Not too long ago, the UK stood proudly as a global economic powerhouse, revered for its industrial might, political stability, and financial influence. The image of bustling London streets filled with well-dressed professionals, the hum of innovation, and the steady drumbeat of growth now feels like a distant memory. The narrative has shifted dramatically.

What was once an empire that held sway over a quarter of the world is now battling deep-seated economic woes, struggling to maintain the standard of living its citizens had long taken for granted.

You wouldn’t be the first to scoff at the idea of comparing the UK to a “third world country.” But when you peel back the layers and take a hard look at the facts, the situation becomes a lot less laughable.

Stagnant productivity, rising inflation, an unmanageable national debt, and a workforce that’s increasingly checking out. The UK’s economy is deteriorating at a pace that’s difficult to ignore.

What follows is an honest look at the profound economic challenges facing the UK, the statistics behind them, the causes driving them, and the very real consequences for anyone with money, assets, or interests tied to Britain.

A Brief Overview of the UK’s Economic Decline

The clearest documentation of the UK growth slowdown sits in the OECD economic survey series and the IMF Article IV reports. Reading them alongside each other gives us a less politicised view than most UK commentary offers.

For real-time macro coverage we read the Financial Times and the Wall Street Journal. The two have different editorial leans, which is precisely why pairing them is useful.

To accurately assess how serious the UK’s economic deterioration really is, you need to start with a clear baseline. Real disposable income, what households actually have left after taxes and essential expenses, has gone virtually nowhere for more than a decade.

According to the Office for National Statistics (ONS), between 2010 and 2026, inflation-adjusted household incomes have grown by less than 0.5% annually. That’s a rate that lags far behind rising living costs, and it’s been grinding on for years.

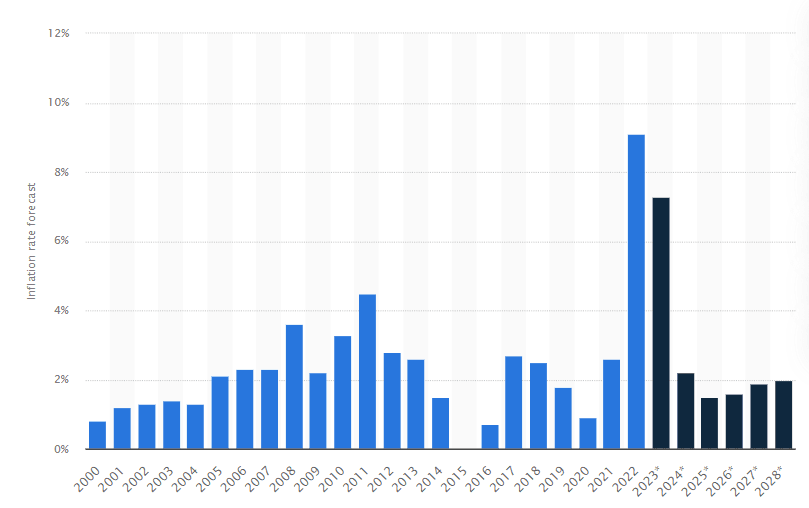

At the same time, the Consumer Prices Index has surged. Inflation peaked at 11.1% in October 2022, the highest in over 40 years. Although it eased slightly going into 2026, many essential goods, energy, food, housing, are still dramatically more expensive than they were just a few years ago.

That sustained price pressure has eroded purchasing power and pushed millions of UK households toward real financial instability.

What makes this even more striking is that London, long the UK’s economic engine, is not immune. The capital still contributes nearly 23% of national GDP, but it’s becoming increasingly disconnected from the economic realities faced by the rest of the country.

The City of London and Canary Wharf are still major global finance hubs, but stress is building beneath the surface.

Despite higher nominal wages, real wage growth in London has been minimal once you adjust for inflation and the capital’s eye-watering housing and transport costs. ONS data puts median annual earnings for full-time London employees at roughly £44,370 in 2024. But that income gets absorbed fast when you’re living in one of the world’s most expensive cities.

And there’s a deepening economic rift between the capital and everywhere else.

Southeast England, including London, produces almost half of the UK’s GDP while accounting for just a third of its population. Meanwhile, regions like the North East, West Midlands, and parts of Wales have seen little to no real growth, with lower wages, higher unemployment, and deteriorating public infrastructure.

The UK is becoming economically polarized. Pockets of affluence persist in London and its surrounding commuter belts, but large stretches of the country face stagnation or outright decline. Nationally, real household income has been flat for nearly 15 years, meaning that despite modest nominal wage increases, British workers are experiencing no meaningful rise in their living standards.

In comparative terms, UK households are falling behind their international peers. Research from the Resolution Foundation shows that typical British middle-class households are now poorer than their counterparts in France, Germany, and the United States, with Norwegian households enjoying significantly higher disposable income and wealth accumulation.

The deterioration in living standards hits the British middle class hardest of all, once the engine of economic stability, now a group struggling to cover essentials. Rising energy bills, expensive childcare, unaffordable housing, and stagnant wages are chipping away at middle-class security. If you’re thinking about relocating your wealth or residency out of the UK, you’re far from alone, and the numbers explain why.

The UK’s Productivity Crisis

One of the most critical, and often underreported, drivers of the UK’s long-term economic stagnation is its persistent productivity crisis.

In economic terms, productivity measures the efficiency with which goods and services are produced. It’s a key determinant of a nation’s competitiveness, wage growth, and overall standard of living.

The UK has experienced one of the sharpest productivity slowdowns in the developed world. Full stop.

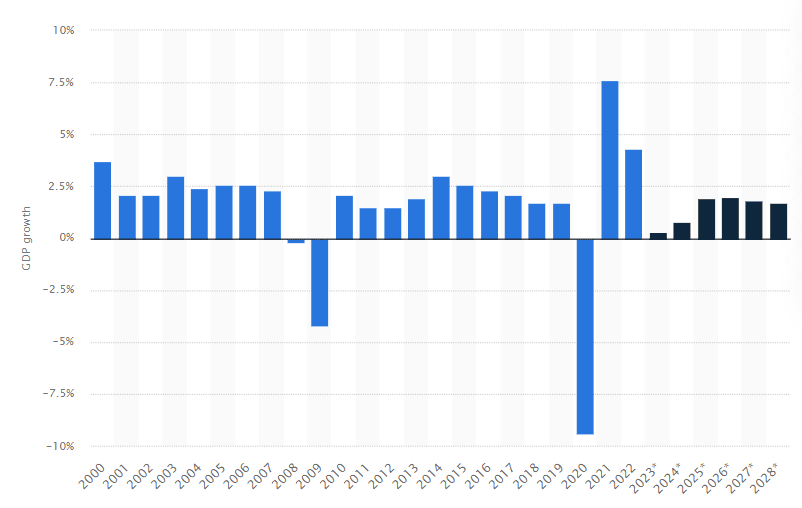

Before the 2008 global financial crisis, UK productivity was growing at a healthy pace of around 2% per year, broadly in line with G7 averages. Since 2008, that growth has collapsed, averaging just 0.5% annually between 2010 and 2026, according to ONS data.

That decline puts the UK second-to-last among G7 economies for productivity performance, ahead of only Italy. Germany and the United States have maintained far stronger productivity trajectories over the same period.

Stagnant productivity isn’t just a statistical concern. When output per worker fails to improve, businesses face higher unit costs and find it harder to compete globally. That undermines the UK’s ability to attract foreign direct investment, grow exports, and support long-term industrial expansion.

- For example, British manufacturers in the automotive and aerospace sectors—once pillars of UK industrial strength—have struggled to keep pace with their German and French counterparts, due in part to lower capital investment and slower adoption of automation and digital infrastructure.

- Sectors like construction, retail, and public administration continue to report some of the lowest productivity per hour worked in Western Europe, highlighting inefficiencies that remain unresolved.

The productivity malaise also hits wages directly. In most advanced economies, productivity and wages rise together. In the UK, that relationship has broken down. With businesses squeezed by slim margins and elevated input costs, many are reluctant to raise wages, even when labor is scarce.

According to the Institute for Fiscal Studies, real wages in the UK in 2026 are still lower than they were in 2008. That makes this one of the worst stretches of wage stagnation in post-war history. Lower wages mean less consumer spending, weaker domestic demand, and further drag on GDP growth.

The UK’s productivity crisis is both a cause and a symptom of its broader economic decline. It feeds on itself.

Poor productivity leads to stagnant wages. Stagnant wages reduce consumer spending and limit tax revenues. That results in underfunded public services and insufficient investment in the sectors, infrastructure, education, innovation, that are needed to revive productivity in the first place.

With capital investment in the UK ranking lowest among G7 countries as a share of GDP, according to OECD data, the underlying drivers of productivity, technology adoption, skills training, and research and development, are chronically underfunded. Public sector productivity, especially within the NHS and local government, has also been declining, adding further fiscal pressure to an already strained state.

Brexit’s Economic Bombshell

The decision to leave the European Union in 2016 sent shockwaves through the UK’s economy, and the full impact is still playing out. The most immediate consequence was a sharp drop in foreign investment. Domestic and international investors alike grew wary of the political and economic uncertainty Brexit introduced.

Between 2016 and 2021, foreign investment in the UK fell by 25%, a massive blow to an economy already wrestling with sluggish growth and stagnant productivity.

The long-term economic fallout is even more troubling. By severing its relationship with the EU, the UK effectively cut itself off from one of the largest trading blocs in the world. Trade barriers, tariffs, and regulatory hurdles have made it considerably more expensive for UK companies to do business with European partners, and the consequences have rippled through manufacturing, finance, and agriculture.

But the damage runs deeper still. Brexit has contributed to a 6% reduction in the UK’s Gross Value Added, a measure of the value of goods and services produced in the country. That translates to roughly £140 billion stripped from the UK economy, a staggering figure that puts the scale of the consequences in sharp relief.

London alone has absorbed approximately £30 billion in lost economic output and nearly 300,000 jobs. The financial services sector, once the crown jewel of the British economy, has taken particularly heavy hits as firms seek more stable footing within the EU. You can see how this shapes the broader picture by reading about which markets are most exposed when geopolitical shocks hit.

COVID-19’s Contribution to Economic Destruction

Just as the UK was beginning to grapple with the full weight of Brexit, COVID-19 arrived and pushed the economy into an even deeper crisis. The government borrowed an additional £280 billion during the pandemic to keep businesses and individuals afloat. That spending helped prevent a total economic collapse, but it also pushed the UK’s national debt to levels that are difficult to justify over the long term.

At first, low interest rates made debt management relatively manageable. But as inflation surged and interest rates climbed, servicing that debt became increasingly painful. The government now pays over £100 billion annually in debt repayments, a figure that crowds out spending on healthcare, education, and social welfare.

The trade-off is brutal and very real.

COVID-19’s impact on the UK workforce has been equally damaging. Millions of jobs were lost during the pandemic, and while many have returned, a significant portion of the population has drifted into economic inactivity. This includes retirees, students, and caregivers, but also a growing number of people who have simply stopped looking for work.

As of 2026, around 11 million people in the UK are classified as economically inactive. That’s a number that should give any serious observer pause.

Inflation and Rising Debt

Debt sustainability commentary from S&P Global and Moody's provides a useful pricing signal on the UK's path. Our UK prime markets coverage tracks how that filters into property.

Inflation has been another punishing force for the UK in recent years. The cost of goods and services has climbed sharply, eroding consumer purchasing power and making it harder for businesses to stay viable. High inflation has also raised the cost of servicing national debt, creating a cycle where rising prices feed rising debt, and rising debt makes inflation harder to control.

Energy prices tell that story most visibly. Global pressures, including the war in Ukraine, sent UK energy costs into orbit. British households are now paying roughly three times more for heating than they were just a few years ago.

To soften the blow, the government borrowed an additional £60 to £100 billion for energy support, further swelling a national debt that was already under serious strain.

Workforce Challenges and Immigration

The UK’s workforce challenges have been amplified by demographic shifts and changing social dynamics. As the population ages, the pool of available workers shrinks. At the same time, many younger people are opting out of traditional employment in favor of further education or different ways of living.

The government has attempted to address the labor shortage by opening borders to workers from South Asia and Sub-Saharan Africa.

But that influx of immigrant workers has brought its own complications. Social tensions have risen sharply, with protests and unrest becoming a more regular feature of life in parts of the country. Many British citizens feel their economic struggles have been worsened by large-scale immigration, and that resentment has hardened into division.

The debate cuts both ways. Without immigrant labor, sectors like healthcare, agriculture, and construction would struggle to function. And yet large-scale demographic change has placed real strain on housing, public services, and local communities, strain that hasn’t been adequately managed.

The social fabric of the UK is being tested. Government policy on integration has been largely reactive rather than forward-thinking, leaving both newcomers and long-standing residents feeling let down. The result is a deepening social divide that compounds an already fragile economic situation.

For wealthy individuals weighing up where to plant roots or capital, this kind of instability is a factor worth taking seriously. Our relocation guide for high-net-worth individuals covers exactly what to consider when evaluating a country’s stability.

The political climate around immigration has grown increasingly hostile, with anti-immigration sentiment fueling the rise of far-right movements and protests. The UK clearly needs immigrant labor to sustain key parts of its economy. But without a structured, forward-looking immigration policy that balances economic need with social cohesion, this issue will keep adding pressure to an already lengthy list of problems.

Forecasting Continued Economic Decline

The economic outlook for the UK, looking ahead, is not encouraging. Without meaningful policy shifts, the country is on a trajectory of further decline. By 2035, the UK’s real Gross Value Added is projected to be £311 billion lower than it would have been without the economic headwinds it now faces.

London, historically the driver of UK economic success, is expected to see its GVA shrink by £63 billion over that same period. That forecast underscores just how deeply the current crisis has embedded itself in the country’s long-term direction of travel.

The job market is another area where the picture looks bleak without intervention. Financial services and manufacturing, already battered by Brexit and the uneven post-pandemic recovery, are expected to face further pressure as businesses migrate to more stable environments. That will widen the already significant gap between London and the rest of the UK, with regional economies slipping further behind.

The cost of living crisis shows no sign of resolving itself either. Inflation is proving stubborn, and household incomes are unlikely to rise fast enough to keep pace with the cost of basic necessities.

Food prices are expected to keep climbing, squeezing families who are already stretched thin. That reduces disposable incomes, dampens consumer spending, and feeds the kind of slow economic downturn that’s very hard to pull out of once it takes hold.

Energy prices loom large as well. Government subsidies have provided some short-term relief, but they’re not a sustainable solution. As global energy markets stay volatile, the UK could face an even more acute energy crisis in the years ahead.

Rising energy costs don’t just hurt households, they erode business margins and ripple through the entire economy, pushing more people toward poverty and threatening companies already operating on the edge.

Is There Any Hope?

It’s easy to feel disheartened when you look at where the UK’s economy stands right now and where it appears to be heading. But history has a habit of surprising people. Economic crises have sometimes acted as catalysts for genuine, meaningful reform.

The UK has overcome serious adversity before, and it’s possible that this period of hardship could push the country toward bold, structural change.

Any real recovery starts with productivity. That means investing in education, skills training, and infrastructure, and creating conditions where businesses feel confident enough to innovate and adopt new technologies. Without that foundation, the UK will keep falling behind other major economies, and the gap will only widen.

The housing crisis needs to be tackled with equal urgency. The UK’s housing market is under serious strain, and the supply of affordable homes, especially in high-demand urban centers, is nowhere near sufficient. Getting that right would relieve pressure on households, give a shot in the arm to the construction industry, and create jobs that stimulate broader economic activity.

For those interested in how real estate markets respond to economic stress, the dynamics around financing real estate in Europe offer a useful point of comparison.

Workforce challenges also need a serious rethink. That means creating accessible jobs, not just jobs in theory. Flexible working arrangements, meaningful childcare support, and retraining programs could bring more people back into the labor market.

And immigration policy needs to be redesigned from the ground up, attracting the talent the UK genuinely needs while also addressing the social tensions that poorly managed large-scale immigration creates.

The national debt problem can’t be ignored either. Borrowing was necessary to navigate the pandemic and the energy crisis, but the UK now needs a credible long-term plan to bring debt back to manageable levels. That means hard choices about public spending and taxation.

Without that plan, the UK risks being trapped in a cycle of rising debt and sluggish growth that becomes increasingly difficult to escape.

Energy policy will be central to any recovery worth the name. Investing in sustainable, renewable energy sources would reduce the UK’s exposure to volatile global markets while positioning the country as a serious player in the green economy. Done right, that creates jobs, builds new industries, and provides a foundation for durable long-term growth.

Is the UK Truly Becoming a “Third World” Country?

Calling the UK a “third world country” might still sound like an overstatement. But when you sit with the data, the comparison becomes harder to dismiss. High debt, sluggish productivity, persistent inflation, a shrinking workforce, and growing social inequality are all characteristics of economies struggling to hold their position in the developed world.

The UK isn’t there yet. But it’s on a path that, without serious intervention, leads somewhere uncomfortable.

London still functions as a global financial hub and a center of wealth, as the Financial Times regularly documents in its coverage of UK financial markets. But beyond the capital, the picture darkens fast. Regional disparities are widening, and for millions of people living outside London, the economic opportunities that once defined the UK as a prosperous nation are quietly slipping away.

If these structural problems go unaddressed, the UK risks becoming a country of stark contrasts, a wealthy capital city surrounded by regions that bear less and less resemblance to a thriving, first-world economy.

FAQ

Why do some people say the UK is becoming a ‘third world’ country?

The phrase reflects deep concerns about the UK’s economic decline, marked by stagnant wages, poor productivity, rising inflation, and growing inequality. While the UK is still classified as a high-income country, structural issues such as regional poverty, public service erosion, and a shrinking middle class have drawn comparisons to struggling economies.

How has productivity affected the UK’s economic performance?

UK productivity growth has slowed dramatically since the 2008 financial crisis, averaging just 0.5% annually versus 2% before. This stagnation has weakened wage growth, reduced business competitiveness, and placed the UK near the bottom of the G7 for productivity.

What economic impact has Brexit had on the UK?

Brexit triggered a 25% drop in foreign investment between 2016 and 2021, increased trade barriers, and caused significant job losses in sectors like finance and manufacturing. The UK’s Gross Value Added (GVA) has declined by £140 billion, with London alone losing an estimated £30 billion in economic output.

How did COVID-19 worsen the UK’s financial situation?

The UK government borrowed £280 billion during the pandemic, pushing national debt to record levels. As of 2025, £100+ billion is spent annually on debt servicing. Meanwhile, over 11 million people are now classified as economically inactive, contributing to labor shortages and reduced productivity.

What’s driving the UK’s inflation crisis?

Inflation surged to 11.1% in 2022, driven by global energy shocks, supply chain disruptions, and domestic policy responses. Although inflation has eased in 2025, essential costs like housing, energy, and food remain significantly elevated, squeezing household budgets and eroding real income.

How serious is the UK’s national debt problem?

The UK’s public debt now exceeds £2.5 trillion, with interest payments alone costing over £100 billion per year. High inflation and rising interest rates have made debt servicing increasingly unsustainable, limiting the government’s ability to invest in public services or stimulate growth.

Is the UK still considered a developed country?

Yes. The UK remains part of the OECD and G7 and is classified as a high-income economy. However, several long-term indicators, like low real wage growth, rising poverty, and declining regional investment, are eroding its position relative to other developed nations.

What does the future look like for the UK economy?

Without significant policy reform, forecasts show that the UK’s GVA could be £311 billion lower by 2035 than pre-crisis projections. Continued pressure on household incomes, public services, and key industries suggests a slow, uneven recovery unless structural issues are addressed head-on.

We last reviewed this analysis in May 2026.

![]()

Stefanos Moschopoulos

Stefanos Moschopoulos founded The Luxury Playbook in Athens and has spent the better part of a decade following the auction calendar, the en primeur releases, and the watchmakers, gallerists, and shipyards the magazine covers. He writes the field guides and listicles that anchor the Connoisseur section — pieces built on Phillips and Christie's results, Liv-ex movements, and conversations with collectors he has met across Geneva, Bordeaux, Basel, and Monaco. His own collecting habits sit closer to watches and wine than art, and it shows in the level of detail in the magazine's coverage of those categories. Under his direction, The Luxury Playbook now publishes long-form field guides, market-defining year-end listicles, and the Voices interview series with the founders behind the houses and the brands.