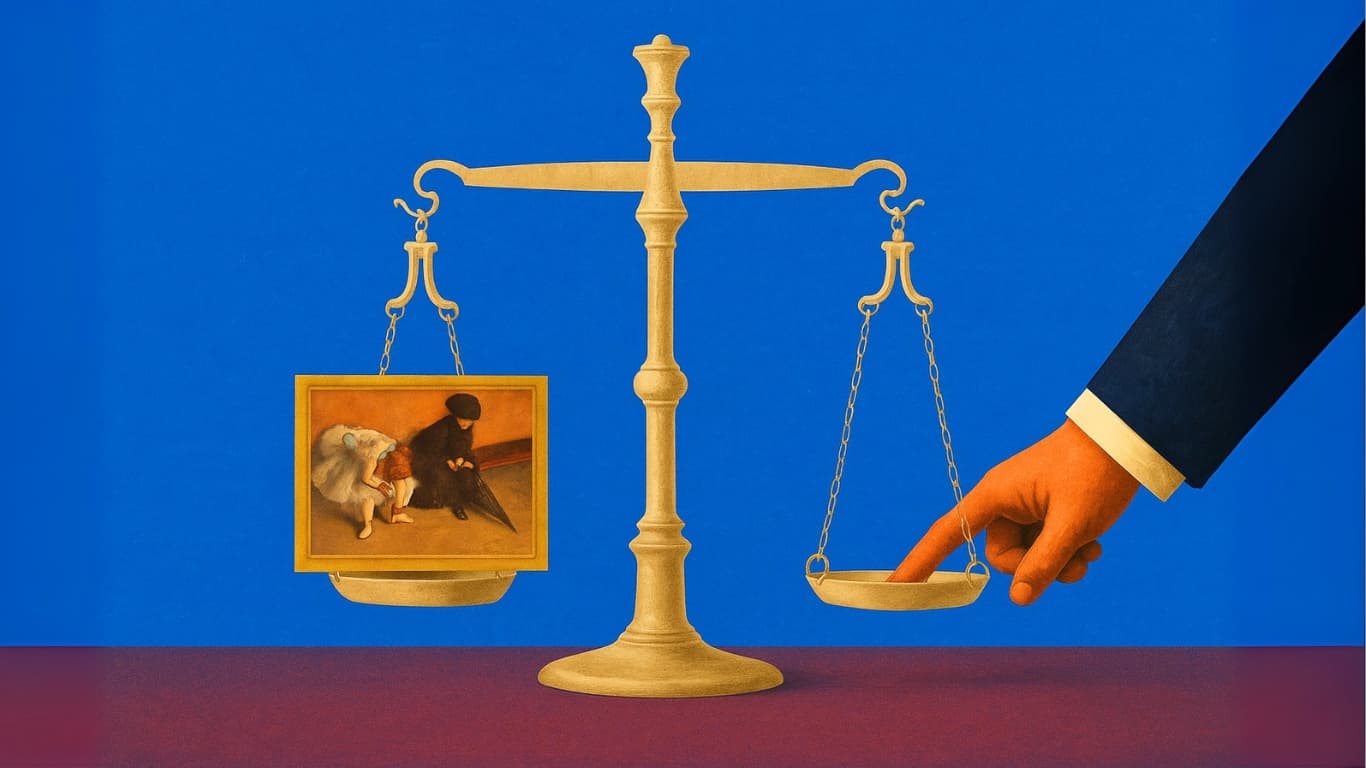

The US tariff escalations of the past two years have rerouted significant transaction flow in the art market, and collectors are absorbing the cost. The pattern shows up in customs documentation, in auction-house shipping advisories, and in the geographic redistribution of mid-tier sales across Christie's, Sotheby's, and Phillips' international calendars.

The market response has been adaptive rather than panicked. The trade has worked around tariff exposure for decades, and the current cycle is producing a recognisable rotation toward European and Asian transaction venues for material that would once have moved through New York. Our coverage of Art Basel Paris traces part of that geographic shift.

- United States tariff escalations of the past two years have rerouted significant transaction flow in the art market, with collectors absorbing the cost across multiple channels.

- The traditional customs exemption for original works of art has narrowed in scope, with additional documentation, longer hold periods and case-by-case adjudication adding meaningful friction.

- Collectors planning major acquisitions are increasingly closing transactions through European and Asian sale rooms when the work’s geography permits a venue shift to be made.

- Free-port storage in Geneva, Luxembourg and Singapore continues to hold a meaningful share of high-value contemporary and post-war material under the current tariff regime.

- Christie’s, Sotheby’s and Phillips have all expanded international sale calendars in Hong Kong, Paris, London and Dubai to absorb material once routed through New York.

- Tax counsel and entity structuring have become routine planning conversations, with many serious collectors restructuring holdings through international vehicles to manage tariff exposure.

- Who is this for?

- United States and international collectors, advisors and family offices managing tariff exposure across acquisitions, storage and the geographic distribution of significant art holdings.

- What is happening?

- An editorial read on how United States tariffs are reshaping collector behaviour, covering customs exposure, venue shift, free-port storage and the auction-house adaptation across regions.

- When did this emerge?

- Most relevant before any cross-border acquisition, during annual tax and estate-planning reviews and when collections are being relocated, lent or restructured for generational transfer.

- Where is this happening?

- Centred on the United States customs landscape and the European and Asian alternative venues, with free-port storage anchored in Geneva, Luxembourg, Delaware and Singapore.

- Why does it matter?

- Reading the tariff landscape correctly matters because the cost of getting it wrong now compounds across acquisitions, storage and the geographic shape of serious holdings.

The tariff exposure, mapped

The current tariff structure imposes meaningful costs on art entering the United States from a widening list of source countries, with the specific rates and exemptions changing as the trade negotiations evolve. The trade press, including the Art Newspaper and Artnet News, has tracked the practical effects across multiple shipments.

The traditional exemption for original works of art has narrowed in scope. Customs entries that previously moved cleanly now face additional documentation, longer hold periods, and case-by-case adjudication that adds friction even when the final tariff exposure is zero.

The cost effect for collectors is twofold: direct tariff exposure on certain categories of works, and indirect cost through shipping, storage, and broker fees that have risen materially across the segment.

How collectors are responding

The most visible adaptation has been venue shift. Collectors planning major acquisitions are increasingly closing transactions through European and Asian sale rooms when the work's geography permits. Christie's and Sotheby's London evening sales have absorbed material that might once have moved through New York, and Hong Kong has reabsorbed Chinese contemporary material that was routing through New York in the late 2010s.

Free-port storage has become more attractive. The Geneva, Luxembourg, and Singapore free ports continue to hold a meaningful share of high-value contemporary and post-war material, and the cost-benefit calculation has shifted further in their favour under the current tariff regime.

For collectors managing the logistics, our piece on best art transportation methods sets out the operational considerations.

The auction-house adaptation

Christie's, Sotheby's, and Phillips have all expanded their international sale calendars in response. Hong Kong, Paris, London, and Dubai have absorbed material that the New York sales would once have anchored, and the houses have invested in the logistical capacity to support the rotation.

Christie's Hong Kong evening sales now run at a tier comparable to its New York November sales for Asian contemporary material. Sotheby's Paris has built up its evening-sale calendar to accommodate European and trans-Atlantic consignors. Phillips' Hong Kong and London sales have grown into structurally important calendar dates.

The shift is not the end of New York as the dominant centre, but it is a meaningful redistribution. The November 2024 sales saw measurably stronger international participation than in prior cycles, and the November 2025 calendar is expected to extend the pattern.

The contemporary market's exposure

Contemporary works are the most exposed segment because the market is most actively international. Living artists working in studios from London to Lagos to Mexico City produce material that routinely crosses borders multiple times before reaching its end collector, and the tariff structure imposes friction at each crossing.

The blue-chip segment has more flexibility because the material is older and the provenance routes are established. Our blue-chip artists defining 2026 coverage tracks the segment that absorbs the regulatory friction with the least disruption.

The Ultra-Contemporary segment, where galleries ship work from studios to fairs to buyers within months of completion, is where the operational cost is felt most acutely. Our contemporary art collectors field guide sets out the broader segment.

Tax and entity planning

Collectors with international holdings are restructuring around the regulatory landscape. Art entities domiciled in jurisdictions with established art-friendly tax and customs frameworks, Luxembourg, Switzerland, Singapore, the United Kingdom, have absorbed a growing share of the segment's structuring activity.

For US-resident collectors, the tax and customs planning has become more involved. Our art collecting tax guide sets out the broader framework, and the trade strongly advises specialist counsel for any cross-border holding above a meaningful size.

The rule of thumb that emerges from the past two years: structure the holding before the acquisition, not after. The cost of restructuring an existing position is materially higher than the cost of acquiring through the right channel from the start.

The longer-term shape

The tariff regime is producing structural rather than cyclical effects. The geographic redistribution of transaction venues, the expansion of free-port storage, and the growth of European and Asian fair calendars are not temporary adjustments; they are the new operational topology of the market.

Collectors who continue to centre their activity on New York will face higher friction costs than collectors who treat the market as genuinely global from the start. The latter pattern is the one the trade has shifted toward and is unlikely to reverse even if the tariff structure later eases.

What the trade expects next

The houses are planning around a continued period of regulatory uncertainty. Sale calendars for 2026 are weighted more heavily toward London, Paris, and Hong Kong than at any point in the past decade, and the private-sale practices are absorbing material that would once have moved through public sale rooms because the negotiated channels offer more flexibility on customs treatment.

The fair calendar is reflecting the same shift. Art Basel Paris, Frieze London, TEFAF Maastricht, and Art Basel Hong Kong all expanded their 2025 footprints, and 2026 forecasts continue the trajectory.

What this means for collectors

The tariff cycle is the operating environment, not a passing disruption. The collectors who adapt are the ones treating venue, storage, and structuring as integral parts of the acquisition decision rather than afterthoughts.

The market is functioning; it is just functioning through a more distributed set of channels than it did in the 2010s. The work is more involved, but the underlying access to the same artists, dealers, and houses is intact.

We last reviewed this analysis in May 2026.

Frequently Asked Questions

Do tariffs apply to all art entering the United States?

The traditional exemption for original works of art has narrowed in scope under the current tariff structure, with rates and exemptions changing as trade negotiations evolve. Customs entries that previously moved cleanly now face additional documentation, longer hold periods, and case-by-case adjudication. The Art Newspaper and Artnet News track the specific rates in their ongoing coverage.

How are collectors avoiding tariff exposure?

Through venue shift, free-port storage, and entity structuring. Major acquisitions are increasingly closing through European and Asian sale rooms; Geneva, Luxembourg, and Singapore free ports hold a growing share of high-value material; and entities domiciled in established art-friendly jurisdictions absorb the structuring activity for cross-border holdings.

Has the auction-house calendar shifted?

Yes, meaningfully. Christie's, Sotheby's, and Phillips have all expanded their Hong Kong, Paris, London, and Dubai sale calendars in response. The November 2024 calendar saw measurably stronger international participation than in prior cycles, and 2025 and 2026 calendars are continuing the trajectory toward a more distributed venue map.

Should US collectors restructure their holdings now?

The trade strongly advises specialist counsel for cross-border holdings above a meaningful size. The rule that has emerged is to structure the holding before the acquisition, not after; the cost of restructuring an existing position is materially higher than acquiring through the right channel from the start. Our art collecting tax guide sets out the broader framework collectors should walk through with their advisors.

![]()

Stefanos Moschopoulos

Stefanos Moschopoulos founded The Luxury Playbook in Athens and has spent the better part of a decade following the auction calendar, the en primeur releases, and the watchmakers, gallerists, and shipyards the magazine covers. He writes the field guides and listicles that anchor the Connoisseur section — pieces built on Phillips and Christie's results, Liv-ex movements, and conversations with collectors he has met across Geneva, Bordeaux, Basel, and Monaco. His own collecting habits sit closer to watches and wine than art, and it shows in the level of detail in the magazine's coverage of those categories. Under his direction, The Luxury Playbook now publishes long-form field guides, market-defining year-end listicles, and the Voices interview series with the founders behind the houses and the brands.