The global wine industry is booming, fueled by rising demand, a relentless push toward premiumization, and hungry emerging markets. For you as an investor, wine stocks offer something genuinely rare — a blend of financial opportunity, cultural prestige, and surprising resilience when markets get rocky. Heading into 2026, these stocks are drawing serious attention for their historical performance, dividend potential, and compelling growth trajectories. If you’ve been looking for a way to diversify beyond the usual plays, this is worth your time.

Investing in wine stocks is not just about holding shares in a beverage company. You’re buying a stake in a product that fuses centuries of tradition with sharp modern market strategy. Companies in this sector run the gamut from sprawling luxury conglomerates to tight boutique wineries, and each one brings a different kind of investment story to the table. The key is knowing which story fits your portfolio.

Table of Contents

Best Wine Stocks To Invest In 2025

- LVMH Moët Hennessy Louis Vuitton (EPA: MC): €7.1B Wines & Spirits revenue (+9% YoY), Dividend Yield: 1.9%, 5-Year Growth: +80%.

- Constellation Brands (NYSE: STZ): $9.5B revenue (+7% YoY), Dividend Yield: 1.3%, 5-Year Growth: +75%.

- Treasury Wine Estates (ASX: TWE): AUD $2.8B revenue (+13% YoY), Dividend Yield: 2.1%, 5-Year Growth: +55%.

- Diageo PLC (NYSE: DEO): £12.7B revenue (+6% YoY), Dividend Yield: 2.5%, 5-Year Growth: +58%.

- The Duckhorn Portfolio (NYSE: NAPA): $420M revenue (+9% YoY), No Dividend, 5-Year Growth: +62%.

- LQR House Inc. (NASDAQ: LQR): $15M revenue (+12% YoY), No Dividend, 3-Year Growth: +22%.

- Willamette Valley Vineyards (NASDAQ: WVVI): $27M revenue (+4% YoY), No Dividend, 5-Year Growth: +18%.

- Splash Beverage Group (NYSE: SBEV): $23M revenue (+17% YoY), No Dividend, 5-Year Growth: +25%.

- Vintage Wine Estates (NASDAQ: VWE): $320M revenue (+6% YoY), No Dividend, 5-Year Growth: +22%.

- Compañía Cervecerías Unidas (NYSE: CCU): $3.2B revenue (+5% YoY), Dividend Yield: 3.5%, 5-Year Growth: +48%.

- Ambev S.A. (NYSE: ABEV): $15.4B revenue (+7% YoY), Dividend Yield: 4.2%, 5-Year Growth: +35%.

- Brown-Forman (NYSE: BF.B): $4.4B revenue (+5% YoY), Dividend Yield: 1.6%, 5-Year Growth: +40%.

- Pernod Ricard (EPA: RI): €12.8B revenue (+6% YoY), Dividend Yield: 2.2%, 5-Year Growth: +45%.

LVMH Moët Hennessy Louis Vuitton

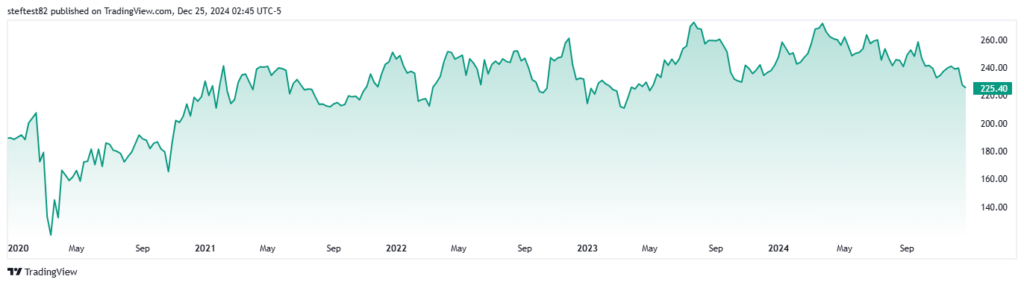

LVMH Moët Hennessy Louis Vuitton (EPA: MC) sits at the very top of the global luxury wine and spirits world. With names like Dom Pérignon, Moët and Chandon, Krug, and Château d’Yquem in its stable, the group commands a presence that few can touch. Its Wines and Spirits division cuts across established and emerging markets with equal confidence, and it operates alongside fashion, retail, and hospitality arms that most competitors can only dream of. If you want blue-chip wine exposure, this is where the conversation starts.

In 2024, LVMH posted a 15% increase in overall revenue, with the Wines and Spirits segment alone pulling in €7.1 billion. That’s 9% year-over-year growth, driven by surging demand across Asia-Pacific and North America. The segment’s operating profit margins consistently clear 30%, which tells you everything you need to know about the pricing power these brands carry.

Over the past five years, LVMH’s stock has climbed roughly 80%, with an 18% jump in 2024 alone. That kind of sustained appreciation reflects exactly what you’d expect from a luxury house built to weather economic storms. On top of the capital gains, shareholders collected a €7.00 dividend per share in 2024, translating to a 1.9% yield. Not bad for a stock that also delivers serious growth.

The real engine here is brand equity. Dom Pérignon and Krug aren’t just wine labels — they’re cultural institutions, and that status insulates them from the kind of price sensitivity that hits lower-tier producers hard. Layer on LVMH’s global distribution machine, and you get a company that can sell premium wine in Paris, Shanghai, and Mumbai with equal ease. That reach matters.

Portfolio diversification is another quiet advantage. Even if the Wines and Spirits segment hits a rough patch, LVMH’s fashion and retail arms provide a natural cushion. And the company has been putting serious capital into sustainable viticulture, which strengthens its brand reputation while reducing long-term operational risk. It’s the kind of forward thinking you want to see from a company you’re holding for the long haul. You can explore how rare wine grapes are quietly attracting billionaire investors to understand why sustainability and exclusivity are driving premium valuations across the sector.

Outlook for 2026

Looking ahead, LVMH is well set to keep building on its wine and spirits momentum through 2026. Rising affluence in emerging markets keeps demand for premium wines on an upward curve, while digital sales channels have matured into a genuine revenue pillar. The group also stays active on the acquisition front, regularly picking up boutique wineries and premium brands to sharpen its already formidable portfolio.

For you as an investor, LVMH offers something rare — luxury appeal, financial firepower, and consistent returns all wrapped into one position. Its market dominance, iconic wine brands, and diversified operations make it a strong anchor for long-term growth and portfolio stability.

Key Financial Highlights

- 2024 Wines & Spirits Revenue: €7.1 billion (9% YoY growth)

- Dividend Yield: 1.9% (€7 per share)

- 5-Year Stock Appreciation: +80%

- Operating Margins: Over 30%

Investing in LVMH Moët Hennessy Louis Vuitton puts you inside the premium tier of the global wine market, backed by world-class brands, robust financials, and the kind of strategic vision that keeps compounding over time.

Constellation Brands

Constellation Brands (NYSE: STZ) is one of the largest beverage alcohol companies on the planet, with a portfolio that spans wine, beer, and spirits. You’ll know brands like Robert Mondavi, Kim Crawford, and Meiomi from retail shelves across North America, and those names carry real weight in the premium segment. The company’s track record of strategic acquisitions, a sharp focus on premiumization, and tight operational discipline has produced consistent growth that deserves a close look from any serious investor.

In 2024, Constellation Brands posted net sales of $9.5 billion, a 7% gain year-over-year. The wine and spirits division, while a smaller slice of overall revenue compared to beer, punches well above its weight in terms of profitability. That growth was driven largely by premium wine demand in the United States and select international markets, where consumers are trading up fast.

The stock has delivered a cumulative 75% gain over the past five years, with a strong 15% increase in 2024 alone. You’ve also been collecting a quarterly dividend of $0.84 per share along the way, which works out to an annual yield of roughly 1.3%. That combination of appreciation and income is a solid return profile.

Constellation Brands maintains operating profit margins consistently around 28%, which reflects a company that knows how to price its products and control its costs at scale.

The wine portfolio here is genuinely well-constructed. You get both high-volume commercial labels and premium offerings aimed squarely at affluent consumers. Kim Crawford and Meiomi have been standout performers in the premium tier, capturing meaningful market share across North America with a consistency that larger conglomerates often struggle to match.

The push toward premiumization, shifting focus away from mass-market wines toward high-end offerings, has kept margins healthy and long-term growth prospects intact. And Constellation has been smart about layering in data analytics and digital platforms to sharpen its distribution and customer targeting. That’s not just a nice-to-have anymore. It’s a real competitive edge.

Beyond its North American stronghold, Constellation has been making deliberate moves into Asia-Pacific and Latin America, where rising disposable incomes are creating a fresh appetite for premium wines. Partnerships with local distributors and targeted marketing campaigns have given the company early footholds in markets that could become significant contributors over the next decade.

Constellation has also put real money into sustainable vineyard management and eco-friendly production. And on the innovation side, you’re seeing lower-calorie wines, organic offerings, and digital wine experiences rolling out to capture a consumer base whose preferences keep evolving. These aren’t cosmetic moves. They’re responses to where the market is genuinely heading.

Outlook for 2026

Looking ahead, Constellation Brands is positioned to ride the ongoing wave of premium wine consumption well into 2026. Strategic acquisitions and smart partnerships will remain core growth levers, while digital transformation keeps improving market efficiency across the board.

For you as an investor seeking steady growth, reliable dividends, and exposure to premium wine brands, Constellation Brands makes a strong case. Its balanced portfolio management, operational discipline, and commitment to sustainability add up to a compelling investment story.

Key Financial Highlights

- 2024 Net Sales: $9.5 billion (7% YoY growth)

- Dividend Yield: 1.3% ($0.84 per share quarterly payout)

- 5-Year Stock Growth: +75%

- Operating Profit Margins: ~28%

With solid financials, premium brand positioning, and a clear growth strategy, Constellation Brands is a top-tier option for investors who want stability and growth potential sitting side by side in the same position.

Treasury Wine Estates

Treasury Wine Estates (ASX: TWE) is one of the biggest wine companies in the world, and if you know wine, you know its brands. Penfolds, Wolf Blass, 19 Crimes, Beringer — these aren’t just labels, they’re category leaders. Based in Australia, Treasury has built a dominant position across both the premium and luxury wine markets, backed by a global distribution network that gives it genuine reach in the markets that matter most.

In 2024, Treasury Wine Estates posted revenue of AUD 2.8 billion, a 13% jump year-over-year. That growth came on the back of stronger demand for premium wines and a successful push back into Asian markets, particularly China after trade restrictions eased. The luxury tier, led by the iconic Penfolds Grange, kept delivering for the bottom line and showed no signs of slowing down.

The stock climbed 10% over the past year, in line with the company’s deliberate strategy of tilting the portfolio toward premium and luxury categories. Zoom out to five years and you’re looking at a cumulative return of roughly 55%, which reflects steady, purposeful execution rather than short-term noise.

Treasury Wine Estates paid a final dividend of AUD 0.18 per share in 2024, landing at an annual yield of around 2.1%. For income-focused investors, that’s a meaningful return on top of the capital appreciation story.

The premiumization strategy is the core of what Treasury does well. Brands like Penfolds and Wolf Blass Platinum Label command serious loyalty and serious margins globally. By concentrating on higher-end wines, the company has reduced its exposure to the thin-margin commercial segment where pricing pressure is relentless. That’s a smart trade-off, and the numbers back it up.

Treasury has also invested heavily in direct-to-consumer channels, letting enthusiasts buy wines through digital platforms and exclusive memberships. Beyond the margin uplift, these channels deepen customer relationships in ways that traditional retail simply can’t match.

Asia is where the real growth story gets exciting. China’s return as an accessible market after the removal of punitive tariffs on Australian wines is a genuine tailwind. Treasury has also been expanding across Southeast Asia and Japan, tapping into consumer markets where rising incomes and evolving tastes are creating demand for exactly the kind of premium wines Treasury excels at producing.

In the United States, the picture is equally solid. Beringer and 19 Crimes both carry strong consumer recognition, and that brand equity translates directly into shelf space and repeat purchases across the country.

Outlook for 2026

Heading into 2026, Treasury Wine Estates has the pieces in place for continued growth. The premiumization strategy, global distribution infrastructure, and focus on high-growth regions in Asia and North America all point in the same direction. Digital and direct-to-consumer channels will play an expanding role in driving future sales, while strategic partnerships will keep tightening the company’s market position.

For investors wanting exposure to a global wine powerhouse with a clear focus on premium growth and reliable income, Treasury Wine Estates makes a genuinely strong case. Its brand portfolio, market positioning, and financial discipline create a compelling combination for both long-term appreciation and steady dividends.

Key Financial Highlights

- 2024 Revenue: AUD 2.8 billion (13% YoY growth)

- Dividend Yield: 2.1% (AUD 0.18 per share)

- 5-Year Stock Growth: +55%

- Key Growth Markets: Asia, United States

With luxury wines, sustainable practices, and a well-executed global expansion strategy, Treasury Wine Estates stands out as one of the most serious wine stocks you can own.

Diageo PLC

Diageo PLC (NYSE: DEO) is one of the world’s largest beverage alcohol companies, and its reach goes far beyond Johnnie Walker and Guinness. The wine side of the business, anchored by Sterling Vineyards, Chalone Vineyard, and Beaulieu Vineyard, has carved out a real presence in the global premium wine market. Diageo’s approach blends deep tradition with genuine innovation, and its focus on premium wine selections speaks directly to the kind of discerning consumer who drives the most valuable growth in this category.

In 2024, Diageo reported net sales of £12.7 billion, up 6% year-over-year. Wine is a smaller slice of the overall pie, but it plays a strategic role in the company’s premiumization push, contributing 8% of total revenue with strong support from North America and Europe. That’s not an afterthought. It’s a deliberate positioning choice.

The stock gained 12% in 2024, extending an upward trend that has delivered 58% cumulative appreciation over five years. And while you’re waiting for that capital growth, Diageo pays a semi-annual dividend of £0.47 per share, adding up to a 2.5% annual yield. The operating profit margin holds at around 27%, which tells you the premium pricing strategy is working.

Diageo’s operating profit margin holds at approximately 27%, reflecting tight cost management and the strong profitability of its premium product segments across both spirits and wine.

Diageo’s greatest asset in wine is its global distribution reach. Sterling Vineyards and Chalone already benefit from relationships that took decades to build in retail and hospitality, and that kind of access is genuinely hard to replicate. When you’re sitting inside Diageo’s network, your wine gets seen.

Sterling Vineyards Reserve and Chalone Estate Chardonnay both target high-income consumers willing to pay for exceptional quality. That premium positioning protects margins even when broader market conditions get choppy. And Diageo is disciplined enough to protect that positioning rather than chasing volume at the expense of brand equity.

Innovation and Consumer Trends

Diageo has moved early and decisively on digital sales channels and direct-to-consumer platforms, giving wine lovers direct access to its premium labels while generating customer insights that sharpen every marketing decision. Exclusive wine releases through these platforms have become a genuine brand-building tool, creating scarcity and desire in equal measure.

The company is also leaning into emerging consumer trends including low-alcohol wines, organic varieties, and sustainable production methods. These aren’t just trend-chasing moves. They reflect a real shift in what premium wine consumers want, and Diageo is meeting them where they are.

North America and Europe are delivering strong results, but the bigger opportunity for Diageo’s wine division sits in Asia-Pacific and Latin America. Rising disposable incomes and shifting consumption habits in these regions are creating fertile ground for premium wine sales, and Diageo’s localized marketing campaigns and distributor partnerships are helping it build position before competitors lock down the territory.

Outlook for 2026

Diageo is set up for steady wine segment growth heading into 2026, capitalizing on global demand for premium labels while pushing harder on digital transformation and product innovation. The balance between tradition and modernity that defines Diageo’s brand identity is exactly what premium wine consumers respond to, and that should continue to pay dividends, literally and figuratively.

For investors looking for exposure to a stable, diversified beverage giant with serious premium wine credentials, Diageo PLC is a genuinely attractive option. Consistent revenue growth, solid dividend payouts, and global distribution make it a reliable addition to any well-constructed portfolio.

Key Financial Highlights

- 2024 Net Sales: £12.7 billion (6% YoY growth)

- Wine Segment Contribution: 8% of total revenue

- Dividend Yield: 2.5% (£0.47 per share)

- 5-Year Stock Growth: +58%

- Operating Margin: ~27%

If you want long-term stability, reliable dividends, and exposure to premium wines inside a company with world-class distribution, Diageo PLC belongs on your shortlist.

The Duckhorn Portfolio

The Duckhorn Portfolio (NYSE: NAPA) is the kind of wine company that doesn’t need to shout about its quality because its bottles do the talking. Based in Napa Valley, California, Duckhorn has built an extraordinary reputation through brands like Duckhorn Vineyards, Decoy, Paraduxx, and Goldeneye. Its focus on high-quality wines, a powerful direct-to-consumer engine, and smart distribution has made it one of the most compelling pure-play wine investments you can find on a public exchange.

In 2024, The Duckhorn Portfolio posted net sales of $420 million, a 9% year-over-year increase. That growth was powered by stronger sales volumes across its premium labels and a North American market that continues to show robust appetite for luxury wine. This is not a company depending on one lucky vintage. The results are consistent and structural.

The gross margin sitting at roughly 49% is exceptional by any measure in this space. Duckhorn doesn’t pay a dividend, choosing instead to put profits back into vineyard expansions, marketing, and enhancing its direct-to-consumer platforms. If you’re a growth-oriented investor, that’s exactly the capital allocation you want to see.

The stock has delivered an 18% gain in 2024 and a cumulative 5-year growth of 62%. Investors who recognized Duckhorn’s quality early have been rewarded, and the underlying fundamentals suggest that story has more to run.

Duckhorn operates almost entirely in the luxury and ultra-luxury wine segments, which means the people buying these bottles are not price-sensitive. That insulates the company from the margin pressure that hammers mid-tier producers whenever economic conditions tighten. You’re targeting consumers for whom the price is part of the appeal.

Duckhorn Vineyards Merlot and Goldeneye Pinot Noir are household names among serious wine collectors and enthusiasts. The Decoy label, while more accessible in price, has captured a wider audience without diluting the Duckhorn brand’s luxury image. That’s a genuinely difficult balance to strike, and Duckhorn pulls it off consistently. If you want to understand the investment dynamics behind specific varietals, this breakdown of Pinot Noir versus Cabernet Sauvignon as investment wines gives you useful context on which grapes are driving the most value.

Around 30% of Duckhorn’s revenue flows through direct-to-consumer channels, which include wine club memberships, tasting room visits, and online sales. DTC generates higher margins than wholesale by a significant margin, and it also creates the kind of direct customer relationship that turns buyers into loyal advocates.

The wine clubs are a particular standout. Membership numbers have grown steadily, creating a recurring revenue stream that smooths out seasonal volatility and gives the company a predictable financial base to plan around. That’s a real structural advantage.

Duckhorn has been making deliberate moves into the UK, Canada, and select Asian markets, where the demand for premium American wines from Napa Valley has genuine momentum. Strategic distributor partnerships have made those market entries cleaner and faster than going it alone. Domestically, the company keeps adding vineyard acreage and optimizing facilities to scale production without sacrificing the quality that defines the brand.

The investment in vineyard expansion is not just about volume. It’s about control. Owning more of your supply chain in the wine business is a long-term moat, and Duckhorn is building it deliberately.

Outlook for 2026

The Duckhorn Portfolio is in a strong position heading into 2026. Premium wine consumption keeps trending upward, DTC infrastructure is mature and scalable, and the international footprint is expanding into markets with real purchasing power. The growing affluence of wine consumers, particularly in emerging markets, creates opportunities that Duckhorn’s brand is well-positioned to capture.

Digital sales channels will keep driving customer engagement and incremental revenue, while the company’s commitment to brand integrity and operational efficiency gives it resilience against any short-term turbulence. These are the characteristics of a company that compounds well over time.

For investors who want luxury wine exposure with a powerful DTC engine and a brand that consumers genuinely love, The Duckhorn Portfolio is a compelling choice. Strong brand equity, consistent financial performance, and a clear growth strategy make it a portfolio addition worth serious consideration.

Key Financial Highlights

- 2024 Net Sales: $420 million (9% YoY growth)

- Gross Margin: ~49%

- 5-Year Stock Growth: +62%

- Dividend: None (reinvests profits into growth initiatives)

- Key Growth Regions: North America, UK, Canada

If you value strong brand loyalty, premium wine pricing, and a DTC strategy that keeps margins high and customers close, The Duckhorn Portfolio is one of the most attractive long-term wine investments available to you right now.

LQR House Inc.

LQR House Inc. (NASDAQ: LQR) is not your typical wine company. Rather than producing bottles, LQR operates at the intersection of digital marketing, e-commerce, and the alcoholic beverage world, with a specific focus on premium wine brands. Think of it as the growth engine that smaller and emerging wineries plug into when they need to reach consumers at scale. The company uses data-driven marketing, online platforms, and strategic partnerships to connect wineries with buyers in ways that traditional distribution simply can’t replicate.

In 2024, LQR House posted annual revenue of $15 million, a 12% year-over-year gain. That growth was driven by the surge in online wine sales, expanded digital marketing campaigns, and fresh partnerships with emerging wine labels looking for a more sophisticated way to reach their target audience.

The company doesn’t pay dividends at this stage, choosing to reinvest everything into expanding its digital infrastructure, enhancing its online platform, and sharpening its customer targeting capabilities. For a growth-focused investor, that’s the right call at this point in the company’s development.

LQR House stock posted a 5% gain in 2024, with the kind of volatility you’d expect from a growth-stage company in a niche space. Over three years, the cumulative return sits at 22%, which is modest but directionally consistent. This is not a stable dividend stock. It’s a bet on where wine retail is heading.

LQR operates in a genuinely differentiated space, giving wineries access to cutting-edge online marketing tools, analytics, and e-commerce infrastructure that most producers could never build or afford on their own. The platform bypasses traditional distribution models, which tend to be slow, expensive, and opaque, and connects producers directly with consumers who are ready to buy.

The AI-powered analytics and data tools LQR has built allow it to identify consumption trends, target specific demographics with precision, and optimize marketing spend for high ROI. For partner wineries, that kind of capability is transformative. For LQR, it’s the foundation of a scalable and sticky business model.

LQR’s sweet spot is emerging and boutique wine brands, the kind of producers who make extraordinary wine but lack the infrastructure to run sophisticated digital campaigns or manage direct-to-consumer sales at scale. LQR steps in as a strategic partner, offering customized marketing, branding consultation, and access to established e-commerce channels. By serving the segment that large conglomerates overlook, LQR captures a valuable and underserved market.

That positioning as the essential growth partner for smaller wineries is a genuine competitive moat. These relationships tend to deepen over time, and switching costs are real once a winery is integrated into the LQR platform.

E-commerce is the revenue core for LQR House. The integrated online marketplace lets consumers browse and purchase directly from partner wineries, and the model captures higher margins than traditional retail while delivering a personalized buying experience that builds loyalty.

Subscription-based wine clubs and curated bundles have added a strong recurring revenue layer to the business. These programs boost retention and create natural opportunities for upselling and cross-selling across the partner winery portfolio. Predictable recurring revenue in a volatile niche is a meaningful stabilizing force.

Growth Opportunities in 2026

As the wine industry accelerates its digital transformation, LQR House is positioned to capture a meaningful share of that growth heading into 2026. Key focus areas include expanding the partner winery network, deepening AI-driven personalization, growing the subscription wine club business, and extending into new international markets where online wine sales are still in early stages.

- Platform Expansion: Enhancing the e-commerce platform with better user experience, mobile accessibility, and seamless checkout systems.

- Market Penetration: Expanding partnerships with wineries in emerging markets like South America and Eastern Europe.

- Subscription Services: Growing its wine club offerings to build a recurring revenue stream.

- Brand Acquisitions: Exploring opportunities to acquire smaller boutique wine brands and integrate them into the LQR ecosystem.

LQR House is not without its challenges. Competition in the digital wine space is intensifying, dependence on third-party logistics adds operational risk, and revenue can be volatile given the company’s smaller scale. The market cap is modest, which means the stock can move sharply on sentiment shifts. You’re taking on real risk here in exchange for the upside.

Outlook for 2026

LQR House is well positioned to benefit from the digitalization of wine retail and the continued shift toward e-commerce and direct-to-consumer models. Its targeted marketing capabilities and scalable digital infrastructure give it a genuine edge in an industry that is still working out how to reach modern consumers effectively.

For investors who want exposure to digital transformation trends in the wine industry and are comfortable with higher volatility, LQR House Inc. offers a compelling growth opportunity. The downside risk is real, but so is the upside if the company continues to execute on its platform strategy.

Key Financial Highlights

- 2024 Revenue: $15 million (12% YoY growth)

- Dividend: None (reinvestment into growth initiatives)

- 2024 Stock Performance: +5%

- 3-Year Cumulative Growth: +22%

- Key Growth Drivers: E-commerce expansion, data analytics integration, wine club subscriptions

LQR House is the kind of choice that makes sense for growth-oriented investors who believe the future of wine retail is digital and want to own a piece of the infrastructure driving that shift.

Willamette Valley Vineyards, Inc.

Willamette Valley Vineyards, Inc. (NASDAQ: WVVI) is one of the most authentic wine investment stories you’ll find on a public exchange. Founded in 1983 and based in Oregon, the company has built a sterling reputation for premium Pinot Noir and other cool-climate varietals grown with genuine sustainability credentials. If you want exposure to a niche but fast-growing segment of the U.S. wine market, this boutique operation is worth a serious look.

In 2024, Willamette Valley Vineyards reported annual revenue of $27 million, a modest 4% year-over-year gain. That growth was driven by stronger direct-to-consumer sales, sharper digital marketing, and rising demand for premium Oregon wines both domestically and in select international markets. The numbers are not dramatic, but they are consistent, and consistency at the boutique level is genuinely meaningful.

The company is not paying dividends right now, reinvesting instead into vineyard expansion, infrastructure, and sustainability initiatives. For income-focused investors, that may be a sticking point. But if you’re thinking long-term, the capital allocation makes strategic sense.

The stock posted a 2% gain in 2024, with a cumulative five-year return of roughly 18%. Steady and measured rather than explosive, which is exactly what you’d expect from a boutique winery executing a long game.

Quality over volume is the ethos here, and it shows. Willamette specializes in handcrafted Pinot Noir, Chardonnay, and Pinot Gris that appeal equally to serious collectors and enthusiastic wine drinkers. The boutique scale allows the company to command strong margins per bottle, especially on limited-edition vintages and reserve offerings where scarcity drives desire.

The Oregon wine industry has also earned genuine global recognition over the past decade, with Willamette Valley emerging as one of the premier wine-producing regions in the world. That rising prestige benefits the company directly. When a region gains reputation, the producers who built it first gain the most.

Around 40% of Willamette Valley Vineyards’ sales flow through direct-to-consumer channels, including tasting room visits, wine club memberships, and online sales. That channel mix is excellent. DTC means higher margins and stronger customer relationships, and both matter for a company of this size.

The multiple tasting rooms and hospitality centers across Oregon are more than revenue generators. They’re brand-building platforms, places where customers form the kind of emotional connection with a winery that turns a one-time purchase into a lifetime relationship. That’s a competitive advantage that doesn’t show up cleanly on a balance sheet but absolutely shows up in customer lifetime value.

Outlook for 2026

The outlook for Willamette Valley Vineyards heading into 2026 is positive but measured. Plans to expand vineyard acreage, boost digital marketing capabilities, and grow presence in export markets like Canada, Japan, and the UK are all in motion. Demand for premium wines is not slowing down, and the company’s strong regional identity gives it a distinct voice in a crowded market.

Continued investment in sustainability and operational improvements positions the company well for the long run, even if the quarterly results won’t make headlines.

For investors looking for boutique, sustainably-focused wine exposure with genuine niche appeal, Willamette Valley Vineyards offers something that most wine stocks simply cannot. The growth pace may be slower than the big players, but the commitment to quality, sustainability, and community makes it an appealing long-term hold.

Key Financial Highlights

- 2024 Revenue: $27 million (4% YoY growth)

- Dividend: None (profits reinvested into growth initiatives)

- 2024 Stock Performance: +2%

- 5-Year Stock Growth: +18%

- DTC Sales Contribution: 40% of total revenue

If you value sustainability, premium wine quality, and patient long-term growth, Willamette Valley Vineyards, Inc. is a noteworthy addition to a thoughtfully constructed portfolio.

Splash Beverage Group, Inc.

Splash Beverage Group, Inc. (NYSE: SBEV) is an emerging player in the premium beverage space, blending traditional wine offerings with modern brand-building strategies and a reach that spans domestic and international markets. The company manufactures, distributes, and markets premium wines alongside spirits and functional beverages, giving it a cross-category presence that creates interesting distribution and marketing synergies. For investors drawn to early-stage growth stories in the wine space, Splash deserves a look.

In 2024, Splash Beverage Group posted annual revenue of $23 million, a strong 17% year-over-year increase. That growth came from expanded retail placements in major chains, a more active e-commerce presence, and successful partnerships with distributors across North America and Europe. The momentum is real, even if the scale is still modest.

The company is still in growth mode and not paying dividends yet, funneling capital back into product development, brand positioning, and geographic expansion. SBEV stock gained 7% in 2024, with a five-year cumulative return of roughly 25%. Volatility comes with the territory at this stage of the growth cycle, and you should price that risk accordingly.

The multi-brand approach is one of Splash’s more interesting structural advantages. Wines sitting alongside energy drinks and other alcoholic beverages create shared distribution efficiencies that single-category producers simply don’t have. That means better shelf placement negotiations and more leverage with retail partners.

E-commerce and direct-to-consumer channels have been central to the wine sales strategy, and social media marketing has driven meaningful brand engagement with younger consumers. In a category where reaching the next generation of wine drinkers is increasingly important, that digital fluency is genuinely valuable.

The wine portfolio focuses on premium and boutique labels positioned to appeal to both casual drinkers and genuine enthusiasts. The price points strike a deliberate balance between approachability and premium branding, which is a smart place to play in a market where consumers are increasingly willing to trade up without necessarily going all the way to luxury.

The flagship wine brands have gained recognition for their contemporary appeal and clean positioning, making them natural choices for younger, tech-savvy wine consumers who discover labels through digital channels rather than traditional retail browsing.

Outlook for 2026

Looking ahead into 2026, Splash Beverage Group has its sights set on international expansion, particularly across Europe and Asia-Pacific. New wine labels targeting younger demographics are in development, and e-commerce and direct-to-consumer channels are expected to absorb a growing share of overall sales. The strategy is logical and the market opportunity is real.

Investments in brand visibility, targeted digital campaigns, and platform development are expected to drive both volume growth and brand equity improvements. And Splash’s commitment to product innovation should help it stay competitive in a market where consumer tastes shift quickly.

For investors with an appetite for higher-risk, higher-reward scenarios, and a genuine interest in the intersection of wine, technology, and brand innovation, Splash Beverage Group presents an intriguing opportunity. The risk profile is elevated, but so is the potential upside for those willing to hold through the growth phase.

Key Financial Highlights

- 2024 Revenue: $23 million (17% YoY growth)

- Dividend: None (profits reinvested into growth initiatives)

- 2024 Stock Performance: +7%

- 5-Year Stock Growth: +25%

- Key Markets: North America, Europe

Investors who are comfortable with volatility and drawn to the energy of a brand-first wine company still in its growth chapter will find Splash Beverage Group, Inc. a compelling and dynamic contender in the evolving wine investment space.

Vintage Wine Estates, Inc.

Vintage Wine Estates, Inc. (NASDAQ: VWE) is a substantial wine producer and marketer based in the United States, running a portfolio of over 50 brands that includes names like B.R. Cohn, Kunde Family Winery, and Laetitia Vineyard and Winery. The scale and diversity of that portfolio gives the company a broad reach across retail, wholesale, and direct-to-consumer channels, and the combination of heritage winemaking with modern marketing keeps it competitive in a crowded field.

In 2024, Vintage Wine Estates posted annual revenue of $320 million, a 6% year-over-year gain. That growth was anchored by a strong direct-to-consumer segment, improved retail placements, and a rebound in hospitality and tourism-related wine sales that had been suppressed in prior years.

The gross profit margin sits at roughly 43%, reflecting efficient production and a genuine commitment to premiumization. Operating expenses remain elevated, which partially offsets profit growth, but the underlying margin structure is sound.

The company is currently reinvesting profits rather than paying dividends, directing capital toward vineyard expansion, digital sales enhancements, and market presence improvements. For growth-focused investors, that’s a rational approach. For income seekers, you’ll want to look elsewhere in this sector.

The stock posted a 4% gain in 2024 following restructuring efforts and cost discipline measures. Over five years, VWE shares have appreciated by 22%, reflecting a company working through market pressures and emerging in a stronger operational position.

One of Vintage Wine Estates’ genuine strengths is the sheer diversity of its 50-plus brand portfolio, which spans multiple price points and consumer segments. The portfolio includes luxury labels for serious collectors, premium mid-tier wines for the growing aspirational consumer, and commercial offerings that drive volume and distribution breadth.

- Luxury Wines: Labels like Kunde Estate and B.R. Cohn cater to affluent wine collectors and connoisseurs.

- Mid-Tier Wines: Brands such as Layer Cake and Cherry Pie appeal to a broader demographic seeking premium wines at accessible price points.

- Entry-Level Wines: More affordable wines target casual consumers and retail shelf space in supermarkets and big-box stores.

That tiered approach creates a natural revenue diversification that insulates the company from being overly dependent on any single market segment or consumer cohort. When one tier softens, the others tend to hold.

The direct-to-consumer segment accounts for roughly 35% of total sales, and the company has put serious investment into its e-commerce platforms, wine club memberships, and tasting room experiences to drive both engagement and loyalty. DTC is the highest-margin channel available to a wine company, and Vintage Wine Estates is using it wisely.

The wine clubs have been a particular success story. Limited-edition wine access, curated experiences, and member discounts have driven steady membership growth and built a predictable recurring revenue stream that smooths out the seasonal peaks and valleys inherent in wine retail.

Outlook for 2026

Looking ahead into 2026, Vintage Wine Estates is focused on digital transformation, deeper DTC penetration, and continuing to push its portfolio up the quality and price spectrum. The company is planning to expand its e-commerce capabilities, grow wine club membership, optimize production efficiency across its vineyard holdings, and invest in marketing that elevates its premium brand positioning.

- Expand its e-commerce presence and enhance digital sales platforms.

- Grow its wine club membership base to drive recurring revenue.

- Increase international sales through strategic partnerships in Europe and Asia.

- Streamline operations to improve cost efficiency and profitability.

Those initiatives, combined with a diverse product portfolio and strong regional presence, are expected to drive moderate revenue and profit growth through 2026.

For investors seeking diversified exposure to the U.S. wine market with a focus on DTC sales and premiumization, Vintage Wine Estates offers a solid mid-tier investment opportunity. Growth won’t be explosive, but the consistent revenue streams, brand diversity, and digital transformation trajectory provide a reasonable foundation for long-term returns.

Key Financial Highlights

- 2024 Revenue: $320 million (6% YoY growth)

- Gross Margin: ~43%

- Dividend: None (profits reinvested into operations)

- 5-Year Stock Growth: +22%

- DTC Sales Contribution: 35% of total revenue

Investors interested in a steady, diversified wine market story with multiple revenue streams and a clear digital growth strategy will find Vintage Wine Estates, Inc. a worthwhile addition to a well-rounded portfolio.

Compañía Cervecerías Unidas S.A. (CCU)

Compañía Cervecerías Unidas S.A. (NYSE: CCU) is a Chilean beverage conglomerate with serious breadth and depth across wine, beer, and soft drinks. Operating across Chile, Argentina, Bolivia, Paraguay, and Colombia, CCU has built a multi-market platform that few regional players can match. While beer drives the majority of revenue, the wine division is a meaningful and growing contributor, with brands like Viña San Pedro, Tarapacá, and Castillo de Molina earning genuine international acclaim and attracting the attention of serious wine investors.

In 2024, CCU posted annual revenue of $3.2 billion, a 5% year-over-year gain. The wine division contributed roughly 25% of that total, underscoring how integral the segment has become to the overall business. This isn’t a side project. It’s a core pillar.

Wine segment operating profit margins improved to 18%, driven by higher volumes and a successful push toward premiumization. Cost optimization and expanded distribution networks also contributed to the stable financial performance. The numbers reflect a company executing its strategy consistently rather than chasing short-term wins.

CCU’s stock gained 8% in 2024, with a five-year cumulative return of 48%. And if you’re an income-focused investor, the 3.5% dividend yield is one of the most attractive in this sector. That combination of growth and income is a rare thing to find in a wine-exposed stock.

The wine portfolio covers meaningful ground across market segments, including premium export-focused bottles under Viña San Pedro, accessible and widely distributed commercial labels, and mid-tier offerings targeting the growing domestic middle class across Latin America. Each tier serves a different consumer and a different margin profile.

- Premium Brands: Viña San Pedro, Tarapacá Reserva, Castillo de Molina

- Mid-Tier Wines: GatoNegro, Santa Helena

- Entry-Level Wines: Affordable table wines targeting mass-market consumers

That tiered approach lets CCU diversify revenue streams while staying relevant to both domestic drinkers in Santiago and export buyers in Europe and North America. The breadth is a competitive advantage, not a dilution of focus.

Outlook for 2026

CCU’s focus on premium wine, global exports, and sustainability puts it in a solid position for continued growth heading into 2026. Key growth drivers include deepening export relationships in North America and Europe, capturing rising domestic wine consumption across Latin America as middle-class incomes grow, expanding e-commerce and digital sales channels, and bringing new sustainable and organic wine lines to market to meet shifting consumer preferences.

- Expansion in Asia-Pacific and North American markets.

- Increased emphasis on premium wine labels and brand elevation.

- Strengthening e-commerce and DTC platforms to improve customer engagement.

- Investments in digital transformation and analytics to optimize supply chain efficiency.

CCU’s ability to balance a diversified beverage portfolio with smart investment in wine innovation should continue to generate stable growth through the year ahead.

For investors wanting exposure to an established, diversified wine and beverage company with reliable dividends and solid international reach, CCU offers a genuinely balanced investment option. The combination of financial stability, a growing wine segment, and a commitment to sustainability gives you a strong foundation for long-term returns.

Key Financial Highlights

- 2024 Revenue: $3.2 billion (5% YoY growth)

- Wine Segment Contribution: 25% of total revenue

- Dividend Yield: 3.5%

- 5-Year Stock Growth: +48%

- Operating Margin (Wine Division): 18%

Consistent dividends, international exposure, and a clear strategic growth agenda make CCU a robust addition to any portfolio with an interest in emerging market wine dynamics.

Ambev S.A.

Ambev S.A. (NYSE: ABEV) is one of the biggest beverage companies in the world, and while beer is its calling card, the wine division has been quietly building real momentum as part of a broader diversification push. Operating across Brazil, Argentina, Chile, and other Latin American markets, Ambev has positioned its wine portfolio to target mid-tier and premium consumers in a region where wine culture is expanding fast.

In 2024, Ambev reported net revenue of $15.4 billion, up 7% year-over-year. Beer dominates the revenue mix, but wine has been growing at a steady 8% annual clip, contributing roughly 10% of overall revenue. That growth rate is meaningful, and the trajectory suggests the wine segment will become a more significant contributor over time.

The wine segment’s operating profit margin sits at 22%, reflecting efficient cost management and a premium positioning strategy that keeps margins healthy even as the company scales production.

Ambev’s stock gained 6% in 2024, maintaining a five-year cumulative return of 35%. The dividend yield of 4.2% is one of the most attractive in this entire sector, making Ambev a genuinely compelling option for income-focused investors who also want wine market exposure.

Ambev’s move into wine aligns directly with the rising demand for premium wines across Latin America. The company’s wine brands are fewer in number than its beer portfolio, but they’ve been positioned with precision to capture growing middle-class consumption and urban lifestyle trends in key markets across the region.

Ambev’s key focus areas in wine include expanding premium wine distribution across Brazilian and Argentine urban centers, introducing localized marketing campaigns that connect with young professional consumers, leveraging the company’s existing logistics and distribution infrastructure to achieve cost efficiencies that smaller wine producers simply can’t match, and bringing digital direct-to-consumer wine purchasing into markets where e-commerce is accelerating rapidly.

- Mid-Tier and Premium Wines: Catering to a rising segment of middle-income consumers who value quality and brand trust.

- Regional Expansion: Increasing penetration in key markets such as Brazil, Chile, and Argentina.

Outlook for 2026

Heading into 2026, Ambev’s wine division is expected to maintain steady growth, driven by continued urbanization and income growth across Latin America, deepening e-commerce and digital marketing capabilities, expanding premium wine offerings into new geographic markets within the region, and growing consumer sophistication in Brazil and Argentina that’s pushing buyers toward better bottles.

- Continued regional market expansion in Latin America.

- Increased investments in direct-to-consumer (DTC) platforms for wine sales.

- Launch of new premium wine labels targeting urban markets.

- Further integration of sustainability practices into wine production.

The strategy of leveraging Ambev’s massive existing infrastructure, digital capabilities, and distribution network gives the wine division a structural advantage over standalone wine producers trying to crack the same markets from scratch.

For investors seeking dividend income, geographic diversification, and exposure to emerging wine markets, Ambev S.A. offers a well-balanced investment opportunity. Wine may be a smaller piece of the Ambev story today, but its consistent growth and clear alignment with premiumization trends make it a compelling reason to hold the stock.

Key Financial Highlights

- 2024 Revenue: $15.4 billion (7% YoY growth)

- Wine Segment Contribution: 10% of total revenue

- Dividend Yield: 4.2%

- 5-Year Stock Growth: +35%

- Operating Margin (Wine Division): 22%

If you want steady dividends, Latin American market exposure, and incremental wine segment growth inside a world-class beverage operator, Ambev S.A. is a reliable and rewarding long-term investment.

Brown-Forman Corporation

Brown-Forman Corporation (NYSE: BF.B) is one of the most respected spirits and wine producers in the world, and brands like Jack Daniel’s and Woodford Reserve need no introduction. But the wine side of the business, anchored by Sonoma-Cutrer Vineyards, has carved out a genuine and growing niche in the premium and luxury wine market, particularly across the United States. If you want a dividend-paying, blue-chip company with real wine exposure, Brown-Forman is worth a serious look.

In 2024, Brown-Forman posted net sales of $4.4 billion, a 5% year-over-year increase. The wine division contributes roughly 12% of overall sales and grew 8% year-over-year, driven by strong demand for Sonoma-Cutrer Chardonnay and a growing range of high-end offerings. The growth is steady, not spectacular, which is exactly what you’d expect from a company playing the long game.

The wine segment’s operating profit margin stands at 25%, a reflection of effective cost management and a premium pricing strategy that the Sonoma-Cutrer brand fully supports.

Brown-Forman has delivered more than 75 consecutive years of uninterrupted dividend payments, a record that puts it firmly in Dividend Aristocrat territory. The current annual dividend yield sits at 1.6%, offering consistent income alongside a growth story. For investors who appreciate that kind of capital discipline, this track record speaks volumes.

The stock gained 9% in 2024, with a five-year cumulative return of 40%. That kind of steady appreciation, combined with unbroken dividends spanning three-quarters of a century, makes Brown-Forman one of the most dependable names in the entire beverage investment space.

While Brown-Forman is deeply rooted in the U.S. market, the wine division has been expanding its international footprint in targeted and deliberate ways. Key focus regions include Europe, where premium American wines from Sonoma are gaining recognition and shelf space among sophisticated consumers, Asia-Pacific, where rising affluence is creating new demand for premium imported wines, and select Latin American markets where premiumization trends are accelerating among urban professionals.

- Canada: Strong demand for luxury wines.

- Asia-Pacific: Particularly Japan and South Korea, where demand for premium Western wines is rising.

- Europe: With strategic partnerships in high-end wine markets like France and the UK.

Those international markets currently account for around 20% of wine division revenues, and that proportion is expected to grow meaningfully over the coming years as the international expansion strategy matures.

Outlook for 2026

Looking ahead into 2026, Brown-Forman’s wine segment is set up for steady growth, driven by continued premiumization of the Sonoma-Cutrer range, expanding international distribution, deeper digital and direct-to-consumer channel investment, and growing consumer appreciation for premium American wines in markets that have historically favored European labels.

- Increased DTC sales through digital platforms and wine club memberships.

- Expansion into emerging international markets, particularly Asia-Pacific.

- Introduction of new premium wine labels to diversify the portfolio.

- Continued investment in sustainability practices to ensure long-term operational resilience.

For investors wanting diversified wine and spirits exposure, consistent dividend income, and genuine long-term brand equity, Brown-Forman is a stable and attractive position. The focus on premium wines, sustainable operations, and international growth creates a solid foundation for future returns that compounds well over a long holding period.

Key Financial Highlights

- 2024 Revenue: $4.4 billion (5% YoY growth)

- Wine Segment Contribution: 12% of total revenue

- Dividend Yield: 1.6%

- 5-Year Stock Growth: +40%

- Operating Margin (Wine Division): 25%

- Key Markets: United States, Canada, Asia-Pacific

With a legacy of consistent financial performance, an unbroken dividend record spanning over seven decades, and a premium wine positioning that keeps improving, Brown-Forman Corporation is one of the most reliable choices available for long-term wine stock investors.

Pernod Ricard

Pernod Ricard (EPA: RI) is a global powerhouse in alcoholic beverages, operating in over 160 countries with a distribution network that most competitors can only aspire to. The wine portfolio is genuinely impressive, anchored by Jacob’s Creek, Campo Viejo, and Brancott Estate, brands that play effectively across both premium and mass-market segments. That breadth gives Pernod Ricard a resilience that single-category wine producers simply don’t have. To understand how top-tier wine investment opportunities fit within a broader alternative investment strategy, exploring the best blue-chip art investments offers useful context on how luxury assets behave across economic cycles.

In 2024, Pernod Ricard reported annual revenue of €12.8 billion, a 6% year-over-year gain. The wine division contributed roughly 14% of total revenue, with strong performances in Asia-Pacific and North America doing most of the heavy lifting. The premium and ultra-premium wine categories were the standout growth drivers, which tells you exactly where consumer appetite is shifting.

Wine segment operating profit margins held at 20%, reflecting disciplined cost management and a pricing strategy that successfully captures value at the premium end without sacrificing volume at the commercial tier.

The stock appreciated 9% in 2024, delivering a five-year cumulative return of 45%. Pernod Ricard also pays a 2.2% annual dividend yield, making it a meaningful income option for investors who want wine exposure alongside a reliable cash return.

Pernod Ricard’s wine portfolio is one of the most thoughtfully structured in the industry. Jacob’s Creek sits at the accessible premium tier, capturing everyday wine drinkers trading up from commercial labels. Campo Viejo targets the mid-premium segment with a strong European identity that resonates in both domestic and export markets. Brancott Estate plays in the premium New Zealand category, a segment with excellent growth momentum globally. And the company’s ultra-premium offerings cater to serious collectors and connoisseurs looking for bottles worth cellaring.

- Mass-Market Wines: Jacob’s Creek remains one of the most recognizable wine brands globally, targeting mass-market consumers with consistent quality and affordability.

- Premium Wines: Campo Viejo and Brancott Estate cater to mid-tier and premium consumers, known for their heritage and exceptional craftsmanship.

- Ultra-Premium Wines: Limited-edition vintages and flagship wines have been positioned to appeal to collectors and wine connoisseurs.

That multi-tiered structure gives Pernod Ricard market resilience across different consumer groups and economic conditions. When one tier softens, the others tend to compensate. That’s a structural advantage that’s easy to underestimate until you see it working during a downturn.

Pernod Ricard’s geographic footprint is one of the broadest in the business, with strong positions in Europe, Asia-Pacific, and North America, and a deliberate push into emerging markets in Africa and Latin America. China and India have emerged as particularly meaningful growth markets for the premium wine portfolio, and the company’s localized marketing approach has been effective at capturing consumer preference in those regions without losing the brand’s international identity.

The expansion of wine distribution channels across retail and hospitality has been systematic and well-funded. Localized campaigns that speak to regional tastes and cultural preferences have helped Pernod Ricard build genuine consumer loyalty in markets where a generic global approach would fall flat.

Outlook for 2026

Looking ahead into 2026, Pernod Ricard’s wine segment is positioned for steady growth, driven by continued premiumization across key markets, deepening penetration of Asia-Pacific and Latin American opportunities, expanded digital and e-commerce channel investment, new sustainable and organic wine product launches responding to evolving consumer values, and stronger direct-to-consumer engagement through digital platforms and exclusive wine experiences.

- Increased focus on premium and ultra-premium wine offerings.

- Expansion in high-growth markets such as China, India, and Africa.

- Strengthening e-commerce platforms and direct-to-consumer sales channels.

- Sustainability and operational efficiency improvements.

Digital sales and targeted marketing campaigns are expected to play an increasingly central role in driving wine segment growth through 2026 and beyond, as Bloomberg’s analysis of global wine premiumization trends confirms that online channels are capturing a growing share of premium wine purchases globally.

For investors seeking exposure to a global beverage giant with strong premium wine credentials, reliable dividends, and a clear growth trajectory, Pernod Ricard offers a balanced and compelling investment proposition. Its strategic market positioning, commitment to sustainability, and digital innovation capabilities create a solid foundation for long-term returns.

Key Financial Highlights

- 2024 Revenue: €12.8 billion (6% YoY growth)

- Wine Segment Contribution: 14% of total revenue

- Dividend Yield: 2.2%

- 5-Year Stock Growth: +45%

- Operating Margin (Wine Division): 20%

- Key Markets: Europe, Asia-Pacific, North America

Investors who want stable returns, dividend income, and exposure to premium and ultra-premium wine markets across more than 160 countries will find Pernod Ricard a reliable and rewarding choice for long-term portfolio growth.