Long-term stock investing serves as a formidable strategy for boosting financial growth. It involves holding onto assets like stocks and bonds for more than a year. The goal is to tap into compounding returns while minimizing trading costs. Historical data supports its effectiveness, with the S&P 500 noting annual gains in 37 of the last 50 years.

A geometric average return of 9.80% per year was recorded from 1928 to 2023. This outpaces Treasury bills and gold, showcasing long-term stocks’ superior performance. Moreover, investors benefit from lower tax rates on long-term capital gains, while capitalizing on the power of dividend reinvestment.

Better Long-Term Returns on Equity Investments

Investing in equities has historically provided stronger long-term returns compared to other asset classes. This analysis delves into the performance of stocks, the advantages of asset allocation, and historical data, highlighting the effectiveness of these strategies for wealth accumulation.

The Outperformance of Stocks

Over the long haul, stocks have significantly outperformed other asset classes. For instance, since 2000, the S&P 500 has soared by 287%, far surpassing the 215% gain in real estate during the same period.

This impressive growth stems from the continuous expansion of companies and their potential for earnings, offering investors substantial gains from equity investments over time.

Comparison with Other Asset Classes

Equities consistently deliver higher returns than bonds, savings accounts, and even gold. Historically, Treasury bills (T-bills) have averaged an annual return of 3.30%, and gold has returned 6.55%.

However, the S&P 500 has averaged an annual return of 9.80% from 1928 to 2023. This stark contrast underscores the superior ability of stocks to generate long-term wealth.

Here’s a detailed comparison of annual returns across various asset classes:”

| Asset Class | Annual Return (%) |

|---|---|

| Stocks (S&P 500) | 9.80 |

| T-bills | 3.30 |

| Gold | 6.55 |

| Real Estate (since 2000) | 5.58 |

Historical Returns Data

Historical data clearly demonstrate the advantages of equity investments. Over the past decade, the Russell 1000 index, which represents large-cap stocks, has returned 12.39%, while the Russell 2000 index, representing small-cap stocks, has provided a 7.08% return.

This data indicates that investing across various sectors and market capitalizations can reduce risk and enhance growth.

A portfolio with a 60% allocation to the Vanguard Total Stock Market Index and 40% to the Vanguard Total Bond Market Index returned 8.74% over 37 years (from 1987 to 2023). In contrast, a fully equity-driven portfolio yielded a remarkable 10.62% over the same period.

These figures highlight the importance of diversification in maximizing long-term returns while mitigating risks.

Buy-and-Hold Keeps You in the Game

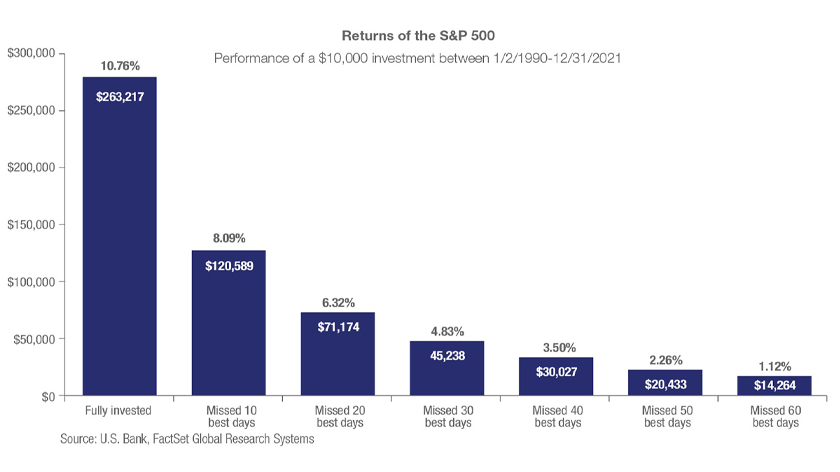

A buy-and-hold strategy proves beneficial by keeping investors engaged during the market’s most crucial days. This approach minimizes the risk of missing significant gains, which can drastically impact overall returns.

Attempting to time the market—deciding when to enter or exit—poses substantial challenges.

Historically, a substantial portion of the stock market’s gains occurs in just a few days each year. For instance, missing just the best five days of the S&P 500 over the past 20 years could halve your returns.

Data from J.P. Morgan Asset Management shows that missing the 10 best days from 2001 to 2020 reduced the annual return from 7.47% to 3.35%. This stark difference underscores the risk of market timing.

A buy-and-hold strategy encourages consistent, long-term investment, helping investors ride out short-term volatility.

This method leverages the market’s natural growth over time, ensuring participation in its best-performing days.

Historical evidence suggests that the market trends upward over long periods despite short-term fluctuations. For instance, the S&P 500 has an average annual return of about 10% over the past century.

During significant market downturns like the 2008 financial crisis, those who maintained their investments saw substantial recovery and gains in subsequent years.

Conversely, investors who exited the market during downturns often missed the rapid recoveries that followed. The power of compound interest significantly benefits long-term investors.

Reinvesting dividends and staying invested allows earnings to generate more earnings over time, leading to exponential growth.

Albert Einstein famously referred to compound interest as the “eighth wonder of the world” for its powerful effect on wealth accumulation.

Emotional Discipline

A buy-and-hold strategy also fosters emotional discipline. By sticking to a long-term plan, investors can avoid the pitfalls of emotional decision-making, such as panic selling during market drops or overenthusiastic buying during peaks.

Embracing a buy-and-hold strategy helps investors stay engaged during pivotal market moments, maximizing returns and leveraging the natural upward trend of the market.

This approach, coupled with the benefits of compound interest and emotional discipline, forms a robust foundation for successful long-term investing.

Faster Losses Recouperation

Faster Loss Recovery with a Buy-and-Hold Strategy

For most investors, adopting a buy-and-hold strategy can lead to a quicker recovery from losses, even after experiencing a bear market. Bear markets occur when major indexes like the S&P 500 drop by more than 20% from their recent highs.

These periods of decline can be daunting, but history shows that staying invested pays off in the long run.

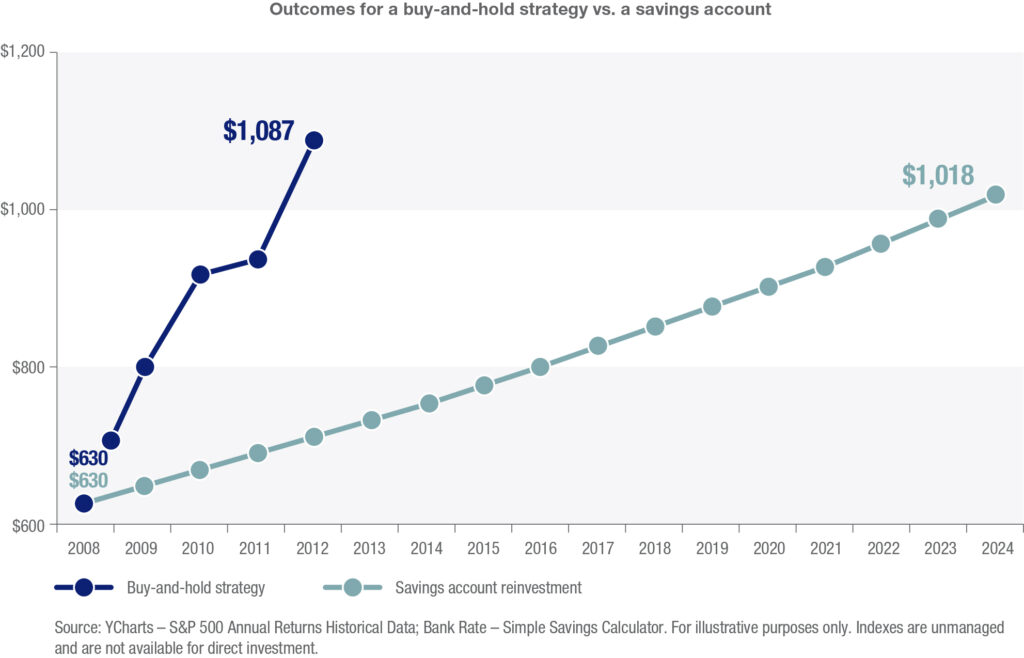

Consider this example: You invest $1,000 in the S&P 500 on January 1, 2008. That year, the S&P 500 experienced a severe downturn, losing 37% of its value.

By the end of 2008, your investment had dropped to $630. Let’s compare two scenarios: maintaining a buy-and-hold strategy versus reinvesting the remaining $630 into a savings account with a 3% annual interest rate, compounded monthly.

If you stuck with the buy-and-hold strategy, your investment would have recovered its losses by 2012. This recovery occurred even without adding any additional funds to the original stock market investment.

The S&P 500 has historically rebounded from downturns, and those who remain invested benefit from this recovery.

The market’s average annual return of approximately 10% over the past century supports the resilience and long-term growth potential of equities.

In contrast, if you moved your $630 to a savings account with a 3% annual interest rate, compounded monthly, the road to recovery would be significantly longer.

With the savings account, it would take approximately 16 years to surpass the $1,000 threshold.

This prolonged recovery period highlights the limitations of low-yield investments, especially when compared to the stock market‘s potential for higher returns.

Tax Benefits

Understanding the tax advantages associated with long-term investments is crucial for effective tax planning. Long-term assets benefit from significantly lower capital gains tax rates compared to short-term assets.

This difference can greatly influence investment decisions, highlighting the benefits of holding onto assets for longer periods to minimize tax burdens.

Taxation of Short-Term vs. Long-Term Gains

Short-term capital gains, or assets held for less than a year, are taxed at the same rates as ordinary income, which can be as high as 37%. Conversely, long-term capital gains, or assets held for more than a year, are taxed at much lower rates of 0%, 15%, or 20%, depending on the investor’s income level.

This differential encourages investors to adopt a long-term investment strategy to benefit from lower tax rates.

Here are the federal long-term capital gains tax brackets for single filers in 2023 and 2024:

| Year | 0% Rate | 15% Rate | 20% Rate |

|---|---|---|---|

| 2023 | Up to $44,625 | $44,626 – $492,300 | Over $492,300 |

| 2024 | Up to $47,025 | $47,026 – $518,900 | Over $518,900 |

These brackets underscore the significant tax savings possible by holding investments for longer periods.

Additional Tax Strategies

Investors can further optimize their tax situations through several additional strategies:

- Tax-Deferred Accounts: Utilizing tax-deferred accounts such as 401(k)s and IRAs can defer taxes on investment gains until withdrawals are made, usually during retirement when income may be lower, resulting in a lower tax rate.

- Capital Loss Harvesting: By selling losing investments, investors can offset capital gains from winning investments, reducing taxable income by up to $3,000 annually. Any excess losses can be carried forward to future tax years.

- Avoiding Wash Sales: To maintain the benefits of capital loss harvesting, investors must avoid wash sales, which occur if the same or substantially identical asset is repurchased within 30 days before or after the sale. This rule ensures that the tax benefits of realizing a loss are not negated.

Cost-Effectiveness of Long-Term Investment

One of the primary benefits of a long-term investment strategy is cost-effectiveness. Holding stocks for extended periods saves on various costs compared to frequent trading.

The longer you keep your investments, the fewer fees you incur, which enhances your overall returns.

Frequent trading incurs higher transaction fees. These fees vary based on your brokerage account type and the investment firm managing your portfolio. Traditionally, investors pay commissions when buying and selling stocks through a broker.

Additionally, markups may apply when trades are executed through the broker’s inventory. Each transaction diminishes your portfolio balance, as fees are deducted whenever you trade stocks. With the rise of online brokerages in 2024, many active investors benefit from fee-free transactions.

Platforms like Plus500, E*TRADE, and Charles Schwab have popularized commission-free trading, making it more accessible to buy and sell stocks without incurring traditional fees.

However, even in a fee-free environment, the cost-effectiveness of a long-term strategy remains significant.

Active trading often incurs hidden costs, such as the time and effort required to monitor and execute trades. Analyzing market trends, making frequent trades, and constantly managing a portfolio can be time-consuming.

Investors must consider whether the potential gains from active trading justify the time spent and whether those gains consistently outperform a long-term buy-and-hold strategy. Studies have shown that long-term investment strategies often outperform active trading over time.

According to a 2020 study by Dalbar, Inc., the average investor’s returns lag significantly behind market indices due to poor market timing and frequent trading.

Over a 20-year period, the average equity investor earned an annualized return of 5.04%, compared to the S&P 500’s 7.68%. This performance gap underscores the benefits of a disciplined, long-term approach to investing.