South African wine is having its moment in the spotlight, with critics from Wine Spectator to Jancis Robinson praising the country’s “New Wave” producers for creating wines that rival anything from Burgundy or Barolo. The narrative is compelling: exceptional terroir, innovative winemakers, and prices that seem almost too good to be true for wines of this quality.

Yet for wine investors looking beyond the critical acclaim, South African wine faces fundamental structural challenges that make it a risky bet for serious capital allocation.

The central question isn’t whether South Africa makes great wine, it clearly does, but whether the market infrastructure, global recognition, and investment ecosystem exist to support meaningful returns for collectors putting their money where the critics’ praise is.

Table of Contents

Key Takeaways

Navigate between overview and detailed analysisKey Takeaways

- South Africa’s “New Wave” wines are critically acclaimed, with 95+ scores rising 43% YoY in 2025 and global sommelier recognition increasing.

- Despite excellence, weak distribution, low brand recognition, and limited auction presence keep these wines from being investment-ready.

- Wines retail 40–60% below Burgundy/Barolo, reflecting structural limitations rather than inefficiency.

- Liquidity is limited: small production volumes and negligible secondary market activity restrict investor exits.

- Macro risks like currency volatility, politics, and infrastructure challenges add barriers for institutional capital.

- To become investable, South Africa needs stronger distribution, deeper secondary markets, and institutional adoption.

The Five Ws Analysis

- Who:

- UHNW collectors, wine investors, and global funds evaluating emerging wine regions.

- What:

- South Africa’s acclaimed wines offer exceptional quality but lack the infrastructure for reliable investment performance.

- When:

- Momentum peaked in 2025, with acclaim rising faster than investment readiness.

- Where:

- Key regions include Swartland (Chenin, natural reds), Hemel-en-Aarde (Pinot Noir, Chardonnay), and Stellenbosch (Cabernet blends).

- Why:

- Because while quality rivals Burgundy, limited liquidity, recognition, and macro instability prevent South African wines from being true investment-grade assets.

The Hype Around South Africa’s New Wave Wines

The critical momentum behind South African wine has reached fever pitch in 2025, with international wine publications falling over themselves to discover the next great South African producer.

Tim Atkin’s annual South Africa Report, published in September 2025, awarded 95+ point scores to 127 South African wines, up from 89 wines in 2024, representing a 43% increase in top-tier recognition.

Similarly, Wine Spectator’s 2025 annual rankings included 23 South African wines scoring 92+ points, compared to just 11 in 2020, according to their digital archive.

Regional recognition has become particularly pronounced, with Swartland leading the charge for innovative winemaking that emphasizes minimal intervention and old-vine fruit. According to Decanter’s September 2025 regional survey, Swartland now boasts 15 producers regularly achieving international scores above 93 points, including breakthrough stars like Sadie Family and Mullineux whose wines command £60-120 retail prices in London wine shops.

Stellenbosch continues evolving beyond its Cabernet Sauvignon reputation, with producers like Klein Constantia and Kanonkop earning recognition for elegant Bordeaux-style blends that compete quality-wise with classified growth châteaux.

The sommelier community has embraced South African wines with particular enthusiasm, creating buzz in restaurants from New York to Tokyo. According to Wine & Spirits Magazine’s 2025 sommelier survey, 67% of sommeliers in top-tier restaurants now include South African wines on their lists, up from 34% in 2020.

This restaurant presence has created important word-of-mouth marketing that money can’t buy, with influential wine professionals championing South African producers to affluent clientele who might eventually become collectors.

Barriers Holding Back South African Wine Investments

Despite the critical acclaim, South African wine faces substantial structural barriers that make it challenging for investors to achieve meaningful returns. Global distribution remains severely limited, with most top South African producers exporting less than 30% of their production according to Wines of South Africa’s 2025 export data.

This creates immediate liquidity problems for investors, as wines that can’t be easily bought and sold in major markets struggle to develop the secondary market activity that drives investment returns.

Brand recognition gaps compared to established regions present another fundamental challenge. According to Wine Intelligence’s Global Wine Brand Power Index 2025, no South African wine brand ranks in the global top 50 for consumer awareness, while regions like Bordeaux and Champagne dominate recognition metrics.

This awareness deficit translates directly into pricing power limitations, as even exceptional South African wines struggle to command the premiums that drive investment appreciation in more established regions.

Currency volatility adds another layer of risk that investors must carefully consider. The South African rand has depreciated 23% against the dollar over the past five years according to Reserve Bank of South Africa data through September 2025, creating headwinds for international investors even when wine prices appreciate in local currency terms.

Political and economic uncertainties, including ongoing concerns about land reform and infrastructure reliability, create additional risk premiums that sophisticated wine investors factor into their allocation decisions.

Production scale limitations further constrain investment potential, with most acclaimed South African producers making fewer than 10,000 cases annually according to industry data compiled by Wine Magazine in August 2025. This small-scale production creates scarcity that critics love but investors find problematic, as limited availability makes it difficult to build meaningful positions or achieve portfolio-moving returns even when wines perform well.

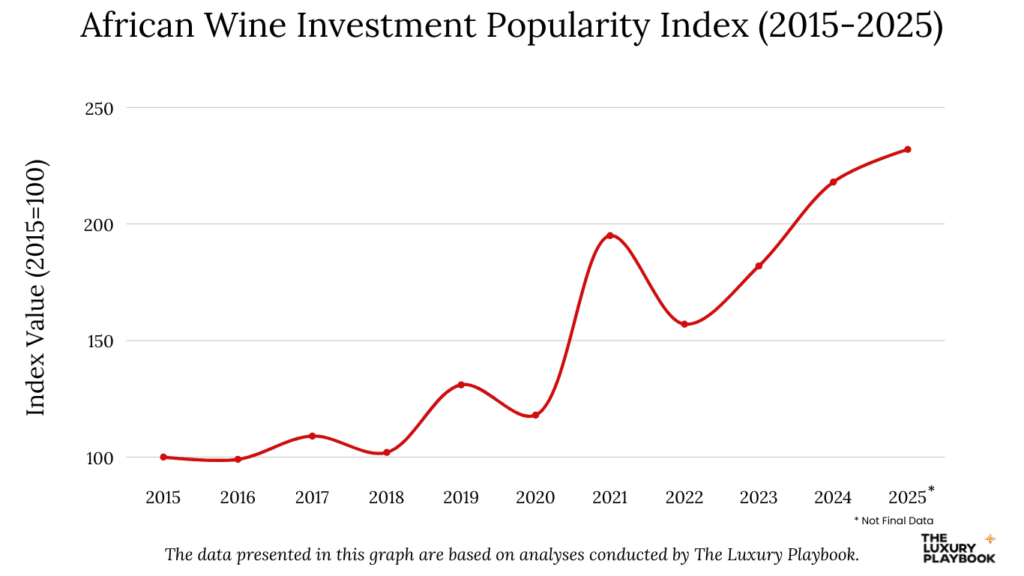

Price vs Value Challenges for Investors

The pricing dynamics of South African wine present a paradox that initially attracts investors but ultimately limits return potential. According to Liv-ex data from September 2025, top South African wines trade at 40-60% discounts to qualitatively comparable wines from Burgundy or Barolo, creating an apparent value proposition that seems almost too good to ignore. However, this pricing reflects market realities rather than temporary inefficiencies, as South African wines lack the historical track record and collector base necessary to support higher valuations.

Auction market performance reveals the challenges facing South African wine investors seeking exit liquidity. According to Wine Market Journal’s 2025 auction analysis, South African wines represented just 0.3% of total auction lots sold globally, with average lot values of £247 compared to £1,247 for Burgundy and £823 for Bordeaux. Even more concerning, many lots failed to meet reserve prices, indicating limited collector demand despite critical acclaim.

The domestic market provides some support but insufficient scale for meaningful investment returns. According to South African Wine Industry Statistics 2025, domestic consumption accounts for 67% of total production, but local collectors typically focus on established European regions rather than domestic wines.

This creates a ceiling on domestic demand that limits price appreciation potential regardless of quality improvements or critical recognition.

The Risk of Overhyping South Africa’s Potential

The current enthusiasm for South African wine bears troubling similarities to previous investment bubbles in emerging wine regions that ultimately disappointed investors. The Australian wine boom of the 1990s provides cautionary parallels, as critical acclaim and “discovery” narratives drove investment interest that wasn’t supported by sustainable market fundamentals.

According to Wine Business Monthly’s retrospective analysis published in July 2025, Australian wine investments from that era delivered average annual returns of -2.3% over the subsequent decade as hype gave way to market reality.

Media narratives around South African wine often emphasize quality improvements and critic scores while glossing over structural market challenges that determine investment viability. Wine publications benefit from discovery stories that generate reader interest, but their enthusiasm doesn’t necessarily translate into the sustained collector demand required for investment appreciation.

According to a September 2025 analysis by Wine Investment Analytics, regions that achieve critical acclaim without corresponding improvements in distribution, brand recognition, and collector base typically see initial price spikes followed by stagnation or decline.

The “next big thing” mentality can lead investors to overlook fundamental factors that drive long-term wine investment success. Historical analysis of wine investment returns shows that sustained appreciation requires not just quality wine but also strong secondary markets, institutional recognition, and demographic tailwinds from growing collector populations.

South African wine may eventually develop these supporting factors, but current evidence suggests the market infrastructure remains years away from maturity.

What Needs to Change Before Investors Commit

For South African wine to become a viable investment category, several fundamental changes must occur beyond continued quality improvements and critical acclaim. Distribution network expansion represents the most immediate need, with successful wine investments requiring availability in major global markets including New York, London, Hong Kong, and increasingly, mainland China.

Secondary market development requires sustained collector interest that goes beyond restaurant sommeliers and wine enthusiasts to include serious investors willing to pay premium prices for proven performers.

Auction house data from September 2025 shows that viable wine investment categories require minimum annual auction volumes of £50 million to provide adequate liquidity, a threshold South African wine currently misses by more than 90%.

Brand recognition improvements need systematic marketing investment and time to develop consumer awareness that supports premium pricing. According to brand consulting firm Wine Vision’s 2025 analysis, wine regions typically require 15-20 years of consistent quality and marketing to achieve the recognition levels that support investment-grade pricing power.

While South African wine quality has improved dramatically, the brand building process remains in early stages.

Institutional recognition from wine funds, wealth managers, and serious collectors represents perhaps the most critical missing element. Until established wine investment advisors begin recommending South African allocations to their clients, the region will struggle to attract the patient capital required for sustained price appreciation.

Current evidence suggests this institutional adoption remains years away, despite improving wine quality and growing critical acclaim.