The global wine trade has always been sensitive to shifts in politics and trade policy, and the recent tariffs introduced under the Trump administration are a prime example. By imposing duties on European imports, particularly French, Italian, and Spanish wines, the U.S. has effectively reshaped the competitive balance in the premium wine segment.

Bottles that once dominated restaurant lists and retail shelves are now arriving at higher prices, forcing both consumers and businesses to reconsider their choices.

For U.S. wine producers, however, this disruption presents a unique opportunity. With European labels facing inflated costs at the point of sale, premium American wines are suddenly in a stronger position to capture market share.

As one of our Wine Analysts recently remarked, “Tariffs may have closed one door, but they’ve opened another for U.S. producers who can now compete more directly with Bordeaux and Burgundy at price points that once seemed out of reach.”

From an investment standpoint, this creates an environment where U.S. wines, particularly those from established regions like Napa, Sonoma, and Oregon, are no longer just domestic favorites—they are being elevated on the global stage.

Investors who once overlooked American wines in favor of European prestige labels are beginning to view them as assets capable of appreciation, especially as scarcity and shifting demand patterns drive long-term value.

Table of Contents

How Tariffs Are Affecting European Wine Imports in the U.S.

The most immediate impact of tariffs has been felt in pricing. European wines that once entered the U.S. market with relatively low import duties are now arriving at inflated costs, in some cases rising by 15–25% at retail level depending on the country of origin and wine category.

Importers and distributors, who often operate on slim margins, have little choice but to pass these increases directly to restaurants and consumers.

French Bordeaux and Burgundy, Italian Barolo and Chianti, and Spanish Rioja—all staples in the premium wine segment—are among the categories most affected. According to U.S. customs data, French wine imports declined by nearly 12% in volume year-over-year following tariff implementation, while Italian imports fell by around 8%.

This is particularly notable in the $20–$50 per bottle range, where consumers are highly price-sensitive.

Restaurants and retailers are adjusting quickly. Wine lists that once leaned heavily on Old World selections are increasingly turning to domestic alternatives, not only because of price but also availability. As a result, sommeliers and buyers are giving more shelf and menu space to Napa Cabernet Sauvignon, Oregon Pinot Noir, and Washington State Merlot.

For investors, these shifts are more than short-term inconveniences—they represent a structural realignment in U.S. consumer behavior. If European wines remain expensive, even temporarily, American wines could secure lasting loyalty from both casual drinkers and fine wine collectors.

This potential change in demand patterns could translate into stronger price appreciation for premium U.S. labels in the years ahead.

The Growing Appeal of U.S. Premium Wines

With European wines facing higher prices, U.S. producers are stepping into the spotlight. Regions like Napa Valley, Sonoma County, and Oregon’s Willamette Valley have long been respected for quality, but tariffs on imports have accelerated their rise in the domestic market.

For many consumers, the choice is no longer between Old World and New World—it’s about finding the best value without compromising quality, and U.S. wines are increasingly winning that comparison.

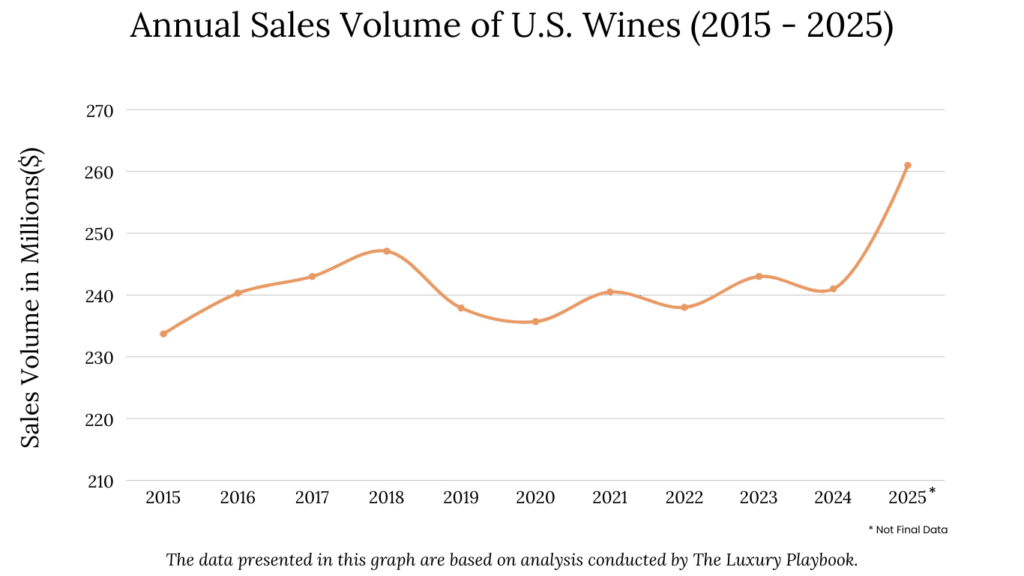

Sales data supports this shift. According to NielsenIQ, sales of U.S. premium wines priced above $20 per bottle grew nearly 9% year-over-year, outpacing the overall wine market. Napa Valley Cabernet Sauvignon, in particular, has seen strong momentum, with auction prices for iconic labels like Screaming Eagle and Opus One rising between 6–10% annually since 2020. Meanwhile, Oregon Pinot Noir has captured younger drinkers, who are often looking for elegance at a more approachable price point compared to Burgundy.

Culturally, American consumers are also showing pride in supporting local vineyards. Rising awareness of sustainability and climate-resilient practices has further boosted U.S. wineries that emphasize organic and biodynamic farming. These values resonate strongly with millennial and Gen Z buyers, two groups that now account for nearly 30% of fine wine purchases in the U.S.

As Master Sommelier Evan Goldstein noted in a recent industry panel, “Tariffs may have given U.S. wineries a short-term edge, but what’s truly cementing their role is consistent quality and consumer loyalty. Once a buyer discovers a domestic alternative they love, they’re less likely to switch back—even if tariffs disappear.”

This combination of pricing, quality, and cultural alignment is transforming U.S. premium wines from niche alternatives into true staples of the luxury wine market. For investors, this suggests stronger long-term demand—and potentially higher returns—for carefully selected American labels.

Market Pricing Trends Between European and U.S. Wines

The price gap between European imports and U.S. wines has widened noticeably since tariffs came into play. Before tariffs, a mid-tier Bordeaux or Burgundy bottle could often compete directly with a Napa Cabernet or an Oregon Pinot Noir on price. Now, with European wines facing tariffs of up to 25%, that balance has shifted, giving U.S. producers a clear pricing advantage.

For example, data from Wine-Searcher shows that the average retail price of a 2018 Bordeaux classified growth has risen from around $60 to $75 per bottle since tariffs were applied. In contrast, a comparable Napa Cabernet from the same release year has held steady at $55–65.

Burgundy has been hit even harder, with many well-known village-level wines moving into the $80–100 range, pushing consumers toward Oregon Pinot Noir, which continues to sit closer to $45–65 on average.

At the higher end of the market, the impact is even more pronounced. Collectible Burgundy labels like Domaine de la Romanée-Conti and top Bordeaux châteaux such as Lafite Rothschild were already expensive, but tariffs have driven them further out of reach for many U.S. buyers.

By contrast, premium American wines such as Opus One or Screaming Eagle—while still costly—are now viewed as more reasonable alternatives when adjusted for price appreciation.

Here’s a snapshot comparing pricing trends since tariffs were introduced:

| Wine Category | Pre-Tariff Avg. Price (2019) | Current Avg. Price (2025) | % Change | U.S. Comparable Price (2025) |

|---|---|---|---|---|

| Bordeaux Classified Growth (2018) | $60 | $75 | +25% | Napa Cabernet: $60 |

| Burgundy Village-Level | $65 | $90 | +38% | Oregon Pinot Noir: $50 |

| Super-Tuscan (Italy) | $80 | $95 | +19% | Washington Cabernet: $55 |

| Top Bordeaux (e.g., Lafite) | $650 | $800 | +23% | Opus One: $425 |

These shifts are not just short-term price spikes—they’re reshaping consumer buying habits. Wealthy buyers who might have defaulted to Bordeaux for their cellars are experimenting with Napa alternatives, while younger drinkers who would have tried Burgundy are turning to Oregon or Washington wines instead.

For investors, this creates two key dynamics: European wines are becoming more scarce and expensive, which could support long-term value for top-tier bottles, but U.S. wines are gaining broader acceptance and enjoying faster turnover in the short to medium term.

Key American Wine Regions Benefiting From Tariff Pressures

The tariff environment has given American wineries a unique moment in the spotlight. With European imports climbing in price, U.S. producers are filling the gap, and certain regions are experiencing a surge in both demand and recognition. This is not just a matter of consumers swapping French for American—it’s a structural shift that could leave lasting effects on the premium wine market.

California remains the anchor of U.S. wine prestige. Napa Valley, in particular, has been one of the biggest winners. With Bordeaux pricing up sharply, high-end Napa Cabernets are increasingly viewed as a more affordable yet equally prestigious substitute.

According to Liv-ex data, Napa Valley’s top labels saw a 12% rise in U.S. trading volume in 2024, with brands like Screaming Eagle and Harlan Estate drawing attention from both collectors and investors. Sonoma is also benefiting, especially in Pinot Noir and Chardonnay, as Burgundy imports move further out of reach.

Oregon has emerged as a serious alternative to Burgundy. The Willamette Valley, already known for world-class Pinot Noir, is gaining traction among younger collectors and sommeliers. Since tariffs were imposed, Oregon Pinot exports to major U.S. cities have grown by 18% year over year, and many restaurants that previously leaned heavily on Burgundy have started to spotlight Oregon producers like Domaine Serene and Beaux Frères.

Washington State is also climbing the investment ladder. Known for Cabernet Sauvignon, Merlot, and Syrah, Washington has long been considered undervalued compared to Napa. But now, with Super Tuscans and Bordeaux blends carrying a heavier price tag, Washington wines are being recognized as strong value buys. Auction records from 2024 show a 15% increase in demand for collectible Washington labels, signaling rising investor interest.

Even Texas and Virginia are beginning to benefit in niche circles. While they don’t compete directly with European icons, these emerging regions are seeing greater curiosity from adventurous buyers who want to explore American terroir while staying within competitive price points.

What makes this particularly significant is that tariffs haven’t just shifted consumer buying temporarily; they’ve expanded the market share of U.S. producers who now have the opportunity to cement themselves as long-term alternatives to Europe’s traditional strongholds.

Challenges for U.S. Producers Despite Tariff Advantages

While tariffs have boosted the visibility of U.S. wines, the benefits don’t come without significant challenges. Producers may be winning short-term market share, but they are also navigating rising costs, environmental pressures, and structural issues that could limit their long-term gains.

One of the biggest hurdles is production costs. Land and labor in California, particularly Napa Valley, are among the most expensive in the world. A 2024 survey by Silicon Valley Bank’s Wine Division found that the average cost of producing a bottle of premium Napa wine exceeds $50 before it even reaches distributors.

By contrast, many Bordeaux estates can produce wine at a fraction of that cost, thanks to larger estates, economies of scale, and cheaper labor markets. Even with tariffs, U.S. producers don’t always have a clear pricing edge.

Climate change is another looming concern. U.S. vineyards, especially in California and Oregon, are experiencing more frequent wildfires, droughts, and erratic weather patterns. The 2020 and 2023 wildfires in California led to “smoke taint” issues that rendered some vintages unsellable, costing Napa producers over $600 million in lost revenue according to the Wine Institute. Rising insurance costs for vineyards and wineries are also eating into margins.

Distribution is also a sticking point. While European producers have established global networks, many American wineries still struggle with limited international distribution. This makes it harder for them to capitalize on growing foreign demand, especially in Asia where French and Italian wines dominate. Without aggressive expansion into export markets, U.S. producers risk staying overly dependent on domestic buyers.

Finally, there is the issue of consumer perception. While American wines are increasingly respected, many investors and collectors still see Bordeaux and Burgundy as “safe bets” for long-term appreciation.

The Liv-ex Power 100 ranking continues to be dominated by European labels, with only a handful of U.S. producers making the list. This suggests that while demand is rising, American wines have not yet achieved the same level of global investment credibility.

Long-Term Outlook for the Premium U.S. Wine Market

Tariffs may have been the spark, but the future of U.S. premium wine will be decided by a combination of trade policy, rising production costs, and the growing influence of climate change. These forces together will shape whether the current surge in demand for American wines becomes a lasting transformation or simply a temporary reaction to market pressures.

In the most likely scenario, tariffs remain in place for the medium term, keeping European wines relatively expensive. That would give U.S. producers continued momentum, particularly in the $40–$100 range where many Napa, Sonoma, Oregon, and Washington wines compete.

Well-established estates with strong critic scores and direct-to-consumer models are likely to see steady appreciation, while smaller producers benefit from a spillover effect as buyers expand their horizons within the domestic market.

There is also a bullish case. If tariffs persist longer than expected, or if Europe faces tighter supply due to smaller harvests and higher energy costs, American wines could gain an even bigger foothold. In this scenario, top Napa Cabernets and Oregon Pinots could see price gains in the mid-to-high single digits annually, with older vintages in pristine condition becoming even more desirable at auction.

The downside risks are equally clear. A rapid rollback of tariffs, combined with a slowdown in luxury spending or a difficult wildfire season, could dampen demand and compress margins. In such a case, only the strongest brands would hold their value, while many mid-tier wineries might be forced to discount in order to compete again with Europe.

For investors and collectors, the path forward is to focus on resilient producers—those with diversified vineyards, consistent quality, and strong distribution networks. Estates that have built loyalty through wine clubs, direct sales, and careful allocation strategies will be best positioned to hold pricing power.

For those building a portfolio, mixing Napa “anchor” labels with Oregon Pinot Noir and Washington State wines provides diversification across both region and style.

If tariffs stay in place through 2026, this shift may become more than a short-term market distortion. It could mark the beginning of a longer-term reweighting toward U.S. premium wines, with domestic producers turning temporary trade advantages into permanent brand loyalty among both collectors and everyday consumers.