India is the most-watched structural growth story in the global wine category today. The market is small (per-capita consumption sits below one litre annually, against China's roughly 1. 2 litres at peak), but the trajectory is meaningful.

India's urban middle class is growing, and so is its appetite for imported wine.

This is our editorial read on whether India can structurally replace China as the major growth market for fine wine through 2030. The honest answer is that it cannot in the short term, but the long arc is more interesting than the headline numbers suggest.

According to OIV and Indian Council for Wine Research data tracked through 2025, India's total wine consumption is roughly 5% of China's at peak. The growth rate matters more than the absolute base.

Key Takeaways & The 5Ws

- India’s demographics and rising middle class make it look like “the next China” for wine on paper, but structural realities make that outcome far from guaranteed.

- If India even reaches a fraction of China’s former per-capita wine consumption, the market could be multiple times larger than today’s $520m–$1bn projections, especially if India also becomes a regional hub.

- Punitive tax structures and state-by-state fragmentation make imported wine three to five times more expensive than in many markets, limiting true mass-market potential.

- Cultural and religious attitudes toward alcohol sharply reduce the addressable population, meaning large parts of India may never become wine consumers regardless of income growth.

- The realistic opportunity is a premium, urban, state-specific strategy, not a copy-paste of the China playbook, so “India as the next China” should be treated as a high-risk, selective bet rather than an inevitability.

- Who is this for?

- Global wine producers, importers, distributors, and alternative-asset investors weighing whether to commit serious capital to India, plus family offices and funds treating India as a long-duration demand story rather than a short-term export target.

- What is the real opportunity?

- A risk–reward case for India versus China’s historical wine trajectory, where upside is demographic-driven but ceilings are set by taxes and regulation, making premium, focused positioning more realistic than mass-market scale.

- When does it matter most?

- From now through roughly 2034, as the middle class expands, tax and trade negotiations evolve, and early movers either entrench brand and distribution or discover that structural barriers cap growth well below China-style scale.

- Where will demand concentrate?

- In more liberal, economically dynamic states and major cities, Mumbai, Delhi, Bengaluru, Goa, parts of Maharashtra, while also watching India’s potential role as a South Asian re-export and education hub serving neighboring markets.

- Why is “India as the next China” risky?

- Because India may be the last enormous untapped wine market on paper, but taxation, regulatory fragmentation, and culture determine the addressable market, so only investors who position state-by-state and premium-first avoid the “India mirage.”

What changed in China, and why India came up

China was the wine category's anchor growth market across the 2010s. From 2010 to 2017, Chinese wine imports grew at roughly 20% compound annual rate, and the category became one of the structural drivers of fine-wine pricing across Bordeaux, Burgundy, and the broader European top tier.

That structural growth has reversed sharply across the past five years. China's wine consumption collapsed roughly 50% from peak by 2024, driven by economic slowdown, real-estate sector weakness, and structural changes in younger-cohort drinking patterns. The category implications across Bordeaux pricing have been profound.

India came up in the post-China conversation because it is the next-largest Asian economy with a growing urban middle class. The structural question is whether India's absolute consumption base can grow fast enough to offset China's structural compression.

India's structural position today

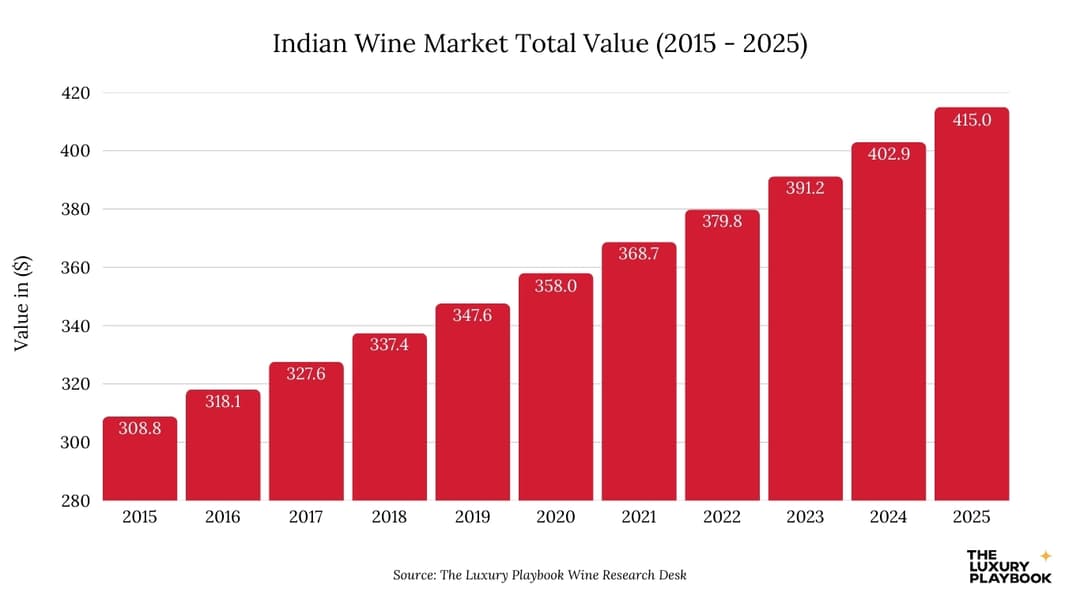

India's wine market sits at roughly 25 to 30 million litres annually, against China's peak of roughly 1. 7 billion litres. The base is two orders of magnitude smaller.

Indian wine consumption growth is running at roughly 15% annually in volume terms across recent years, which compounds meaningfully but does not close the gap to China at peak within the decade.

The structural drivers are real, though. Indian urban middle-class growth is the largest in the world by absolute headcount. Domestic Indian wine production has grown significantly (Sula, Grover, and Fratelli at the named-producer tier), building category familiarity.

And import duty structures, while still high, have been incrementally relaxed.

The named-producer tier of Indian wine consumption (focused on Delhi, Mumbai, Bengaluru, Pune) has shown sustained year-over-year growth across recent years.

The structural challenges for Indian wine market growth

Three structural challenges sit at the centre of why India cannot replace China at the global fine-wine demand level through the rest of the decade. First, the absolute base is small enough that even sustained 15% growth does not produce the volume needed to offset Chinese contraction.

Second, the price-point distribution of Indian wine consumption sits structurally lower than China at peak. Indian middle-class wine consumption clusters at the sub-£15-per-bottle import tier. Chinese consumption at peak supported a meaningful share of the £50-to-£300 import tier that drove fine-wine pricing.

Third, the import duty structure remains a meaningful drag. Indian import duties on wine sit at roughly 150% effective rate after federal and state taxes, against China's 14% baseline at peak. The structural reform of Indian import duties would change the picture meaningfully, but no near-term political pathway exists for that reform.

What this means for serious fine-wine collectors

The named producer tier of fine wine (Bordeaux First Growth, Burgundy named domaine, Champagne prestige cuvée) operates at production volumes where Indian demand growth is not the marginal pricing factor. The structural pricing for Romanée-Conti, Lafite, Dom Pérignon will continue to be set by Anglo-Saxon (US, UK) and Northeast Asian (Hong Kong, Singapore, Japan, South Korea) buyer demand across the rest of the decade.

Indian demand growth is a marginal positive at the named-producer tier rather than the structural anchor that China's growth provided across the 2010s. The category will not see a 2010-to-2017 Chinese-style demand shock from India.

For serious collectors thinking about the broader Asian fine-wine landscape, the structural picture sits across multiple markets simultaneously rather than concentrated in any one country. We have written separately on the factors that shape fine wine prices and quality and on how scarcity and distribution control shape ultra-premium wine positioning.

The Indian fine-wine category as it stands

The named Indian producer tier (Sula's Rasa, Grover Zampa's La Réserve, Fratelli's Sette) is producing wines of legitimate ambition. They will not replace named European producers in serious cellars, but they are building category credibility within India.

The structural import side is more interesting. The named Italian, French, and Spanish producers most positioned to capture Indian middle-class growth are those building specific Indian distribution rather than treating the market as marginal. Penfolds, Concha y Toro, and Antinori have all made meaningful Indian distribution investments in recent years.

The named premium-tier producers (Bordeaux mid-tier, Italian mid-tier) sit in the structurally most-positioned tier for Indian growth through 2030.

The long arc

The structural answer is that India cannot replace China in the global fine-wine demand picture within the rest of this decade. The absolute base is too small, the price-point distribution sits too low, and the import duty structure is too restrictive.

The long arc beyond 2030 is more interesting. If India sustains 15% annual wine consumption growth across the rest of the decade and into the 2030s, the absolute base could reach 50 to 80 million litres by the early 2030s. The category implications for the named-producer middle tier across European wine would be meaningful, even if the named-top-tier dynamics remain anchored elsewhere.

For the broader Asian-market and category context, we have written on wine as an investment category more broadly, which sits alongside the Indian growth story as part of the structural picture for fine wine through 2030.

What we watch next

Three signals will tell us whether the Indian wine market story accelerates or remains a slow build. First, the GST reform and import duty structure changes. Second, the named-producer Indian distribution rollouts from European mid-tier producers.

Third, the per-capita consumption data through the next OIV cycle, particularly across the urban middle-class cohort.

India is not the next China for fine wine. But the structural growth story matters for the broader European mid-tier through the rest of the decade and beyond. Patient collectors and patient producers are positioning for that long arc.

We last reviewed this analysis in May 2026.

Stefanos Moschopoulos

Stefanos Moschopoulos founded The Luxury Playbook in Athens and has spent the better part of a decade following the auction calendar, the en primeur releases, and the watchmakers, gallerists, and shipyards the magazine covers. He writes the field guides and listicles that anchor the Connoisseur section — pieces built on Phillips and Christie's results, Liv-ex movements, and conversations with collectors he has met across Geneva, Bordeaux, Basel, and Monaco. His own collecting habits sit closer to watches and wine than art, and it shows in the level of detail in the magazine's coverage of those categories. Under his direction, The Luxury Playbook now publishes long-form field guides, market-defining year-end listicles, and the Voices interview series with the founders behind the houses and the brands.