Private credit has become indispensable in investors’ private market portfolios, offering alternative funding to SMEs not rated as investment grade. Unlike traditional banking, it comprises non-bank lending with customizable terms.

This financing serves as a potent diversification tool, counteracting the high correlation seen in public equities. With banks limited by regulations, the private credit space is ripe with opportunities.

Private debt strategies are now more tailored, focusing on direct investments and periodic income. This is appealing to investors looking for more control and predictable yields.

However, investing in private credit has its challenges, including regulatory and market risks. Thus, it necessitates thorough due diligence and strategic risk management. Only through careful analysis can investors maximize returns and minimize losses in this area.

Understanding Private Credit

Modern investors aim to diversify and seek enhanced returns through private credit. Unlike standard bank lending, private credit comes from non-bank entities. These lenders provide loans to companies often overlooked by traditional banks due to their ratings.

This segment’s growth is notable, as it offers flexibility and solutions specific to borrowers’ needs, a stark contrast to conventional banking.

Private Credit vs. Traditional Bank Lending

Private credit differs from bank lending in its adaptable loan arrangements. Post-financial crisis, banks, bound by strict regulations, have shown decreased enthusiasm for higher-risk loans.

In contrast, private lenders offer customized services, devising less rigid structures. They enjoy wider spreads—between 200 and 600 basis points over public market rates. This has led to a boom in direct lending, especially to mid-size firms.

Regulatory Changes and Market Opportunities

Banking regulations have shifted considerably since the 2008 crisis. Banks now prioritize safer loans, paving the way for private credit entities to thrive. These firms design specific strategies to cater to diversified sectoral needs, seizing market openings.

Such maneuvers have positioned private credit as a pivotal source of finance, characterized by its significant growth and strategic liquidity.

For instance, leveraging structured finance vehicles, senior debt funds might employ fund-level leverage to enhance returns.

Types of Private Credit Investments

Investors in the private credit market have several options to consider, each varying by risk-return profiles and investment strategies. Understanding these options helps align financial goals with risk tolerance and investment objectives.

Direct Lending

Direct lending involves providing loans directly to companies without intermediaries like banks. This approach typically targets mid-sized companies, offering investors a stable return profile.

Direct lending has historically constituted a significant portion of private credit capital raising.

As of April 2024, direct lending funds from 2018 and 2019 reported median net Internal Rates of Return (IRRs) of 7.6% and 8.6%, respectively.

This strategy secures consistent income streams while managing risks, owing to its senior position in the capital structure.

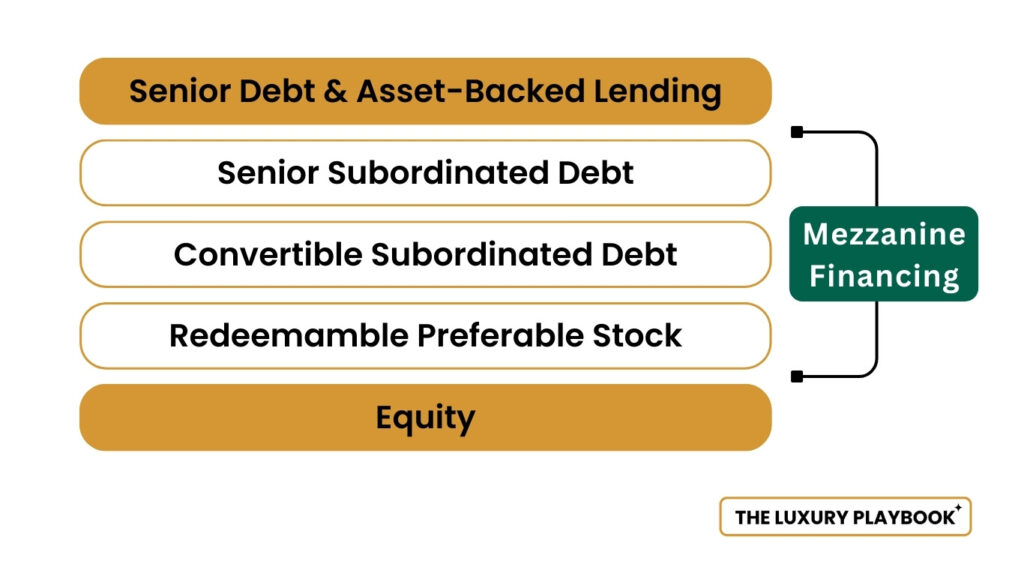

Mezzanine Financing

Mezzanine financing combines elements of debt and equity financing. It is subordinate to senior debt but ranks higher than equity. This option appeals to investors seeking higher returns at slightly increased risk.

Specialty finance funds, which include mezzanine financing, recorded median net IRRs of 9.6% and 11.2% for 2018 and 2019 vintages.

Mezzanine investments usually carry higher interest rates and equity-like features, making them suitable for lending to borrowers with slightly below investment-grade credit.

Distressed Debt Investing

Distressed debt investing targets the debt of financially troubled companies, offering the potential for substantial returns but at significant risk. This strategy requires deep market knowledge and a high tolerance for volatility.

The 2008 and 2009 distressed fund vintages achieved impressive net IRRs of 16.1% and 13.8%. Investors in distressed debt need to understand the market dynamics and restructuring strategies of distressed firms to profit from debt recovery or company turnarounds.

Middle-Market Lending

Middle-market lending focuses on firms that are too large for small-business loans but too small for traditional financing sources. This segment has been relatively neglected by traditional banks, presenting unique opportunities for private credit investors.

From 2018 to 2022, US sponsor-focused direct lending, a part of middle-market lending, comprised less than 20% of total fundraising.

This lending type blends features of various private credit forms, offering diverse risk-return profiles based on the borrower’s creditworthiness and loan structure.

| Investment Type | Typical Net IRR | Risk Profile | Target Borrower |

|---|---|---|---|

| Direct Lending | 7.6% – 8.6% | Moderate | Mid-sized Companies |

| Mezzanine Financing | 9.6% – 11.2% | Moderate to High | Below Investment Grade Borrowers |

| Distressed Debt Investing | 13.8% – 16.1% | High | Financially Distressed Companies |

| Middle-Market Lending | 7% – 15% | Varies | Mid-sized Companies |

Benefits of Private Credit for Private Credit Investors

The private credit market has grown significantly, expanding from approximately $1 trillion in 2020 to about $1.5 trillion at the beginning of 2024.

This growth highlights the numerous benefits private credit offers to investors.

Yield Enhancement

Private credit investments, particularly in direct lending, have consistently provided higher returns compared to leveraged loans and high-yield bonds.

For example, during periods of high and rising interest rates, direct lending yielded an average return of 11.6%, outperforming leveraged loans (5%) and high-yield bonds (6.8%).

This yield enhancement is a major draw for investors seeking to maximize their returns.

Investment Diversification

Private credit investments typically exhibit low correlation with broader market indices and experience lower volatility.

This diversification can protect against market fluctuations, making it an attractive option for investors aiming to reduce overall portfolio risk.

The low correlation with traditional assets helps smooth out portfolio returns, providing a stabilizing effect during periods of market turbulence.

Income Generation

The structure of private loans often includes periodic payments, offering regular income streams to investors.

This regular income can mitigate the J-curve effect observed in private market investments, where gradual inflows follow initial capital outflows.

Long-Term Capital Growth

The private credit market is poised for substantial growth, with assets under management projected to double from $1.2 trillion in 2021 to $2.3 trillion by 2027.

BlackRock projects that private credit AUM will exceed $3.5 trillion by 2028. This growth potential supports long-term capital appreciation for investors in the sector.

Inflation Hedge

Many private credit investments are provided on a floating interest rate basis, which can act as a hedge against inflation and rising interest rates.

This feature makes private credit an attractive option for preserving purchasing power and enhancing returns in an inflationary environment.

Comparative Performance Metrics

Here’s a comparative look at key performance metrics within private credit, using data from recent years:

| Investment Type | Average Return | Correlation with S&P 500 | Volatility |

|---|---|---|---|

| Direct Lending | 11.6% | 0.30 | Low |

| Leveraged Loans | 5% | 0.70 | Moderate |

| High-Yield Bonds | 6.8% | 0.75 | High |

| Private Equity | 15% | 0.60 | High |

Risk Management in Private Credit

Effective risk management strategies are vital for the success of private credit investments. The sector presents unique challenges that require a comprehensive approach to risk mitigation.

Practices such as enhanced due diligence and strategic investment agreements are crucial for safeguarding capital and achieving attractive returns.

Enhanced Due Diligence

Enhanced due diligence is the cornerstone of risk management in private credit. Borrowers undergo rigorous screening processes where credit managers evaluate financial health and potential risks, looking beyond conventional metrics.

Advanced tools and artificial intelligence (AI) play a significant role in refining these assessments.

For instance, the Federal Reserve Board’s 2023 Financial Stability Report highlighted that private pension funds hold a substantial portion of private credit, emphasizing the need for meticulous due diligence.

Structuring Expertise

Expert deal structuring is critical in managing risk within private credit. This involves crafting investment agreements that include protective covenants and collateralization to safeguard investor interests.

Protective covenants might involve stipulations on financial performance metrics, while collateralization ensures that investors have a priority claim on assets in the event of borrower defaults.

Over recent years, direct lending in private credit has outperformed many asset classes, with returns exceeding syndicated leveraged loans by 2-4%, showcasing the importance of structuring expertise.

Protective Covenants and Collateral

Protective covenants and collateral are central to securing private credit investments. Senior secured loans, backed by these protections, offer robust security against capital loss.

Since 2022, the average loan size in the private credit market has surged, exceeding $80 million.

Emphasizing strong protective covenants and collateral-backed investments helps managers minimize default risks and improve recovery chances during economic downturns.