introduction of new compliance programs and carbon border taxes, could further tighten supply and increase demand.