Israel’s housing market, long known for steady growth and relentless demand, has hit a dramatic turning point. Property prices across the country have fallen to levels not seen in more than a decade, creating real uncertainty for homeowners and a genuine opening for investors who know where to look.

According to data from Israel’s Central Bureau of Statistics, average residential prices have dropped by nearly 12% year over year, marking one of the sharpest corrections in recent memory. In some regions, declines have been even steeper, signaling that this is more than just a temporary slowdown.

What makes this moment worth paying attention to is the collision of long-term fundamentals with short-term weakness. On one hand, Israel faces strong demographic growth, limited land supply, and an economy that historically drives rising housing demand. On the other, global and domestic pressures ranging from higher interest rates to reduced foreign capital have created a rare situation where prices have slipped to record lows.

For buyers and investors, this environment presents an opening that does not come around often. As one of our senior real estate analysts put it, “We are witnessing a once-in-a-generation alignment of factors where prime assets can be acquired at a discount. The question is not whether prices will recover, but when.”

This rare buying window is already drawing attention from both domestic buyers and international investors seeking value in a market that has historically proven resilient. If you have been watching Israel from the sidelines, now is the time to pay closer attention.

Table of Contents

Current State of Israel’s Property Market in 2026

In Tel Aviv, where property values once seemed untouchable, average prices have fallen by almost 15% over the past year. Apartments that were selling for more than $1.15 million in 2022 can now be found closer to $950,000, opening up a city that had long felt out of reach for most local buyers. If you have had Tel Aviv on your radar, the math is suddenly looking a lot more interesting.

Jerusalem has experienced a milder correction of around 9%, but that is still a meaningful shift for a market known for its stability and strong international appeal.

In Haifa, prices are down nearly 10%, reflecting softer demand even in historically affordable northern markets.

The most dramatic declines are hitting secondary cities hardest. Speculative buying during the pandemic years pushed prices to unsustainable levels in these markets, and the correction has been sharp. In Beersheba, the average cost of an apartment has dropped by more than 17% year over year, while Ashdod and Netanya have seen similar double-digit falls. For investors, these numbers point to oversupply and weaker local demand accelerating the reset outside the central hubs.

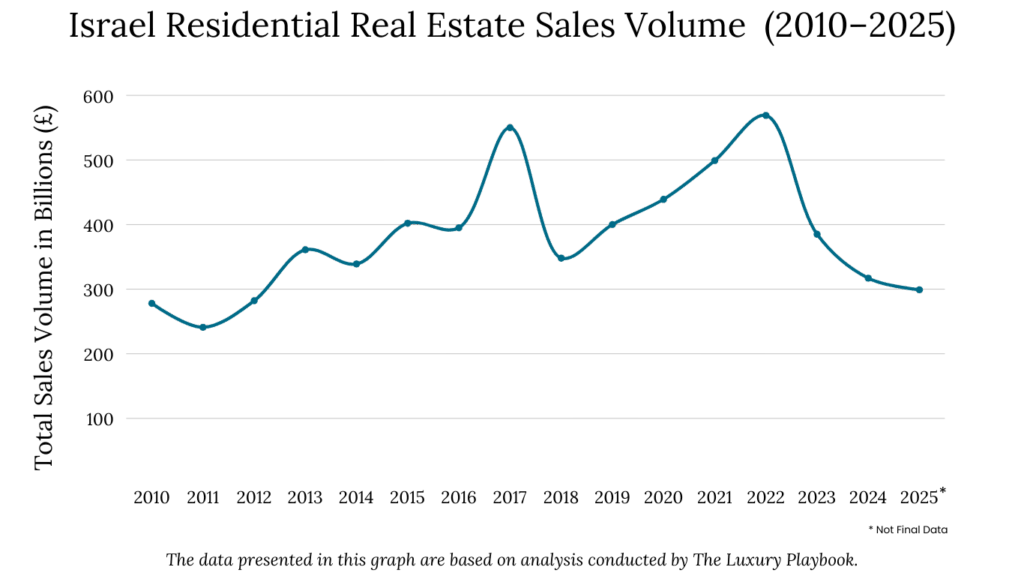

Compared to what came before, the contrast is striking. Between 2017 and 2022, Israeli property prices climbed by more than 60% nationwide, fueled by population growth, limited land supply, and strong foreign investment. The sharp reversal has caught many by surprise, but it also reminds you just how cyclical real estate can be, even in markets that seem bulletproof.

From an investment perspective, these record lows are not necessarily a sign of long-term weakness. They may well be a rare entry point into a market that has historically rebounded quickly once macroeconomic pressures ease.

Main Reasons Behind the Drop in Property Prices in Israel

Several forces have combined to push Israel’s property market into one of its sharpest downturns in recent memory. Some of these drivers are global in nature, while others are uniquely tied to Israel’s economic and political environment.

The first and most immediate factor is the impact of higher interest rates. Over the past two years, the Bank of Israel raised its key lending rate from near zero to 4.75%, making mortgages much more expensive. Monthly payments on a typical home loan have increased by as much as 30 to 40% compared to 2021, forcing many buyers to step back and wait. For younger families in particular, affordability has become the single biggest barrier to entering the market.

Political and economic uncertainty has also played a role. The ongoing war in Gaza has created short-term instability, dampening investor confidence both locally and abroad. Property markets tend to be resilient over the long term, but geopolitical risks can delay buying decisions and push prices lower in the near term.

Neutral observers note that this is not the first time conflict has influenced real estate cycles in Israel, but each period of instability tends to cool demand until conditions stabilize. If you want to understand how to protect your capital during periods of conflict, that context matters here.

Another important factor has been the decline in foreign investment. For years, buyers from the U.S., France, and the U.K. provided steady capital inflows into cities like Tel Aviv and Jerusalem. But global economic headwinds, stricter financial regulations, and a stronger shekel relative to some currencies have reduced this demand.

According to Ministry of Finance data, foreign property purchases in Israel dropped by nearly 25% in 2024 compared to the year before, weakening one of the market’s most important demand pillars.

Finally, the broader economic slowdown has weighed on household confidence. Inflation, higher living costs, and job market uncertainty have all made Israeli households more cautious about taking on large mortgages. Sellers who once enjoyed multiple offers above asking price are now facing buyers who negotiate aggressively, or simply wait on the sidelines.

Taken together, these factors have created the perfect storm. High borrowing costs, reduced foreign inflows, and uncertainty tied to both domestic and geopolitical developments have all converged at once.

Which Israeli Cities Are Seeing the Biggest Price Drops

Israel’s property downturn is playing out differently across its major urban centers, with each city telling its own story depending on local demand and investor behavior.

Tel Aviv has long been the heartbeat of Israel’s property market, attracting both domestic and international capital. The recent correction has shifted sentiment fast. Buyers who were once priced out are now revisiting opportunities, while developers are slowing new project launches.

The city’s luxury segment has softened the most, as high-net-worth buyers adopt a wait-and-see approach. That has left mid-market apartments as the most liquid part of the market right now.

Jerusalem is showing more resilience, but it is not immune. Demand from foreign buyers, particularly from North America and Europe, stays steady, though more cautious than in previous years. The city’s cultural and religious significance keeps housing demand underpinned, yet negotiations are now more common and sellers are having to show real flexibility on terms.

In Haifa, the story is about domestic affordability. The city has long appealed to middle-class families and professionals seeking value outside the Tel Aviv and Jerusalem corridor. Rising mortgage costs have slowed transactions, but Haifa’s relative affordability keeps it an attractive option for first-time buyers who are still serious about getting into the market.

Secondary cities such as Beersheba, Ashdod, and Netanya are facing the most visible corrections. These markets saw a surge in speculative buying during the pandemic, fueled by investors chasing quick gains. With sentiment cooling, they are now dealing with more price pressure, longer selling times, and higher inventory.

Still, they present intriguing opportunities for rental investors, given their large student populations, growing infrastructure projects, and appeal to younger households priced out of central Israel. If you are thinking about entering the property market for the first time, these secondary cities deserve a serious look.

Impact on the Rental Market and Yields

While property prices have been sliding, the rental market in Israel is telling a very different story. Demand for rentals has stayed strong, partly because many potential buyers are delaying purchases due to high mortgage rates and ongoing uncertainty. That shift has pushed more households into the rental market, keeping occupancy levels high in major cities.

For landlords and investors, this dynamic is creating an unusual balance. Purchase prices are falling, which lowers your cost of entry. At the same time, rents are holding steady or even ticking up slightly in key urban areas, especially in Tel Aviv and Jerusalem, where demand for central locations stays consistent. That combination is improving gross yields across several regions, making buy-to-let more attractive than it has been in years.

In secondary cities, the picture is slightly different. Places like Beersheba and Ashdod are seeing slower rental growth, but yields stay competitive because entry prices have come down so sharply. In Beersheba, for example, the large student population continues to provide steady demand for smaller units, helping landlords maintain occupancy even as sales values decline.

Another factor boosting the rental market is population growth. Israel’s relatively young demographics and strong urbanization trends mean that rental demand is unlikely to soften in any meaningful way, even during downturns.

With new construction projects being delayed due to financing challenges, the supply of rental housing could tighten further, creating upward pressure on rents over the medium term. That is good news if you are building a rental portfolio today.

Why This Is a Rare Buying Opportunity

Every property market goes through highs and lows, but few moments create the kind of opportunity now unfolding in Israel. After a long run of rising prices, the sudden downturn has opened the door for buyers who were previously locked out. For seasoned investors, these rare dips are often where future gains are born.

What makes this correction stand out is not just the size of the price drop, but the timing. It comes at a moment when global capital is searching for safe, income-producing assets, and Israel keeps attracting attention for its resilient economy, strong workforce, and high long-term housing demand. As Bloomberg’s real estate coverage has noted, markets with structural supply constraints tend to rebound faster than those where oversupply drives the correction.

Unlike some markets where falling prices are linked to overbuilding or weak demographics, Israel’s situation is different. Demand for homes is still there. Affordability pressures and financing costs have temporarily slowed transactions, but the underlying need for housing has not gone away.

Another reason this moment stands out is the structural constraint on housing supply. Much of Israel’s land is state-owned, and strict planning frameworks make it difficult to bring new housing online quickly. Even when developers secure approvals, projects often face delays from regulatory reviews, infrastructure constraints, or financing challenges. That bottleneck means that once demand revives, prices tend to rebound faster than in markets with abundant supply.

Investor psychology also plays a role. In times of uncertainty, fear often drives sellers to accept discounts that would have been unthinkable just a couple of years ago. Buyers who are willing to act during this phase of the cycle can secure high-quality assets at reduced prices, positioning themselves for strong gains when sentiment shifts.

The rental market is providing an additional safety net on top of that. With many households renting longer due to high mortgage costs, landlords are benefiting from steady demand and improving yields. You can generate reliable income today while waiting for long-term capital appreciation to follow.

Put simply, this downturn is less a warning sign than a reset. It is giving you a rare chance to acquire properties in a market that has historically bounced back stronger after periods of stress. For those who can take a long-term view, 2026 is shaping up to be one of the most attractive entry points in Israel’s property market in years.

Risks Buyers Should Keep in Mind

While Israel’s property market now offers rare opportunities, you need to go in with clear eyes. Entering at lower prices improves your long-term potential, but the short term may stay unpredictable for longer than you expect.

One of the biggest risks is the possibility of further short-term declines. Even though much of the correction has already taken place, markets often take time to find their floor. If interest rates stay elevated or economic uncertainty drags on, prices in certain areas could dip further before stabilizing. Rushing in and expecting an immediate rebound is a mistake that has burned investors before.

Policy and regulatory changes are another factor worth watching closely. Israel’s housing market has always been closely linked to government intervention, whether through tax adjustments, housing subsidies, or planning reforms. A new tax on property purchases, or stricter rules around foreign ownership, could reduce demand and weigh on prices even in desirable neighborhoods. You need to stay alert to any policy shifts that alter the risk-return balance. Looking at how expats navigate property purchases in nearby markets, such as buying real estate in Cyprus as a foreigner, gives you a useful framework for thinking through the regulatory side of cross-border investing.

Liquidity risk is also worth taking seriously, especially in secondary cities and smaller towns. Tel Aviv or Jerusalem apartments typically find buyers relatively quickly, but homes in Beersheba, Ashdod, or peripheral areas may take much longer to sell. That means you need to be prepared for longer holding periods if you want to realize your gains.

Geopolitical and security concerns add another layer of risk. The war in Gaza has highlighted how regional instability can affect sentiment, investor confidence, and cross-border capital flows. Israel’s property market has historically recovered from such events, but they can create real volatility in the short run. The Financial Times has covered how geopolitical risk repricing in emerging and frontier markets often creates both the dip and the eventual recovery.

Finally, financing conditions deserve careful attention. With mortgage costs elevated, even discounted property prices can feel expensive if you are relying on credit. For cash-rich buyers, this is actually a competitive edge right now. But if you depend on financing, you need to run the numbers carefully and avoid overextending yourself before the market turns.