Traditional finance theory teaches a pretty straightforward relationship between risk and market conditions. High beta “trash stocks” sitting at the riskiest, most speculative end of equity markets should rise more aggressively when overall market sentiment is buoyant and capital flows freely toward risk assets.

And when downturns hit, those same worst US stocks should fall harder as investors flee to quality and capital preservation takes priority over speculative gains. Yet 2026 has flipped that script entirely, with junk stocks soaring while quality blue chips bleed value according to Financial Times reporting, creating a paradox that challenges conventional market wisdom and leaves both institutional and retail investors questioning whether established patterns still apply.

The “trash stocks” category encompasses a diverse collection of equity market outcasts united by common characteristics that mark them as speculative or distressed.

So what actually falls into this category? Think unprofitable technology companies, heavily shorted stocks where hedge funds have placed concentrated bets against survival, high beta names that amplify market movements whether up or down, and companies trading under $5 per share that appeal to retail traders seeking lottery ticket upside. Together, they round out the speculative and distressed end of equity markets.

Historical precedents exist for temporary rallies in the most hated stocks. The most memorable came during the 2020 to 2021 meme stock era, when retail investors orchestrated massive rallies in heavily shorted companies like GameStop and AMC Entertainment.

But that phenomenon unfolded during an overall bull market backed by monetary stimulus, near zero interest rates, and fiscal transfers that put cash directly into retail accounts. The current environment is a different animal entirely. Trash stocks are rallying despite broader market weakness, economic uncertainty, and tightening financial conditions that should theoretically punish exactly these kinds of speculative positions.

For clarity, here is how you can define the worst stocks in this context. These are stocks belonging to the unprofitable tech basket, the most-shorted basket, the sub-$5 cohort, or high-beta factor groups.

Junk rallies and quality-versus-low-quality dispersion are well-tracked by the institutional research desks. Goldman Sachs publishes factor research that captures these episodes, and Morgan Stanley tracks the short-squeeze dynamics that often sit underneath them.

The data backbone sits with the index and rating providers. S&P Global hosts the index methodology behind the headline benchmarks, and Morningstar covers the factor-fund performance that captures these tape rotations in real time.

Key Takeaways & The 5Ws

For deeper context, the breakdown in how to manage risk when the tape turns against quality is worth reading alongside this analysis.

- In 2026, the riskiest “trash stocks” are rallying while quality blue chips lag, inverting the usual risk-on / risk-off playbook that traditional finance expects.

- Narrowing junk-bond spreads and easier credit conditions disproportionately benefit weak, cash-burning companies whose survival is most sensitive to funding costs.

- Retail traders now dominate sub-$5 and high-beta names, turning low-quality stocks into momentum casinos where social media flows can overwhelm fundamentals.

- Crowded quant shorts and factor bets in unprofitable, high-beta stocks have triggered violent short squeezes as systematic hedge funds are forced to cover into rising prices.

- History suggests these moves tend to be temporary “quant tremors,” with sharp reversals once deleveraging is complete and markets re-price businesses on cash flow and solvency rather than pure momentum.

- Who is driving it?

- Retail traders, high-frequency and quant hedge funds, and speculative investors concentrating in unprofitable tech, heavily shorted names, and low-priced high-beta stocks are the main actors behind the reversal in the usual quality-versus-junk pattern.

- What is happening?

- A paradoxical 2026 environment where distressed and speculative equities are surging despite broader fragility, driven by easier credit, retail flows, and systematic short covering, creating a wide gap between price action and business quality.

- When does it tend to last?

- The “trash rally” has unfolded into early 2026 after multiple quant-driven tremors in 2025, and typically persists only while spreads stay tight, volatility stays elevated, and deleveraging flows continue, conditions that can reverse abruptly.

- Where is it most visible?

- Primarily in U.S. equities, especially unprofitable tech and sub-$5 names on major exchanges where retail order flow is heaviest, while cash-generative blue chips and many high-quality S&P 500 constituents have lagged.

- Why is it happening now?

- Because even small improvements in funding conditions, combined with crowded shorts and retail speculation, deliver the biggest relative boost to companies closest to the edge, yet if macro tightens or sentiment fades, these names face the steepest downside and the fastest snap-back to fundamentals.

What Is Driving The Rally Of The Worst US Stocks Despite Broader Market Weakness?

The seemingly counterintuitive rally finds its primary explanation in how easing financial conditions disproportionately benefit the weakest companies rather than the strongest. US junk bond spreads have narrowed sharply to one-year lows, according to the ICE BofA US High Yield Index tracked by Bloomberg, with the option-adjusted spread dropping 16 basis points as credit markets signal improving conditions for risky borrowers.

That spread compression makes borrowing substantially cheaper for companies that depend on credit markets for survival. The survivability of cash-generating blue chip corporations was never in question. These companies maintain fortress balance sheets, generate consistent free cash flow, and access credit markets at favorable terms regardless of whether spreads are wide or narrow.

Riskier, unprofitable companies that face genuine bankruptcy risk when credit markets tighten gain disproportionately when borrowing costs fall and near-term survival concerns recede, even temporarily. The lifeline gets longer, and the market prices that in fast.

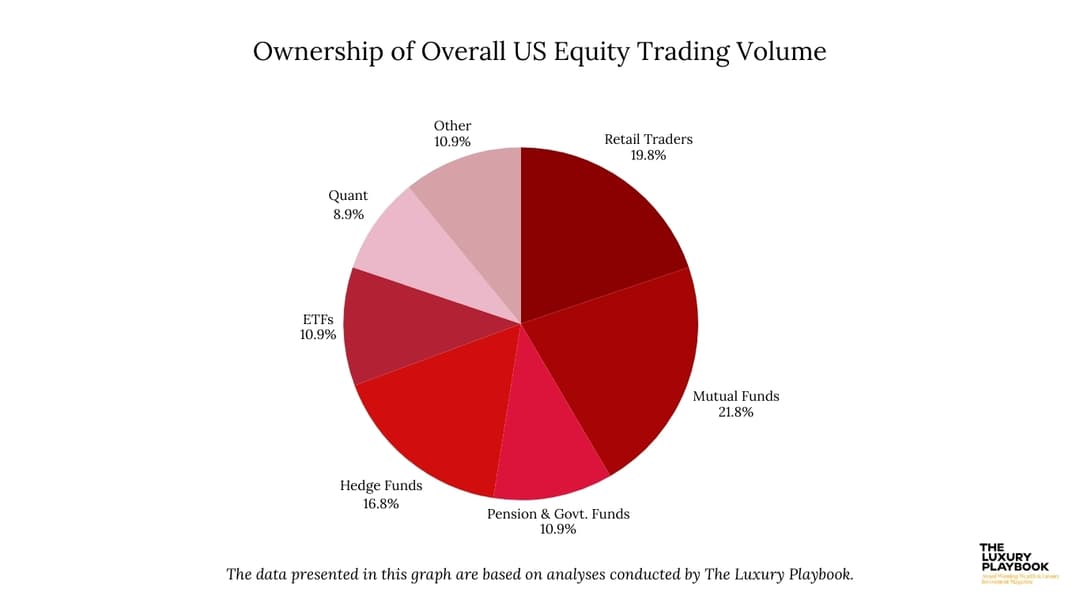

At the same time, the composition of market participants trading these speculative names has shifted dramatically toward retail investors who now dominate low-price stock universes. Retail traders account for over 20% of overall US trading volume according to recent market structure data, which means more activity than hedge funds and mutual funds generate combined when measured by share volume.

That retail presence concentrates even more heavily in stocks trading under $5 per share, where institutional participation stays minimal due to compliance restrictions, liquidity concerns, and the reputational risk of owning penny stocks. The same retail force that drove the 2020 to 2021 meme stock rallies has returned with coordinated buying in speculative names, amplified through social media platforms where investment thesis discussions and momentum signaling happen in real time across millions of participants. If you want to understand how retail traders now move markets in ways that were impossible before commission-free trading and fractional shares, understanding how investment clubs and collective capital work gives you useful context.

Beyond retail enthusiasm, systematic hedge fund short covering has created violent squeezes that accelerate moves far beyond what underlying fundamentals would justify. Quantitative hedge funds had established crowded short positions in high beta and unprofitable stocks based on factor models suggesting these names should underperform as economic conditions normalize and easy money policies reverse.

But when those positions moved sharply against their models, algorithmic deleveraging systems forced covering regardless of fundamental outlook. That created feedback loops where short covering drives prices higher, triggering more short covering as stop losses activate and risk management systems demand position reductions.

UBS estimates that US-focused quant funds lost 2.8% in the first two weeks of 2026 alone, marking their worst start to a year since the October 2025 quant tremors that similarly forced rapid deleveraging. This systematic covering transforms what might have been modest rallies into explosive moves as algorithms chase prices higher just to exit positions that were sized on assumptions of continued decline.

Should Investors Chase The Trash Rally Or Prepare For The Inevitable Reversal?

Despite the powerful forces supporting the current rally, historical patterns should give you serious pause before chasing these moves at current levels. The year 2025 witnessed three separate quant tremors during June through July, October, and other periods that all coincided with temporary rallies in unprofitable and heavily shorted stocks before eventually reversing. And as you can see from studying other counterintuitive market stories, what looks like a trend change often turns out to be a dislocation.

Each tremor created a brief window where trash stocks dramatically outperformed quality names, attracting attention from retail investors and momentum traders who interpreted the moves as sustainable trend changes rather than temporary dislocations.

But these episodes eventually stabilized without triggering systemic crisis. In each case the speculative rallies reversed as quant funds completed their deleveraging, retail enthusiasm waned, and markets returned to rewarding fundamentals over momentum.

Timing these reversals proved impossible even for sophisticated institutional traders. Late entrants who bought after rallies had already advanced 20% or 30% suffered substantial losses when mean reversion occurred within weeks or even days.

Unlike institutional investors who employ strict stop-loss disciplines and risk control systems that automatically reduce positions when losses exceed predetermined thresholds, retail traders in stocks priced at $5 and under often hold through significant declines. They expect a “diamond hands” recovery based on meme stock era experiences where some heavily shorted stocks eventually bounced back after brutal drawdowns.

That buy-and-hold mentality works during periods when retail buying pressure continuously refreshes and new participants enter to support prices. But when sentiment shifts and the marginal buyer disappears, liquidity evaporates with alarming speed in low-quality names that lack the institutional bid that supports blue chip stocks even during market stress.

Retail investors hoping to exit at reasonable prices discover that bids vanish, spreads widen dramatically, and the only available buyers demand prices far below recent trading levels. You end up trapped in positions that may take months or years to recover, if they recover at all.

Perhaps most concerning from a fundamental perspective is the disconnect between current valuations and underlying business realities. Anyone evaluating these positions as investments rather than speculative trades should find that gap troubling.

S&P 500 companies collectively generate enormous profits, return cash to shareholders through dividends and buybacks, and demonstrate business model viability through decades of operating history across multiple economic cycles. These companies may face cyclical headwinds, but their survival is not in question.

The unprofitable technology index constituents rallying most aggressively burn cash quarter after quarter, depend entirely on credit markets staying open and willing to finance continued operations, and face existential questions about whether their business models will ever achieve profitability at scale. If macroeconomic conditions deteriorate through recession, renewed inflation forcing central bank tightening, or credit spreads widening as default concerns resurface, the survival risk returns immediately. This is a dynamic that differs sharply from the AI investment case, where at least some underlying revenue growth justifies elevated valuations.

If you are tempted to participate based on fear of missing out, remember that in every previous cycle, the transition from euphoric rally to brutal reversal came with little warning. Those who confused temporary momentum with sustainable trends ended up holding positions that destroyed capital rather than building wealth.

The question for 2026 is not whether trash stocks can keep rallying in the near term, because momentum and technical factors often extend moves beyond what seems rational. The real question is whether the fundamental disconnect between business reality and market pricing eventually matters, as it has in every previous cycle where speculation temporarily triumphed before fundamentals reasserted dominance. Reuters Markets continues to track how quickly these dynamics can shift when institutional sentiment turns.

Disclaimer: This is market commentary, not investment advice

We last reviewed this analysis in May 2026.

Alex Tzoulis

Alex Tzoulis is Co-Owner and Markets Analyst at The Luxury Playbook, specializing in equities, crypto, forex, and global financial markets. His work focuses on analyzing macroeconomic trends, geopolitical developments, and monetary policy, translating them into actionable insights across both traditional and digital asset classes. He leads the platform's financial market coverage, providing structured analysis across stock market investing, trading strategies, and cryptocurrency markets. His expertise strengthens the publication's authority in financial markets and capital allocation, bridging traditional finance with emerging digital investment ecosystems.