In 2026, the fine wine market is no longer defined solely by geography or vintage. It’s increasingly shaped by the sensory spectrum of dry wine versus sweet wine. For investors, collectors, and industry analysts, this isn’t just a stylistic divide. It’s a question of allocation strategy, liquidity, aging trajectory, and ROI.

Dry wine has long been the darling of sommeliers and serious cellars, dominating premium allocations especially in the red wine segment. Iconic labels like Château Lafite Rothschild, Sassicaia, and Gaja Barbaresco set the benchmark for long-term capital appreciation, often gaining 7 to 12% annually in secondary markets.

Their dryness, coupled with complex tannins and long aging curves, has positioned them as core components in any wine-based portfolio strategy.

Sweet wines, though, are no longer just dessert pairings. They’ve gained renewed attention among collectors seeking undervalued assets with historical prestige and limited production. Regions like Sauternes, Tokaj, and the German Auslese and Trockenbeerenauslese appellations have seen a 42% increase in auction volume since 2020, driven especially by Asian and Eastern European buyers.

Rare vintages of Château d’Yquem and Egon Müller Rieslings now routinely cross six-figure thresholds, revealing an overlooked niche with asymmetric upside potential.

With global demand for wine forecast to grow at a 4.6% CAGR through 2030, and fine wine increasingly recognized as a hedge against inflation and fiat depreciation, understanding the difference between dry and sweet wines goes well beyond palate preference. For serious investors, it’s become a portfolio imperative.

Table of Contents

What Makes a Wine Sweet or Dry?

The distinction between dry wine and sweet wine comes down to one core metric: residual sugar, or RS. That’s the unfermented natural grape sugar left in the wine after fermentation completes. Simple chemistry on the surface, but the implications for market positioning, pricing elasticity, aging potential, and collector behavior are anything but simple.

In a dry wine, fermentation runs nearly to completion. Yeast converts almost all of the grape’s natural sugars into alcohol, leaving minimal residual sugar, typically under 4 grams per liter. These wines tend to feature higher acidity, structured tannins in reds, and a palate that leans into minerality, spice, and earthy complexity rather than overt fruit or sweetness.

Dry wines dominate in regions like Bordeaux, Tuscany, Burgundy, and Rioja, where tradition and food compatibility have long dictated stylistic choices.

Sweet wines, by contrast, retain significant residual sugar, ranging from around 20 g/L in lighter off-dry styles to over 150 g/L in botrytized or late-harvest varieties. The method of achieving that sweetness varies widely. Some wines come from overripe or shriveled grapes, as with Trockenbeerenauslese. Others rely on grapes affected by noble rot, as in Sauternes and Tokaji. And some use interrupted fermentation to halt sugar conversion, as with Moscato d’Asti.

Each of these processes demands precision viticulture and typically yields lower production volumes, which adds genuine scarcity value to the top labels.

For investors, this chemical difference matters more than most realize. Dry wines age along tannin and acid structure, developing tertiary notes that are highly prized at auction. Sweet wines use sugar as a natural preservative, making them some of the longest-lived wines in existence. Top vintages of Sauternes or Tokaji can mature gracefully for 50 to 100 years.

Dry Wine vs Sweet Wine: Grape Characteristics

The difference between dry wine and sweet wine begins not just in the winery but in the vineyard itself. Ripeness at harvest, sugar concentration, acidity levels, and fermentative behavior all play a role. For investors and serious collectors, understanding which grape varietals define each style is essential when evaluating both the longevity of a wine and its position in the market.

Knowing your varietals means knowing your holding period, your exit strategy, and your buyer. It’s that foundational.

Dry Wine Grapes

Dry wines rely on varietals with moderate to low sugar accumulation and a natural tendency to ferment fully. These grapes typically exhibit high acidity or tannic structure, both of which preserve the wine through long-term cellaring and increase its viability at auction over time.

- Cabernet Sauvignon: The cornerstone of most investment-grade dry reds. Known for thick skins, firm tannins, and aging potential that often exceeds 20–30 years in top vintages. Bordeaux First Growths, Napa cult wines, and Super Tuscans derive much of their value from Cabernet’s cellar strength and global brand appeal.

- Nebbiolo: Native to Piedmont, Nebbiolo underpins Barolo and Barbaresco wines. High in both acidity and tannin, it ages into complex, highly collectible wines. Auction sales of Giacomo Conterno and Gaja demonstrate 15–18% annualized ROI on rare vintages.

- Syrah: Particularly from Hermitage or Côte-Rôtie, Syrah creates dry wines with deep spice, earthiness, and remarkable ageworthiness. Rare bottlings from producers like Jean-Louis Chave have shown consistent value growth over the last decade.

- Chardonnay: On the white wine side, dry Chardonnay—especially from Burgundy’s Grand Cru vineyards—dominates the high-end white wine investment category. Domaine Leflaive and Coche-Dury routinely break the $5,000 per bottle threshold, driven by scarcity and global demand.

Sweet Wine Grapes

Sweet wines depend on varietals that retain sugar at high ripeness, often with skin structures that can tolerate botrytis cinerea, or noble rot, as well as late harvesting. Their ability to balance sugar with acidity is the key to both flavor and longevity.

- Sémillon: The backbone of Sauternes, often blended with Sauvignon Blanc. When affected by noble rot, it produces intensely sweet wines with high viscosity and honeyed complexity. Top vintages of Château d’Yquem have appreciated up to 300% over 20 years, outperforming some red Bordeaux benchmarks.

- Furmint: Used in Hungary’s Tokaji Aszú, this grape delivers exceptional sugar-acid balance and oxidative complexity. Vintage Tokajis from István Szepsy and Disznókő now fetch $500–$3,000 per bottle, particularly for 5 and 6 Puttonyos classifications.

- Riesling: In Germany and Austria, late-harvest or botrytized Rieslings (Auslese, Beerenauslese, Trockenbeerenauslese) command strong prices, especially from producers like Egon Müller or J.J. Prüm. The top Riesling lots have outperformed even top Burgundy whites in appreciation over the past five years.

- Muscat and Zibibbo: Used in fortified and unfortified sweet wines, especially in Pantelleria and Southern France. While often lower in absolute price, rare bottlings with historic provenance have seen 40–60% appreciation in boutique markets.

From a purely investment perspective, dry wine grapes dominate broader portfolio allocations because of their wider global appeal and stronger liquidity. But select sweet wine grapes, especially those tied to legacy producers, offer strong asymmetric returns for collectors willing to invest in rarity, age, and story. If you want to explore how varietal-driven investment choices play out in practice, the comparison between Pinot Noir and Merlot is a useful reference point.

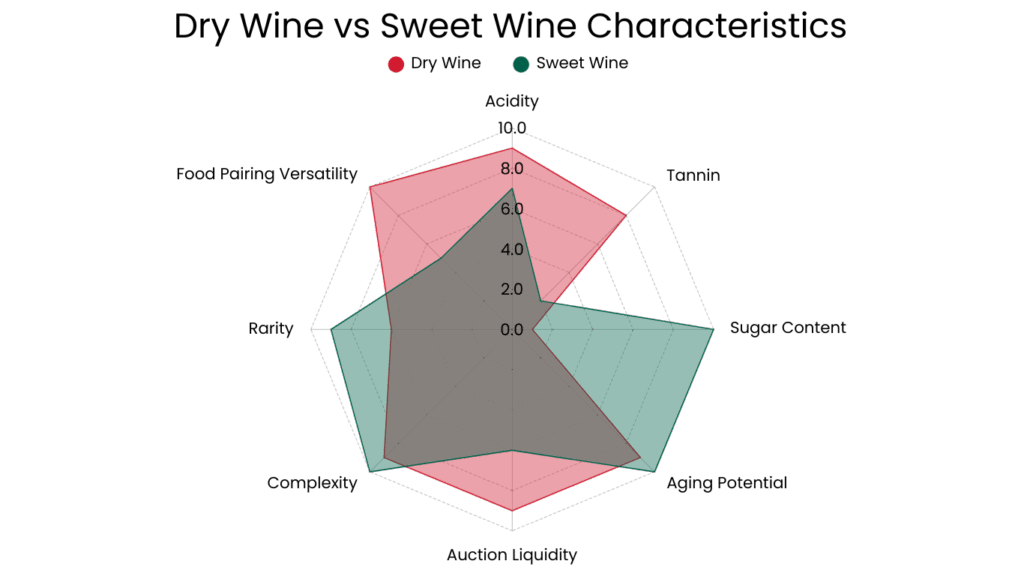

Dry Wine vs Sweet Wine: Appearance, Aromas, and Tasting Notes

The sensory profile of a wine isn’t just an aesthetic experience. It directly shapes market appeal, collector desirability, food pairing versatility, and, in many cases, auction performance.

Understanding how dry wine and sweet wine differ in appearance, aromatic structure, and tasting evolution gives investors and connoisseurs real insight into why certain wines command premium pricing and long-term relevance.

Dry Wine

Dry wines are valued not only for their lack of sweetness but for their multidimensional aromatic complexity. In top examples, sweetness is replaced by layers of minerality, savory tones, and subtle fruit evolution. These wines often display restrained power in youth, opening into profoundly expressive profiles over decades in the cellar.

- Appearance: Dry reds such as aged Barolo or Bordeaux often show garnet hues with brick-like rims as they mature, indicating oxidation and tertiary development. Dry whites, especially aged Chardonnays or Rieslings, transition from pale gold to deep amber, depending on age and barrel influence.

- Aromas: Dry reds exhibit aromas of dried cherry, tobacco leaf, leather, cedar, graphite, and spice. The nose is often subtle in youth and becomes more open with aging. Dry whites offer notes of flint, lemon pith, hazelnut, wet stone, and butter (in oak-aged variants).

- Palate: Tasting profiles lean toward structure over sweetness—with high acidity, complex tannin interplay, and layered finishes. Wines like Côte-Rôtie or Grand Cru Burgundy often reveal a long, savory finish, low sugar perception, and food pairing precision. This adaptability makes them a staple on tasting menus and collector tables.

For investors, those characteristics drive broad secondary market interest, especially in vintages that allow gradual aromatic development over time.

Sweet Wine

Sweet wines, when well-made, are never cloying. They’re balanced by vibrant acidity and aromatic lift. At their best, they deliver unmatched depth, viscosity, and concentration of fruit and botrytis-derived notes. Their sensory signature makes them ideal for vertical tastings, long-term cellaring, and celebratory consumption.

- Appearance: Sweet wines often present as deep gold, amber, or even copper, particularly when aged. The viscosity is immediately visible in the glass, with slow-moving legs and density on the swirl.

- Aromas: Leading sweet wines like Château d’Yquem or Tokaji Aszú exude aromas of honeycomb, dried apricot, candied orange peel, saffron, almond, and noble rot (botrytis). These profiles are unmatched in aromatic concentration and are considered luxurious sensory experiences in their own right.

- Palate: Rich yet balanced, with unfermented sugars offset by high acid or oxidative complexity. Exceptional examples provide a multi-layered finish that can persist for over 60 seconds. Unlike simplistic sweet table wines, these wines offer a collector-level complexity that places them among the most age-worthy wines ever produced.

From an investment standpoint, sweet wines tend to outperform on rarity and aging curve rather than global mainstream appeal.

Their intensity and exotic profile create niche but high-value demand, especially across Asia and Central Europe where gifting culture and dessert wine pairings fuel acquisition at the premium level. According to the Financial Times, fine wine gifting in Asian markets has become one of the strongest drivers of price appreciation in niche appellations.

Dry Wine vs Sweet Wine: Pricing

In fine wine markets, pricing is not solely dictated by production cost or critic score. It reflects demand elasticity, vintage scarcity, aging potential, and brand mythology. The price gap between dry wine and sweet wine is real, but it’s also widely misunderstood.

Each category holds its own hierarchy of value, but they behave very differently in primary versus secondary markets, especially when it comes to volume turnover and price ceiling performance.

Dry Wine Pricing

Dry wines from benchmark regions have long commanded higher average prices, supported by global liquidity, cross-market recognition, and inclusion in institutional wine portfolios.

- First Growth Bordeaux (e.g., Château Margaux, Lafite Rothschild): Entry-level releases for recent vintages typically begin around $650–$900 per bottle, with top vintages (e.g., 2009, 2010, 2016) trading well above $1,200–$3,000+ per bottle on the secondary market.

- Grand Cru Burgundy (e.g., Domaine de la Romanée-Conti, Armand Rousseau): Pricing starts at $2,000–$15,000 per bottle, with older vintages and rare plots like La Tâche exceeding $50,000 at auction. Burgundy’s micro-parcel production drives per-bottle scarcity, even in high-volume vintages.

- Super Tuscans and Napa Cult Wines (e.g., Sassicaia, Screaming Eagle): Top-rated vintages range between $300–$4,000, depending on release year and critic score. Napa’s recent inclusion in Liv-ex benchmarks has pushed prices up 18% between 2021 and 2024.

Price stability in the dry category is high. Volatility tends to be confined to release year fluctuations, weather-driven vintage variation, and global macro shifts. Liquidity stays consistently strong, which is why dry wines are a favored option for short to medium-term resale strategies.

Sweet Wine Pricing

Sweet wines tend to trade at a discount relative to dry wines, despite equal or greater aging potential. That undervaluation is often tied to limited table-pairing versatility and a smaller global buyer base. But certain legacy producers have broken through that ceiling and now offer some of the best long-term ROI in wine.

- Château d’Yquem (Sauternes): Primary market pricing ranges from $250–$600 per 750ml bottle, with top vintages (e.g., 2001, 2005, 2011) selling between $800 and $3,000 on the secondary market. Magnum formats and historic vintages (pre-1950s) have sold for $8,000–$25,000 at major auctions.

- Tokaji Aszú (Hungary): While 5 Puttonyos bottles start as low as $70, rare 6 Puttonyos and Eszencia vintages from producers like Szepsy or Royal Tokaji reach $500–$2,500, particularly for bottles with aging provenance. These wines are still considered undervalued relative to their quality and aging ability.

- German TBA Rieslings (e.g., Egon Müller, J.J. Prüm): Among the few sweet wines to consistently outperform dry counterparts. A 375ml of Egon Müller Trockenbeerenauslese 2003 sells for over $6,000, with annual appreciation rates that rival top Burgundy whites.

The sweet wine category is also highly vintage-sensitive. Small production runs, often under 5,000 bottles, lead to sharp upward price movement as older vintages disappear from the market entirely. Liquidity is lower and resale cycles are longer, which makes sweet wines far more attractive for long-hold strategies or legacy cellaring.

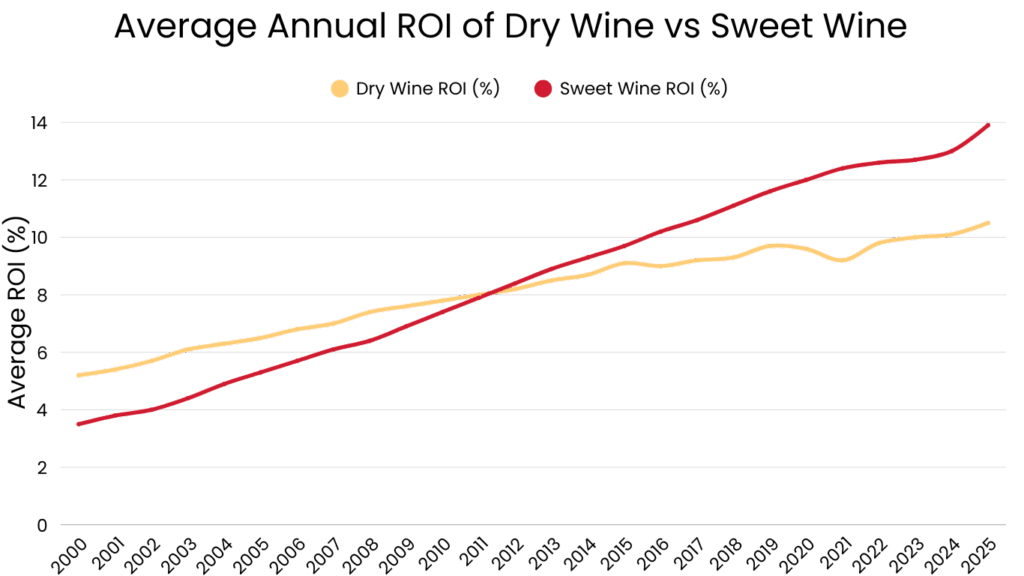

Dry Wine vs Sweet Wine: Historical ROI

Dry wines have traditionally anchored most portfolio models. But sweet wines, especially those from historically significant appellations, have quietly outperformed expectations for years, often delivering high compounding returns well below the radar.

Dry Wine ROI

Dry wines dominate secondary markets and wine indices like Liv-ex 100 and the Liv-ex Bordeaux 500, largely because of their trading volume, auction regularity, and broad collector base. That liquidity translates into consistent performance metrics and real ease of entry and exit for investors.

- First Growth Bordeaux: Over the past 15 years, Lafite Rothschild and Château Margaux have shown compound annual growth rates (CAGR) between 6.5% and 9.3%, with specific vintages (like 2000, 2005, 2010) appreciating over 200% from release price to 2024 auction sales.

- Burgundy Grand Crus: The standout performers. Domaine de la Romanée-Conti wines have delivered 10–15% CAGR for rare vintages, with some bottles appreciating over 500% in the past decade, fueled by tightening supply and exploding global demand, particularly from Asia.

- Napa Cult Wines: Screaming Eagle, Harlan Estate, and Scarecrow have shown 7–12% annualized growth, though with higher vintage volatility and stronger correlation to critic scores and domestic market sentiment.

These wines offer a strong ROI profile paired with short to mid-term liquidity, making them ideal for funds, wealth management firms, and private investors seeking reliable capital growth through tangible assets. If you’re thinking about how fine wine fits alongside other alternative assets, understanding how art market trends are evolving in 2026 offers a useful parallel.

Sweet Wine ROI

Sweet wines have historically been treated as undervalued anomalies, coveted by connoisseurs but overlooked by institutional collectors. But those who have studied their performance over decades know that top-tier sweet wines offer some of the highest risk-adjusted returns in the entire wine category.

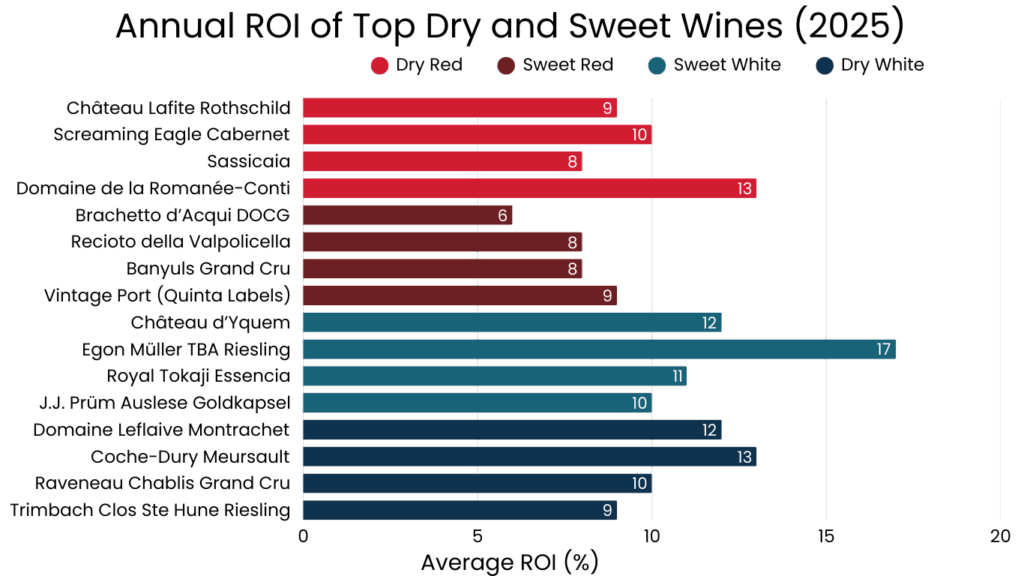

- Château d’Yquem: Widely regarded as the crown jewel of Sauternes, top vintages (like 1975, 1990, 2001) have demonstrated CAGR of 9–14%, particularly in large formats and older vintages with pristine provenance. Some 19th-century bottles have returned over 1,000% since their last documented sales.

- Egon Müller TBA Rieslings: These are among the top five performing wines globally in ROI over 20 years. With ultra-low production volumes (often under 150 bottles per vintage), their scarcity drives prices upward with every passing year. The 2005 TBA sold at auction in 2023 for over $13,000 per 375ml, marking a 17% CAGR since release.

- Tokaji Aszú (6 Puttonyos and Eszencia): Vintages from Royal Tokaji and Szepsy have shown 8–11% average annual returns, with limited production, aging potential, and growing collector interest from the EU and Asia pushing demand upward.

Unlike dry wines, sweet wines behave more like long-term compounding assets. They appreciate steadily, driven by rarity and aging potential, but they require a patient holding period and strategic liquidation timing, often through specialty auctions or private placement.

Best Sweet Red Wines to Invest In (2026 Outlook)

Best Sweet Red Wines to Invest In (2025 Outlook)

Best Dry Red Wines to Invest In (2026 Outlook)

Best Dry Red Wines to Invest In (2025 Outlook)

Best Sweet White Wines to Invest In (2026 Outlook)

Best Sweet White Wines to Invest In (2025 Outlook)

Best Dry White Wines to Invest In (2026 Outlook)

Best Dry White Wines to Invest In (2025 Outlook)

Which Is Better for Investment: Dry Wine vs Sweet Wine?

In 2026, determining whether dry wine or sweet wine offers better investment potential hinges less on stylistic preference and more on fundamentals. Liquidity, price behavior, aging dynamics, and market demand across collector classes are what drive the answer.

Both categories carry genuine historical significance. But they serve very different roles within a portfolio, and confusing the two is where most amateur investors go wrong.

Dry wines are the dominant asset class in fine wine investment. They’re supported by global trading infrastructure, frequent appearances on wine indices like Liv-ex, and broad consumer recognition. Bordeaux First Growths, Burgundy Grand Crus, and cult Napa Cabernets aren’t just collector trophies. They’re portfolio anchors.

These wines trade actively, appreciate predictably, and offer exit optionality across private sales, online platforms, and global auctions. Holding periods are flexible and performance, often 7% to 12% annually for top names, is both well-documented and institutionally validated.

Sweet wines, by contrast, are long-duration asymmetric bets. They don’t move on quarterly critic scores or restaurant demand. They move on scarcity, provenance, and historical weight. Wines like Château d’Yquem, Egon Müller TBA, and Royal Tokaji Essencia are rarely traded in volume, but when they do change hands, they often outperform red wine benchmarks over 20-plus year periods.

Their markets are thinner, but the upside is steep, especially in rare formats and exceptional vintages that disappear from circulation entirely.

Sweet wines reward patience. They aren’t built for flipping. They’re built for compounding. Their structure, high sugar, high acid, botrytis concentration, makes them biologically suited for multi-decade cellaring, a trait that very few dry wines can match. Just as principal investing rewards long-term conviction over short-term activity, sweet wine investment follows the same logic.

Dry wines dominate headlines and indices. But the quiet appreciation of aged sweet wines is often what delivers the most impressive ROI per bottle held over time.

So, which is better? The honest answer is that it’s not a binary choice. It’s a strategic one.

For liquidity, frequent turnover, and allocation by wine funds, dry wine wins. Full stop.

For long-term, low-supply, legacy positioning with high rarity leverage, sweet wine is in a category of its own.

The most sophisticated portfolios in 2026 aren’t built around one style. They’re calibrated across both, using dry wines for capital rotation and sweet wines for long-term value capture. According to Bloomberg’s coverage of alternative asset allocation, collectors who blend both styles consistently outperform single-category strategies over a decade or more.

FAQ

Which is better, dry or sweet wine?

For investment, dry wine offers higher liquidity and global market turnover. For long-term appreciation and rarity-driven value, sweet wine delivers better asymmetrical ROI, especially in older vintages and niche formats.

What are the benefits of sweet wine?

Sweet wines offer longer aging potential, low volatility, and high rarity premiums. Top-tier labels like Château d’Yquem and Egon Müller are prized by collectors for their complexity, cellar endurance, and auction performance.

Is sweet wine less expensive than dry wine?

Generally, yes. Sweet wines have lower entry prices, but rare vintages can surpass dry wines in value when provenance and aging align. Top Sauternes and Tokaji Essencia can fetch thousands per half bottle.

Do sweet wines age longer than dry wines?

Yes. The natural sugar and acidity in sweet wines act as preservatives, allowing them to age 50–100 years or more, outperforming most dry wines in cellar longevity.

What is the best dry wine for investment?

Top performers include Domaine de la Romanée-Conti, Screaming Eagle, Château Lafite Rothschild, and Sassicaia—all with high auction turnover and price resilience.

What is the best sweet wine for investment?

Elite bottles include Château d’Yquem, Egon Müller TBA, Royal Tokaji Essencia, and J.J. Prüm Goldkapsel—known for exceptional ageability and rising international collector demand.