The Athens real estate market in 2025 is entering a decisive period of maturation. What began as a post-crisis recovery has now transitioned into sustained growth, driven by rising international demand, record-high tourism figures, and a robust pipeline of urban redevelopment. Compared to other European capitals, Athens offers compelling value—combining capital upside with one of the highest rental yields in Southern Europe.

As Greece’s economic capital, Athens is attracting investors seeking long-term value, strong short-let returns, and a foothold in a fast-reforming EU real estate market.

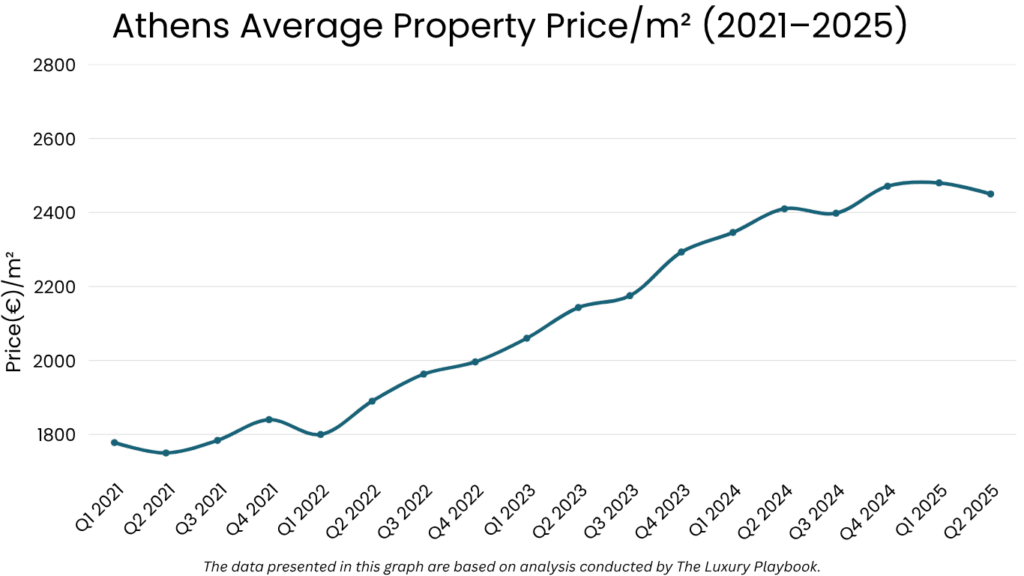

Throughout the first quarter of 2025, residential prices in Athens have increased by 7.6% year-over-year, outpacing inflation and exceeding price growth in many other Eurozone cities. This performance is being driven by continued investor interest in both short-term rental conversions and long-stay housing for students and professionals.

At the same time, developments like The Ellinikon Megaproject are reshaping the city’s urban coastline, raising demand and values along the Athens Riviera.

For investors, the market now offers two distinct tracks: revitalized central neighborhoods offering liquidity and rental yield, and emerging suburban zones with long-term appreciation potential. The balance between tourism-driven returns and domestic rental stability is giving Athens a unique edge in 2025.

Table of Contents

Overview of The Athens Real Estate Market

As of Q2 2025, the Athens real estate market continues its upward trend, supported by sustained foreign investment, strong domestic demand, and ongoing infrastructure improvements. Property prices in the capital have now surpassed pre-2008 levels in several districts, marking a full recovery and transition into a new growth phase.

The average residential sale price in Athens currently stands at €2,450 per square meter, representing a 7.6% year-over-year increase.

Central areas such as Exarchia, Koukaki, and Pangrati continue to lead in price growth, while the southern suburbs and seafront districts along the Athens Riviera are commanding a premium due to proximity to The Ellinikon and high tourism interest.

The median apartment price in central Athens is approximately €170,000 to €230,000, depending on condition, floor level, and proximity to metro stations. Renovated units in heritage buildings or Airbnb-ready layouts typically transact faster and closer to the asking price.

Transaction volumes remain strong. In Q2 2025, over 9,000 residential transactions were recorded across Athens, with nearly 40% of those involving foreign buyers. The average time-on-market for centrally located apartments is 58 days, down from 73 days a year earlier, reflecting increased buyer urgency and tighter inventory in sought-after neighborhoods.

Investment demand continues to be fueled by the Greek Golden Visa program, which now requires a minimum investment of €500,000 in central Athens. This has narrowed the buyer pool at the high end, but simultaneously increased competition for lower-priced, high-yield units below the threshold.

- Average residential prices at €2,450/sqm, up 7.6% YoY.

- Median apartment values range from €170K to €230K, with faster turnover on renovated units.

- 9,000+ transactions in Q2 2025, nearly 40% from foreign investors.

- Time-on-market averages 58 days, down 15 days from 2024.

- Increased investor focus on Airbnb-capable and sub-€500K properties.

In summary, the Athens housing market in 2025 remains highly liquid, price-positive, and increasingly segmented by investor type and location. With constrained supply, rising demand, and new infrastructure supporting growth, the market offers opportunities across a wide range of budget and strategy profiles.

Neighborhood Analysis

Athens is made up of highly diverse neighborhoods, each offering distinct pricing dynamics, rental demand profiles, and investment potential. From heritage-rich urban centers to upscale coastal districts and rapidly developing suburbs, investors can choose from a variety of entry points based on risk tolerance and yield objectives.

Koukaki

Koukaki has evolved into one of Athens’ most popular residential and investment areas. Known for its walkability, neoclassical buildings, and proximity to the Acropolis Museum, the district remains a magnet for both short-term rental operators and long-stay tenants.

The median home price in Koukaki is approximately €2,950 per square meter, reflecting a 9.1% year-over-year increase. Renovated one-bedroom apartments priced between €200,000 and €230,000 often sell within 30–45 days. The area benefits from high tourism foot traffic and reliable year-round demand for furnished rentals.

Koukaki continues to be one of the most liquid and high-yielding neighborhoods for short-term and long-term rental investors alike.

Pangrati

Pangrati offers a balance between affordability and lifestyle. Located just east of the city center, the neighborhood has seen a surge in demand among younger buyers and international investors looking for low-cost entry into a rising zone.

The median home price in Pangrati is €2,450 per square meter, with a 7.4% annual increase. Apartments under €180,000 are especially competitive, with fast absorption for units close to metro stations and green spaces.

Glyfada

Located on the Athens Riviera, Glyfada is one of the city’s most prestigious and sought-after coastal neighborhoods. It appeals to luxury buyers, diplomats, and Golden Visa investors seeking proximity to both the beach and high-end retail.

The median home price in Glyfada is €4,250 per square meter, up 6.2% year-over-year. High-spec villas and penthouses often exceed €600,000, while modern two-bedroom apartments in low-rise buildings trade between €320,000 and €420,000.

Neos Kosmos

Neos Kosmos is an emerging central neighborhood, benefiting from infrastructure upgrades, modern residential projects, and spillover demand from nearby Koukaki. The area remains affordable relative to its location and has strong rental momentum.

The median home price in Neos Kosmos is €2,150 per square meter, with a 6.8% increase year-over-year. Investors are targeting small apartments under €160,000 for refurbishment and short-let conversion.

Marousi

Marousi is one of the most active northern suburbs of Athens, offering strong fundamentals for family buyers and long-term tenants. The area is home to corporate offices, medical centers, and international schools, making it attractive for mid- to high-income residents.

The median price in Marousi is €2,800 per square meter, up 5.9% compared to Q2 2024. Modern apartments and maisonettes range from €250,000 to €400,000, depending on size and proximity to amenities.

Marousi combines stable rental demand with solid capital preservation, especially for investors with a medium- to long-term horizon.

Neighborhood Median Prices and Price per Square Meter

Athens Rental Market Overview

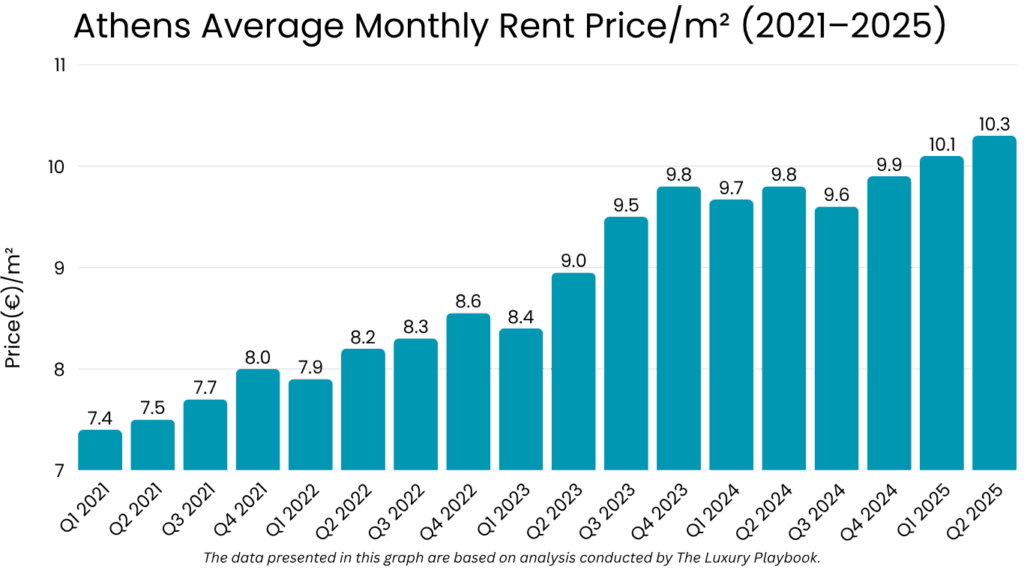

The Athens rental market in 2025 remains one of the strongest in Southern Europe, characterized by high occupancy, yield-focused demand, and limited new rental supply. As both local and international tenant bases expand, landlords continue to benefit from rising lease rates and longer-term rental commitments—particularly in centrally located and tourist-adjacent neighborhoods.

Average rents in Athens have increased by 5.2% year-over-year, with the strongest growth in one- and two-bedroom apartments suited for short- and mid-term leasing. The city’s combination of affordability, vibrant urban life, and tourism appeal continues to attract tenants from across the EU, the Balkans, and Asia.

Average Rent Prices by Unit Type

- Studio Apartments: €420/month (~€5,040/year)

- 1-Bedroom Apartments: €590/month (~€7,080/year)

- 2-Bedroom Apartments: €770/month (~€9,240/year)

- 3-Bedroom Apartments: €960/month (~€11,520/year)

- 4-Bedroom Apartments: €1,250/month (~€15,000/year)

Rent levels vary significantly by district, proximity to metro stations, and building condition. Renovated apartments in tourist zones or near universities tend to achieve higher rates with quicker tenant placement.

Rent by Neighborhood

- Koukaki: One-bedroom apartments average €700/month, driven by high short-let demand and year-round tourism appeal.

- Pangrati: Two-bedroom units lease for €780–€850/month, particularly in newer buildings near cafes and parks.

- Glyfada: Three-bedroom sea-view apartments rent for €1,400/month, while smaller units start at €850/month.

- Neos Kosmos: Studios lease at €450/month, with strong demand from students and young professionals.

- Kypseli: One-bedrooms range from €480 to €560/month, offering value for longer-term tenants and mid-income residents.

Vacancy and Leasing Trends

Athens maintains a low vacancy rate of 3.9%, with the tightest supply in city-center districts and areas popular with digital nomads and students. Landlords increasingly prefer 12-month renewable leases over short stays, particularly in zones affected by Golden Visa investment thresholds, which have tightened Airbnb conversions.

Tenant demand is most concentrated near universities, metro stations, and tourist corridors. Lease turnover remains high in studio and one-bedroom units, offering flexibility for landlords to reprice more frequently in rising markets.

Investor’s Outlook

Rental yields in Athens remain highly attractive, particularly for small apartments in central districts. Gross returns of 6% to 9% are typical for well-located, renovated properties, while suburban units in newer developments average 4.5% to 6% annually. Regulatory stability and low property tax rates further enhance net income performance.

In summary, Athens continues to deliver reliable rental returns, with tight supply and growing tenant diversity supporting income-driven investment strategies. For landlords focused on cash flow, the city’s rental market offers some of the most resilient yields in the EU.

Factors Influencing The Athens Housing Market

The Athens housing market in 2025 is shaped by a complex blend of macroeconomic trends, regulatory shifts, urban development, and investor sentiment. Together, these forces continue to drive pricing, influence investor strategy, and determine long-term growth across both the residential and rental sectors.

- Strong Foreign Investment: Athens remains a top destination for international buyers due to its affordability within the EU, lifestyle appeal, and favorable residency programs. Foreign investors accounted for nearly 40% of residential transactions in Q2 2025, with demand concentrated in central Athens and along the Riviera. The Greek Golden Visa continues to serve as a major catalyst, despite the recent €500,000 minimum investment rule in prime districts.

- Infrastructure & Urban Redevelopment: Major infrastructure projects—most notably The Ellinikon coastal redevelopment—are reshaping the city’s southern landscape. As this €8 billion project progresses, neighboring areas such as Glyfada, Elliniko, and Voula are seeing accelerated price growth, increased investor activity, and new high-spec residential supply.

- Tourism Recovery & Airbnb Demand: Tourism in Greece has surpassed pre-pandemic levels, with Athens benefiting as both a primary and transit destination. This trend has fueled demand for short-term rentals in areas like Koukaki, Plaka, and Monastiraki. Despite regulatory efforts to limit saturation, Airbnb continues to play a key role in the pricing dynamics of small city-center apartments.

- Rising Construction & Renovation Costs: Renovation-driven investment remains a cornerstone of Athens’ property market, especially in older urban stock. However, rising material and labor costs have compressed margins for flippers and increased acquisition thresholds. This trend is encouraging investors to focus on finished or lightly refurbished properties to reduce capex exposure.

- Rental Market Imbalance: A mismatch between supply and tenant demand persists across most central districts. Many units remain underutilized due to legal restrictions, inheritance issues, or reluctance to upgrade aging stock. This supply bottleneck has allowed rents to rise faster than inflation, keeping gross yields attractive even as purchase prices climb.

- Financing Conditions: Access to mortgage financing has improved slightly, with more Greek banks offering competitive rates for local buyers. However, the market remains largely cash-driven, especially for international investors. Low loan-to-value ratios and moderate credit demand have kept the housing market less exposed to financial volatility.

Athens Housing Market Forecast for 2026

The Athens housing market is expected to remain on a growth trajectory through 2026, although the pace of appreciation may moderate compared to the previous two years. Demand will continue to be supported by international investment, limited new supply in central zones, and sustained rental pressure—particularly in neighborhoods near universities, infrastructure nodes, and coastal redevelopment areas.

While rapid gains may slow, Athens is forecast to retain its position as one of the most attractive European markets for yield-focused and mid-term capital growth investors.

Property prices in Athens are projected to increase by 4% to 6% in 2026. With the current average at €2,450 per square meter, prices are expected to climb toward €2,580 to €2,630/sqm depending on neighborhood, condition, and investor activity. Central districts like Koukaki, Neos Kosmos, and Pangrati are likely to outperform due to demand spillover and scarcity of new stock.

Luxury zones such as Kolonaki, Glyfada, and Voula will remain stable, driven by lifestyle buyers and Golden Visa investors. However, affordability constraints and stricter short-term rental regulations may limit further aggressive price surges.

Inventory will continue to be tight in 2026, particularly in the resale apartment segment. While some new development projects will complete in the south and northeast suburbs, central Athens will remain undersupplied due to zoning, preservation restrictions, and limited land availability.

Properties in renovated buildings, close to transit and education hubs, are expected to see the strongest price resilience and liquidity.

Rental prices are forecast to rise by 3% to 5%, supported by continued pressure from tourism, student housing shortages, and low availability of modern long-term lease units. One-bedroom apartments could reach €630–€650/month, while short-let rates will remain robust in zones with strong tourism infrastructure and limited regulation.

Vacancy rates are expected to remain below 4% in most city-center districts. The balance between domestic long-term leases and short-term rentals will become increasingly neighborhood-specific, with certain districts leaning more heavily into one segment over the other.

From a macroeconomic standpoint, Greece’s improved credit rating, low property tax burden, and stable eurozone membership will continue to attract foreign buyers looking for relatively secure, income-producing assets.

Demographic trends—especially digital nomads, retirees from Western Europe, and regional student migration—will further support occupancy and pricing momentum.

Is It Worth Buying a Property in Athens?

Buying property in Athens in 2025–2026 can offer tangible benefits, particularly for investors targeting income-generating assets or medium-term capital appreciation. However, as the market becomes more competitive and segmented, it is important to weigh the city’s strengths against its structural limitations.

Residential prices are forecast to rise by 4% to 6% in 2026, supported by limited supply, international buyer interest, and neighborhood-level regeneration. Central districts such as Koukaki, Pangrati, and Neos Kosmos continue to offer good liquidity and rental demand, while coastal zones like Glyfada and Voula maintain long-term lifestyle value.

Rental yields remain competitive across the market. One-bedroom apartments in well-located areas typically deliver gross returns between 6% and 9%, depending on lease structure and property condition. Demand from tourists, students, and young professionals supports year-round occupancy in central Athens.

That said, there are constraints to consider. Regulatory shifts—especially related to short-term rentals—could impact ROI in tourist-heavy areas. Additionally, renovation costs have increased significantly, which may narrow profit margins for value-add strategies. Liquidity in luxury and suburban zones can be uneven, and legal due diligence in older buildings remains essential.

Investors should also be aware that returns are highly localized. Neighborhood selection, building quality, and tenant targeting play a crucial role in overall performance. While Athens has emerged as a reliable property market within the EU, it does not offer the scale, institutional transparency, or financing depth of larger Western capitals.

In conclusion, Athens presents a viable opportunity for investors with a clear strategy, realistic time horizon, and a focus on income and urban value creation. It is not a speculative market—but it remains one of Europe’s most affordable and resilient urban centers for property acquisition.

Other Market Forecasts & Overviews

Thessaloniki Real Estate Market Overview & Forecast

Mykonos Real Estate Market Overview & Forecast

Santorini Real Estate Market Overview & Forecast

FAQ

Are Athens property prices expected to rise in 2026?

Yes. Prices are forecast to increase by 4% to 6% across most residential zones.

Is Athens a good place to invest in real estate?

Yes, especially for investors targeting strong rental yields, urban regeneration, and long-term value.

What are the best neighborhoods to invest in Athens?

Top areas include Koukaki, Pangrati, Glyfada, Neos Kosmos, and Marousi—each offering distinct rental or capital appreciation potential.

Are rental yields in Athens attractive?

Yes. Gross rental yields range between 6% and 9%, particularly in central districts and renovated apartments.

Does Greece charge property or capital gains tax on real estate?

Yes, but taxes are relatively low. Greece offers competitive annual property taxes and tax exemptions under specific conditions for foreign buyers.