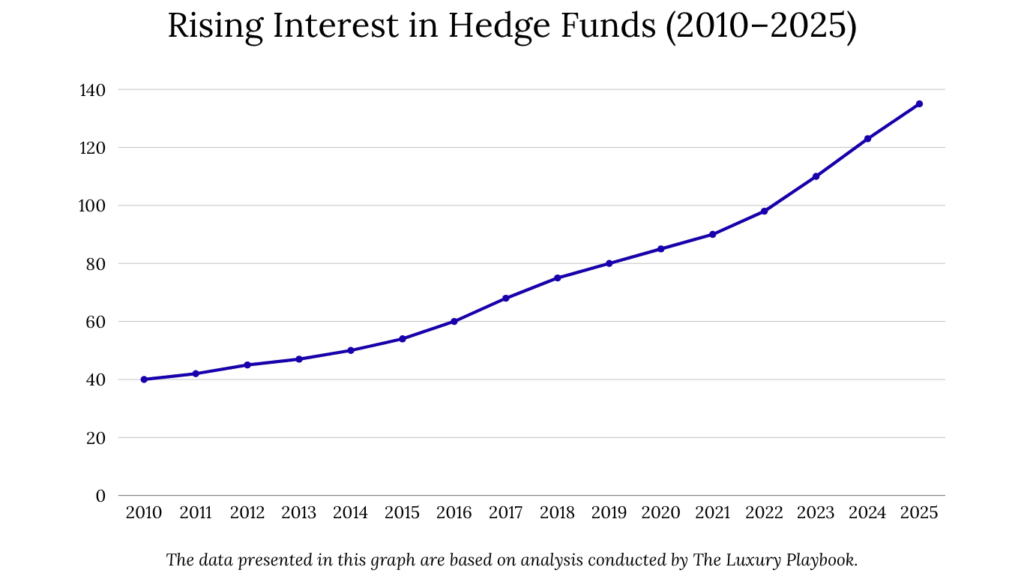

Hedge funds have long been viewed as exclusive investment vehicles for the financial elite—but that’s no longer entirely true. In 2025, more investors are gaining access to hedge funds than ever before. However, access doesn’t automatically mean success.

The real challenge lies in choosing the right fund—one that aligns with your goals, risk tolerance, and financial strategy.

Whether you’re a high-net-worth individual seeking portfolio diversification, or a seasoned investor aiming to optimize returns through active management, understanding how hedge funds work is essential. These funds use complex strategies—like long/short equity, global macro, or quantitative models—to pursue alpha, often in ways traditional funds can’t.

But with complexity comes responsibility. Between opaque fee structures, limited liquidity, and high minimums, the hedge fund world isn’t one to walk into blindly.

Table of Contents

What Is a Hedge Fund and How Does It Work?

A hedge fund is a private investment vehicle that pools capital from accredited investors to pursue returns using a wide range of strategies. Unlike mutual funds, which are publicly accessible and tightly regulated, hedge funds are more flexible — but also more complex and often riskier.

At their core, hedge funds aim to generate positive returns regardless of market direction. To do this, managers might go long on undervalued stocks, short overvalued ones, trade derivatives, speculate on interest rates, or even invest in cryptocurrency or distressed assets.

This flexibility is one reason why many hedge funds have historically delivered strong returns during both bull and bear markets.

To invest in a hedge fund, you typically need to be an accredited investor — meaning you meet certain income or net worth thresholds (e.g., $1 million in assets or $200,000 in annual income for individuals). These funds are not designed for everyday retail investors, largely due to their complexity and risk profile.

Most hedge funds follow a limited partnership structure. Here’s how it usually works:

- The fund manager acts as the general partner, making investment decisions.

- Investors come in as limited partners, contributing capital.

- The manager earns a management fee (usually 2% of assets) and a performance fee (commonly 20% of profits).

This is often referred to as the “2 and 20” model, and while controversial due to its high cost, it remains the industry standard.

As Paul Singer, founder of Elliott Management, once said: “Performance fees should only exist if there’s true outperformance — otherwise it’s just expensive asset gathering.”

Many hedge funds also include features like a lock-up period (when investors can’t withdraw capital) and high-water marks (ensuring managers only earn performance fees on new profits).

| 🧾 Feature | 💡 Description |

|---|---|

| 🏛️ Accredited Status | Must meet income/net worth criteria ($1M net worth or $200k/year income) |

| ⏳ Lock-up Period | Time frame during which withdrawals aren’t allowed |

| 🧮 High-Water Mark | Fees only apply on new profits above the previous peak |

| 📈 Fee Structure | “2 and 20” model: 2% AUM + 20% performance fees |

| 🔁 Strategy Freedom | Long/short equity, crypto, distressed assets, global macro, etc. |

In summary, hedge funds operate with fewer constraints than traditional investments, giving them the freedom to pursue a broader range of opportunities. This can lead to impressive returns — but also demands careful due diligence from investors.

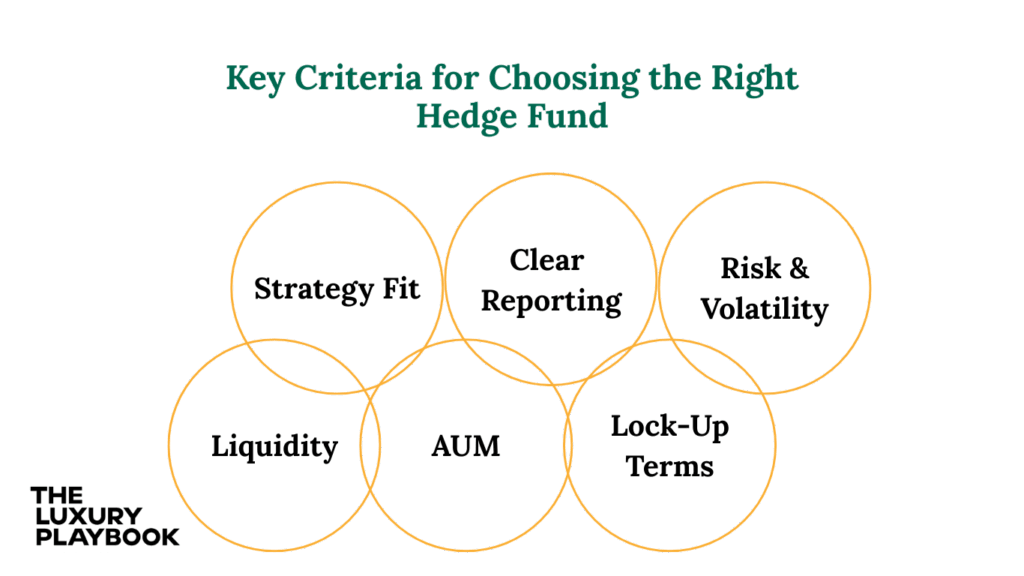

Key Criteria for Choosing the Right Hedge Fund

Choosing the right hedge fund isn’t just about chasing returns — it’s about finding a strategy, manager, and structure that fits your overall financial goals and risk appetite. With thousands of hedge funds operating globally, filtering the right ones comes down to a few essential factors.

1. Strategy Fit

Before anything else, you need to understand how the fund makes money. Is it long/short equity, macro, quantitative, credit, or event-driven? Some strategies thrive in volatile markets, others during periods of stability.

Ask yourself: Does this fund’s investment style align with how I want to grow or protect my capital?

For instance, if you’re looking for diversification away from equities, a global macro or credit fund might make more sense than a fund focused on tech stocks.

2. Risk and Volatility

Don’t just look at returns. Focus on risk-adjusted returns — how much risk the fund took to achieve its performance. Tools like the Sharpe ratio are key here. A fund with a Sharpe ratio above 1 is generally considered efficient.

Also consider maximum drawdown — how much the fund has fallen from its peak. If you can’t stomach a 20% drop in a bad quarter, that’s important to know upfront.

3. Liquidity and Lock-Up Terms

Some hedge funds let you redeem quarterly, others might require your capital to stay locked for a year or more. This is known as the lock-up period, and it varies widely.

Check if the redemption policy matches your liquidity needs. Do you have flexibility with your capital, or do you need access within a certain timeframe?

4. Assets Under Management (AUM)

Size can matter — but bigger isn’t always better. A hedge fund with over $5 billion AUM might signal stability and a proven track record. But sometimes smaller, boutique funds can be more agile and opportunistic.

That said, if a fund is managing just a few million, do more due diligence. Look at how much of the fund is seeded by the manager (skin in the game) and how long it’s been operating.

5. Transparency

Top funds provide clear reporting, regular investor updates, and full access to performance history. If a fund is vague about its process or won’t provide documentation, that’s a red flag.

As Ray Dalio of Bridgewater Associates puts it: “Transparency breeds trust.”

Important Hedge Fund Strategies

One of the first things to understand when evaluating hedge funds is that they don’t all play by the same rules. In fact, their biggest strength is flexibility. Hedge fund managers have the freedom to pursue a wide range of investment strategies—some aggressive, others cautious—depending on the fund’s goals and market outlook.

Let’s walk through the most common strategies you’ll encounter and what kind of investor each might appeal to.

Long/Short Equity

This is one of the most popular hedge fund approaches. The idea is simple: buy stocks you believe are undervalued (long) and sell those you think are overpriced (short). The goal is to profit whether the market goes up or down.

These funds can perform well in turbulent markets, but success hinges on the manager’s stock-picking ability. According to a 2024 analysis from Preqin, long/short equity funds returned an average of 7.8% annually over the past five years, outperforming many traditional equity funds.

As billionaire investor Steve Cohen puts it: “You need to have the ability to see what the market is missing. That’s where alpha lives.”

Global Macro

Global macro funds look at the big picture. They invest based on broad economic trends—interest rates, inflation, geopolitical events, and currency movements. Because these funds can move across asset classes (stocks, bonds, currencies, commodities), they’re often used by investors seeking diversification with high upside potential.

In 2022, for example, global macro strategies were among the top-performing hedge fund categories during market volatility, with many posting double-digit returns as they capitalized on rising rates and energy price shocks.

Event-Driven

Event-driven strategies focus on opportunities created by corporate events—mergers, acquisitions, spin-offs, or bankruptcies. These funds make money by predicting the outcome of these events and positioning themselves accordingly.

Two common sub-strategies:

- Merger arbitrage: Profiting from the price difference between a target company’s current share price and the acquisition offer.

- Distressed investing: Buying the debt or equity of companies in trouble, hoping for a turnaround.

These funds don’t rely as much on market trends, which makes them a good hedge in uncertain environments.

Quantitative (Quant)

Quant hedge funds rely on math, algorithms, and data models to drive their trades. Everything is numbers-driven—from identifying opportunities to executing trades. Some quant funds operate at high speed, using machine learning and predictive analytics to act in fractions of a second.

Renaissance Technologies, often cited as the most successful quant hedge fund in history, famously avoids media but consistently delivers returns that have made it a legend in the space.

If you’re someone who trusts data over gut feeling, quant strategies can be appealing—but they’re also highly complex and often hard to access for the average investor.

Market Neutral

Market-neutral funds try to remove overall market exposure. They balance long and short positions so that gains (or losses) aren’t driven by whether the market is rising or falling. Instead, returns come from the manager’s ability to pick winners and losers on both sides.

These strategies appeal to conservative investors who value stable returns with lower volatility. In a low-growth or sideways market, market-neutral funds can quietly outperform more aggressive peers simply by preserving capital.

How to Evaluate a Hedge Fund Manager

Choosing the right hedge fund is as much about who’s managing it as it is about the strategy itself. A great manager doesn’t just follow market trends—they anticipate them. They make smart decisions under pressure, communicate transparently, and manage risk like a professional chess player, always thinking a few moves ahead.

One of the first things to look at is the manager’s track record. Not just returns in a bull market, but how they performed during downturns. Did they protect capital when markets crashed? Did they bounce back quickly?

Historical data over multiple market cycles can offer valuable clues about consistency, resilience, and adaptability. According to a 2024 study by BarclayHedge, hedge funds led by managers with 10+ years of experience outperformed newer funds by an average of 2.4% annually. That kind of edge matters.

Equally important is understanding the manager’s investment philosophy. Are they data-driven or more instinctive? Do they lean toward aggressive growth or focus on preserving capital?

A mismatch between your financial goals and their approach can lead to disappointment—even if the fund performs well on paper. For instance, a manager focused on long/short equity might generate double-digit returns, but if you’re seeking stable, low-volatility income, the experience could feel too bumpy.

Communication also plays a major role in building trust. Good managers are transparent about their process and keep investors informed. This means regular updates, honest performance reporting, and a willingness to answer questions—especially when things aren’t going perfectly. If a fund manager avoids questions or provides vague reports, that’s a red flag.

Another key consideration is how aligned the manager is with your interests. Do they have “skin in the game”? Managers who invest significant personal capital into their funds tend to be more motivated to protect and grow your investment.

It’s also worth checking whether the fund has a high-water mark provision—a built-in rule that ensures managers only earn performance fees if they surpass the fund’s previous peak value. This aligns incentives and protects you from paying fees on partial recoveries after losses.

In the end, evaluating a hedge fund manager is part numbers, part narrative. You want someone with a solid track record, a clear and compatible investment style, open communication habits, and an incentive structure that aligns with your success. Because when markets get unpredictable—and they always do—it’s the manager’s discipline and judgment that often make the difference between sustained returns and costly mistakes.

Typical Hedge Fund Fee Structures

| Fee Type | Description | Typical Range / Rate |

|---|---|---|

| Management Fee | An annual fee (commonly 2%) charged on assets under management (AUM), regardless of performance. | 1.5% – 2.5% |

| Performance Fee | A percentage of the fund’s profits (usually 20%) taken if the fund exceeds a benchmark. | 15% – 25% |

| High-Water Mark | Ensures performance fees are only charged on new profits above previous highs. | Yes (varies by fund) |

| Hurdle Rate | A minimum return the fund must generate before performance fees apply. | 5% – 8% |

| Redemption Fee | A charge applied when investors withdraw capital earlier than agreed upon. | 0.5% – 2% |

Important Risk Factors to Consider Before Investing

Investing in hedge funds can be rewarding, but it’s not without risks — and understanding those risks is crucial before you commit any capital. Hedge funds differ significantly from traditional investments like mutual funds or ETFs. They’re less regulated, use complex strategies, and often carry more volatility. That’s why knowing what you’re getting into matters just as much as the potential upside.

One of the most important metrics to assess risk is the Sharpe ratio. This tells you how much return you’re getting for each unit of risk. A higher Sharpe ratio means the fund is generating better returns relative to the level of risk it’s taking.

For example, a fund with a Sharpe ratio above 1.0 is generally seen as performing well on a risk-adjusted basis. It helps you compare funds more fairly — not just by their raw returns, but how efficiently they’re achieving them.

Another concept to pay attention to is drawdown — essentially, how much a fund’s value has declined from its peak during a tough period. A large drawdown can take years to recover from, so a fund’s ability to manage downside risk is just as important as its upside potential.

Then there’s the issue of liquidity and lock-up periods. Hedge funds often restrict when you can withdraw your money. Some require you to keep your investment locked up for a year or more, while others may only allow quarterly or semi-annual redemptions with advance notice. That means you need to be sure your cash flow needs align with the fund’s withdrawal policies.

It’s also worth noting that hedge funds may use leverage — borrowing capital to amplify returns. While this can boost gains in favorable markets, it also magnifies losses when things turn.

As billionaire investor Howard Marks puts it, “Leverage is neither good nor bad. It’s merely a tool. Whether it works for or against you depends on how you use it.”

Finally, consider the strategy-specific risks. A global macro fund may be sensitive to geopolitical shocks, while a quant fund might underperform during market anomalies. You’re not just choosing a fund — you’re choosing an approach to risk.

Legal and Regulatory Considerations for Investors

Before putting money into a hedge fund, it’s essential to understand the legal and regulatory framework that surrounds these types of investments. Hedge funds operate differently than mutual funds or ETFs — and that freedom comes with both opportunity and responsibility.

For starters, hedge funds are typically only open to accredited investors. That means individuals or institutions must meet certain wealth or income thresholds, as defined by the U.S. Securities and Exchange Commission (SEC).

As of 2025, this usually means having a net worth of over $1 million (excluding your primary residence) or earning more than $200,000 annually for the past two years.

Because hedge funds aren’t required to register under the Investment Company Act of 1940, they have fewer compliance obligations. This gives fund managers the flexibility to pursue more complex, aggressive strategies — but it also means you, the investor, need to do more due diligence.

One of the key terms to understand is the offering memorandum or private placement memorandum (PPM). This document outlines the fund’s strategy, risks, fee structure, and legal disclaimers. It’s your legal roadmap — and reading it carefully helps protect you from unpleasant surprises later. A good PPM should clearly explain your rights, responsibilities, and any restrictions on withdrawals or liquidity.

Another term you’ll come across is high water mark, which governs how performance fees are calculated. This rule ensures a fund manager only earns incentive fees on profits that exceed the fund’s previous highest value. It’s a way of keeping the fee structure fair and aligned with investor interests.

Then there’s AML/KYC compliance — anti-money laundering and know-your-customer regulations. Any legitimate hedge fund will require detailed documentation before you invest. This includes identity verification, proof of funds, and sometimes even background checks.

It might feel intrusive, but it’s a regulatory safeguard designed to prevent fraud and ensure the fund meets international compliance standards.

Finally, tax treatment is a key legal aspect. In the U.S., hedge fund gains are typically taxed as capital gains, but the exact outcome depends on the strategy used and how long you hold your investment. If the fund invests in short-term instruments, you could face higher ordinary income tax rates.

And if the fund operates offshore or through complex structures, the reporting requirements can get even more nuanced.

This is why many sophisticated investors work with legal and tax advisors before committing to a hedge fund.

Who Can Invest in a Hedge Fund?

Hedge funds aren’t open to just anyone. Whether you’re based in the U.S. or Europe, these investments are typically reserved for experienced or high-net-worth individuals—people who can handle risk and understand the complex strategies hedge funds often use.

In the United States, the term to know is “accredited investor.” To qualify, you usually need to meet at least one of the following:

- Have a net worth over $1 million, excluding your primary residence

- Earn $200,000 or more annually (or $300,000 with a spouse) for the past two years

- Be a qualified professional (like a director, partner, or employee at the hedge fund)

The idea is simple: hedge funds use riskier, more flexible strategies, so regulators want to ensure investors can afford potential losses.

In Europe, the rules vary by country, but the equivalent status is often called a “professional investor” under MiFID II (Markets in Financial Instruments Directive). To qualify, investors must meet at least two of the following three criteria:

- Have a financial portfolio of at least €500,000

- Work or have worked in the financial sector for at least one year in a professional capacity

- Make frequent transactions of significant size on relevant markets

In both regions, the logic is the same: hedge funds aren’t retail products. They’re meant for investors with the financial and technical capacity to understand the risks and the patience to commit capital—often for several years.

Even once you qualify, hedge funds set their own minimum investment thresholds, which can range from $100,000 to over $5 million, depending on the fund’s strategy and reputation. Some newer or niche funds may be more flexible, but top-performing funds typically require a substantial upfront commitment.

It’s also important to note that hedge funds often restrict withdrawals through lock-up periods and redemption terms, meaning you won’t have instant access to your money like you would with public stocks or ETFs.