Israel’s economy has long been heralded as one of the most resilient and innovative in the world, especially given the geopolitical pressures it faces daily. As a small nation, Israel has built a formidable economic engine, with a sharp focus on high technology and relentless innovation. But recent developments, from ongoing military conflicts to internal political unrest and shifting global economic currents, have raised serious questions about whether the strain is finally becoming too much.

Here’s a closer look at where things actually stand, what the key indicators are telling you, and whether the concern is warranted.

- Israel’s economy is absorbing simultaneous war costs, reservist mobilisation and a sharper-than-expected fiscal expansion this cycle.

- The shekel has held up better than headline risk would suggest, supported by central bank intervention and elevated foreign reserves.

- High-tech exports and venture funding remain the structural ballast that keeps the wider macro picture from rolling over.

- Sovereign credit metrics have deteriorated but still sit well inside the investment-grade band across the major rating agencies.

- Foreign direct investment has cooled at the margin, with allocators reweighting between core tech and defence-adjacent themes.

- For HNW allocators with Israeli exposure, the question is sizing and time horizon rather than whether to retain the position.

- Who is this for?

- Global allocators, family offices with Israeli exposure and macro investors tracking the durability of the Israeli economic model.

- What is happening?

- We are stress-testing the Israeli economy across currency, fiscal, technology and credit dimensions during a period of elevated conflict cost.

- When did this emerge?

- The analysis covers the current cycle in which war spending, reservist mobilisation and global rate pressure have arrived in parallel.

- Where is this happening?

- The dynamics described are anchored in Israel, with knock-on effects across the wider eastern Mediterranean and global tech corridors.

- Why does it matter?

- Israel remains a material allocation in many sophisticated portfolios, and a clear-eyed read of the macro picture is essential to managing the position.

Historical Economic Resilience

We anchor the Israeli macro picture to IMF Article IV consultations and country reporting from Reuters. The combination gives us both the technical detail and the live operational read.

For sovereign credit signals we watch S&P Global, Moody's, and Fitch. All three agencies have updated outlooks on Israel within the last year, and they tend to disagree just enough to be useful.

Israel’s economy has shown remarkable staying power over the decades, evolving from a primarily agrarian society into a globally recognized high-tech powerhouse. Since its founding in 1948, the country’s economic story has been one of constant reinvention. By 2022, Israel’s Gross Domestic Product reached approximately $521.69 billion, with a per capita income of $53,195, according to Nasdaq data.

The high-tech sector has been the engine driving that growth, accounting for 18.1% of GDP and nearly half of all Israeli exports at 48.3%.

Economic Stability During Global Crises

What makes Israel’s economic track record worth paying attention to is how it has held up when the rest of the world has crumbled. During the 2008 to 2009 global financial crisis, most developed economies took a severe beating. Israel’s economy, by contrast, stayed relatively composed.

A combination of prudent banking regulation, a diversified export base, and a tech sector largely insulated from traditional financial contagion helped cushion the blow.

- Robust Banking Sector: Israel’s banking system was less exposed to the toxic assets that precipitated the global financial meltdown, allowing it to weather the crisis more effectively than many Western economies.

- High Household Savings Rates: The tradition of high household savings provided a cushion that mitigated the impact of the economic downturn on domestic consumption.

- Prudent Fiscal Policies: The government’s cautious approach to fiscal management, including maintaining a relatively low level of public debt, helped shield the economy from the worst effects of the crisis.

The same story played out during the COVID-19 pandemic. While global supply chains collapsed and economies contracted sharply, Israel’s technology sector kept humming. The OECD reported that Israel’s economy contracted by just 2.4% in 2020, well below the average 4.7% contraction across OECD member countries. That kind of outperformance is not accidental. It reflects structural advantages built over decades.

Current Economic Challenges

That historical resilience, though, is being tested in ways that feel genuinely different this time. The ongoing conflict with Hamas, combined with rising tensions involving Hezbollah, has sent shockwaves through key sectors of the Israeli economy. You are looking at a situation where the disruptions are not temporary or superficial.

The damage is cutting deep, and the recovery path is far from certain.

Impact of the Conflict on GDP and Economic Activity

The numbers tell a stark story. According to the OECD, Israel’s GDP contracted by a staggering 19.4% in the fourth quarter of 2023. That is not a rounding error or a seasonal blip.

That is a collapse in economic output driven by the widespread dislocation the conflict has caused across virtually every sector of the economy.

The high-tech industry, which employs roughly 10% of the Israeli workforce and accounts for more than 50% of the nation’s exports, has taken a particularly hard hit. The mass conscription of young, highly skilled workers into military service has gutted productivity inside the sector.

The direct consequences hit export revenues and overall economic output. When your most valuable economic asset is human capital, and that human capital is being redirected to the front lines, the impact is immediate and severe.

High-Tech Sector Vulnerability

The vulnerability of Israel’s high-tech sector matters far beyond the sector itself. For years, it has been the primary engine of GDP growth, the source of Israel’s export competitiveness, and the reason global capital has flowed into the country at the scale it has. Losing momentum here does not just hurt one industry.

It undermines the entire economic narrative.

The conscription of skilled workers has created a labor shortage that is stifling innovation and cutting output. And this is not just a short-term problem. If the conflict drags on, the damage compounds.

Startups miss critical development windows, contracts get delayed or cancelled, and foreign partners start looking elsewhere. Israel’s long-term competitive advantage in the global technology market is genuinely at risk if this dynamic persists.

Broader Economic Disruptions

The tech sector is not alone in feeling the pressure. Tourism, which had been clawing its way back after the pandemic, has collapsed under the weight of security concerns, with international visitor numbers dropping sharply. That decline hits hard in regions where tourism is the backbone of local economic activity.

And if you look at infrastructure and transportation, you find similar stories of disruption, delays, and rising costs that are squeezing businesses from multiple directions at once. For context on how geopolitical stress affects property and investment markets more broadly, this perspective on investing in properties during inflation offers some useful parallels.

Government Response and Fiscal Challenges

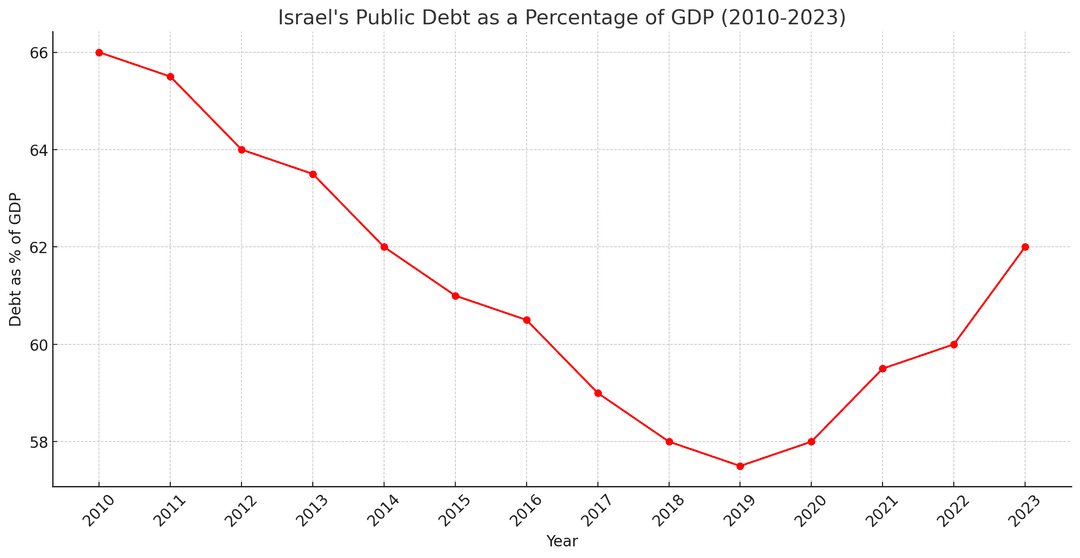

The Israeli government has responded by ramping up military spending and rolling out financial support for affected industries. The catch is that those measures carry a significant fiscal price tag. Israel’s public debt is projected to climb above 80% of GDP by the end of 2024, up from 71.2% in 2023, according to the Ministry of Finance.

A debt load at that level starts to crowd out the kind of long-term investment in infrastructure, education, and innovation that any country needs to sustain growth. The government is essentially spending tomorrow’s resources to manage today’s crisis.

Inflation and Currency Stability

Alongside the fiscal pressures, inflation has become a mounting problem. Supply chain disruptions and surging defense expenditures have pushed up the cost of goods and services across the board. The Bank of Israel has had to tighten monetary policy in response, raising interest rates to fight inflationary pressure.

But higher rates are a double-edged tool. They slow inflation, but they also slow growth, and right now Israel can ill afford another drag on its economy. The Israeli shekel has depreciated against major currencies, adding another layer of instability to an already fragile picture.

Impact of Political Instability

Layered on top of the conflict is a political climate that has introduced its own brand of economic turbulence. The controversial judicial reforms put forward by Prime Minister Benjamin Netanyahu have divided Israeli society in ways that have real, measurable consequences for business and investment.

The protests and civil unrest triggered by those reforms have not stayed contained to the streets. Their effects have rippled directly into the economic environment, landing hardest in the high-tech sector where confidence and capital flows are most sensitive to governance risk.

Erosion of Investor Confidence

When investors, whether domestic or international, start worrying about the strength of a country’s democratic institutions, capital moves. And that is exactly what has been happening in Israel. Reports from DW have documented a sharp pullback in investment, especially within the high-tech industry, as uncertainty around the political and legal environment has grown. Investors who had previously seen Israel as a stable, rule-of-law jurisdiction are reassessing that view.

The result is reduced capital inflows at precisely the moment Israel needs investment most.

Impact on the Israeli Shekel

The political turmoil has put direct downward pressure on the Israeli shekel. According to data from the Bank of Israel, the shekel depreciated by approximately 8% against the U.S. dollar in 2023, one of its steepest declines in recent memory. A weaker shekel makes imports more expensive, which feeds inflation and squeezes consumers.

For a country that relies on imported components and raw materials across multiple industries, that is a problem that compounds quickly.

That depreciation has made daily life more expensive for ordinary Israelis and has added another layer of uncertainty for businesses trying to plan ahead in a volatile environment.

Brain Drain and Its Long-Term Consequences

Perhaps the most concerning long-term risk sitting beneath all of this is brain drain. Israel’s high-tech economy is built on talent. Remove that talent, and the whole structure weakens.

Right now, a growing number of skilled professionals, frustrated by the political situation and unnerved by economic uncertainty, are seriously considering leaving. This is not hypothetical. The surveys are showing it, and the conversations are happening.

According to a survey from the Israel Innovation Authority, around 20% of high-tech employees are actively contemplating emigration because of the political climate. If even a fraction of that group follows through, the consequences for Israel’s innovation economy could be severe. You would be looking at a country that loses its edge in the very sector that has defined its global economic identity, with predictable downstream effects on foreign direct investment and technological progress.

Understanding which economic sectors hold up during periods of stress becomes especially relevant when a country’s anchor industry faces this kind of pressure.

Wider Economic Ramifications

The political instability has also hit sectors beyond tech. Tourism, already vulnerable due to regional conflict, has seen further declines as international travelers steer clear of a country perceived as politically volatile. The construction and real estate markets have slowed, with fewer foreign investors willing to commit capital to a market where the regulatory and political ground can shift unexpectedly.

Across the broader business community, expansion plans are being shelved and new projects are being put on hold. Companies are in wait-and-see mode, and that collective caution is dragging on economic momentum in the short to medium term. When businesses stop moving, growth stalls.

The War’s Economic Toll

The cumulative financial cost of the conflict is staggering. The Bank of Israel has projected that the total economic impact of the war could reach approximately 198 billion shekels, roughly $53 billion. That figure sweeps in disruptions across commerce, tourism, and investment flows, three pillars that Israel’s economy has historically counted on for stability and growth.

Impact on Commerce and Investment

Commercial activity has been battered. Businesses in conflict-affected areas have had to shut down entirely, and even those operating at a distance from the fighting are dealing with reduced consumer spending and heightened uncertainty. Foreign direct investment tells its own story.

According to the Israel Central Bureau of Statistics, FDI dropped by approximately 15% in the first quarter of 2024, as investors grew increasingly cautious about deploying capital into an unstable environment. That kind of pullback has long-lasting consequences for a country that depends on foreign capital to fuel its innovation economy.

Tourism Sector Hit Hard

Tourism normally contributes around 6% to Israel’s GDP and supports thousands of jobs across hospitality, retail, and services. The conflict has brought that sector to its knees. The Israeli Ministry of Tourism reported that international visitor arrivals in 2024 fell by more than 60% compared to the same period in 2023.

Travel warnings issued by multiple governments have effectively closed off a major source of foreign currency income. The knock-on effects for employment and service-sector businesses that depend on tourist spending are substantial and will take years to fully unwind even after conditions improve.

Projected Economic Growth Slowdown

The OECD revised Israel’s growth projections downward as a direct consequence of these disruptions. The updated estimate put GDP growth at 1.9% for 2024, down from 2% in 2023. That might sound like a modest decline on paper, but the number masks the depth of the structural damage underneath.

Reduced consumer confidence, falling investment, and ongoing challenges in both tourism and technology are all pulling in the same direction, and none of those pressures resolve overnight.

Tech Industry Under Pressure

Israel’s tech sector has historically been the economic shock absorber, the part of the economy that holds up and even accelerates when other sectors falter. The current conflict is different, though. The tech workforce itself has been disrupted, with a large share of skilled employees now in military service.

Projects are delayed, innovation cycles have slowed, and the sector’s overall output has declined. The usual buffer is no longer fully operational.

The stakes here are enormous. Tech accounts for more than 10% of the workforce and over 50% of the country’s exports. Every month of reduced productivity is a month of lost output that is hard to recover.

And if global tech companies operating in Israel decide the instability is too great and begin reducing their footprint in the region, the loss of foreign investment and expertise compounds the problem. That is a scenario Israel’s policymakers need to take seriously, and fast.

Future Outlook

Israel’s economy, for all the battering it has taken, still has real foundations to build a recovery on. The technological infrastructure is established, the financial system is relatively sound, and the country has a documented track record of bouncing back. But the path to recovery is not automatic.

It depends on a specific set of conditions coming together, and right now, several of those conditions are missing.

Conflict Resolution and Economic Stability

The single most important step toward economic recovery is ending the conflict. A cessation of hostilities would allow economic activity to resume across sectors that have been frozen or severely disrupted. According to the Israel Central Bureau of Statistics, every month of active conflict is costing the country a 2 to 3% GDP contraction.

That is an enormous ongoing toll, and it underscores just how much the economic recovery is contingent on peace.

Restoring peace would also revive tourism in a way that no government stimulus package can replicate. The tourism sector generated approximately $8.3 billion in revenue in 2019. Getting anywhere close to that level again requires international visitors to feel safe, and that means the guns have to go quiet first.

A recovery in tourism would inject foreign currency back into the economy and provide a much-needed lift to hospitality, retail, and the many service businesses that feed off visitor spending. The relationship between geopolitical stability and real estate values is another dimension worth watching, and understanding the phases of the real estate market cycle can help you read those signals.

Political Stability and Investor Confidence

Political instability has been its own separate anchor dragging on Israel’s economic prospects. The judicial reform controversy and the mass protests it triggered have spooked investors and weakened the shekel. By early 2024, the shekel had depreciated by approximately 15% against the U.S. dollar, a direct reflection of investor anxiety about where the country is headed politically and economically.

Rebuilding that confidence is not optional. It is a prerequisite for recovery. The Israeli government needs to take credible steps toward political stability, which may well mean reconsidering or walking back the most contentious elements of the judicial reforms.

A stable, predictable political environment would bring capital back. According to the OECD, FDI in Israel could recover by 5 to 7% annually if political stability is restored and the rule of law is reinforced. That is real money, and it would fund the kind of innovation-led growth Israel needs.

Supporting the High-Tech Sector

Israel’s high-tech sector, often called Silicon Wadi, has been the cornerstone of the nation’s economic success for good reason. It drives GDP, powers exports, and attracts global talent and capital. But the conflict has hit it hard, above all through the conscription of skilled workers who are the sector’s lifeblood.

Without targeted intervention, the damage to this sector risks becoming structural rather than cyclical.

One practical lever is tax breaks and grants for tech companies that maintain or grow their headcount during the conflict. Another is aggressive talent retention programs aimed at countering the brain drain that is already underway. A survey by Start-Up Nation Central found that nearly 30% of tech professionals are considering relocating abroad due to the combined pressures of political and economic instability.

Relocation subsidies, housing assistance, and enhanced career development programs could change those calculations. Keeping Israel’s tech talent at home is not just good for the sector. It is the single most important thing the country can do to protect its long-term competitive edge in the global technology arena.

We last reviewed this analysis in May 2026.

![]()

Stefanos Moschopoulos

Stefanos Moschopoulos founded The Luxury Playbook in Athens and has spent the better part of a decade following the auction calendar, the en primeur releases, and the watchmakers, gallerists, and shipyards the magazine covers. He writes the field guides and listicles that anchor the Connoisseur section — pieces built on Phillips and Christie's results, Liv-ex movements, and conversations with collectors he has met across Geneva, Bordeaux, Basel, and Monaco. His own collecting habits sit closer to watches and wine than art, and it shows in the level of detail in the magazine's coverage of those categories. Under his direction, The Luxury Playbook now publishes long-form field guides, market-defining year-end listicles, and the Voices interview series with the founders behind the houses and the brands.