The Greek property market has been one of the most closely watched real estate stories in Europe over the past few years. What was once considered a distressed market during the debt crisis is now attracting some of the world’s most active investors.

In 2025, Greece has firmly positioned itself as a hotspot for both private buyers and institutional capital, with demand showing no signs of slowing.

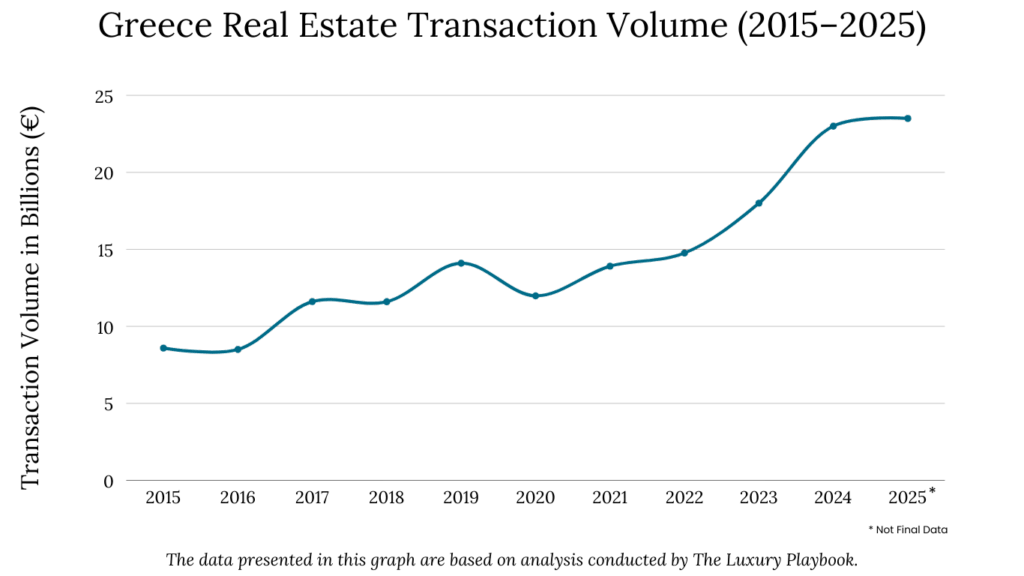

The momentum is not just speculative—it is backed by structural shifts in the economy, tourism growth, and international investor confidence. According to the Bank of Greece, residential property prices rose by 13.4% year-on-year in 2024, continuing a trend of double-digit growth that started in 2022.

This is especially striking when compared to many Western European markets, where price growth has slowed or even reversed due to rising interest rates.

Global investors are paying attention. From pension funds exploring commercial assets in Athens to high-net-worth individuals buying luxury homes in Mykonos and Crete, capital inflows are broadening. The Hellenic Statistical Authority reported more than €2.1 billion in foreign direct investment in Greek real estate in 2024, the highest figure since records began.

As George Chrysochoidis, a leading Athens-based developer, recently commented, “Greece is no longer seen as a recovery market. It’s now seen as a growth market with strong fundamentals.”

For investors, this means Greece is not just a lifestyle-driven destination but also a serious opportunity for long-term returns.

Table of Contents

Historical Performance of the Greek Real Estate Market

To understand why investors are so confident in Greece today, it helps to look back at how far the market has come in just over a decade. During the Greek debt crisis (2009–2016), property prices collapsed by nearly 42% nationwide, according to the Bank of Greece.

This made it one of the hardest-hit real estate markets in Europe, with many homeowners selling at deep losses and developers halting projects.

However, the downturn also reset valuations and created an entry point for long-term investors. Since bottoming out in 2017, the market has staged a powerful recovery. Residential property prices have climbed more than 75% between 2017 and 2024, with prime areas in Athens and Thessaloniki often doubling in value.

This rebound has not been a quick bubble-like spike but a steady upward trend supported by tourism growth, foreign demand, and gradual economic stability.

Rental yields have also followed the same path. In central Athens, gross rental yields that were once hovering around 3% in 2015 have now risen to 5–6% in 2024, especially in neighborhoods that attract both expats and tourists.

Islands like Santorini and Mykonos have recorded even stronger figures, with short-term holiday rentals delivering returns of 7–8% during peak seasons.

Industry experts highlight that this recovery is more than just cyclical. As Savvas Savvaidis, CEO of Greece Sotheby’s International Realty, noted in a recent interview, “The Greek real estate market is now on a sustainable growth path, and international buyers see the long-term fundamentals as very compelling.”

This historical turnaround has set the stage for the confidence we see today. Rather than fearing past volatility, investors are recognizing that Greece’s recovery has laid the groundwork for sustainable growth in the 2020s.

Current Property Prices and Growth Trends in Greece

Greece’s real estate market has entered 2025 with strong momentum. According to the Bank of Greece, residential property prices rose by 13.4% in 2023, followed by another 11% increase in 2024, marking the fastest pace of growth since before the financial crisis.

Unlike the speculative surges seen in some European hotspots, this growth has been supported by real demand, particularly from international buyers and high-income Greeks returning to the market.

In Athens, prime neighborhoods such as Kolonaki, Glyfada, and Kifisia are leading the charge, with average prices now exceeding €4,500 per square meter for luxury apartments. By comparison, these areas were closer to €2,200–€2,500 per square meter in 2016, showing how much recovery and wealth inflows have reshaped the capital’s housing market.

Thessaloniki has also become a strong investment hub, with average property prices rising by nearly 10% annually in the past three years, fueled by new infrastructure projects and a growing student and expat population.

On the islands, demand remains heavily tourism-driven: in Mykonos and Santorini, prime villas can command more than €10,000 per square meter, with limited supply keeping prices elevated.

The transaction volume tells the same story. The Greek Land Registry reported over 20% more property sales in 2024 compared to 2022, a clear sign of both domestic and international confidence. Meanwhile, foreign direct investment in Greek real estate surpassed €2.3 billion in 2024, reflecting the continued draw of the Golden Visa program and Greece’s strategic appeal as a lifestyle and investment destination.

Rental yields remain attractive, with long-term urban leases averaging 4–5%, while short-term Airbnb-style rentals often deliver 6–8% returns in tourist-heavy locations.

For investors, this combination of rising prices and solid income streams underlines why the Greek property market is seen as both a safe haven and a growth play in 2025.

Key Drivers Behind the Greek Property Market Boom

The surge in Greece’s property market is not happening in isolation. It is being fueled by a mix of economic, political, and social factors that together create a strong foundation for growth.

One of the most important drivers is economic recovery. After more than a decade of hardship following the debt crisis, Greece has recorded steady GDP growth — 2.5% in 2023 and 2.2% in 2024, according to Eurostat. This stability has improved consumer confidence and increased demand for residential housing from local buyers, who are finally regaining purchasing power.

Another critical factor is foreign capital inflows. The Greek Golden Visa program has been a magnet for international investors, particularly from China, the Middle East, and Europe. By the end of 2024, Greece had issued over 20,000 residency permits through property investment, injecting billions into the housing market.

For many, Greece’s €250,000 minimum investment threshold (€800.000 for Athens, Thessaloniki, Mykonos & Santorini) remains one of the most accessible residency-by-investment schemes in Europe.

The country’s booming tourism industry is also a major contributor. Greece welcomed more than 33 million tourists in 2024, setting a new record. This influx has fueled demand for short-term rentals, second homes, and holiday villas, particularly on islands like Mykonos, Santorini, and Crete. Investors know that as long as Greece remains a top global travel destination, rental demand will remain resilient.

Infrastructure upgrades are further strengthening the market. Major projects, such as the redevelopment of the Ellinikon Project in Athens, are reshaping entire neighborhoods and boosting property values nearby. Similarly, new transportation links, like airport expansions and improved ferry networks, are making islands and regional cities more accessible, broadening the appeal of real estate beyond Athens.

Finally, geopolitical stability compared to other Mediterranean regions adds to Greece’s attractiveness. Investors see the country not only as a lifestyle destination but also as a relatively safe environment for capital in an increasingly uncertain global market.

Taken together, these drivers show why Greece’s property surge is built on fundamentals, not speculation.

Rental Yields and Income Potential for Investors

One of the biggest questions for investors entering the Greek property market is whether strong price growth is matched by attractive rental income. The answer, backed by recent numbers, is largely yes. According to the Bank of Greece, average gross residential yields stood at 4.6% in Q2 2025, slightly down from 4.8% in late 2024. This level is competitive compared to many Western European cities, where prime rental yields often sit below 3%.

Urban hubs like Athens and Thessaloniki continue to offer dependable long-term rental demand from students, professionals, and expatriates. Here, yields typically range between 3.8% and 5.5%, depending on micro-location and property quality. For example, centrally located apartments in Athens often achieve higher yields due to both rental demand and limited supply.

Holiday rentals add another layer of opportunity. With Greece welcoming a record 40.7 million visitors in 2024 and generating over €21 billion in travel receipts, demand for short-term accommodation is booming. In popular tourist destinations such as Crete, Mykonos, and Santorini, gross yields of 6–8% are achievable, and best-in-class villas can exceed that when occupancy rates are carefully managed.

Of course, investors need to run their numbers conservatively. Short-term rentals involve cleaning, management fees, and seasonal variability. Factoring in these costs, net yields may be lower, but properties that appeal to both tourists and long-term tenants offer more resilience.

Why the Greek Property Market Is Not a Bubble

Every time real estate prices climb at a double-digit pace, the word “bubble” starts to surface. Yet in Greece’s case, the fundamentals suggest the growth is sustainable rather than speculative.

According to the Bank of Greece, residential property prices rose by 11.2% year-on-year in Q1 2025, following a 13.4% increase in 2024. While these gains are significant, they are still grounded in real demand rather than debt-driven speculation.

One key factor is supply. Greece has one of the lowest construction rates in Europe, with only 16,000 new housing permits issued in 2024, far below pre-crisis averages of more than 70,000 per year in the early 2000s. This lack of new builds means that rising demand from both domestic buyers and foreign investors is not being matched with equivalent supply. Scarcity, not speculation, is keeping prices elevated.

Foreign investment inflows also underpin sustainability. In 2024, foreign buyers injected €2.1 billion into Greek real estate, marking a 30% increase compared to 2023. Much of this is linked to Greece’s Golden Visa program, which remains one of the most attractive in Europe.

Unlike bubbles fueled by cheap credit, this demand is largely cash-based and therefore more resilient to interest rate changes.

Furthermore, rental demand is strong, especially in urban and tourist-heavy areas. As long as investors can secure gross yields between 4% and 7%, the market remains anchored by income potential rather than purely speculative price appreciation.

As real estate analyst Nikos Charalambous commented in a recent report, “What we’re seeing in Greece is not a bubble, but a rebalancing after a decade of undervaluation. Prices are catching up to European norms, not inflating beyond them.”

Risks Investors Should Consider in Greek Real Estate

While the Greek property market looks strong and far from bubble territory, no investment comes without risks. For investors, understanding these challenges is crucial to making informed decisions.

One of the biggest concerns is interest rate pressure. Although the European Central Bank began easing rates in mid-2025, borrowing costs are still higher than the ultra-low levels seen during the 2010s. Mortgage rates in Greece currently average 4.2%, compared to 2.1% in 2019.

This could limit domestic buyer activity and slow demand growth, particularly in middle-class housing segments.

Another risk lies in geopolitical volatility. Greece is strategically positioned but remains exposed to regional tensions in the Eastern Mediterranean. Political shifts within the EU or instability in neighboring countries could affect investor sentiment and tourism flows—both of which are central to the property market.

Tourism itself is another double-edged sword. While it has been a key driver of demand, making up nearly 25% of Greece’s GDP, any disruption—such as global recessions, climate-related travel restrictions, or over-tourism regulations—could affect short-term rental profitability.

Finally, there is the question of valuation risks in prime areas. Hotspots like Athens’ city center and Santorini have seen price increases of 40–50% since 2020, raising concerns that some micro-markets may be overheating. Investors need to differentiate between genuinely sustainable locations and those at risk of plateauing.

In short, while Greece offers attractive returns, investors should factor in interest rate sensitivity, geopolitical risks, and regional valuation disparities when building their strategy. Those who approach the market with careful due diligence are likely to enjoy more stable, long-term gains.